Policy Risk & 86% Refining Concentration Shift Financing Toward Lower-Risk Critical Mineral Projects

Policy risk and 86% refining concentration are reshaping critical mineral financing, increasing the value of projects that reduce single-jurisdiction supply chain exposure.

- China expanded its dual-use export controls on Japan on June 29, extending export licensing from tungsten, molybdenum, and rare earth minerals to finished magnets, including samarium-cobalt and neodymium-iron-boron (NdFeB), used in defense and electric vehicles.

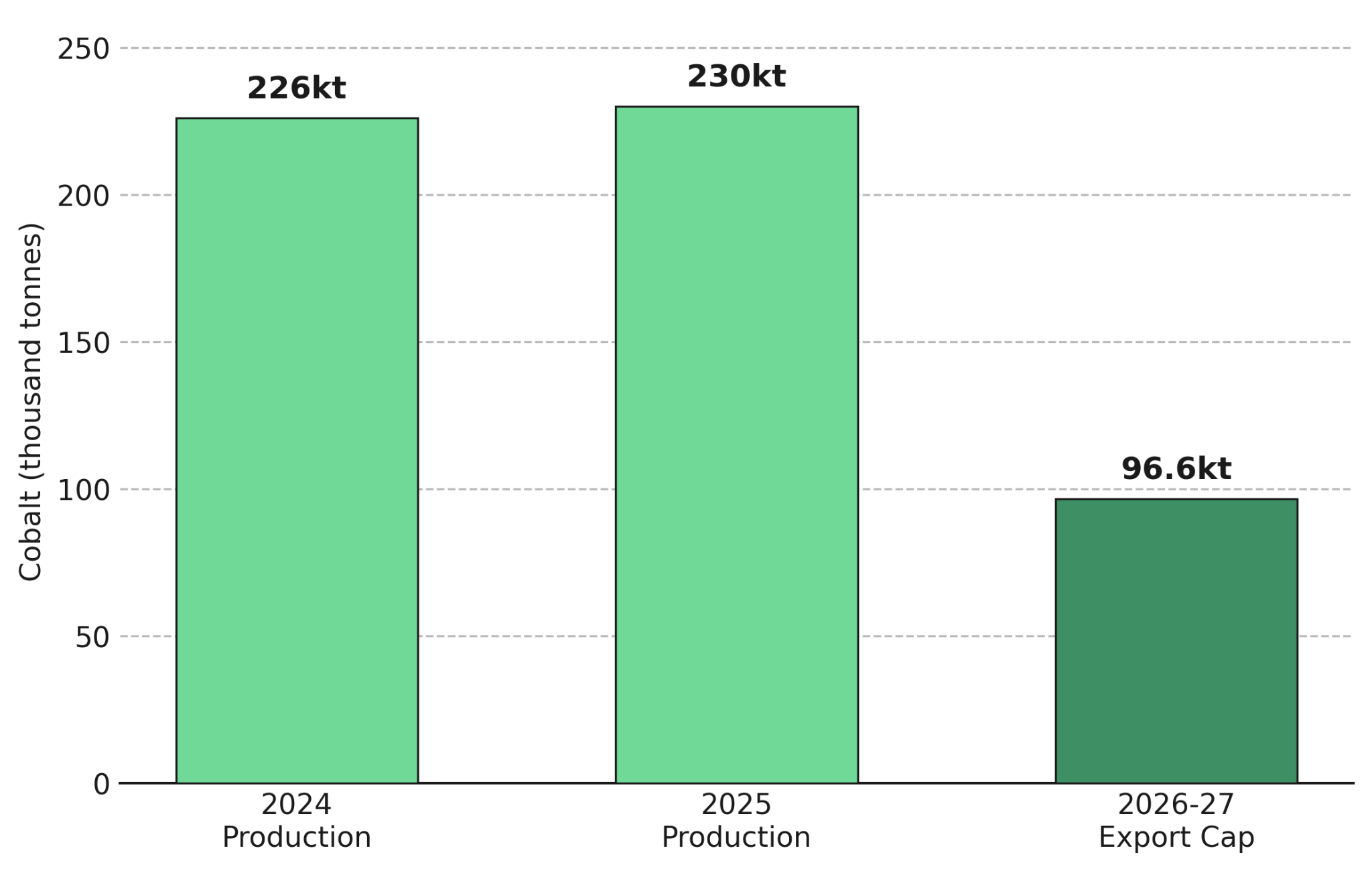

- A customs platform failure in the Democratic Republic of Congo has frozen cobalt export registrations since July 1, putting up to 20,000 tonnes of cobalt worth about $1.1 billion at risk under the country's use-it-or-lose-it export quota rule.

- The International Energy Agency reports that the top three refining nations controlled 86% of global critical mineral processing capacity in 2024, up from approximately 82% in 2020, underscoring continued dependence on a small number of jurisdictions.

- Developers that reduce single-jurisdiction exposure through byproduct production, recycling, or jurisdictional carbon-cost advantages are attracting more development financing than conventional single-commodity projects.

- Production, development, and recycling projects demonstrate multiple approaches to reducing single-jurisdiction exposure, including byproduct production, recycling, and lower-carbon operating models.

Export Controls & Policy Risk Reshape Critical Mineral Markets

Two unrelated policy actions in the first week of July demonstrated that government decisions can disrupt critical mineral supply independently of geology or mine performance. Within days of each other, China expanded its dual-use export restrictions on Japan while the Democratic Republic of Congo's cobalt export system stalled following a customs registration failure. Neither event involved a mine closure, a resource downgrade, or a change in underlying demand. Both affected critical mineral prices despite no change in mine supply or demand, reinforcing that policy decisions now carry the same weight as operational developments when assessing supply risk.

China Extends Export Controls Into Finished Magnets

On June 29, China's Ministry of Commerce blacklisted four Japanese government defense research institutes and added 20 additional entities, including units of Mitsubishi Electric and Mitsubishi Heavy Industries, to its export control list. The restrictions also cover tungsten, molybdenum, and rare earth magnets such as samarium-cobalt and neodymium-iron-boron (NdFeB), key inputs for electric vehicle traction motors and defense applications. By extending controls to finished magnet materials rather than raw oxides, China broadened export restrictions beyond upstream mining into higher-value manufacturing inputs, making downstream processing and component supply more exposed to policy decisions.

Congo's Export Quota System Tightens Cobalt Supply

The Democratic Republic of Congo produces roughly 70% of the world's mined cobalt and has capped annual exports at 96,600 tonnes for 2026 and 2027, less than half of its 2024 production. Under the country's quota rules, any allocation not shipped by a fixed deadline is automatically forfeited to the state's strategic reserve. A registration failure on the country's customs platform, unresolved since July 1, has already put an estimated 20,000 tonnes of cobalt, worth approximately $1.1 billion, at risk of forfeiture, affecting producers including CMOC, Glencore, Eurasian Resources Group, and Huayou Cobalt. The registration failure demonstrates that administrative decisions within the export quota system can reduce available supply and affect cobalt prices even when mine production and demand remain unchanged.

USMCA Non-Renewal Raises North American Supply Chain Risk

A third policy decision during the same week added further uncertainty to North American critical mineral supply chains. On July 1, the US declined to renew the US-Mexico-Canada Agreement in its current form, placing a trade framework covering approximately $2.5 trillion in annual continental commerce into a decade-long cycle of annual reviews instead of confirming a 16-year extension. Although the agreement remains in force, annual reviews make future trade rules less predictable, increasing policy risk for critical mineral projects and battery supply chains that depend on cross-border production between Canada, US, and Mexico.

Refining Concentration Persists Despite Five Years of Diversification

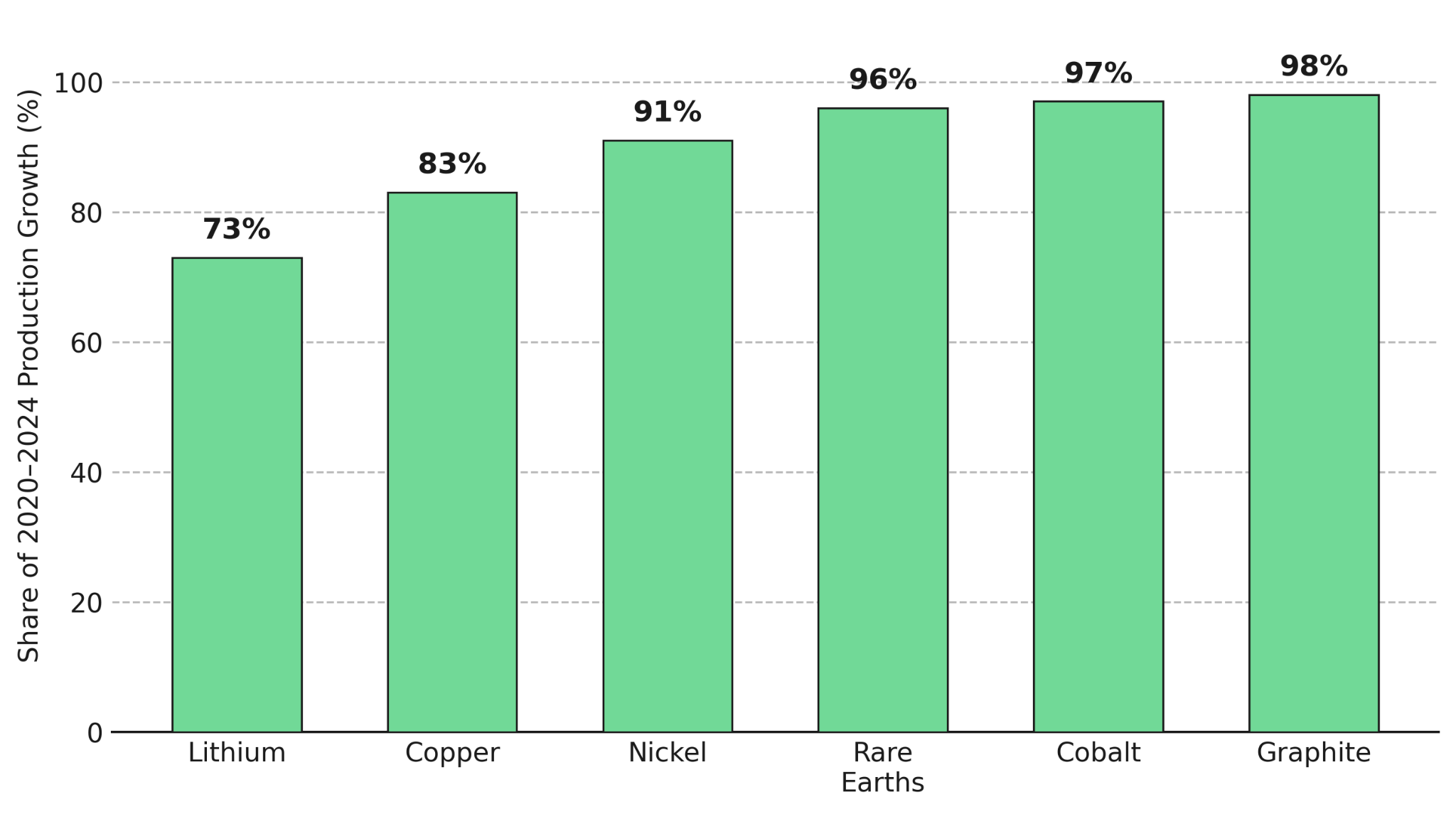

The Congo customs failure and China's expanded export controls are not isolated events but reflect how little global refining concentration has changed despite five years of diversification policies. According to the International Energy Agency, the average market share held by the top three refining nations across copper, lithium, nickel, cobalt, graphite, and rare earth elements rose to 86% in 2024 from approximately 82% in 2020. Refining and processing capacity, rather than mine supply, remains the primary source of concentration risk across critical mineral supply chains.

Almost all incremental supply growth over that period came from a single dominant supplier for each commodity, with Indonesia leading nickel and China accounting for most other critical minerals. The IEA's base-case projection, based on current policy settings and investment trends, shows the top-three refining share declining only modestly over the next decade, remaining close to its 2020 level. Diversification programs launched after the first wave of export restrictions have yet to reduce dependence on a small number of refining countries.

The refining concentration data provides more context than any single quota dispute because it explains why individual policy actions continue to disrupt critical mineral supply chains. The Congo customs failure and China's expanded export controls on Japan reflect the same underlying supply-chain vulnerability rather than unrelated policy events. Both events highlight that refining concentration remains largely unchanged, shifting the focus from predicting the next policy disruption to identifying companies that have reduced their exposure to concentrated supply chains.

Supply Chain Resilience Shapes Critical Mineral Financing

Due diligence now places greater emphasis on jurisdictional policy exposure alongside resource quality. Resource size and grade remain necessary for project financing, but they are no longer sufficient on their own. Financers now place greater weight on a project's exposure to policy decisions in a single jurisdiction than on resource quality alone when assessing long-term supply risk.

Development finance institutions now place greater weight on permitting, environmental compliance, and jurisdictional risk during due diligence. For example, the International Finance Corporation has confirmed that one project's definitive feasibility study and environmental and social impact assessment satisfy its performance standards, allowing other lenders to complete parts of their due diligence more quickly.

Three de-risking approaches have become increasingly important for critical mineral projects: byproduct production, where strategic minerals are recovered alongside an existing mining operation; recycling, where secondary feedstock reduces reliance on primary extraction; and jurisdictional cost or carbon advantages, where project location lowers operating costs, carbon exposure, or policy risk.

Byproduct Production Adds Critical Minerals Without New Greenfield Risk

Adding strategic mineral production to an existing mine or project already under development can reduce permitting, construction, and financing risk compared with building a standalone operation. Because much of the infrastructure, permitting, and resource definition work is already complete, lenders face fewer execution risks and shorter development timelines.

Existing Infrastructure Lowers Capital and Permitting Risk

Energy Fuels’ White Mesa Mill in Utah is the only fully licensed, operating conventional uranium processing facility in the US and the only US facility capable of separating monazite into individual rare earth oxides. The mill processes up to 10,000 tonnes of monazite annually, producing up to 1,000 tonnes of neodymium-praseodymium (NdPr) oxide each year, a key feedstock for permanent magnets used in electric vehicles and defense applications.

Mark Chalmers, then Chief Executive Officer of Energy Fuels, outlines the requirements for a competitive rare earth supply chain:

"The US government's biggest challenge is competing with the ex-China rare earth supply chain. We've got all the skill sets required from mining through alloys, and to compete with China, you have to have every step in that chain."

Existing Mine Plans Support Multiple Mineral Products

Sovereign Metals’ Kasiya's definitive feasibility study reports a net present value (NPV) of $2.2 billion using an 8% discount rate, based primarily on rutile (titanium) and graphite production. A newly confirmed monazite stream, recoverable through the existing tailings circuit at near-zero incremental capital cost, adds rare earth production while avoiding the permitting, infrastructure, and capital requirements of a standalone project.

Ben Stokovich, Chairman of Sovereign Metals, explains Kasiya's low-cost graphite production advantage:

"Our incremental cost to produce graphite as a byproduct from the Kasiya project will be only US$241 per tonne. We'd generate a 50% operating margin even if we sold only into the lower-value battery graphite market."

Recycling & Lower-Carbon Jurisdictions Reduce Development Risk

Byproduct production is one way to reduce development risk, but it is not the only approach. Recycling end-of-life material and developing projects in jurisdictions with lower operating and carbon costs provide two additional ways to reduce permitting, capital, and execution risk beyond the byproduct model.

Recycling Expands Critical Mineral Supply Without New Mining

Lifezone Metals' US PGM Recycling Project recovers critical minerals from recycled feedstock rather than new mine development. Pilot-scale testwork has demonstrated recovery rates of up to 99% for platinum and palladium and up to 95% for rhodium using the company's proprietary Hydromet technology, originally developed for its Kabanga nickel project in Tanzania. Because recycling does not require a new mine, resource estimate, or environmental and social impact assessment, it avoids many of the permitting and development risks associated with primary production. The reported recovery rates, however, are based on pilot-scale testing and have not yet been demonstrated at commercial scale.

Lower-Carbon Jurisdictions Gain Under CBAM

Canada Nickel's Crawford project in Ontario uses the province's low-carbon electricity grid to support a lower-carbon operating profile. Instead of relying on byproduct production or recycling, the project's potential advantage comes from Ontario's low-carbon electricity grid, which can reduce the embedded carbon intensity of its products and lower future compliance costs under the European Union's Carbon Border Adjustment Mechanism (CBAM).

Mark Selby, Chief Executive Officer of Canada Nickel, highlights Ontario's low-carbon advantage for European steel:

"We're in an ideal position to leverage Ontario's lower-cost, low-carbon energy grid, powered by nuclear and hydro, while adding more than 10,000 megawatts of nuclear capacity. That puts us in a tremendous position to help Europe decarbonize its steel industry."

Policy Risk Continues to Shape Critical Mineral Markets

The broader pattern is that companies are responding to critical mineral concentration in different ways rather than relying on a single solution. Existing infrastructure, byproduct production, recycling, and lower-carbon operating jurisdictions each reduce exposure to different parts of the supply chain where policy decisions continue to shape availability and cost.

The expanded China-Japan export controls, the Congo customs failure, and the USMCA non-renewal reflect different forms of policy risk affecting critical mineral supply chains rather than isolated events. The top three refining nations still controlled 86% of global processing capacity in 2024 despite five years of diversification efforts, leaving critical mineral supply chains highly exposed to future policy decisions.

The Investment Thesis for Critical Minerals

- With refining capacity still concentrated in a small number of countries, jurisdictional exposure remains a key consideration when assessing critical mineral projects across the development cycle.

- Adding strategic mineral production to an existing mine plan or processing circuit reduces the need for new infrastructure, lowering capital requirements and execution risk compared with standalone developments.

- Recycling reduces permitting and resource-definition risk by relying on existing feedstock rather than new mineral extraction. However, pilot-scale recovery rates do not necessarily translate into commercial-scale throughput.

- Projects located in jurisdictions with lower-carbon electricity grids and supportive regulatory frameworks may face lower carbon-related compliance costs under mechanisms such as the European Union's Carbon Border Adjustment Mechanism (CBAM).

- As policy decisions increasingly influence critical mineral supply and pricing, jurisdictional risk has become a core consideration alongside geological, metallurgical, and economic assessments in project due diligence.

- Financing milestones are a more reliable indicator of project de-risking than development announcements because they reflect third-party assessment of technical, permitting, and execution risks.

The events of the first week of July did not involve a mine closure, resource downgrade, or demand shock, yet they affected critical mineral pricing without any change in underlying supply or demand. That is the defining feature of the current critical minerals cycle: government policy decisions in a small number of exporting countries now influence critical mineral pricing as much as changes in geology or mine development. With refining concentration remaining largely unchanged over the past five years, differences between projects increasingly reflect how they reduce exposure to concentrated supply chains and policy risk. Financing commitments and offtake agreements remain subject to project milestones and final approvals, making execution an important consideration alongside resource quality and jurisdictional exposure.

TL;DR

China's expanded export controls, the Democratic Republic of Congo's cobalt export disruption, and the USMCA non-renewal show that government policy decisions can affect critical mineral supply and pricing even without changes in mine production or demand. With the top three refining nations controlling 86% of global processing capacity, supply chain concentration remains a key market risk. Development finance is increasingly favoring projects that reduce exposure through existing infrastructure, byproduct production, recycling, and lower-carbon jurisdictions, while financing milestones remain a more reliable indicator of project progress than company announcements.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed