Zero-Dollar Treatment Charges Signal a Multi-Year Mine Supply Shortfall & Lift Copper Project Values

Zero-dollar copper treatment charges signal a multi-year mine supply shortfall, improving the outlook for high-quality development projects and exploration discoveries.

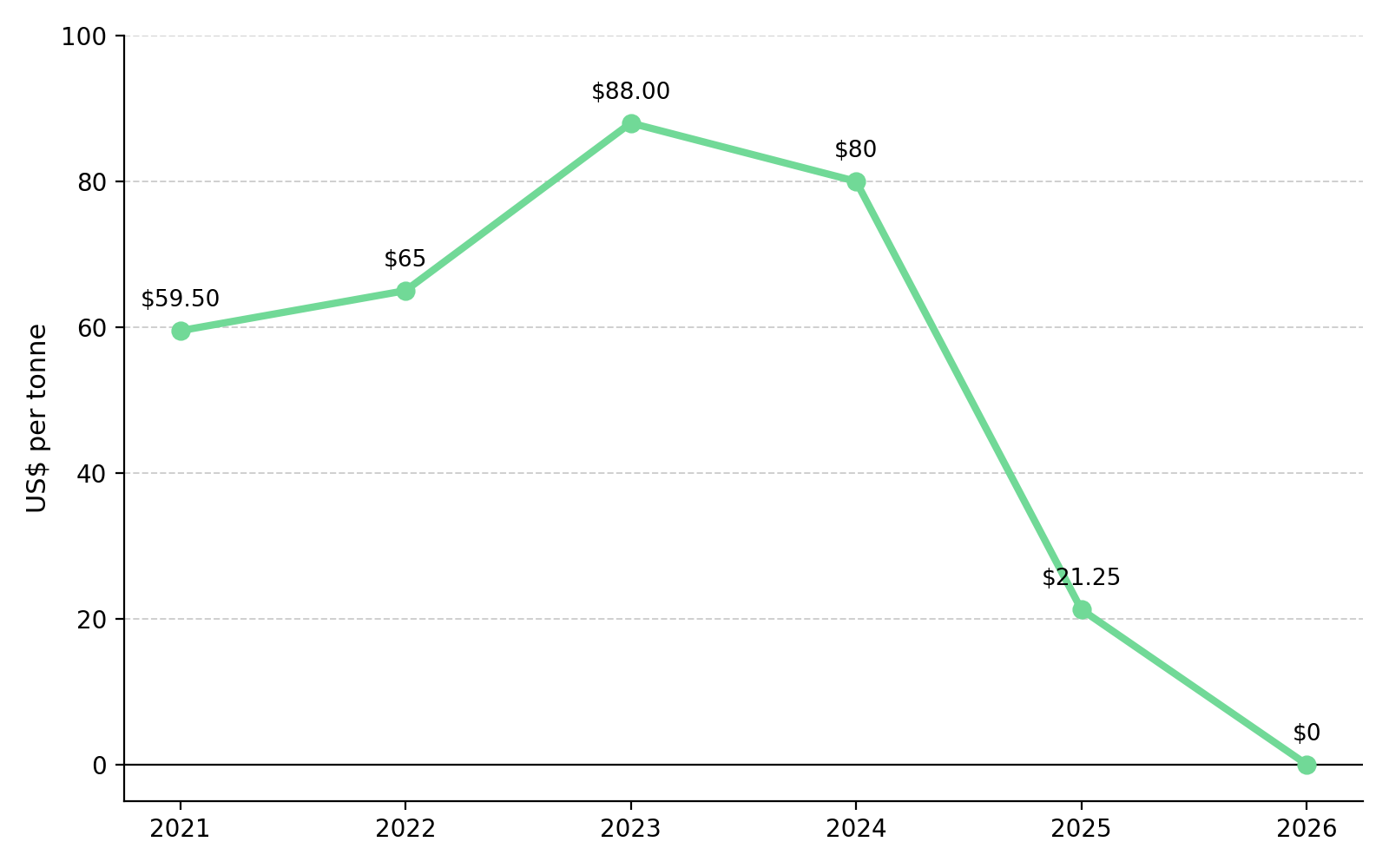

- Chinese smelters accepted a benchmark treatment charge of US$0 per tonne for copper concentrate in 2026, down from US$21.25 per tonne in 2025 and the lowest benchmark treatment charge on record.

- The collapse in treatment charges reflects a shortage of copper concentrate rather than excess smelting capacity. The zero-dollar benchmark shows that mine supply, not refining capacity, now limits global copper output.

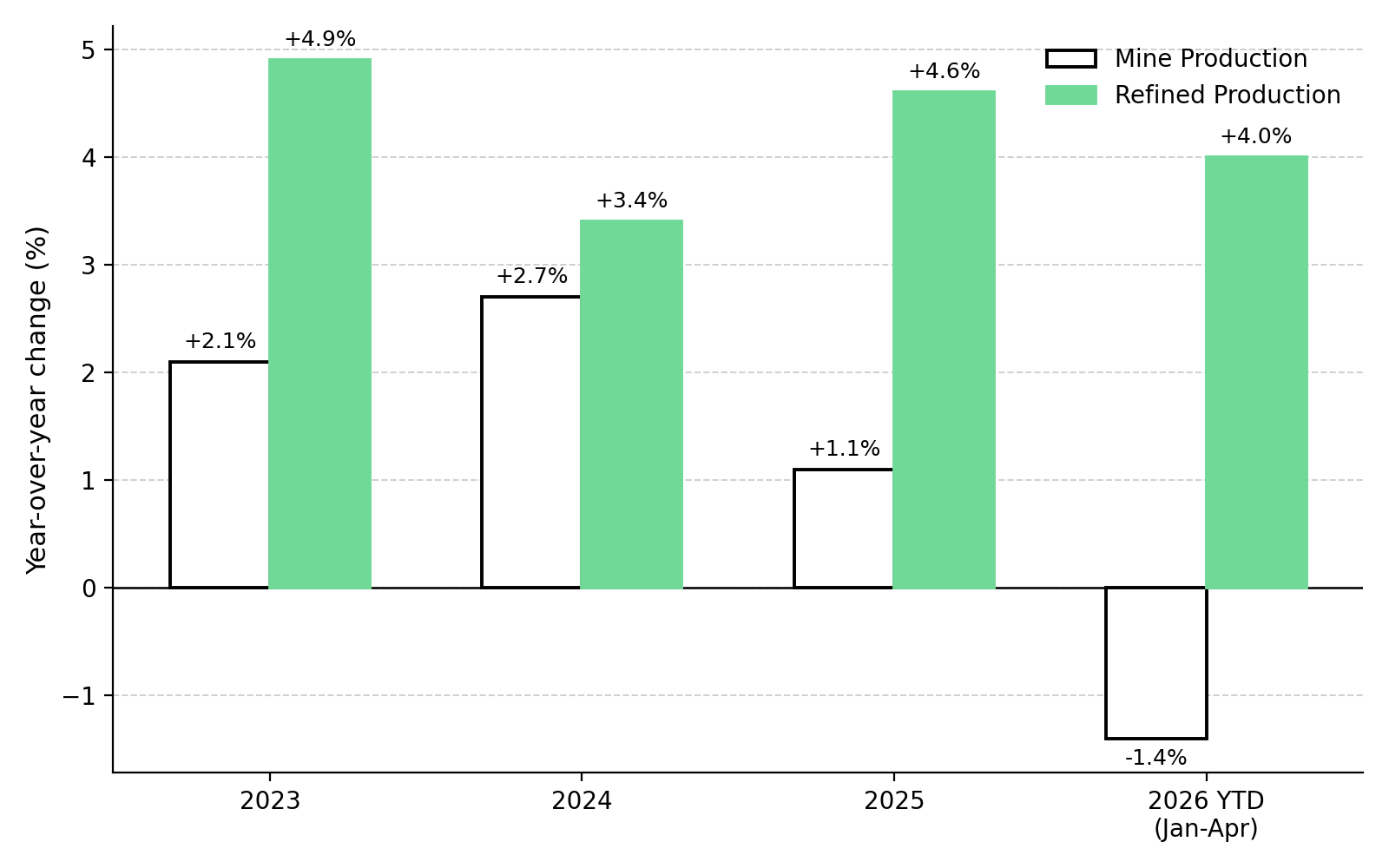

- Despite pledging to cut output by more than 10 percent in 2026, Chinese refined copper production grew 7.4 percent year over year from January through April, showing that concentrate shortages had not yet reduced refined copper output.

- The shortage of copper concentrate is now a primary driver for developers advancing toward a final investment decision, as it supports higher long-term copper price assumptions in valuation models, thereby increasing project net present value and improving financing prospects.

- Successful copper discoveries become more valuable because producers need new mine supply to replace declining reserves and limited development pipelines.

Shrinking Processing Margins & Smelter Profitability

Treatment and refining charges are the fees smelters charge miners to convert copper concentrate into refined copper. They reduce the price miners receive for copper concentrate, rising when concentrate supply exceeds smelting capacity and falling when concentrate becomes scarce. In 2026, concentrate shortages drove benchmark treatment and refining charges to zero. The 2026 benchmark settlement between a major Chilean miner and a leading Chinese smelter set the charges at US$0 per tonne and 0 cents per pound, down from US$21.25 per tonne and 2.125 cents per pound in 2025.

A benchmark treatment charge of zero eliminates the processing margin that traditionally supported smelter earnings. Many smelters now rely on byproduct revenue, primarily sulfuric acid sales and gold and silver credits recovered during refining, to remain profitable. The shift toward byproduct revenue shows that the treatment charge collapse reflects an industry-wide shortage of copper concentrate rather than a disruption at a single mine.

China's largest custom smelters agreed to reduce collective output in 2026 because of the concentrate shortage. The group committed to reducing output by more than 10 percent because concentrate supply was insufficient to utilize existing smelting capacity. Those production cuts confirm that copper concentrate, rather than smelting capacity, is now the main constraint on refined copper production.

Mine Development Timelines & Copper Availability

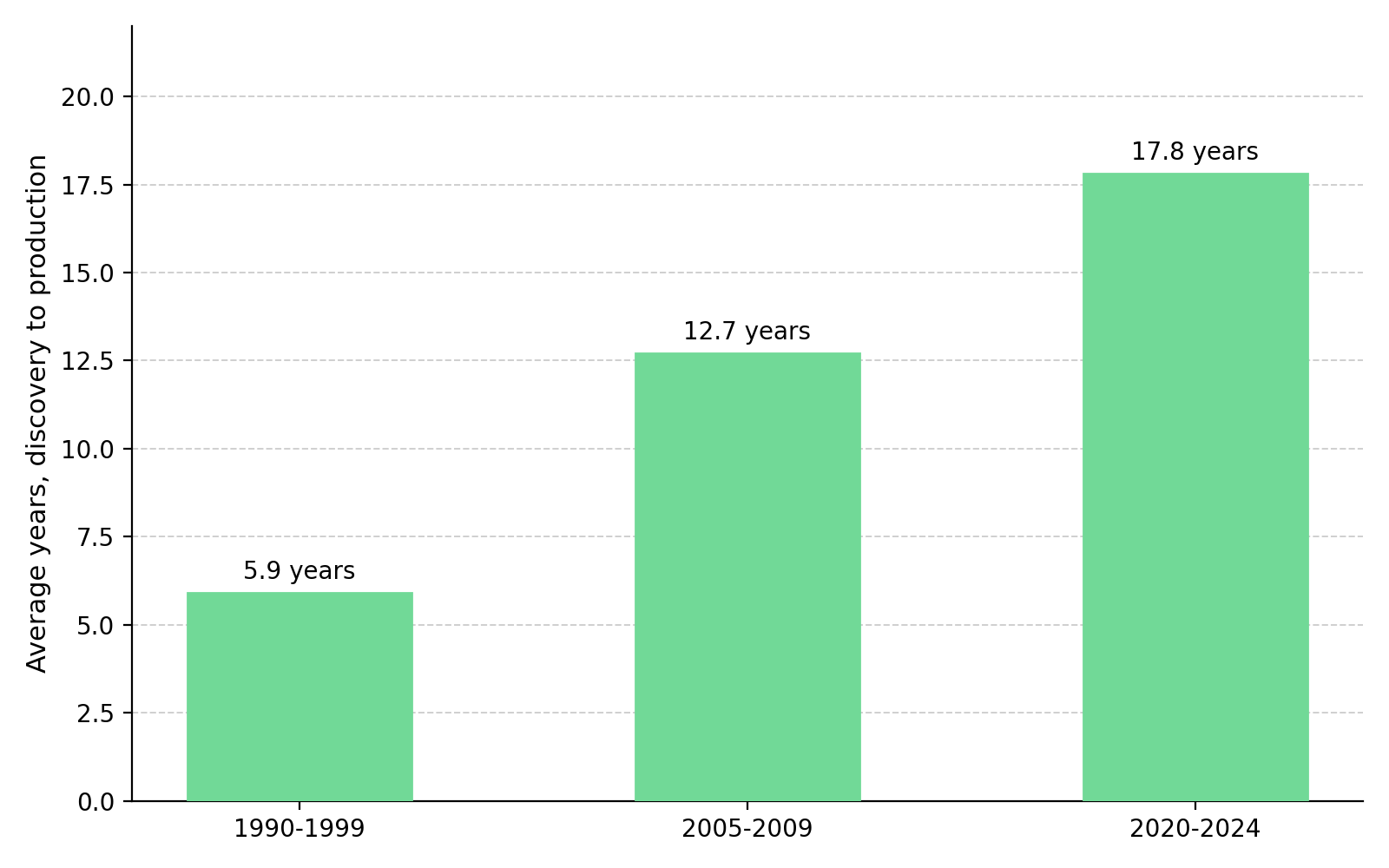

The concentrate shortage resulted from years of smelting capacity expanding faster than mine supply. Over the past several years, China added smelting capacity at roughly four times the rate of global concentrate supply growth. New smelters can be permitted, financed, and built within a few years. By contrast, a new copper mine typically requires a decade or more from discovery to first production, including resource definition, economic studies, permitting, and construction. Unlike smelter expansions, higher copper prices cannot accelerate the permitting, engineering, and construction needed to bring a new copper mine into production.

Despite committing to reduce output by more than 10 percent in 2026, Chinese refined copper production grew 7.4 percent year over year from January through April, showing that concentrate shortages had not yet reduced refined copper output. Because concentrate shortages increase the value of near-term mine supply, companies with defined reserves, realistic development timelines, or restart opportunities are more likely to secure financing and commercial interest than projects still defining a resource.

Long-Term Copper Pricing & Project Valuation

A shortage of copper concentrate supports higher long-term copper price assumptions, increasing project valuations and improving financing prospects. Developers use long-term copper price assumptions in feasibility studies to calculate post-tax net present value and internal rate of return, and continued concentrate shortages make higher long-term price assumptions more credible. Concentrate shortages also encourage offtake partners and cathode buyers to secure future supply before a final investment decision, improving financing prospects for development-stage projects.

Marimaca Copper is advancing the Marimaca Oxide Deposit toward a final investment decision in Chile's Antofagasta region. The project contains Proven and Probable reserves of 748,000 tonnes of contained copper, supporting a post-tax net present value of approximately US$1.1 billion at an 8 percent discount rate. Marimaca is also drilling the separate high-grade Pampa Medina target, providing additional exploration upside beyond the current reserve base. Hayden Locke, Chief Executive Officer of Marimaca Copper, highlights operating cost resilience amid market uncertainty:

"There's a lot of uncertainty caused by the Iran war. There's a lot of uncertainty caused by the sudden spike in asset prices. We're very comfortable that our assets will be significantly below US$300 a ton."

Near-Term Project Timing & Existing Infrastructure

Past-producing assets with existing infrastructure can offer a shorter path toward development than comparable greenfield discoveries. As new copper projects become harder to replace, exploration companies advancing these assets may attract greater market attention because they can potentially reach key development milestones sooner.

Selkirk Copper is advancing the past-producing Minto project in Yukon as a restart opportunity that could return copper supply faster than a greenfield development. An existing mineral resource estimate provides the foundation for an updated preliminary economic assessment, with a feasibility study and targeted production restart by mid-2028.

Acquisition Demand & High-Quality Discoveries

Recent acquisition activity shows that high-grade, large-scale exploration projects are attracting interest earlier in the development cycle as new copper discoveries become harder to replace. Mining companies with strong cash flow and declining development pipelines have driven much of this acquisition activity as they seek to replenish future reserves and production.

Abitibi Metals is advancing the B26 polymetallic deposit in Quebec's Abitibi Greenstone Belt, where the combined resource has grown to approximately 25.3 million tonnes grading 2.15 percent copper equivalent, a 124 percent increase since 2023. The company is targeting a preliminary economic assessment in the first quarter of 2027, marking the project's next major development milestone. Jon Deluce, Founder and Chief Executive Officer of Abitibi Metals, emphasizes demand for scarce copper-gold deposits:

"Many producers have gone on record saying copper-gold is the most sought-after deposit in the market today. We see that in recent M&A, including Foran. It speaks to the rarity of these opportunities and the demand for large, long-life assets, which we believe is what we're building at B26."

Constrained Mine Growth & Exploration Results

Exploration success in established copper jurisdictions becomes more valuable when the region's largest producers struggle to increase output, because new discoveries offer one of the few remaining sources of future mine supply. In that environment, a strong drill intercept provides evidence of additional resource potential in a district where existing producers face limited opportunities to replace declining mine supply.

Fitzroy Minerals is drilling the Buen Retiro copper project in Chile's Atacama region, where recent drilling returned 59.0 meters grading 1.73 percent copper. The company has expanded its 2026 drilling program to approximately 22,000 meters as it evaluates the project's resource potential. Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, frames limited copper supply growth and rising costs:

"Production growth in Chile, and globally, is difficult. It's a very mature industry struggling to maintain production. BHP says there will be zero growth from Chile between 2031 and 2040. The capital intensity of new projects is rising. All of this shows copper prices have to rerate."

Established Copper Districts & Discovery Potential

As new mine supply becomes more difficult to replace, projects located within proven copper districts become more strategically valuable because they offer additional opportunities to define economic mineralization beyond their existing resources.

Mogotes Metals is advancing the Albor discovery at its Filo Sur project in Argentina, where drilling returned 86 meters at 0.70 percent copper, including 43 meters at 1.1 percent copper. The project sits directly along strike from that discovery. Allen Sabet, Chief Executive Officer of Mogotes Metals, notes rare discoveries draw strong acquisition interest:

"There have been no other large discoveries like Filo in the last 30 years. When you start to clip into something like that, it attracts interest whether you want it or not."

Cobra Resources is advancing the Manna Hill copper project in a proven porphyry and skarn province in South Australia. The project sits within the same broader region as several Tier-1 copper deposits exceeding one million tonnes of contained copper, while recent drilling at the Blue Rose prospect returned intercepts including 74 meters at 1.02 percent copper. Together with Mogotes Metals, Cobra Resources shows how discovery and development results in established copper provinces are increasingly evaluated in the context of limited new mine supply.

Long-Term Mine Constraints & Project Selection

The zero-dollar treatment charge signals a shortage of mine supply rather than a short-term change in smelter economics. It resulted from years of mine supply growing more slowly than smelting capacity. That imbalance will not be resolved by a single price cycle, Fed decision, or trade policy ruling. Smelting capacity can be added within a few years, but a new copper mine typically requires a decade or more to reach production.

Because new copper mines take much longer to develop than smelters, concentrate shortages are likely to persist even if additional smelting capacity is built. Because new mine supply typically takes a decade or more from discovery to first production, today's concentrate shortage is likely to support copper prices and competition for new projects over multiple years. As a result, development-stage projects with strong economics and exploration companies advancing high-quality discoveries are likely to be evaluated more on project quality and execution than on short-term copper price movements.

The Investment Thesis for Copper

- A benchmark treatment charge of zero reflects a multi-year mine supply shortfall that additional smelting capacity cannot solve, supporting demand for development projects and high-quality copper discoveries.

- Developers with completed or near-complete economic studies and defined reserves may find it easier to secure project financing because concentrate shortages support higher long-term copper price assumptions used in net present value and internal rate of return models.

- Past-producing assets with existing mill, camp, and processing infrastructure offer a more capital-efficient path back to production than greenfield developments, shortening development timelines and reducing capital requirements.

- High-grade exploration results in established Tier-1 copper provinces are more likely to attract acquisition interest because producers need new discoveries to replace declining reserves and future production.

- Projects with existing infrastructure and well-defined development pathways may require less new capital and reach key development milestones sooner than comparable greenfield projects.

- Because new copper mines typically require a decade or more to reach production, demand growth from electrification, grid investment, and data center expansion is likely to keep competition for new copper projects elevated over multiple years.

A zero-dollar treatment charge shows that mine supply, rather than smelting capacity, has become the limiting factor in the copper market. The focus shifts from short-term copper price movements to companies capable of advancing new mine supply through defined reserves, economic studies, and realistic development timelines while concentrate remains in short supply. Reserve-backed developers, restart projects with existing infrastructure, and exploration projects in established copper districts are positioned to benefit from a market where new mine supply remains difficult to replace over multiple years.

TL;DR

Chinese smelters accepted a record benchmark treatment charge of US$0 per tonne for copper concentrate in 2026, confirming that mine supply, rather than refining capacity, has become the main constraint on global copper production. Because new copper mines typically require a decade or more to reach production, concentrate shortages are likely to support stronger long-term project economics, financing prospects, and acquisition activity. Development projects with robust economics and exploration companies advancing high-quality discoveries in established copper districts are positioned to benefit as producers seek new sources of future supply.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed