Palladium One (PDM) - What Retail Investors Need to know

Matthew Gordon spoke with Derrick Weyrauch, President and CEO of Palladium One Mining to discuss the global Palladium market, especially in the light of the currently planned sanctions against Russia.

Palladium may be seen as an unsung hero in the fight against climate change. The metal is a crucial component of catalytic converters in internal combustion vehicles and is almost primarily consumed by the global automotive market. We spoke with Derrick Weyrauch, the President and CEO of Palladium One Mining Inc, an experienced mining executive and corporate director to better understand the global palladium market and give potential investors insight into this small yet critical mineral industry.

Matthew Gordon spoke with Derrick Weyrauch, President and CEO of Palladium One Mining (TSX-V: PDM) to discuss the global Palladium market, especially in the light of the currently planned sanctions against Russia.

Company Overview

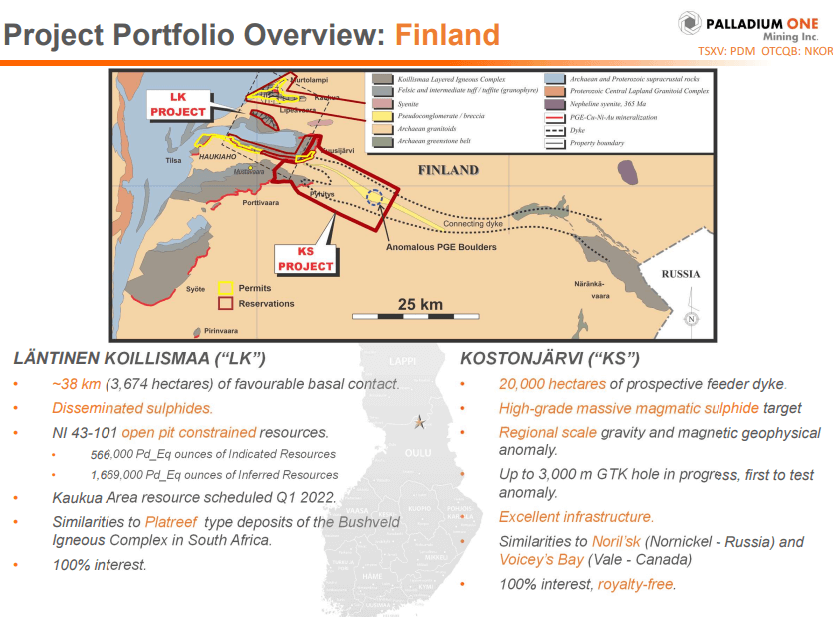

Palladium One Mining Inc. is a Platinum Group Element (PGE) green energy metals focused company operating in tier 1 jurisdictions. The company boasts a highly experienced management team, with its assets consisting of the Läntinen Koillismaa (LK) project in north-central Finland and the Tyko Property located near Ontario Canada.

The Palladium Market

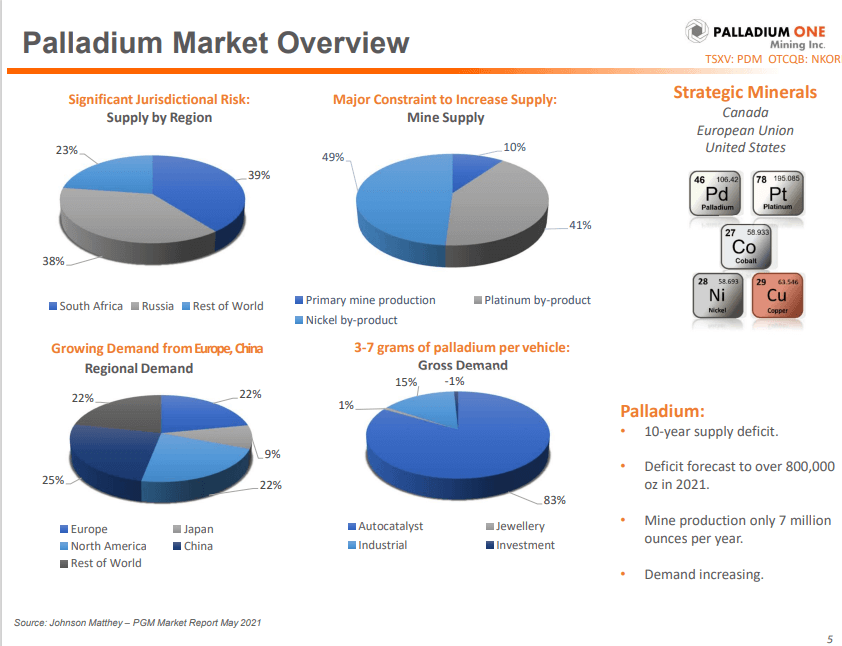

The global Palladium market is small when compared to other mineral markets, with the amount produced globally per annum being only 7 million ounces, approximately 200 tons. In 2021 the global palladium industry was worth approximately USD$ 18.6 billion which comprised 200 tons at an average price of USD$ 2,600 per ounce.

The global palladium market is primarily controlled by Russia and South Africa, which are each responsible for 40% of the world’s palladium supply. Weyrauch explains the market as follows:

“What’s really interesting about the palladium market is it’s only about a 7Moz mined production profile, so it’s actually quite small, and just under 40% of that comes from Russia and is obviously at risk of sanctions, but there’s another roughly 40% that comes from South Africa, another challenged jurisdiction. The whole issue of security of supply is a very hot topic and we’ve seen that translate into the commodity price.”

Palladium is a crucial part of emission control devices fitted to cars and trucks ensuring that the discharged exhaust fumes of the vehicles are environmentally compliant.

The international community fears that due to planned and currently imposed sanctions against Russia, 40% of the worldwide palladium supply may vanish. Weyrauch however believes that the international community will not impose sanctions regarding palladium against Russia until such a time that an alternative source of supply is found. He explains:

“Palladium for the most part is used in the automotive catalytic converter for the gas engine. … If you turn off 40% of the supply, how are you going to see the environmental standards that are required to put vehicles on the road? I’m not 100% sure that we’re going to see the supply cut off until there are alternate sources of supply.”

The sanctions according to Weyrauch will in all probability also not be very effective, he believes that should sanctions be imposed against Russia that prohibit the country from supplying palladium to the international market, China may step in and buy the palladium at a discount from where it may then supply the international community.

The automotive sector has been searching for alternatives to palladium since 2014 when the South African mineral sector was plagued with workforce strikes. The strikes resulted in a price escalation globally as the international community became aware of the scarcity of the metal. Weyrauch notes that since this time the spot price of palladium has increased per annum:

“…because of the shocks that the market has had since 2014 when the South Africans had strikes and started to cause a huge escalation in the price of palladium that has caused the spot price to increase year over year.”

The automotive industry has investigated replacing palladium with platinum, but due to the inherent chemical differences between palladium and platinum, the replacement was found to be not viable unless major changes are made to the automotive exhaust systems. The implementation of platinum would also require the incorporation of rhodium into the catalytic converters which also affects the price differential. He states:

“The chemical properties of palladium and platinum are different. Palladium performs much, much better and it’s not just that particular element. You’re also dealing with rhodium. While you could substitute a palladium-based catalytic converter for one that’s platinum, you’re also going to bring along more loading of platinum, and you’re also going to be bringing in very expensive rhodium, which I think today is trading at incredibly high levels.

Weyrauch explains that the substitution of palladium would entail various technical changes that would include the redesign of the exhaust systems of cars and trucks. Platinum also tends to sinter which results in a short lifespan for the platinum catalyst and it not adhering to stringent driving emission standards. He states:

“…with the more stringent regulatory standards that have come about over the last 10-years is this concept of a real driving emission standard, and that requires the catalytic converter to perform as new 10-years into its lifecycle. When you’re using platinum, for example, it has a tendency to sinter and doesn’t have the same lifespan if it gets too hot. I think there are some real technical issues that can be addressed. Certainly, there can be some substitution, but how far it’s going to go is a question, and as you’ve also pointed out, redesigning the car.”

Palladium price volatility, production and stressors

The price of palladium has been highly volatile since the start of the geopolitical situation unfolding in Ukraine. Weyrauch states that it is not only the situation between Russia and Ukraine that will contribute to the future volatility in palladium prices but also the political instability of South Africa. Weyrauch states:

“There are other stressors as well when we’re talking about the security of supply, it’s not necessarily just the sanctions that might come on Russia, but we’ve had lots of conversations over the last 5-years or so about the lack of reinvestment into the South African mines. There are expectations of lower production”

Palladium is primarily produced as a by-product at other mining operations, often at sulphide nickel and platinum operations. The constraint palladium producers face with regards to increasing their palladium production is that it may affect their primary products. He states:

“existing producers are constrained from increasing their activities to supply more palladium because it’s going to affect their primary products. There’s a huge constraint there on the supply side of things, and because of that as we see increasing demand due to regulation or changing buying patterns…”

Palladium demand in the future

The worldwide effort to move to more eco-friendly forms of transport such as electric vehicles (EVs) may affect the palladium sector, but not to such a severe extent as anticipated. Weyrauch believes that the infrastructure and raw materials required to support the construction and charging of EVs is lacking, with various parties beginning to question the validity of EV implementation forecasts. He states:

“We've seen a lot of conversations with governments and automakers saying, ‘We’re going to go purely electric by such and such a date.’ The more sophisticated parties that we talk to in terms of institutions appreciate the supply and demand fundamentals for not just the nickel and the palladium that we’re talking about, but also the copper and the lack of charging infrastructure, and the loading of these metals that would be required in one vehicle.

Weyrauch believes that due to the lacking infrastructure it is much more likely that hybrid vehicles, vehicles that are powered by an internal combustion engine and an electric motor, will become more prominent as the required infrastructure is constructed.

The amount of palladium required for the catalytic convertor of a hybrid vehicle is traditionally more than required for an internal combustion engine. The amount of palladium used in the catalytic convertor of a hybrid can be between 2 to 2.5 more than that of a traditional automobile.

He states:

“…what I think is going to happen, is we’re going to see the hybrid vehicle that still has a very small share of the market grow quicker perhaps than the pure electric vehicle. That hybrid vehicle still uses an internal combustion engine, and because it operates differently, it actually has more loading than you would in a conventional vehicle. What we’ve seen out of China is 2 to 2.5 times the PGEs going into the catalytic converter for the hybrid electric versus the conventional. So, that’s actually positive for demand. It could cause that much more disruption should that transportation mode continue to accelerate its sales percentage.

The palladium industry's future

The development of new projects into producing assets is a challenge for all minerals sectors, but even more so for palladium. Weyrauch states that due to palladium primarily being a by-product, not enough new palladium supply is entering the market to meet the deficits seen. The platinum and nickel mining sector is not expanding fast enough to be able to supply palladium as a by-product, Weyrauch explains:

“…there aren’t that many pure-play palladium producers or primary products being palladium - they just don’t exist. Palladium tends to be in a polymetallic situation where you’ve got a number of metals just as we do, and as I said earlier, it’s often a by-product of sulphide nickel mining. We’re not seeing additional sulphide nickel projects coming online either. That’s 40% of the supply. We’ve got the palladium, or rather the platinum miners as well where, again, palladium is a by-product but we’re not seeing a lot of new supply on the platinum side”

The solution according to Weyrauch is dedicated palladium mining operations in secure jurisdictions, he states:

“…we need to get supply from safe and secure jurisdictions that have a good rule of law, we need to build mines that are palladium dominant, given most of the palladium supply globally is a by-product. 90% is a by-product of nickel and platinum mining.”

Palladium One’s part to play

Palladium One Mining Inc. is well positioned to be able to supply to the global palladium market in the future. The palladium dominant Läntinen Koillismaa (LK) project of the company is located in north-central Finland and boasts a mineral resource estimate of 635,600 palladium equivalent ounces in the indicated category and 525,800 palladium equivalent ounces in the Inferred category.

Weyrauch believes that due to the global palladium shortage and the geopolitical factors at play, the rate of advancement regarding palladium operations may be expedited.

“I don’t see red tape being cut down, but what I do suspect is going to happen is that there are going to be accelerated timeframes for making decisions. If something had previously taken, let's call it 6-months to make a decision on an issue, perhaps additional efforts are going to be put in place to have it happen in 3-months.”

The current palladium supply shortage, the geopolitical situation unfolding in Ukraine, the unstable mining sector of South Africa and the shortage of necessary infrastructure and raw material for EVs all contribute to the large potential of pure-play palladium mining operations such as the LK project of Palladium One Mining Inc.

To find out more, go to the Palladium One Mining website

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed