Paladin Energy (PDN) - Uranium Poster Boy Getting Ready

Paladin is focused on Langer Heinrich and engaging with the utility market. It will produce 6Mlbs uranium during its mining phase of 7yrs,

Paladin Energy was the darling of the last boom & bust uranium cycle. Many promoters and brokers point back to the highs that Paladin achieved as an example of where their current uranium stories will go. Only 2 companies actually got into production in that cycle, despite there being c.500 'uranium' companies. We hope investors do their homework and look at the uranium macro and the business fundamentals for their uranium investments.

Ian Purdy joined Paladin Energy in Feb 2020, and has been focused on getting Paladin ready to bring Langer Heinrich back into production, it having gone into care & maintenance in 2018 when prices fell to unsustainable prices.

Paladin is focused on Langer Heinrich and engaging with the utility market. It will produce 6Mlbs during its mining phase of 7yrs, and then they will work their way through the lower-grade, lower-volumes stockpile.

We talk to Purdy about exploration and also the other assets in Australia and Canada. The indication is that these are not core and no money will be spent developing these. The CNNC relationship comes into scrutiny in the market so we look at the implications of how these 25% shareholder actions affect future decisions.

Company Overview

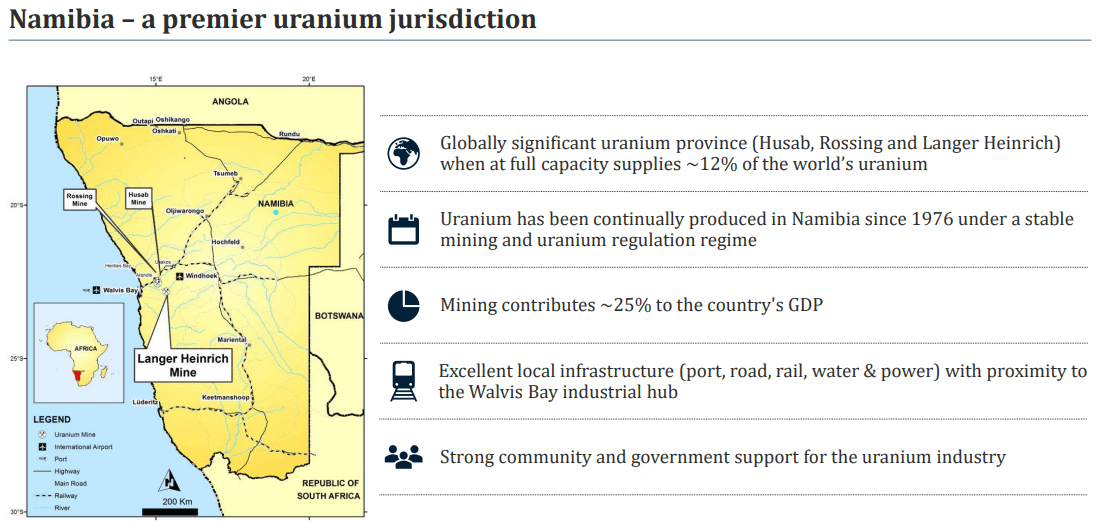

Paladin Energy is a Uranium miner and a producer with an operation in Namibia, the Langer Heinrich mine, which they look to bring back into production as the Uranium prices start to improve. They also have some exploration land and tenements in Australia and Canada but at the moment they're totally focused on the Langer Heinrich mine in Namibia.

History Repeating: On Cycles, Juniors, & Catalysts

Paladin was the darling. It was the poster boy of the last Uranium cycle, but do they look back to the last cycle and think, well we'll just have the same again, or do they think there were lessons learned?

There are a lot of similarities in the market side to the last Uranium boom, and Paladin Energy has a good history and heritage so they now have a great opportunity based on their hard work in the last cycle and they have Langer Heinrich as their focus in their portfolio.

The last decade has been a tough time for all Uranium producers, from the largest in the market through to the juniors who are aspirational producers. The downturn has gone longer and harder than everyone expected, but now we're starting to see the market in its recovery phase at last.

The Uranium market is quite a difficult market to predict. It is quite opaque, and small by global standards. It's defined by confidential contracts between individual producers and suppliers, and utilities. But there is confidence at the moment as Uranium market analysts are indicating a return to the term market. Utilities, particularly in the US, are returning to the term market for the first time in close to a decade, which is great news for the uranium industry.

Business Plan & Focus: Time to Restart & Explore

Purdy joined Paladin Energy in February 2020 following a 2-year period where Paladin shut down because the price in the market wasn't what they needed it to be. Now the primary focus of the company is to move forward with the restart plan of Langer Heinrich. They have really focussed on the commercial side of the plan as their top priority is to reduce expenditure to protect their very strong cash flow. Their focus as a company is solely on Langer Heinrich and they have put all their resources into the 1 asset. They have also spent a lot of time re-engaging with the customers and the utility market and with their shareholders, noteholders and other supporters.

The restart plan suggests that they can produce at a rate of about 6Mlbs per annum during the mining phase, which runs for 7-years. The ramp-up schedule is very quick, being a well-known brownfield operation and they're not making any major changes to the process flow, which worked very well. They're also going to be using the same mining method, which worked very well and expect to be back to full production within 12-months of a restart, and then at 6Mlbs for 7-years, followed by a further 9-years at about 3.5Mlbs when they move to the lower-grade material.

There are lots of exploration opportunities both within their own tenements but also within the Namibian region they’re operating in, on the west coast. It's a very long established Uranium jurisdiction and there are some very good regional opportunities as well as opportunities on Paladin tenements.

Relationship with CNNC

CNNC came on board as a partner to the operation in 2014 and as part of their acquisition of their 25%, which they paid about AUD$190M for, they also put in place an off-take agreement for up to 25% of the production. Paladin likes the off-take because it gives them market exposure and is predominantly priced at spot price. They have a very constructive relationship with CNNC, but it is unclear if CNNC will meet their 25% commitment and obligations.

Timing & Price Incentive

Paladin Energy is looking for an improvement in pricing before they restart and given that they aim to be in production for another seventeen-years, want to make sure they’re successful in the restart. They will be looking for a price that covers not only all of their cash costs, their corporate costs, but also allows them to put in place an appropriate debt-servicing structure, and also make a return for their shareholders.

When you look at the economics of the mine, somewhere between AUD$50 and AUD$60 is a price which would encourage Paladin to restart. The actual number itself will depend on the off-take, the duration, the volume, the credit rating and other factors. AUD$40 doesn't do it, AUD$50 is really interesting and beyond would be fantastic Says Purdy.

All About Debt & Royalties

As part of the restructure, Paladin Energy had some noteholders, and convertible noteholders, who'd been with the company for a long period of time. They converted all of their debt into equity and then they stumped up another AUD$115M to get the company back on its feet. The debt structure they put in place was a very benign structure which they are benefitting from at the moment. They plan to restructure the debt at the restart.

U04 & U308, What's the Difference?

The main focus on the product drying and packaging upgrade is occupational health and safety, and reliability. The old process at Langer Heinrich was very manual and a hazardous environment for employees to be in so they are looking at automating the back end using the same technology as the Husab mining operation. They will then have the flexibility to improve their product specs and will be able to take more moisture out of the product, which will not only make it easier to process at the converters but will also remove some of the logistics costs.

Preparing for the Restart: Team Experience

Paladin Energy is fortunate to be in a mining jurisdiction in Namibia that specialises in Uranium and so have attracted extremely good capability. They've just employed a very good metallurgist from one of their neighbouring operations and have very good mechanical, environmental, human resources, and legal teams. Langer Heinrich was regarded as a very good employer and an employer of choice in the region, and as they have 2 neighbouring operating Uranium mines are very confident they will be able to attract the skills for their operations.

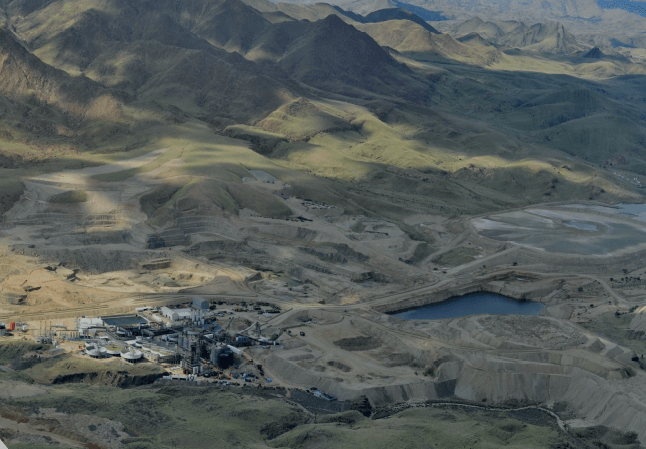

Langer Heinrich Mine: Plan, Timeline, Costs

Langer Heinrich is a conventional Uranium operation with a very simple open-pit mine which has mined successfully for 10-years previously. Once they restart, they have another seven-years in the mine plan, where they will be mining high-grade material. Conventional, some free dig but mainly drill and blast, load and haul. The ore is then taken to where it's fed into an alkaline leach process. It’s a very conventional, proven process flow to produce Uranium concentrate. That's all done on site most likely with contract mining, which has worked very well for Paladin previously in Namibia. Then, the Paladin workforce will run the processing plant and will ship the product out of the deep-water port very close to Swakopmund in Walvis Bay.

Across the life of the operation, their C1 cash cost is circa AUD$27lb and the all in cost is in the mid-30s.

Paladin Energy is taking a very disciplined approach and will not be restarting ahead of starting contracts. So whilst they're very well advanced with their restart plan, they're fully licensed, and have a very detailed schedule to bring the operation back into production, they will not be committing to any expenditure or capital works until they've signed on long-term off-take.

An Update on Australian & Canadian Assets

The Australian and Canadian Assets are very good prospective projects but are at an early stage and have been parked and put on care and maintenance for the moment whilst Paladin concentrates on the Langer Heinrich mine.

The sequence for Paladin Energy is the restart of Langer Heinrich, achieve cash flow positive operations, full production, and then immediately turn attention to their in house projects as well as M&A.

Paladin Energy plans to hold onto their exploration assets at this stage and have rationalised the landholding to the point where they've kept the best and minimised the holding costs.

Mining in Namibia at Present

Paladin Energy has restructured their project team because of the Covid travel restrictions. They've relocated a large proportion of the project at the operation in Namibia, and recruited some new expertise. The team in Namibia is very focused on the plant as it's built today, and the conditioning work to return the plant to full capability. They’ve also done a lot of work on the licensing and renewed their environmental license for another 3-years. The Namibian team is taking a lead in country around everything that's there and are being supported out of South Africa and Australia on the engineering of the new bits of the plant being brought in to improve the mechanical reliability. Between the 2 teams, it's working well and they're making progress as expected pre-Covid. The team in Namibia is responsible for maintaining the plant in care and maintenance.

Paladin Energy has just over AUD$30M in cash and they are not under pressure from anyone to get restarted, but have imposed their own regime in looking for those long-term contracts. So have no other obstacles in their way.

To find out more, go to the Paladin Energy Website.

Analyst's Notes

Subscribe to Our Channel

Stay Informed