Platinum's Sell-Off Leaves Fourth Consecutive 297koz Supply Deficit Intact

Platinum's sell-off reflects higher rate expectations, but a fourth straight 297koz supply deficit continues to support the long-term investment case.

- The Federal Reserve held its policy rate at 3.50% to 3.75% on June 17 but raised its median 2026 policy-rate projection to 3.8%, with futures markets now implying a roughly 77% chance of a December rate hike. Higher rate expectations weighed on non-yielding precious metals.

- Platinum has fallen about 16% in a month to near $1,638 per ounce but remains roughly 21% above its level a year ago. The decline reflects weaker sentiment, not a change in platinum's supply-demand balance.

- The World Platinum Investment Council forecasts a fourth consecutive annual deficit of 297,000 ounces in 2026 after a record 1.082-million-ounce shortfall in 2025, reducing above-ground stocks to about four months of demand.

- Platinum remains in supply deficit, while palladium and rhodium face weaker demand balances as electric vehicle adoption reduces catalytic converter demand.

- Jurisdiction, cost position, and development stage are more important than daily spot-price moves because they determine long-term supply risk and project economics.

How Higher Fed Rate Expectations Pressure Precious Metals

The selloff across platinum group metals was driven by higher Federal Reserve rate expectations rather than changes in physical supply. Higher rate expectations increased the opportunity cost of holding non-yielding precious metals, while platinum's supply deficit remained unchanged.

Higher Fed Rate Expectations Pressure Precious Metals

On June 17, the Federal Open Market Committee left its benchmark rate unchanged at 3.50% to 3.75%, but its updated projections signaled a more hawkish policy outlook. The median 2026 policy-rate projection rose to 3.8% from 3.4% in March, shifting from an implied rate cut to a rate hike, while nine of 18 officials projected at least one increase this year. Futures markets now price a roughly 77% chance of a December rate hike, up from about 24% a month earlier.

For platinum, the key variable is the real interest rate, or the nominal interest rate minus inflation. When real rates rise, non-yielding metals such as platinum, palladium, and rhodium become less attractive than cash or interest-bearing bonds. This was not unique to platinum. On June 20, Goldman Sachs cut its end-2026 gold price target from $5,400 to $4,900 after removing its remaining 2026 rate-cut assumptions, reflecting the broader impact of higher rate expectations across precious metals.

Lower Geopolitical Risk Weighs on Precious Metals

A second factor weighing on platinum prices was the decline in geopolitical risk premiums. A June 17 memorandum of understanding between the US and Iran, followed by the reopening of the Strait of Hormuz and roughly 16 million barrels transiting the waterway on June 21, pushed oil prices lower and reduced inflation expectations, weakening demand for safe-haven assets such as precious metals.

Lower oil prices reduced support for precious metals through two channels. They reduced inflation expectations and removed the geopolitical risk premium that had supported investment demand during the conflict. Together, higher rate expectations and lower geopolitical risk accelerated June's selloff, even though platinum's underlying supply-demand balance remained in deficit.

Price Weakness Masks Platinum's Supply Deficit

Platinum prices can fall even when the physical market remains in deficit. The key is to separate short-term price moves from long-term supply-demand fundamentals.

Investor Sentiment Drives Platinum's Short-Term Correction

As of June 24, platinum traded near $1,638 per ounce, down about 16% over the month but still roughly 21% higher than a year earlier. Palladium fell to roughly $1,202, its lowest level since September 2025, while rhodium traded near $7,950, down about 14.5% over the month but still roughly 46.5% higher than a year earlier.

The recent price decline reflects weaker investor sentiment rather than a change in platinum's supply-demand balance. Short-term prices are driven by investor sentiment and fund flows, while long-term value depends on supply and demand. That disconnect may create opportunities for investors who focus on long-term market fundamentals rather than short-term price movements.

A Fourth Consecutive Deficit Beneath the Sell-Off

The physical platinum market remains in deficit despite the recent price decline. The World Platinum Investment Council forecasts a 297,000-ounce deficit for 2026, meaning demand will exceed available supply, following a record 1.082-million-ounce deficit in 2025. Successive deficits have reduced above-ground stocks to roughly four months of demand, the lowest level in more than a decade. Industrial demand is forecast to rise 9% to 2,238,000 ounces in 2026, driven by glass-capacity expansions, partly offsetting weaker automotive and jewellery demand. Bar and coin investment is also forecast to increase 27%.

Nick Smart, Chief Executive Officer of ValOre Metals, an exploration company advancing a platinum-palladium project in Brazil, explains why higher platinum prices have not yet translated into new mine supply:

"The primary mine production of platinum has been in decline in the last five years... Forecast for this year is around 5 1⁄2 million ounces of primary platinum produced. And that's in the context of a metal price that has doubled over the last year. That tells you something about the inelasticity of supply, and the difficulty of bringing new metal to market."

Supply Concentration Drives the Scarcity Premium

Platinum supply cannot respond quickly to higher prices because production is concentrated in a small number of jurisdictions. As a result, projects that can add secure, long-term supply from lower-risk regions can command a premium.

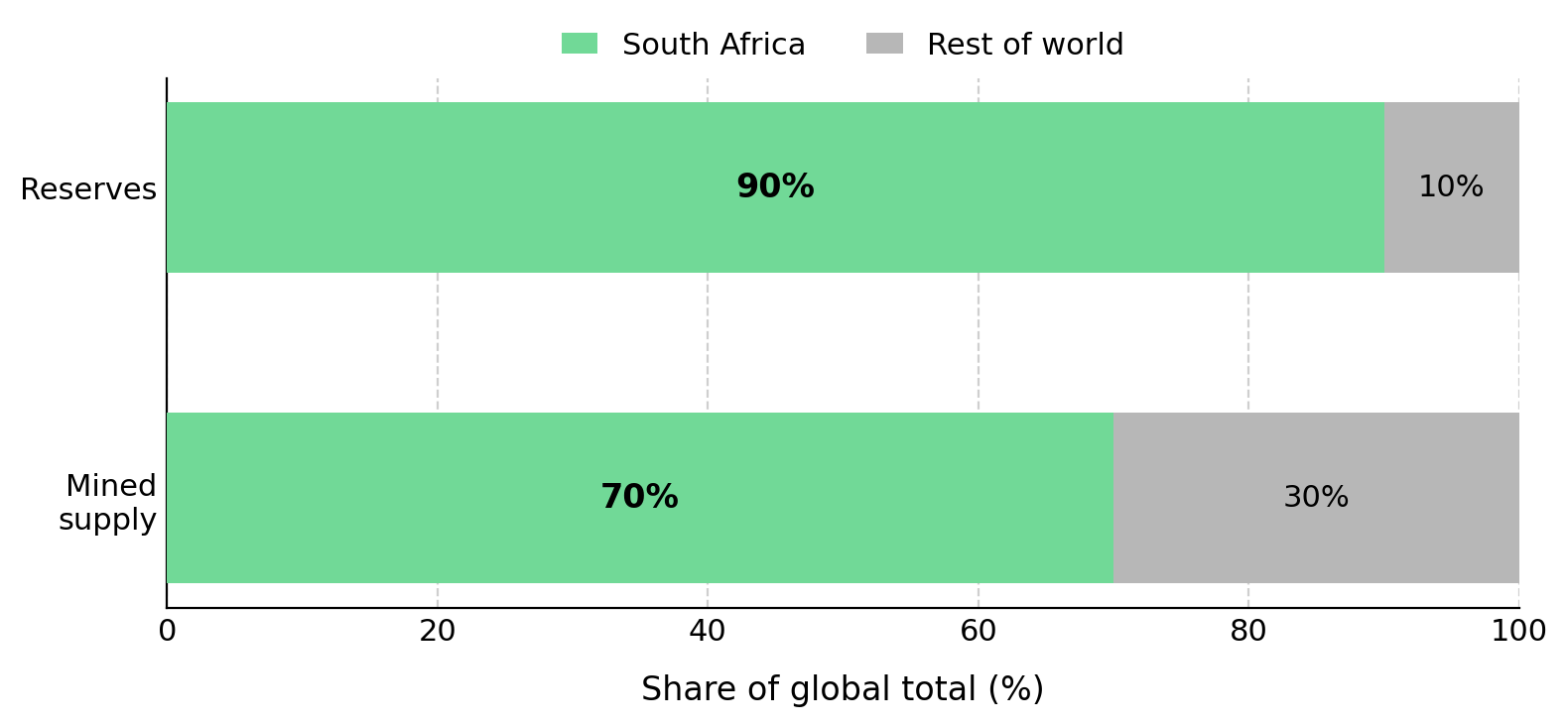

South Africa's Cost Pressures & Grid Constraints

South Africa supplies roughly 70% of primary mined platinum and hosts close to 90% of global reserves, leaving global supply heavily dependent on a single jurisdiction. Many of its mines are old and deep, while electricity reliability and wage negotiations continue to pose operational risks. These constraints limit how quickly supply can respond to higher prices because new mines require years of permitting, financing, and development before production begins.

Rising production costs matter because they increase the price needed to sustain existing mine supply. When the marginal producer's all-in sustaining cost, which includes operating and sustaining costs, approaches the metal price, producers are more likely to reduce output or delay investment, extending the supply deficit.

Trade Policy & the Push to Onshore Metal Supply

Trade policy is increasing supply risks for platinum group metals. The US has proposed a preliminary antidumping duty of 132.83% on unwrought Russian palladium, with a final injury determination from the International Trade Commission expected this month. The case matters because Russia supplies roughly 40% of global palladium, while at least one US producer has been operating at about half capacity. A parallel Section 232 critical minerals investigation also leaves open the possibility of tariffs or quotas on platinum group metals.

Trade policy changes where platinum group metals are sold rather than increasing global supply. It does not create new supply but redirects existing metal. That shift has already increased US exchange-warehoused platinum stocks from about 270,000 ounces at the start of 2025 to roughly 624,000 ounces. As more metal remains in the US, less is available to other markets, increasing the value of supply from stable jurisdictions while adding short-term price uncertainty.

Supply Deficits Increase the Value of New Projects

Comparing platinum group metals companies by development stage provides a clearer view of project risk and potential returns. Producers generate cash flow today and are evaluated on all-in sustaining cost, earnings, and balance-sheet strength, giving investors the most direct exposure to changes in the spot price. Developers have not yet entered construction and are evaluated using economic studies, including net present value (the discounted value of future cash flows), internal rate of return (the annualized project return), capital intensity, and permitting timelines. Explorers are at the earliest stage and are evaluated by grade, tonnage, resource classification, and enterprise value per ounce (EV/oz), which compares a company's market value, adjusted for cash and debt, with its in-ground metal inventory.

Resource confidence progresses from inferred (based on limited drilling) to indicated and then measured as geological certainty increases. Earlier-stage companies offer the greatest upside if projects advance but also the highest risk of dilution and capital loss if development stalls. Choosing between explorers, developers, and producers depends on an investor's risk tolerance and investment horizon.

Scarcity Value & the Investment Case for Exploration

ValOre Metals’ Pedra Branca project in Ceará State, Brazil, hosts a 2022 inferred resource of 2.198 million ounces of platinum, palladium, and gold at 1.08 g/t across 63.3 million tonnes. The estimate excludes five areas drilled in 2023. The company has not yet published an economic study and is conducting metallurgical test work at the University of Cape Town on a near-surface oxide horizon.

Oxide material may support heap leaching, which can reduce processing costs compared with conventional flotation, subject to test results. With a market value of about C$26 million versus peers valued at roughly C$126 million to C$440 million, ValOre trades at a lower EV/oz. Management attributes that discount to the absence of a published economic study rather than to the project's geology.

The upside of early-stage discoveries should be balanced against the likelihood that pre-revenue explorers will require additional financing, which often results in shareholder dilution before a project reaches an economic study.

Supply Deficits Outlast the Commodity Cycle

At the commodity level, platinum's outlook reflects a contrast between short-term macroeconomic pressures and long-term supply constraints. The factors weighing on platinum prices, including a hawkish Fed, a stronger US dollar, and lower geopolitical risk in the Middle East, are cyclical and can reverse as economic data or policy expectations change. By contrast, the supply deficit is supported by production concentrated in a high-cost region, low above-ground inventories, and mine development timelines measured in years rather than months.

The next near-term catalyst is the Federal Reserve's preferred inflation gauge, the Personal Consumption Expenditures (PCE) index. A higher-than-expected reading would strengthen expectations for a 2026 rate hike, support the US dollar, and weigh on precious metals, while a weaker reading could have the opposite effect. In either case, the data influences investor sentiment rather than platinum's underlying supply deficit. The World Platinum Investment Council projects platinum deficits averaging 331,000 ounces annually through 2030, while palladium and rhodium move toward more balanced markets as hybrid and electric vehicle adoption reduces catalytic converter demand. Platinum's continuing supply deficit contrasts with the weaker outlook for palladium and rhodium, making company selection and development stage more important than short-term price volatility.

The Investment Thesis for Platinum

- Exposure to a platinum supply deficit that has entered its fourth consecutive year and is forecast to continue through 2030, supported by low above-ground inventories rather than short-term investor sentiment.

- A preference for low-cost producers, as rising energy and labor costs increase the price needed to sustain mine supply and support companies with stronger margins.

- Recognition that mine supply responds slowly because permitting and development take years, increasing the value of low-cost projects in stable jurisdictions despite short-term changes in interest rates.

- A preference for companies with assets in multiple jurisdictions, as trade measures and critical-minerals policies increase the value of supply outside concentrated producing regions.

- A focus on development stage: producers provide cash flow, developers provide study-defined project economics, and explorers offer higher upside potential at lower EV/oz valuations, alongside higher financing and execution risk.

- A focus on company-specific catalysts, as valuation changes are often driven by resource updates, economic studies, and trade rulings, while pre-revenue explorers face a higher risk of dilution and capital loss.

June's selloff reflected higher interest-rate expectations rather than a change in platinum's supply-demand balance. A hawkish Fed and lower geopolitical risk have weighed on precious metals prices, but the platinum market is still forecast to record a 297,000-ounce supply deficit this year, leaving above-ground inventories at their lowest level in more than a decade. In a market where supply continues to fall short of demand, investors should focus on production costs, jurisdiction, resource quality, and development stage. Lower spot prices create an opportunity to compare producers, developers, and explorers without changing the long-term supply outlook for platinum. Investors who focus on the development stage project economics, jurisdiction, and financing risk will be better positioned to identify opportunities as market conditions change.

TL;DR

Platinum prices have fallen as higher interest rate expectations and easing geopolitical tensions reduced investor demand for precious metals, but the physical market remains in a fourth consecutive supply deficit. The World Platinum Investment Council forecasts a 297,000-ounce deficit in 2026, with above-ground inventories near multi-year lows and mine supply constrained by concentrated production, rising costs, and lengthy development timelines. The recent sell-off creates an opportunity to evaluate platinum companies based on jurisdiction, production costs, development stage, project economics, and financing risk rather than short-term price movements.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed