The New M&A Problem in Gold Mining: A Shrinking Pipeline of Junior Developers

Gold mining producers face a growing M&A challenge as fewer junior developers create acquisition bottlenecks, increasing competition for growth.

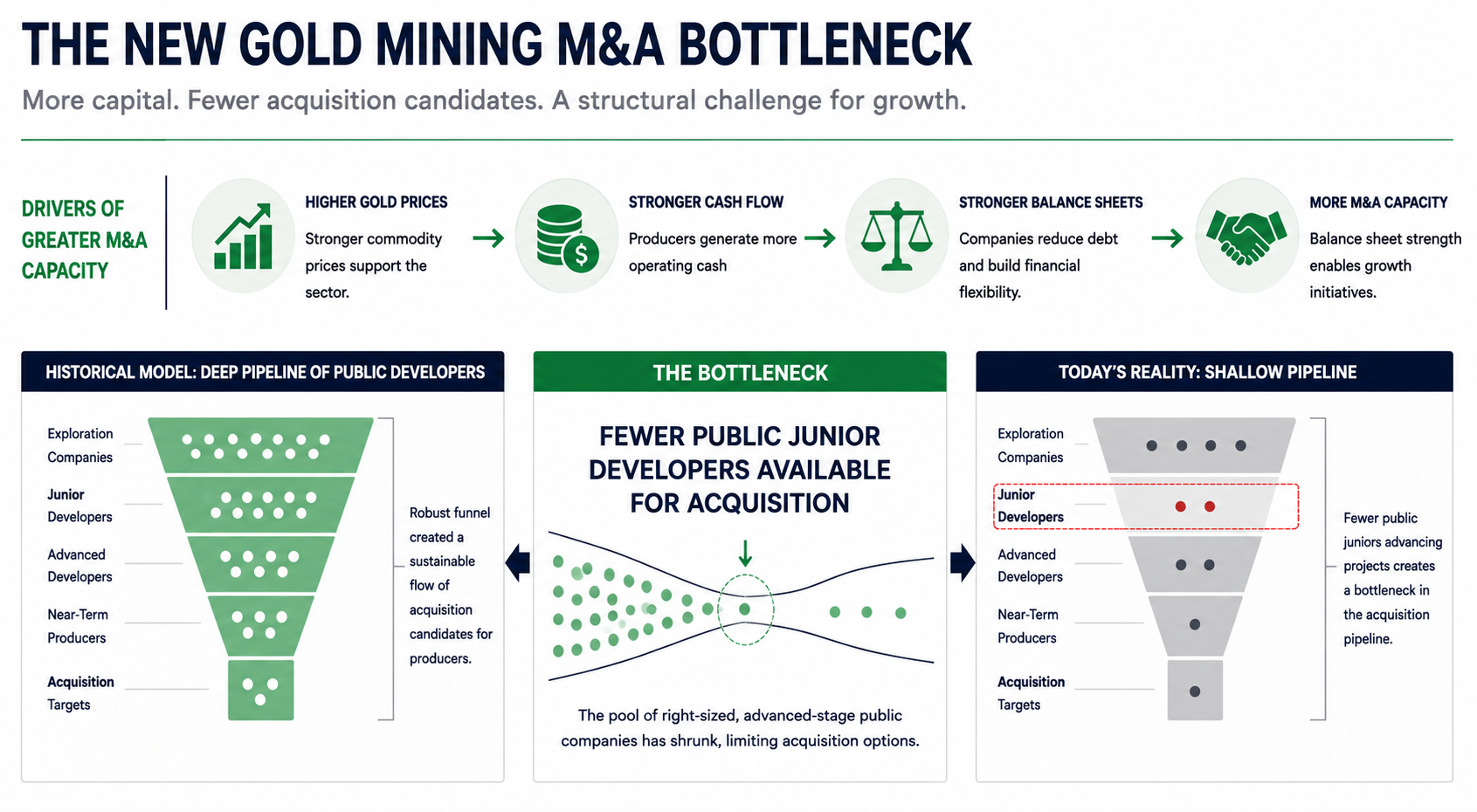

- Stronger gold prices have improved cash generation and balance sheets across the gold sector, but many producers are finding that a shortage of acquisition targets is becoming a new constraint on growth.

- Public junior developers have historically provided a pipeline of acquisition candidates for producers seeking to add production through Mergers and Acquisitions (M&A), but management commentary cited in the article indicates that this pool has become more limited.

- In Brazil, the concentration of assets among larger mining companies has reduced the number of public junior companies and junior-sized projects available for acquisition, making local consolidation more difficult for mid-tier producers.

- As public acquisition opportunities become scarcer, producers are increasingly evaluating private assets, although management described this process as involving a "game of valuations" when assessing potential opportunities.

- A smaller acquisition pipeline increases the importance of capital allocation discipline, as producers compete for a limited number of targets while also considering organic growth options such as brownfield exploration, resource expansion drilling, and plant upgrades.

A Growth Challenge Emerging in a Strong Gold Market

Gold producers spent much of the past decade constrained by limited access to capital. Higher gold prices have since increased operating cash flow, strengthened balance sheets, and allowed many producers to eliminate debt. Yet companies seeking to convert that financial strength into production growth are encountering a different constraint: a shortage of acquisition targets.

The challenge is most visible among producers looking to acquire near-term production or advanced-stage development assets. Historically, public junior developers advanced projects from exploration through development, creating a pipeline of acquisition candidates for larger operators. Today, many producers report that the number of public companies occupying that middle ground has declined.

This matters because acquisitions remain one of the fastest ways for producers to increase production, extend mine life, and improve operating scale. A smaller pool of acquisition candidates increases competition for available assets, raises the risk of higher transaction valuations, and forces management teams to consider alternative growth strategies.

Industry Context: The Hollowed-Out Development Pipeline

The current shortage of acquisitions reflects a change in the structure of the mining sector. During periods of weak financing conditions, many junior developers struggled to fund exploration programmes, complete technical studies, or advance projects toward production. Some companies were acquired, while others failed to progress assets beyond the development stage.

The result is a smaller population of publicly listed developers capable of attracting acquisition interest from producers. Historically, companies seeking growth could evaluate a broader range of public opportunities spanning development, permitting, and near-production stages. Today, the number of publicly traded acquisition candidates appears more limited, particularly for producers seeking assets capable of adding meaningful production within a relatively short timeframe.

The consequence is straightforward. When the supply of acquisition candidates declines while producers accumulate capital, competition for the remaining assets can increase. That dynamic can support higher acquisition premiums while making capital allocation discipline more important for management teams pursuing growth. Stronger gold prices have increased producers' financial capacity to pursue acquisitions, but the number of public junior developers available as acquisition targets appears more limited. The result is a growing bottleneck in the traditional Mergers and Acquisitions (M&A) pipeline.

Regional Perspective: Why Established Mining Jurisdictions Can Offer Fewer Targets

The acquisition shortage is not evenly distributed across all jurisdictions. In established mining regions, many of the most prospective districts are already controlled by large producers with long operating histories and extensive land positions.

Brazil illustrates this challenge. The country remains one of the world's most active mining jurisdictions, but many established mining districts are dominated by larger operators. For producers seeking acquisition opportunities, that concentration reduces the number of publicly traded junior companies that could become takeover targets.

The effect is particularly significant for mid-tier producers that already operate in the country. Acquiring assets within an existing jurisdiction allows companies to leverage their established in-country overhead and avoids the complexity of building a new operating platform in another jurisdiction. However, if the local acquisition pipeline is limited, producers may be forced to broaden their search beyond their preferred operating regions.

Company Example: When Capital Availability Exceeds Target Availability

Serabi Gold plc (AIM: SRB | TSX: SBI | OTCQX: SRBIF) provides an example of how these industry dynamics are affecting acquisition strategy. The company had eliminated debt and accumulated approximately US$65 million in cash by the end of the first quarter of 2026, providing financial flexibility to pursue growth opportunities. Despite that financial position, management indicated that identifying suitable acquisition targets has become increasingly difficult. The challenge is not access to capital but access to appropriately sized opportunities that fit the company's operating profile.

Chief Executive Officer of Serabi Gold, Mike Hodgson, discussed the issue:

"I think one of the challenges we have is that there aren't a lot of the right-sized scale projects and operations for us, partly because Brazil is dominated by larger companies. There aren't many juniors in Brazil, so therefore there aren't many junior-sized projects in Brazil or operations in Brazil."

The significance of that observation extends beyond a single company. If producers with available capital cannot identify sufficient acquisition candidates within their established operating jurisdictions, they may need to broaden their geographic search criteria or pursue alternative growth strategies.

Expanding the Search Beyond Public Companies

As public acquisition opportunities become scarcer, producers are increasingly evaluating privately held projects. For some companies, private assets now represent a larger share of the available acquisition universe than publicly listed developers do.

Private opportunities can provide access to advanced-stage projects, near-term production, or exploration upside that may no longer be readily available among public companies. However, moving into private opportunities introduces what management described as the "game of valuations" - the challenge of determining asset value when comparable public opportunities are limited.

As producers widen their search into private markets, the ability to assess valuation becomes an increasingly important part of the acquisition process. This places greater emphasis on management's ability to evaluate opportunities and allocate capital effectively.

Remaining Challenges: The Risk of Buying for Scale

A smaller acquisition pipeline creates a predictable risk: producers may feel pressure to pursue transactions simply because growth opportunities are limited. Strong gold prices have improved cash generation across much of the sector, and investors increasingly expect management teams to explain how excess capital will be deployed.

When acquisition candidates are scarce, competition can push valuations higher. Assets that might have attracted limited attention during weaker commodity cycles can become strategic targets because alternative opportunities are limited. In these circumstances, transaction discipline becomes a critical determinant of long-term value creation.

Hodgson emphasised the importance of maintaining that discipline:

"We're not going to compromise what we're doing just to chase some scale because there are a lot of things out there that you don't want to buy. My mentor always used to say to me, sometimes the best deals you do are the ones you don't do."

In a market with fewer acquisition candidates, management teams should be evaluated not only on the transactions they complete but also on their willingness to reject opportunities that do not meet return or strategic criteria.

Industry Outlook

New acquisition candidates cannot be created quickly. Before becoming realistic takeover opportunities, projects typically require extensive drilling, environmental and indigenous permitting, and access to development funding. Even in a stronger gold market, those requirements limit how quickly the pool of acquisition candidates can expand.

Until more developers reach advanced stages, many producers may rely more heavily on organic growth. Resource expansion drilling, brownfield exploration, plant upgrades, and operational improvements can increase production without requiring acquisitions, providing an alternative growth pathway when suitable external opportunities are limited.

Competition for quality acquisition targets is therefore likely to remain intense. Producers across the sector are generating stronger cash flows while the supply of advanced-stage public developers remains constrained. The new M&A problem in gold mining is not a lack of capital but a lack of acquisition candidates, making acquisition discipline, organic growth potential, and the ability to assess opportunities beyond traditional public markets increasingly important factors for investors.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed