What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 9

Geopolitical fractures are regionalizing uranium markets. Western supply deficits through 2028 elevate North American producers as conversion & enrichment bottlenecks deepen.

- The shift from global to regional supply frameworks exposes new structural vulnerabilities in the nuclear fuel cycle, particularly in uranium, conversion, and enrichment.

- North America, Europe, and China face widening uranium supply deficits through 2028, driven by import dependency and geopolitical exclusion of Russian supply.

- Conversion and enrichment bottlenecks are deepening: conversion shortfalls could exceed 8,700 tonnes of uranium by 2028, and North American enrichment capacity covers less than one-third of domestic demand.

- Western policy responses, tariffs, bans, and capacity incentives, are driving capital inflows to domestic projects and allied jurisdictions, reshaping investment risk and opportunity.

- Producers, developers, and explorers like Energy Fuels, enCore Energy, IsoEnergy, Global Atomic, ATHA Energy, American Uranium, F3 Uranium, Laramide resources and Myriad Uranium stand to gain as assets align with security-driven demand.

A New Regional Order in the Nuclear Fuel Cycle

The post-Cold War assumption of a frictionless, globalized nuclear fuel market has eroded. Once-interconnected trade routes are fragmenting into regionally siloed systems, each shaped by geopolitics, sanctions, and energy-security imperatives. Analysts who previously modeled supply-demand balances globally now emphasize regional imbalances through 2024–2028, recognizing that uranium and fuel services can no longer flow freely across borders.

This fragmentation is not hypothetical, it is structural. The United States Prohibiting Russian Uranium Imports Act phases out low-enriched uranium imports by 2027. The United Kingdom has imposed a 35% tariff on Russian enriched uranium, while Canada banned all Russian uranium imports outright. Meanwhile, Group of Seven economies are investing billions to onshore enrichment, conversion, and fuel-fabrication capacity.

For investors, the shift means that jurisdictional safety and domestic supply chains now carry intrinsic valuation premiums. Projects located in permitted, allied jurisdictions, especially those with licensed infrastructure, are increasingly favored by utilities seeking contractual certainty. This sets the stage for the most pronounced regional supply-demand dislocation in decades.

Political Fracture & Policy Response

The nuclear fuel market is uniquely exposed to political currents. Unlike most commodities, trade flows are shaped as much by national-security policy as by price. The Russia-Ukraine conflict crystallized this reality, forcing Western utilities to unwind decades-long dependencies on Russian conversion and enrichment services provided by TENEX and TVEL.

At the same time, United States-China trade tensions have intensified, with Washington suspending export licenses for nuclear equipment suppliers and imposing broad industrial tariffs under the 2025 policy package. Each layer of restriction deepens uncertainty over fuel logistics, as ports, carriers, and customs authorities increasingly delay or deny shipments of radioactive materials, a risk factor previously ignored in financial models.

This policy environment is catalyzing an unprecedented alignment between government mandates and private capital. Western nations are co-funding expansion projects, such as the United States Department of Energy Civil Nuclear Credit Program and Euratom's APIS and SAVE initiatives, which directly target the fuel-fabrication gap left by Russia's exclusion.

Uranium Supply Concentration & the Regional Deficit Reality

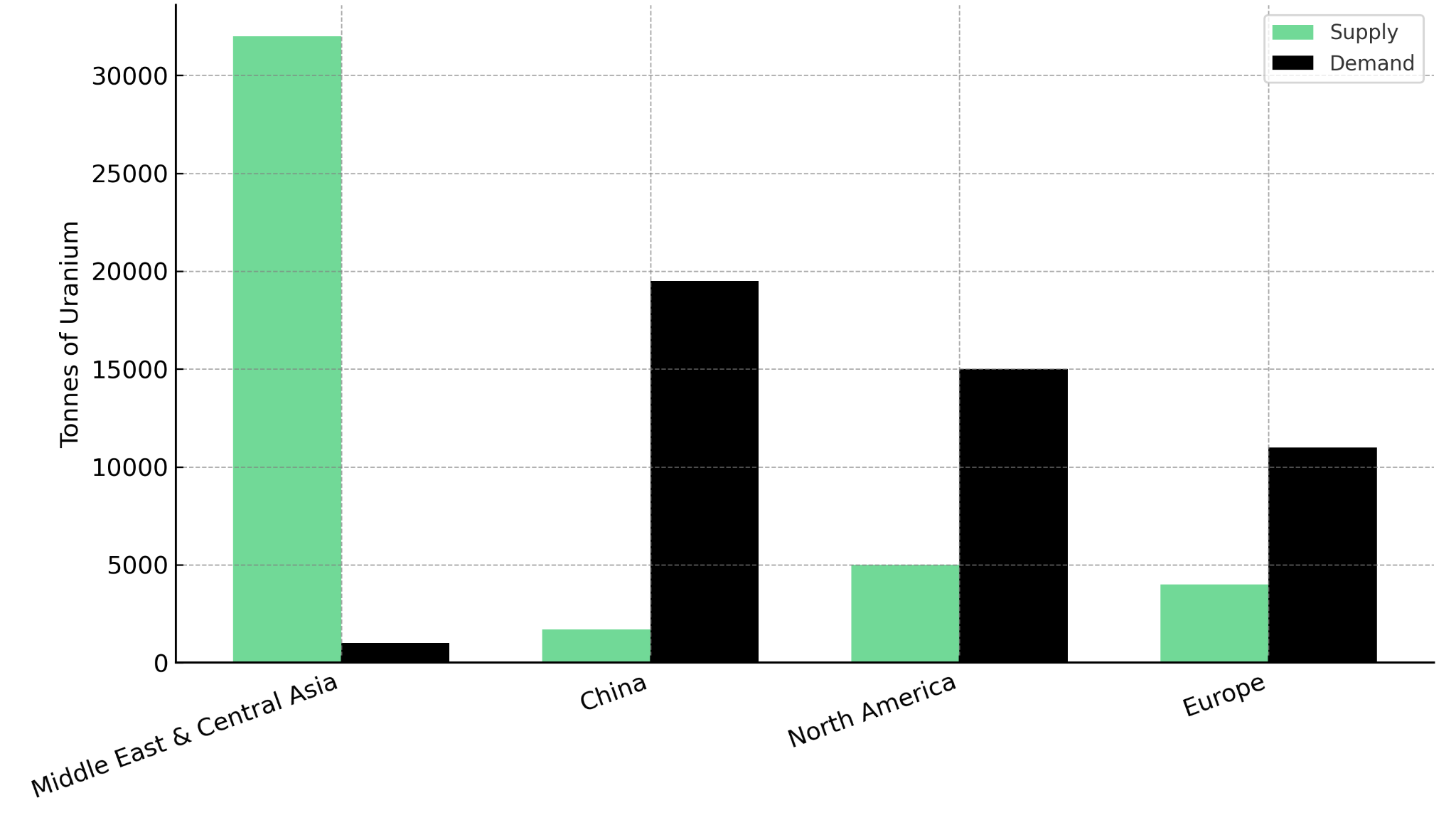

The global uranium landscape remains structurally concentrated. By 2028, the Middle East and Central Asia will produce roughly 32,000 tonnes of uranium, more than any other region, while consuming almost none domestically. In contrast, China, North America, and Europe collectively face deficits exceeding 35,000 tonnes of uranium. China alone requires approximately 19,500 tonnes of uranium in 2028 but produces less than 1,700 tonnes of uranium, a deficit that underscores its accelerating overseas acquisitions.

The ownership mismatch between producer and consumer nations compounds this fragility. Kazatomprom, responsible for over 12,000 tonnes of uranium in 2024, remains a central supplier to global utilities despite Kazakhstan's neutral political stance, a dynamic investors must monitor amid potential sanction escalation.

Jurisdictional Risk & Supply-Chain Security

Events such as the 2023 Niger coup illustrate the volatility embedded in politically exposed jurisdictions. The coup immediately disrupted French utility procurement plans and triggered short-term price spikes, reinforcing the premium on supply from Organisation for Economic Co-operation and Development-aligned regions.

This revaluation benefits developers advancing projects in jurisdictions with established regulatory frameworks. Energy Fuels operates the White Mesa Mill in Utah, which as of 2024 remained the only fully licensed and operating conventional uranium processing facility in the United States. At its high-grade Pinyon Plain Mine in Arizona, Energy Fuels achieved record monthly output at an average grade of 2.14% uranium trioxide, with management projecting sustained low unit costs of approximately $23-30 per pound.

Global Atomic is advancing the Dasa uranium deposit in Niger, which according to the company's feasibility study contains mineral reserves of 73 million pounds of uranium trioxide at an exceptional average reserve grade of 4,113 ppm. The company announced in 2024 that it anticipated closing a 295 million dollar loan supply deal with the United States Development Bank for the project in the first quarter of 2025, with yellowcake deliveries scheduled to begin in the second half of 2026. The company addresses regulatory risk through strong local partnerships and government relations, with community engagement programs ongoing since 2008.

IsoEnergy is advancing the Hurricane deposit in Saskatchewan's Athabasca Basin. According to the company's published technical reports, the Hurricane deposit contains one of the world's highest-grade indicated uranium resources at 34.5% uranium trioxide. The company emerged following the December 2023 acquisition of Consolidated Uranium Incorporated, creating a portfolio spanning the full development spectrum across tier-one mining jurisdictions including Canada, the United States, and Australia. As of June 30, 2025, IsoEnergy maintained cash and equivalents of 84.7 million Canadian dollars, with NexGen Energy maintaining a 30.9% shareholding.

Philip Williams, Director and Chief Executive Officer of IsoEnergy, emphasizes the foundational nature of uranium supply:

"You can have all the conversion capacity in the world, all the enrichment capacity, all the nuclear plants, being coming online or being planned to be built but if you don't have the fuel at the beginning then it's all irrelevant."

Conversion & Enrichment: The New Bottlenecks

Conversion, the process of turning uranium trioxide into uranium hexafluoride, is the first pinch point. Global conversion requirements (64,295 tonnes of uranium in 2024) already exceed nameplate capacity (61,119 tonnes of uranium). By 2028, the shortfall widens to approximately 8,736 tonnes of uranium, assuming perfect operational uptime, a condition never achieved. With Russia's 12,500 tonnes of uranium capacity effectively quarantined from Western markets, available capacity shrinks further.

Regions such as East Asia (excluding China) and South Asia possess no domestic conversion facilities, relying entirely on imports. This dependency exposes them to logistical and political choke points, driving utilities toward long-term fixed-price contracts to mitigate volatility.

Enrichment Concentration & Western Vulnerability

Enrichment dependency is even more severe. Russia's 28.2 million Separative Work Units capacity dwarfs North America's 4.3 million Separative Work Units, against United States demand exceeding 15 million Separative Work Units. Even with expansions at Urenco USA and Centrus Energy, the deficit persists through 2028, underscoring the strategic value of Western enrichment initiatives.

enCore Energy is a leading U.S. uranium producer specializing in In-Situ Recovery (ISR) technology. The company operates two fully licensed ISR processing facilities in South Texas: the Alta Mesa and Rosita Central Processing Plants. Both have a combined current configured capacity of approximately 1.8 million pounds of U₃O₈ per year, and expansion is underway toward full utilization. Alta Mesa, designed for up to 2.0 million pounds annually, is ramping up to full capacity, while Rosita contributes up to 0.8 million pounds per year through its network of satellite ion-exchange facilities. Longer-term growth is supported by the development of the Dewey-Burdock ISR Uranium Project in South Dakota, approved for US Government Fast Track Permitting under the FAST-41 program.

William Sheriff, Founder and Executive Chairman of enCore Energy, underscores the urgency driving domestic production:

"We felt that the sense of urgency was something that needed to be reinforced and the rule of the day actually to deal with this."

Fabrication & the Politics of Acceptability

Fuel-fabrication diversification has evolved from a technical objective into a political mandate. Following the invasion of Ukraine, European utilities sought alternatives to Russia's TVEL for VVER-type reactors. Western fabricators, including Westinghouse and Framatome, are expanding production to meet this demand. Yet the Framatome-TVEL joint venture at Lingen, Germany, illustrates the contradictions of policy versus practicality, demonstrating that energy security often competes with political optics.

For investors, this stage of the fuel cycle is less about capacity growth and more about geopolitical signaling. The projects that secure co-funding under Euratom's APIS and SAVE frameworks will define Europe's fuel independence narrative, indirectly benefitting upstream uranium suppliers positioned within Western regulatory frameworks.

Alignment with Regional Deficits

enCore Energy's existing licensed infrastructure in Texas significantly reduces permitting-related risks, with the company targeting expanded production through the remainder of the decade to align with North American deficit forecasts. Laramide Resources represents a strategic bridge between exploration and near-term production, with a total uranium resource base of 117 million pounds across five projects spanning the United States and Australia. The company's flagship Churchrock ISR Project in New Mexico holds an existing license for up to 3 million pounds per annum of uranium production, with an established resource of 50.8 million pounds of uranium trioxide. According to the company's technical studies, Churchrock is expected to be a low-cost producer, with a pre-tax net present value of 268 million dollars and an internal rate of return of 62% at a uranium price of seventy-five dollars per pound, with life-of-mine post-tax cash flows projected to exceed one billion dollars.

Exploration Optionality

ATHA Energy and F3 Uranium extend discovery pipelines in the Athabasca Basin, ensuring future high-grade supply for Western utilities. ATHA Energy holds one of the largest exploration portfolios in Canada's premier uranium jurisdictions, with a fully funded 10,000-meter diamond drill program planned for 2025 at the Angilak Project. The company's 2024 exploration program at Angilak achieved a 100% hit rate for intersection of uranium mineralization. The Angilak Project has a historical resource estimate of 43.3 million pounds of uranium trioxide at an average grade of 0.69%, with a conceptual exploration target at the Lac 50 Deposit ranging between 60.8 million pounds and 98.2 million pounds of uranium trioxide.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, characterizes the current supply opportunity:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career. The sentiment of the real demand that's being built up coupled with some of the supply side risk is a structural setup like we have not seen in the uranium space."

F3 Uranium is focused on advancing high-grade uranium discoveries in the Athabasca Basin. The flagship Patterson Lake North Project hosts the JR Zone, with the leadership team having been responsible for multiple major uranium discoveries. Denison Mines' 15 million dollar strategic investment in 2024 provides strong validation of F3's potential. As of October 2025, the company reported a total cash on hand of over 28 million dollars.

Scalable United States Exploration Projects

American Uranium and Myriad Uranium represent scalable In-Situ Recovery and open-pit potential in Wyoming's historic uranium belt, critical for domestic resource replacement. American Uranium's Lo Herma project in Wyoming contains a current JORC indicated and inferred mineral resource of 8.57 million pounds of uranium trioxide, located just 10 miles from Cameco's Smith Ranch-Highland facility (the largest ISR uranium plant in the United States). The company targets low-cost ISR production with typical all-in sustaining costs in the region at US$35-$40 per pound. Wyoming operates as one of only four self-regulating United States Agreement States for uranium mining and has a well-established permitting process for ISR projects dating to the 1970s.

Myriad Uranium has consolidated ownership at the Copper Mountain Project in Wyoming, marking the first time in over fifty years that the district has been under unified control. Historical United States Department of Energy estimates from 1983 suggested the Copper Mountain Project contained a potential mineral endowment of approximately 245 million pounds of uranium oxide down to 600 feet. The company received federal approval for a 222-borehole exploration program, with initial drilling validating historical work and returning a best grade interval measuring 5,337 parts per million uranium oxide over 1.28 meters.

The Investment Thesis for Uranium

- Regional deficits drive premium pricing. Structural imbalances, especially in North America and Europe, support long-term uranium price resilience as supply constraints persist through 2028.

- Policy support enhances capital flow. Western mandates for nuclear independence and decarbonization continue to underwrite demand growth and project financing, with programs such as the United States Department of Energy Civil Nuclear Credit Program allocating over two billion dollars toward domestic uranium enrichment and fuel cycle projects.

- Jurisdictional safety becomes a valuation metric. Investors are rewarding companies operating in politically stable mining regions with established regulatory frameworks, particularly in North America and Canada's Athabasca Basin.

- Fuel-cycle bottlenecks create multiplier effects. Shortfalls in conversion and enrichment magnify the value of upstream feedstock security, benefitting producers with near-term output capacity in allied jurisdictions.

- Companies with liquidity, permitted infrastructure, and proven management, such as Energy Fuels, enCore Energy, Laramide Resources, and IsoEnergy, are placed to capture the regional repricing trend as utilities prioritize traceable, sanction-free supply chains.

Regionalization Redefines Value

The nuclear sector's evolution from globalization to regionalization marks a paradigm shift in how investors must assess risk and value. As geopolitical fragmentation reshapes trade flows, the premium for secure, transparent, and politically aligned uranium supply continues to rise. The new market reality is not one of uniform scarcity but of asymmetric access, where availability depends on alliance networks as much as geology.

For investors, the implication is clear: the next phase of uranium investment will reward those positioned at the intersection of security, jurisdictional integrity, and operational readiness. In this environment, the advantage tilts toward producers and developers in North America, Canada, and Australia, regions that will define the new equilibrium of the nuclear fuel market.

Read more:

Part 8 - Fuel Fabrication Supply and Demand

Part 7 - Fuel Fabrication Supply and Demand

Part 6 - Conversion Supply and Demand

Part 5 - Uranium Supply and Demand

Part 2 - Nuclear Energy Security Imperatives

TL;DR

The global nuclear fuel market is fragmenting into regional systems as sanctions, trade restrictions, and energy security mandates disrupt traditional supply routes. North America, Europe, and China face widening uranium deficits through 2028, while conversion shortfalls approach 8,700 tonnes and enrichment capacity gaps persist. Western policies—including the U.S. ban on Russian uranium imports and G7 capacity incentives—are redirecting capital toward domestic and allied producers. This structural shift creates valuation premiums for companies with permitted infrastructure in stable jurisdictions. Energy Fuels, enCore Energy, Laramide Resources, IsoEnergy, Global Atomic, ATHA Energy, and American Uranium are positioned to benefit as utilities prioritize traceable, sanction-free supply chains over traditional cost considerations in an increasingly balkanized market.

FAQs (AI-Generated)

The uranium market is fragmenting due to geopolitical tensions, particularly the Russia-Ukraine conflict and U.S.-China trade disputes. Western nations have imposed sanctions and import bans on Russian uranium, conversion, and enrichment services, forcing utilities to source from allied jurisdictions. The U.S. Prohibiting Russian Uranium Imports Act phases out Russian LEU by 2027, while Canada has banned all Russian uranium imports. These policy actions, combined with denial and delay of radioactive material shipments at ports, have created regional silos where supply can no longer flow freely across borders. Energy security has replaced cost optimization as the primary procurement driver.

Conversion transforms mined uranium (U₃O₈) into uranium hexafluoride (UF₆), while enrichment increases the concentration of U-235 isotopes to reactor-grade levels. Global conversion requirements exceed capacity by 2028, with an 8,736-tonne deficit projected even assuming perfect uptime. North American enrichment capacity (4.3M SWU) covers less than one-third of U.S. demand (15M+ SWU), creating heavy reliance on imports. These bottlenecks create a multiplier effect—constrained conversion and enrichment capacity magnifies demand for uranium feedstock from allied producers. Utilities must secure entire fuel-cycle supply chains, not just uranium, making producers in Western jurisdictions strategically valuable regardless of mining costs.

Companies with permitted infrastructure in stable jurisdictions offer the highest strategic value. Energy Fuels operates the only fully licensed conventional uranium mill in the U.S. and holds the largest domestic resource base. enCore Energy and Laramide Resources hold existing production licenses enabling rapid response to utility demand, with Laramide's Churchrock project licensed for 3 million pounds annually. IsoEnergy's Hurricane deposit (34.5% U₃O₈) represents one of the world's highest-grade resources in Canada's Athabasca Basin. Global Atomic's Dasa project in Niger offers the highest-grade deposit outside the Athabasca Basin (4,113 ppm), with production scheduled for H2 2026 despite jurisdictional challenges. Explorers ATHA Energy and F3 Uranium ensure future pipeline supply from tier-one Canadian jurisdictions.

North America, Europe, and China collectively face uranium deficits exceeding 35,000 tonnes through 2028. China alone requires ~19,500 tonnes but produces less than 1,700 tonnes domestically. North America's requirements exceed domestic production by approximately 15%, while Europe produces only 180 tonnes against demand of 15,296 tonnes. These deficits persist despite Middle East/Central Asia producing 32,000 tonnes—geopolitical barriers prevent this surplus from flowing freely to Western markets. The structural imbalance is worsening: global uranium requirements increase 17% from 2024-2028, while capacity grows only 7%. With Russian supply (historically ~35-40% of Western enrichment services) now restricted, Western utilities face acute shortages that cannot be resolved through spot market purchases alone.

The U.S. Department of Energy's Civil Nuclear Credit Program has allocated over $2 billion toward domestic enrichment and fuel-cycle projects. The Prohibiting Russian Uranium Imports Act creates guaranteed demand for Western supply through 2027 phase-out timelines. G7 nations have committed to expanding domestic conversion, enrichment, and fabrication capacity through coordinated initiatives. Euratom's APIS and SAVE programs (€10M each) fund Western fuel fabrication alternatives to Russian TVEL. President Trump's 2025 executive order explicitly includes uranium in critical minerals definitions, accelerating permitting for domestic projects. Canada's ban on Russian uranium imports and the UK's 35% tariff on Russian enriched uranium further segment markets. These policies create structural demand for Western producers independent of uranium price fluctuations, fundamentally altering investment risk-return profiles.

Analyst's Notes

Subscribe to Our Channel

Stay Informed