Perseus Mining: Resilient Growth in West Africa Amid Rising Costs & Capital Discipline

Perseus Mining demonstrates resilient growth in West Africa with cost discipline, strong cash position, and diversified operations amid sector headwinds.

- Gold’s macro positioning as an inflation hedge has strengthened, but operational cost inflation, FX volatility, and regulatory pressures complicate producer margins.

- Despite rising All-In Sustaining Costs (AISC) globally, select producers are maintaining production guidance while investing in long-life, low-cost projects

- Perseus Mining exemplifies cost resilience and growth discipline, with a strong balance sheet, project visibility, and jurisdictional diversification across West Africa

- Investors are recalibrating expectations for gold equities, focusing on cash margins, operational execution, and jurisdictional optionality

- Near-term milestones like CMA underground permitting and Nyanzaga execution position Perseus as a credible case study in strategic growth during uncertain cycles

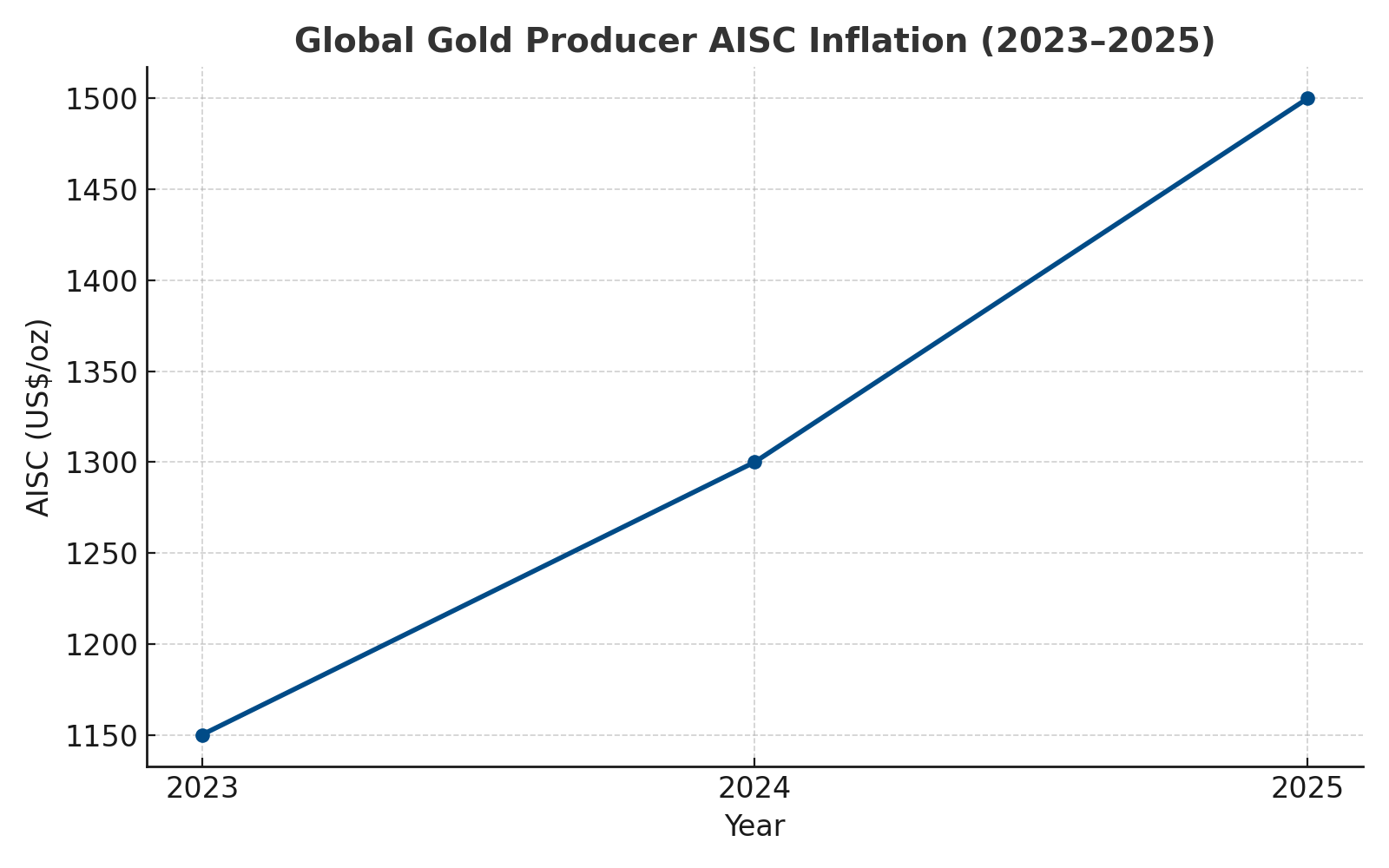

AISC Inflation Squeezes Global Gold Margins

The global gold mining sector faces unprecedented cost pressures as All-In Sustaining Costs continue their upward trajectory. According to World Gold Council data, average AISC across major producers has increased by approximately 15-20% over the past two years, driven primarily by fuel price volatility, labour cost inflation, and escalating royalty obligations tied to higher gold prices.

Foreign exchange dynamics have created additional margin compression across key producing jurisdictions. West African operations, particularly in Ghana and Côte d'Ivoire, have experienced currency headwinds as local currencies strengthen against the US dollar, effectively reducing the local currency value of gold sales while operational costs remain denominated in local terms.

Perseus Mining's fourth quarter FY25 performance demonstrates both the challenges and the company's relative resilience within this environment. The company reported AISC of US$1,417 per ounce for the quarter, representing a 17% quarter-over-quarter increase but remaining within 5% of analyst estimates. This performance occurred despite increased sustaining capital expenditure at Yaouré associated with tailings facility expansion works and higher royalty payments aligned with elevated gold prices.

Navigating Inflation: Capex Discipline vs Growth Aspirations

The industry's response to cost inflation has bifurcated between companies pursuing growth at any cost and those implementing disciplined capital deployment strategies. Perseus represents the latter approach, having beaten full-year FY25 cost guidance at US$1,235 per ounce despite challenging operating conditions.

The company's FY26 guidance of 400-440 thousand ounces at AISC of US$1,460-1,620 per ounce reflects a strategic approach to capital investment. This guidance incorporates US$450 million in growth capital expenditure, split between CMA Underground development (US$80 million), Edikan capitalised waste stripping (US$20 million), and Nyanzaga development capital expenditure (US$340 million).

Chief Executive Officer Jeff Quartermaine's strategic philosophy emphasises cash generation over production volume metrics:

“Our priority is to maximize cash production. In extending mine life, we’ve focused on maintaining the right balance between scale, cost, and margin.”

Central Banks Anchor Gold in Capital Cycle

Gold's fundamental positioning has strengthened amid persistent negative real interest rates and sustained central bank accumulation. International Monetary Fund projections indicate continued monetary accommodation across major economies, supporting gold's role as an inflation hedge and store of value.

Central bank gold purchases reached near-record levels in 2024, according to World Gold Council data, with emerging market monetary authorities continuing to diversify reserves away from traditional fiat currencies. This structural demand has provided price stability even as Exchange-Traded Fund flows have shown periodic volatility.

For gold producers, this macro backdrop emphasises the importance of margin stability over pure production growth. Companies demonstrating consistent cash generation capabilities are commanding premium valuations as institutional investors prioritise operational execution over development-stage expansion narratives.

Equity Market Behaviour & Discounting of Development Risk

Institutional investor fatigue around high-cost gold developers has created a marked preference for near-term cash flow visibility and reduced technical or geopolitical risk exposure. Perseus benefits from this shift through its robust balance sheet position of US$827 million in cash and bullion with no debt, complemented by an undrawn US$300 million revolving credit facility.

The company's Nyanzaga project represents a compelling development opportunity with forecast AISC of US$1,230-1,330 per ounce, positioning it among the lowest-cost development projects globally. This cost structure, combined with Perseus's self-funding capability for the estimated US$520 million capital requirement, distinguishes the company within the development-stage investment universe.

West Africa Demands Jurisdictional Diversification

West African gold mining jurisdictions present a complex risk-reward profile that demands sophisticated operational and political engagement strategies. Recent geopolitical events across the region, including military coups and evolving fiscal regimes, have created risk premiums for companies operating within these markets.

Perseus Chief Executive Officer Jeff Quartermain acknowledges these challenges while emphasising the necessity of adaptation:

“With youth populations rising fast, host governments are under pressure to fund education and employment, making increased taxation of miners an inevitable policy lever.”

Despite these challenges, West African jurisdictions offer compelling operational advantages including strong local labour pools, lower capital expenditure intensity compared to developed markets, and historically shorter permitting timelines for expansion projects.

Perseus as a Case in Jurisdictional Spread

Perseus's operational footprint spans Ghana (Edikan mine) and Côte d'Ivoire (Sissingué and Yaouré mines), with development exposure in Tanzania through the Nyanzaga project. This geographic diversification provides strategic insurance against jurisdiction-specific risks while maintaining exposure to the region's geological prospectivity.

The planned CMA Underground development at Yaouré represents Côte d'Ivoire's first underground mining operation, demonstrating Perseus's technical confidence and commitment to long-term jurisdictional engagement. The project awaits final government approval, which management expects imminently.

Perseus maintains pipeline optionality through its 17.8% stake in Predictive Discovery, providing exposure to additional West African development projects without direct operational risk. This strategic equity position has doubled in value since the initial investment, now worth approximately US$140 million.

Self-Funded Growth in Cost-Sensitive Era

Perseus's capital allocation framework prioritises shareholder value preservation while funding organic growth opportunities. The company's US$450 million FY26 capital expenditure program will be entirely internally funded, avoiding equity dilution during a challenging market environment for gold equity fundraising.

Shareholder value preservation extends beyond project funding through active capital return initiatives. Perseus has executed US$73 million of a US$100 million share buyback program, with completion targeted for September 2025. This approach demonstrates management's confidence in the company's intrinsic value while providing tangible returns to shareholders.

The company maintains a target cash margin of US$500 per ounce at a long-term gold price assumption of US$2,400 per ounce, ensuring robust cash generation capabilities across various gold price scenarios. This conservative approach to financial planning provides downside protection while preserving upside exposure to higher gold prices.

Development Readiness & Permitting Visibility

Perseus's development pipeline benefits from advanced permitting status and construction readiness across both major projects. The Nyanzaga project maintains its timeline for first gold production in January 2027, with the Framework and Shareholder Agreement execution scheduled for completion this quarter.

The approach reflects Perseus's operational expertise and cost consciousness. Rather than employing traditional Engineering, Procurement, and Construction contracts, Perseus has adopted an Engineering and Construction approach while managing procurement internally:

"Perseus already has all of its processes in place for local procurement and local employment."

CMA Underground development at Yaouré awaits final government approval, with Chief Executive Officer Jeff Quartermain expressing confidence in near-term resolution. The project represents a natural extension of existing infrastructure, minimising execution risk while providing substantial production augmentation.

Strategic Hedging Buffers Volatile Cycles

Perseus employs a sophisticated hedging strategy designed to provide downside protection while maintaining upside gold price exposure. The company currently has 240 thousand ounces hedged over three years, representing approximately 16% of forecast production.

The hedging structure utilises zero-cost collar strategies, purchasing put options while selling call options to offset premium costs. Chief Executive Officer Jeff Quartermain explains the rationale:

“Our current approach uses zero-cost collars, we buy downside protection at $2,600/oz and sell upside above that, locking in cash flow without premium cost.”

Recent hedging activity includes FY28 positions added at US$2,600 per ounce strike price, reflecting opportunistic positioning during elevated gold price periods. This approach provides margin protection while avoiding speculative positioning that could limit upside participation.

ESG Ensures Operational Continuity

Perseus's Environmental, Social, and Governance performance serves as insurance against permitting delays and regulatory pushback across its operational jurisdictions. Examples include the Yaouré tailings expansion and Edikan environmental upgrades, which demonstrate proactive engagement with evolving regulatory requirements.

The Investment Thesis for Gold Equities in 2025-2026

- Gold remains macro-relevant amid fiscal expansion and inflationary tailwinds, providing portfolio diversification benefits during periods of monetary accommodation

- Cost inflation represents a structural challenge that only select operators with operational excellence and disciplined capital allocation will navigate successfully

- Companies with diversified asset portfolios, self-funded growth capabilities, and permitting visibility are best positioned to preserve and enhance shareholder value

- Perseus demonstrates balanced growth execution through consistent production delivery, strong liquidity position, and jurisdictional spread across multiple West African countries

- Thematic exposure to West African and East African growth corridors provides leverage to regional economic development without overexposure to single-asset or high-risk development plays

- Asset portfolio longevity through mine life extensions and brownfield expansion opportunities supports sustainable cash generation profiles

- Strategic equity positions in exploration and development companies provide pipeline optionality without direct operational exposure or capital commitment

- Hedging strategies provide margin protection during commodity price volatility while preserving participation in potential upside movements

Strategic Survivors in a Cost-Repricing Era

The current gold mining cycle favours companies that prioritise operational excellence and capital discipline over growth at any cost. Perseus Mining exemplifies this evolution, successfully transitioning into a four-mine operator without diluting shareholder value or overleveraging its balance sheet.

In a market environment characterised by both macro volatility and operational complexity, strategic execution capabilities represent the primary differentiator between companies that will thrive and those that will struggle. Perseus's combination of geographic diversification, strong financial position, and disciplined growth approach positions the company to capitalise on gold's continued macro relevance while navigating the sector's structural challenges.

The company's track record of consistently meeting or exceeding production guidance over nearly five consecutive years, combined with its commitment to cash generation and shareholder returns, establishes Perseus as a strategic survivor in this cost-repricing era. As the gold sector continues to evolve, companies demonstrating Perseus's operational discipline and strategic vision are likely to emerge as the relative winners in an increasingly complex investment landscape.

Analyst's Notes

Subscribe to Our Channel

Stay Informed