Canada Nickel Shifts Focus to Market Development Ahead of Crawford Production

Canada Nickel's RWEST MOU advances Crawford's commercial strategy by targeting market access, carbon pricing advantages & future offtake ahead of production.

- Canada Nickel signed a memorandum of understanding (MOU) with RWE Supply & Trading GmbH (RWEST) on June 1, 2026, targeting a definitive agreement before year-end 2026.

- The MOU is a non-binding framework, not a signed offtake or financing agreement: it targets customer access in the European Union (EU) and the United States, carbon market positioning, and the future development of long-term offtake structures ahead of first production at Crawford.

- RWEST's role centres on positioning Canada Nickel's low-carbon nickel and steel products against the EU's Carbon Border Adjustment Mechanism (CBAM), which management says raises the value of Ontario-sourced, low-carbon supply as European carbon costs increase.

- RWEST is also expected to support access to European and German export credit agencies (ECAs), adding a potential financing channel alongside the company's existing Export Development Canada engagement.

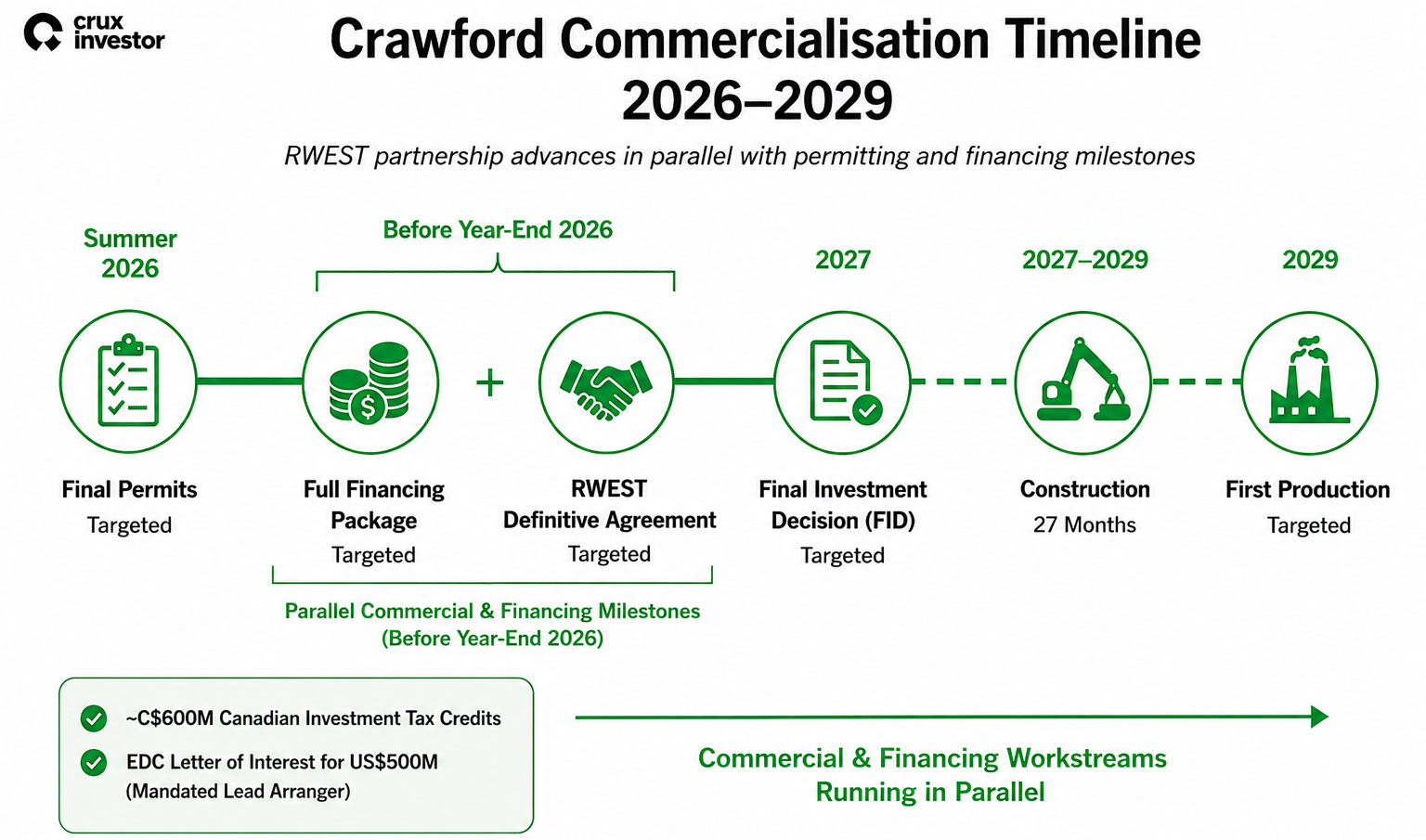

- The agreement follows Crawford's Front End Engineering and Design (FEED) update, which reported a net present value at an 8% discount rate (NPV8%) of US$2.8 billion, with first production targeted for 2029.

Canada Nickel Company Inc. (TSXV: CNC | OTCQX: CNIKF) is moving to close a gap that matters more to Crawford's bankability than any other drill result or cost update: who will buy the output and at what carbon-adjusted price. A memorandum of understanding (MOU) signed June 1, 2026 with RWE Supply & Trading GmbH (RWEST), announced July 6, 2026, gives the company a counterparty with direct exposure to the European Union's (EU) Carbon Border Adjustment Mechanism (CBAM) and to European export credit agency (ECA) channels, at the same time Crawford is working through its remaining permitting and financing milestones ahead of a targeted 2027 final investment decision.

The MOU commits neither party to binding volumes, pricing, or financing terms. Its value to investors sits in what it signals: a deliberate move to begin building offtake structures and market access before construction begins, rather than after.

The CBAM Angle

CBAM changes the economics of carbon-intensive imports into the EU, and Canada Nickel is positioning Crawford's Ontario-based, low-carbon power supply as a pricing advantage rather than an ESG label. Mark Selby, Chief Executive Officer and Director of Canada Nickel, tied the timing of the partnership directly to that mechanism:

"The timing of this strategic partnership could not be better. The implementation of CBAM, driving higher EU carbon costs, combined with persistent energy price volatility in Europe, is creating real demand for stable energy and low-carbon steel supply. Ontario's stable, low-carbon and renewable energy gives us a structural cost advantage that only grows as CBAM carbon costs rise through the decade."

For investors, this reframes the low-carbon narrative around Crawford as a margin variable tied to a specific, dated regulatory mechanism rather than a general sustainability claim. RWEST's stated role is to help Canada Nickel translate that carbon position into commercial terms, including CBAM compliance strategy support, as the EU mechanism phases in.

Offtake & Market Access

Under the MOU, Canada Nickel and RWEST will jointly identify and prioritise target customers in the EU and the United States for semi-finished steel, alloys, and stainless products, including long-term offtake structures. Marc Milligan of RWE Supply & Trading anchored the demand side to specific end markets:

"Canada Nickel's potential to support significant low-carbon stainless and alloy intermediate steel production offers an attractive solution for the European Energy Transition. Low-carbon steel is essential for the planned expansion of offshore and onshore wind capacities and high-quality low-carbon nickel is essential for battery production to support battery storage development in the EU."

That demand link, tied to wind capacity buildout and battery storage rather than general steel demand, is the detail that will matter most when assessing whether the relationship converts into contracted volumes ahead of production.

Financing Complementarity

RWEST's expected support for access to German and EU export credit agencies adds a potential financing channel that runs parallel to, rather than in place of, Canada Nickel's existing capital stack. That stack already includes approximately $600 million in Canadian investment tax credits and an Export Development Canada letter of interest for US$500 million as mandated lead arranger. A European ECA channel, if it materialises through the MOU, would diversify that financing base geographically at a point when the company is targeting a full financing package by year-end 2026, the same window in which it is targeting a definitive agreement with RWEST.

The distinction for investors: the RWEST relationship does not itself add committed capital. It addresses two separate bankability requirements, financing access and demand certainty, on a similar timeline to the project's own financing target.

Milestone Sequencing

The MOU lands inside a defined run of Crawford milestones: final permits targeted for the summer of 2026, a full financing package targeted by year-end 2026, a definitive agreement with RWEST targeted over the same window, a final investment decision targeted for 2027, and first production targeted for 2029 following a 27-month construction period.

Crawford's Front End Engineering and Design (FEED) update reported a net present value at an 8% discount rate (NPV8%) of US$2.8 billion and a 17.6% internal rate of return (IRR). The sequencing matters because it places commercial and financing workstreams on parallel tracks with permitting and project financing, rather than deferring market development until after construction is underway.

Strategic Shareholder Read-Through

As of the company's most recent investor presentation, Canada Nickel shares traded at C$1.79, with a market capitalisation of approximately C$431 million and a 52-week trading range of C$0.73 to C$2.59. The company's existing strategic shareholder base, Agnico Eagle, Samsung SDI, Anglo American, and Taykwa Tagamou Nation, already reflects committed capital and, in Samsung SDI's case, an offtake-linked investment structure tied to Crawford's project value. The RWEST MOU extends that same logic to the European market: a non-equity commercial partner brought in ahead of production to secure demand and financing access, mirroring the role strategic shareholders have played on the capital side. Whether RWEST's involvement deepens into binding offtake or financing commitments over the coming months will be the clearest signal of whether Crawford's commercialisation strategy is converting into contracted certainty ahead of its 2027 investment decision.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed