Queensland's Explorer Partners with Santos to Target Major Gas Resource

Elixir Energy is capitalizing on a world-class Queensland gas opportunity, with a key well in Q3 2025 set to demonstrate commerciality and further de-risk the large-scale play.

- Elixir Energy has shifted focus to a substantial gas project in Queensland, Australia

- Recently completed a deal with Santos to expand acreage and de-risk the play

- Drilling key well in Q3 2025 to prove commerciality, with additional wells planned

- Benefiting from Shell's ongoing work in adjacent blocks that is validating the play

- Aiming for a farm-out deal in 2025 on 100% owned acreage to further de-risk

Australian energy company Elixir Energy (ASX:EXR) has positioned itself to capitalise on the increasingly favorable dynamics in the Queensland gas market through its substantial acreage position in a highly prospective region. The company's recent deal with Australian major Santos has expanded its footprint and significantly de-risked the play, setting the stage for value creation in the near-term.

Pivoting Focus to Queensland Gas

Elixir's strategic shift to focus on Queensland gas began three years ago, diversifying away from its prior Mongolian assets in recognition of changing geopolitical factors. As MD and CEO Neil Young explains:

"Geopolitical events occurred in the McMillan sense and we reacted to them - those events obviously being the sudden invasion of Ukraine and the deepening of the general cold war between the west and China/Russia."

This pivot has proven prescient, with Elixir achieving enormous success in adding acreage, undertaking work, and de-risking the Queensland play. The region is highly advantaged, with strong gas pricing, established infrastructure, and increasing recognition of natural gas as essential for the energy transition. Elixir's early mover position has enabled it to build a dominant land position in the heart of the play.

Interview with Managing Director & CEO, Neil Young

Santos Deal Expands & De-Risks Position

Elixir's recently completed deal with Santos, Australia's second largest oil and gas company, represents a major milestone for the company. Through the deal, Elixir gains a 50% stake in two key permits that are contiguous with its existing 100% owned acreage. Santos was motivated to pursue the deal to gain more time on its exploration commitments. As Young describes:

"Santos have got a couple of very large development projects - the board's incentivised management to focus on those, and this longer dated asset fell down the focus areas."

The deal structure leverages the respective strengths of each company. Elixir operates and pays for the initial well to earn its 50% interest, meeting the permit's exploration commitments. Santos then resumes operatorship for the long-term development, bringing its significant capabilities to bear. The deal expands Elixir's exposure to the play while introducing a highly capable long-term partner.

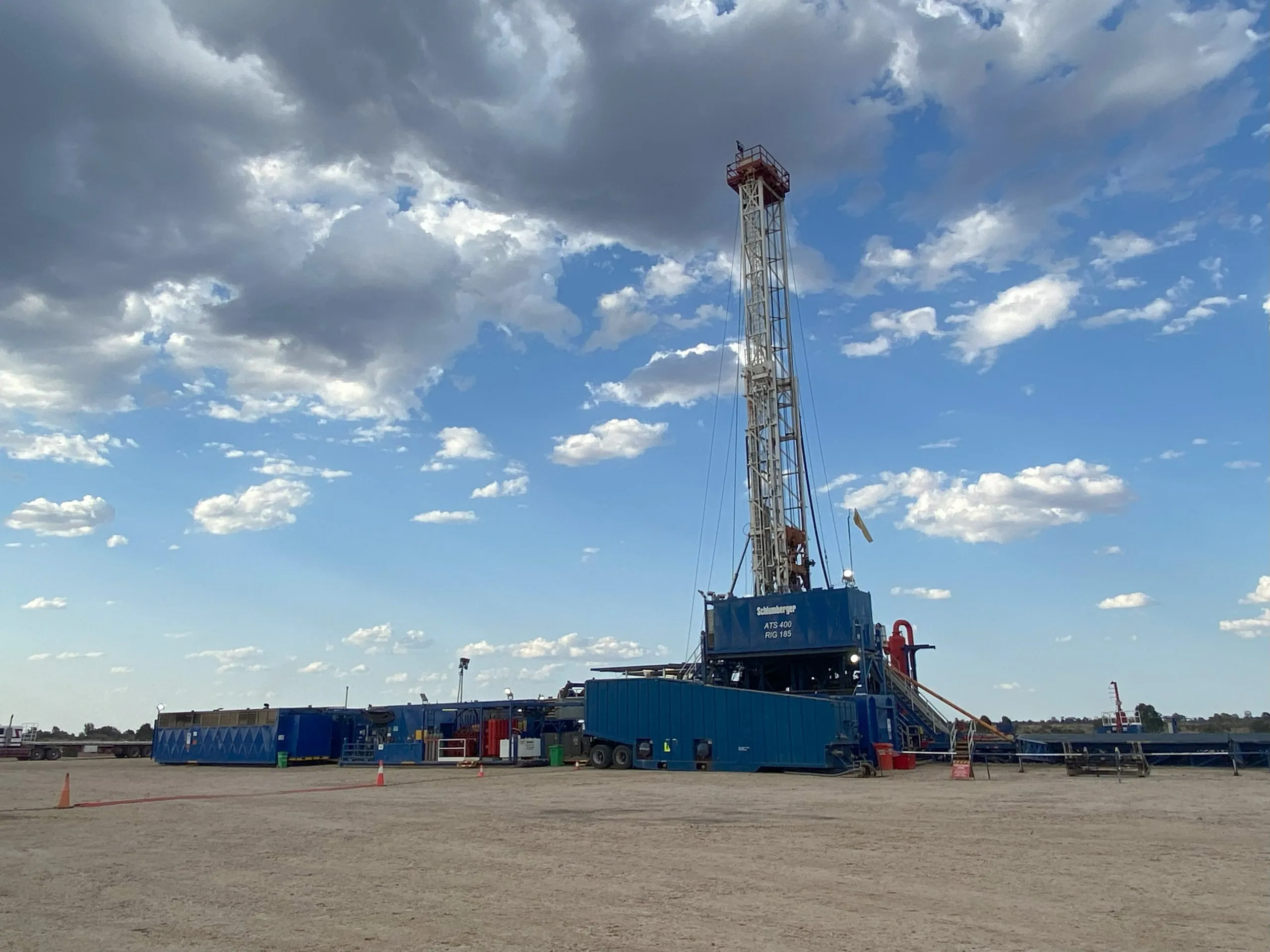

Key Well Planned for Q3 to Prove Commerciality

Elixir plans to drill a key well on the Santos acreage in Q3 2025 to a depth of just over 3,000 m. This well is designed to prove the commerciality of the play by testing productivity and liquids content in an up-dip location that is expected to be more liquids-rich. Commercial flow rates, supported by condensate yields and the region's premium gas pricing, would serve to demonstrate the economic viability of the play.

Elixir's cost exposure is limited, with the well expected to cost distinctly less than $10 million. Roughly half of this is anticipated to be funded through an R&D tax credit from the Australian government. This leveraged risk/reward setup means a successful outcome could be highly value accretive for Elixir.

Additional Wells De-Risk the Play

Beyond the key Q3 well, Elixir has a multi-pronged approach to further demonstrate the potential of the play:

- Planning to drill the Diona-1 conventional well in mid-2025, farm-out discussions underway

- Actively monitoring activity of adjacent operators, particularly Shell and a nearby public company

- Aiming to secure a farm-in partner for its 100% owned acreage to fund further drilling

The Diona Well provides potential for near-term cash flow given its shallow depth and proximity to pipelines. Meanwhile, success by Shell or other nearby operators would serve to meaningfully de-risk Elixir's acreage given the homogeneous nature of the play. Finally, securing a farm-in on the 100% owned block could bring a significant new source of drilling capital.

Benefiting from Shell's Validation of the Play

Shell's ongoing investment in its adjacent acreage is serving to validate the potential of the Taroom Trough play that extends into Elixir's acreage. Shell originally entered the play via its acquisition of BG Group, which had spent ~$300 million in the region. Shell has subsequently invested heavily, with hundreds of millions in additional spending.

Although Shell maintains a low profile, it's clear the major is achieving success. As Young notes:

"What we do know is their predecessor company, British Gas, spent $300 million on this about 12 years ago, Shell came back 2-3 years ago and has probably spent another $200 million. What they've expressed verbally is they'll drill more wells and do more seismic this year - there's another few million dollars."

Young sees Shell's continued investment as enormously encouraging for the play's potential.

Taroom Trough Represents Enormous Opportunity

The Taroom Trough represents a large, homogeneous unconventional gas play that is increasingly being recognised as a world-class opportunity. Elixir estimates its acreage alone contains over 30 TCF of gas-in-place in the deep coals, with additional potential in other horizons. While the deep coals currently have a low estimated recovery factor of <1%, Young sees this as an engineering challenge rather than a geologic one.

With further appraisal and application of unconventional technologies like horizontal drilling and hydraulic fracturing, Elixir sees potential for the play to be commercialised at increasingly large scale over time. As Young explains,

"Because this is an unconventional play located immediately proximate to infrastructure, it doesn't need a single FID with a big signing ceremony and billions in spending. Here you can incrementally spend tens of millions, feed markets that are small to start, then build up your infrastructure and do more drilling to ultimately feed into much larger markets."

The Right Location at the Right Time

Queensland represents an ideal location for Elixir to be pursuing this play. Regional gas prices are currently around $14/GJ at the Wallumbilla Hub, amongst the highest in the world. Forward projections suggest a tightening market, with LNG imports into Southern Australia expected to drive $20+ price signals as soon as 2025. This provides strong economic underpinning for the commercialisation of the play.

At the same time, Queensland has a stable fiscal regime and a government that is highly supportive of gas development given the royalties and economic benefits it provides. Australia as a whole is increasingly recognizing gas as essential for energy security and to support decarbonisation via displacement of coal. Federal policy has become more pragmatic in recent years, with a recognition that gas is needed through the energy transition.

The Path Forward

Elixir is well-positioned to continue advancing its Queensland gas position through a combination of drilling/appraisal on its own acreage and monitoring of industry activity nearby. The Santos deal and planned Q3 well provide potential for a clear commerciality proof-point in the near-term. Continued drilling and a potential farm-out of the 100% owned acreage could further expand and de-risk the opportunity.

Importantly, Elixir has a management team that knows how to get things done. Young and much of the technical/commercial team have prior experience with Santos, providing key relationships and credibility. Elixir's ability to complete the recent deal demonstrates the team's savvy and nimbleness in expanding its position. As Young describes it,

"We came up with a solution that met their needs - it needed to be done quickly, it needed to be done nimbly."

With a dominant acreage position in a world-class gas play and an active program to demonstrate commerciality, Elixir Energy represents a compelling opportunity in the Australian energy sector. Near-term catalysts and continued de-risking of the play provide potential for significant uplift in the coming months and years.

The Investment Thesis for Elixir Energy

- Large acreage position in world-class Queensland gas play, validated by Shell activity nearby

- Santos farm-in deal expands position and introduces capable long-term partner

- Drilling key well in Q3 2025 provides potential proof-point for commercial flow rates

- Additional planned wells and farm-out of 100% owned acreage provide further catalysts

- Robust Queensland gas market with $14+/GJ prices and further tightening expected

- Stable regulatory environment with government highly supportive of gas development

- Management team with strong Santos relationships and demonstrated ability to get deals done

- Near-term catalysts provide potential for significant re-rating as play is further de-risked

Macro Thematic Analysis

The global energy transition is creating opportunities for nimble companies to create value, particularly in gas which is increasingly recognised as a key transition fuel. Elixir Energy's Queensland gas position exemplifies this theme.

As Neil Young describes it:

"Anybody who knows energy deeply knows that you need everything, not just something. Renewables have their place and that's great, but the more of them, the more you need gas to balance the system. Batteries are fine for a few hours, but if you have a period of days or weeks, even politicians know they're not going to be voted back in if there are blackouts."

This pragmatic view is taking hold in Australia, where policymakers are embracing gas as essential for energy security and economic growth. Companies like Elixir that are positioned in the right basins with the right management teams stand to benefit. With increasing recognition of the long-term role for gas, the macro backdrop is highly favourable for Elixir as it advances its Queensland position in the coming months and years.

Young summarised the opportunity:

"We've never been in such a strong position in terms of resource per share before and we're also benefiting not only from the work that we do, but which others do too. So that's a lot of leverage to our outcomes as well - it's money that we're not spending that's helping, as well as the money that we will spend."

Analyst's Notes

Subscribe to Our Channel

Stay Informed