Refined Silver Shortages and Lease Rates Drive Prices Above $52.50: New Cost Curve and Capital Rotation Into High-Grade Producers

Silver surges past $52.50/oz on tight supply, 30%+ lease rates, and fifth consecutive deficit. Solar demand and Fed cuts drive structural rally toward $78/oz.

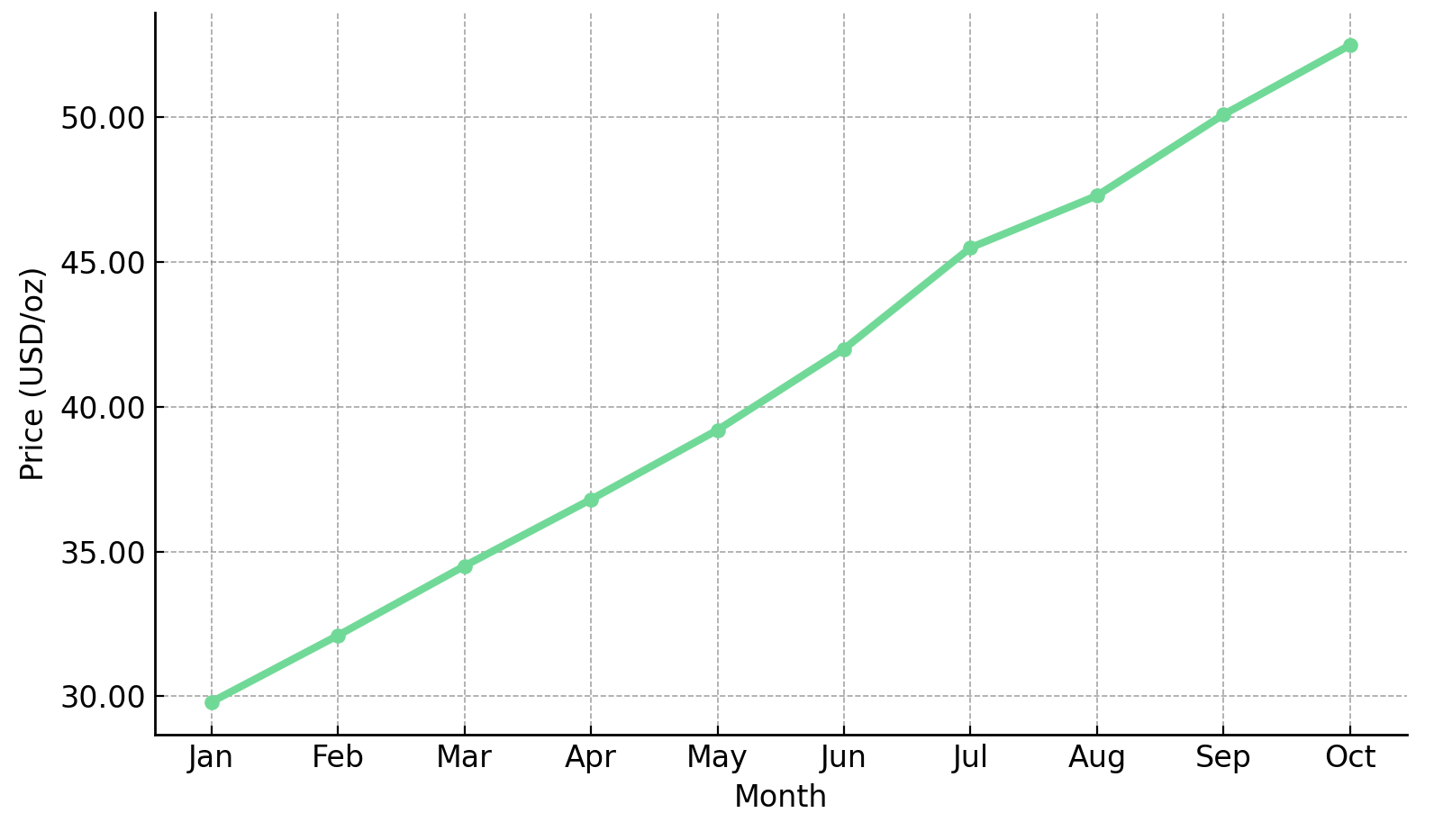

- Silver prices surged above $52.50 per ounce in October 2025, marking a 76% year-to-date gain and reflecting the strongest rally since 2011.

- The rally is driven by tight liquidity in London and New York, soaring lease rates above 30%, and a fifth consecutive global supply deficit.

- Macroeconomic catalysts include Federal Reserve rate-cut expectations, a weaker United States dollar, and persistent inflation hedging demand.

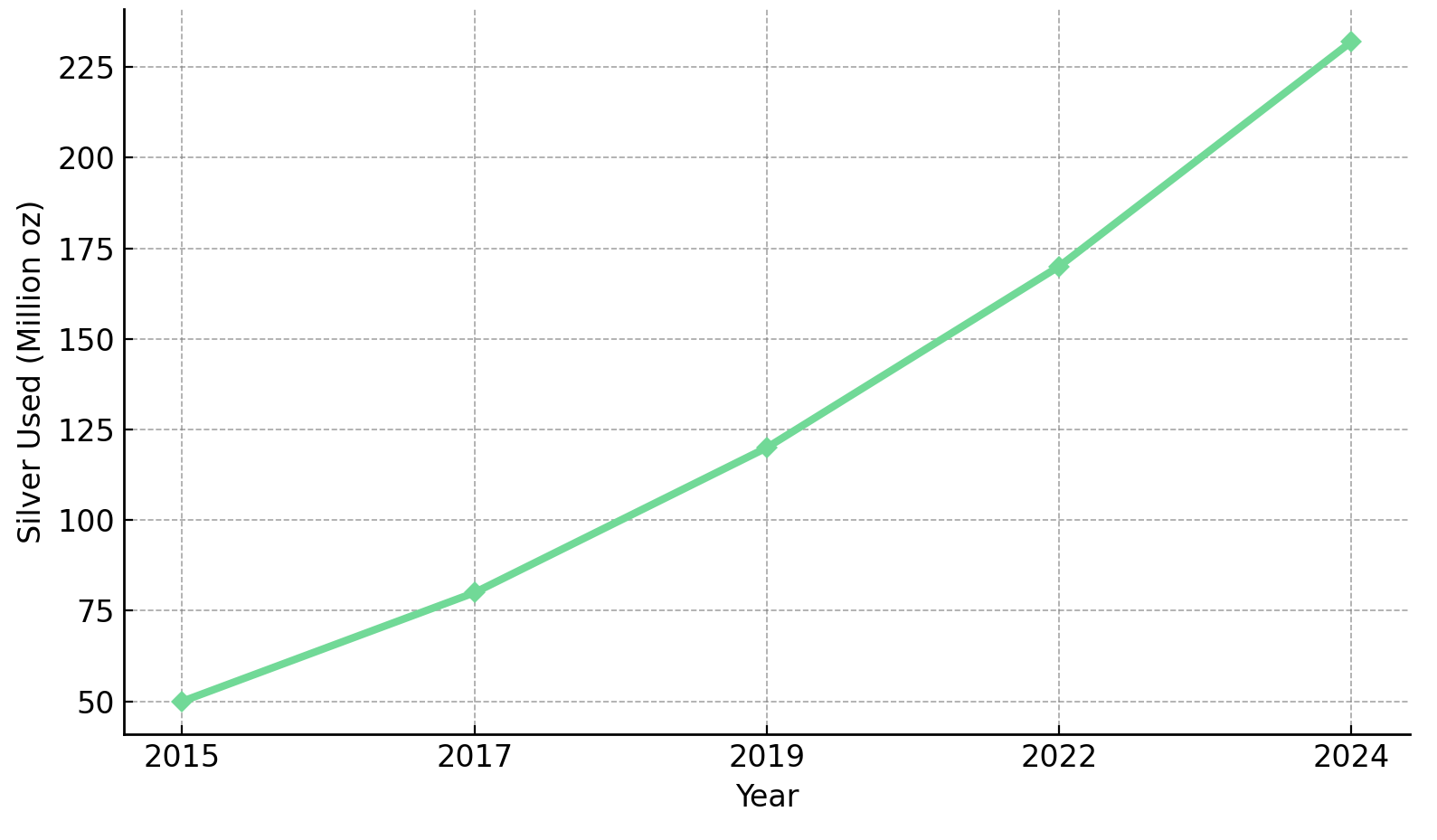

- Industrial consumption, led by the solar photovoltaic sector at 232 million ounces in 2024, has become the largest structural growth engine in silver's dual market identity.

- Silver-focused producers and developers such as Americas Gold & Silver, Cerro de Pasco Resources, Vizsla Silver, and GR Silver Mining stand to benefit as supply bottlenecks and investor inflows reinforce a secular bull market.

Persistent Physical Shortages and Policy Shifts

Silver's ascent past $52.50 per ounce in October 2025 underscores the intersection of macroeconomic and physical market pressures unseen in over a decade. With prices up 76% year-to-date and 168% from 2022 levels, the rally reflects deep structural imbalances in supply, compounded by global liquidity strains and shifting monetary expectations.

London lease rates have surged more than 30%, signaling acute scarcity of deliverable metal in the over-the-counter market. Meanwhile, traders report rolling short positions at unsustainable costs, intensifying volatility. Inventory levels of deliverable silver have fallen steadily throughout the year, declining over 20% as refiners and traders bid up available supply amid mounting demand pressure.

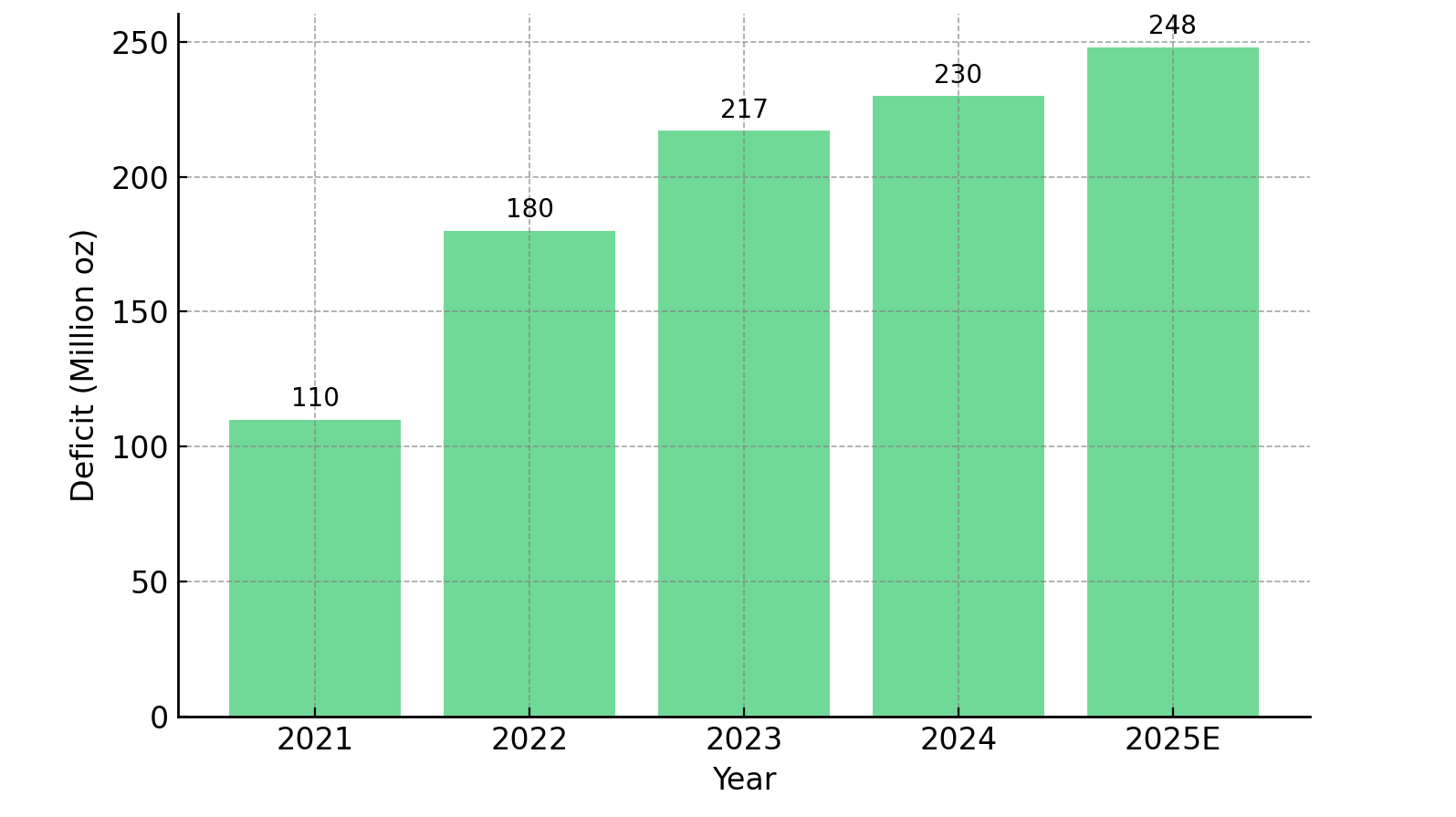

The broader context reveals a fundamental repricing of silver as both a monetary hedge and an industrial necessity. Global silver consumption is expected to exceed supply for the fifth consecutive year in 2025, creating a structural deficit that reinforces upward price momentum. This tightness is not a temporary dislocation but rather the result of years of underinvestment in primary silver production, compounded by supply chain bottlenecks and rising industrial consumption.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold & Silver, captures the operating environment:

"The core mine was shut down when silver prices were $12 to $13 an ounce. We are now more than $30 above those prices, which is phenomenal. The economics in some of these areas are just leaping off the page at us."

This repricing is forcing market participants to reassess long-term supply adequacy and the valuation framework for silver-exposed equities. Producers with low all-in sustaining costs and developers advancing scalable projects are emerging as primary beneficiaries of this structural shift.

Safe Haven Flows, Inflation & Policy Reversal

Silver's price surge is as much a reflection of macro policy dislocation as it is of market fundamentals. Investors are reallocating capital into tangible stores of value amid Federal Reserve rate cut expectations, a weakening United States dollar, and persistently high inflation eroding real bond yields.

The Federal Reserve's quarter-point rate cut this month, with a likely follow-up move in December, has undermined the appeal of yield-bearing assets and boosted non-yielding alternatives like precious metals. Lower interest rate expectations reduce the opportunity cost of holding silver, while simultaneously weakening the dollar and making dollar-priced commodities more affordable for foreign buyers. This dynamic has intensified global demand, particularly from buyers in India and Asia, further straining already tight supply.

Safe-Haven Bid Amid Geopolitical & Fiscal Stress

Tensions across the United States, Europe, and Asia, ranging from United States fiscal gridlock and government shutdown concerns to instability in France and Japan, have reinforced silver's monetary role alongside gold. Economic uncertainty and mounting global debt pressures are driving investors toward precious metals as a hedge against sovereign risk and currency debasement.

Silver's smaller market capitalization magnifies price reactions, often moving 1.7 times faster than gold during flight-to-quality episodes. This amplification effect has been evident throughout 2025, as institutional capital has rotated into metals exchange-traded funds and physical silver contracts in response to geopolitical instability and shifting United States-China trade dynamics.

Inflation Hedge & Bond Market Disconnect

With core inflation remaining sticky and yields failing to compensate for purchasing power loss, institutional capital is re-entering metals ETFs and physical silver contracts. Silver's affordability versus gold offers leveraged exposure for investors seeking inflation protection without the capital commitment required for gold allocations.

Inflows into major silver ETFs such as iShares Silver Trust, Global X Silver Miners ETF, and abrdn Physical Silver Shares ETF have surged in tandem with the physical squeeze, reflecting investor conviction that inflation will remain elevated and real yields will stay compressed. This dynamic is particularly pronounced among retail buyers and hedge funds re-establishing long positions as volatility increases.

Deficits Deepen as Industrial Demand Accelerates

The physical market tightness is now the central narrative. The fifth consecutive annual deficit and falling inventories at COMEX and LBMA vaults highlight structural shortages that are reshaping price discovery mechanisms in both spot and futures markets.

Deliverable inventories have declined by over 20% year-to-date, forcing refiners and traders to bid up available supply. This shortage is not confined to financial markets, it extends across the entire supply chain, from mining operations to refining capacity to logistics networks. Supply disruptions, reduced mine output, and delays in shipment have created bottlenecks that amplify price pressures and extend delivery cycles.

Renewable Energy & Photovoltaic Growth

Industrial demand remains the largest catalyst, led by solar photovoltaic installations consuming 232 million ounces of silver in 2024, up fivefold from 2015. With governments accelerating renewable buildouts under Net Zero policies, demand is set to outpace supply through 2027 and beyond.

Silver is essential for the solar energy sector due to its superior electrical conductivity, which maximizes photovoltaic efficiency. As global solar capacity expands to meet climate commitments, silver consumption in this sector alone is expected to absorb a growing share of total supply, leaving less available for financial investment and other industrial applications. Wind turbine technology, electric vehicles, advanced electronics, and semiconductors represent additional demand vectors that are structurally expanding silver's industrial footprint.

Supply Constraints & Refining Bottlenecks

Refining backlogs and logistics bottlenecks have delayed delivery cycles, amplifying price pressures. Primary silver output remains stagnant as multi-metal mines prioritize zinc and lead over silver credits, creating a gap between rising consumption and flat production growth.

This dynamic is particularly acute for producers operating at high grades with low all-in sustaining costs. Americas Gold & Silver is positioned to capture higher margins at its Galena Complex in Idaho, the Cosalá Operations in Mexico, including the San Rafael mine and EC120 development project targeting all-in sustaining costs of $10.80 per ounce, a fraction of current spot prices. The company's focus on high-grade operations ensures profitability even in volatile price environments, while byproduct credits from lead, copper, gold, and antimony provide additional margin support.

Cerro de Pasco Resources exemplifies a low-cost reprocessing model, turning tailings at approximately $1 to $2 per ton into silver-equivalent production. This approach aligns with environmental, social, and governance mandates for resource recycling while delivering cost structures that provide substantial margin expansion at current prices.

Steven Zadka, Executive Chairman of Cerro de Pasco Resources, highlights the offtake interest:

"There's going to be 20 offtakers lined up at the door, all competing with each other. They would be doing that for any other opportunity, not because we're special, but because of the market conditions."

Silver's Repricing Through the Energy Transition

Silver's dual identity, monetary and industrial, is now converging under the global electrification and decarbonization trend. Beyond photovoltaics, silver is critical in electric vehicle electronics, wind turbine conductors, 5G systems, and medical applications. This convergence is driving a fundamental reassessment of silver's long-term value proposition.

The energy transition represents a multi-decade demand tailwind that is structurally different from cyclical industrial demand. Unlike traditional electronics or manufacturing applications, renewable energy infrastructure requires upfront silver consumption that cannot be easily substituted or deferred. This creates demand visibility that extends well beyond typical commodity cycles, providing a foundation for sustained price support even during periods of economic weakness.

Structural Undervaluation Relative to Gold

Despite a 7-to-1 physical supply ratio, silver trades near 90-to-1 versus gold, highlighting its undervaluation. As investors rotate into industrial hedges and recognize silver's essential role in the energy transition, this disconnect may narrow sharply. Historical precedent suggests that gold-silver ratio compressions can occur rapidly during periods of industrial demand acceleration and monetary policy shifts.

The current valuation gap reflects decades of silver being perceived primarily as a byproduct metal with limited monetary significance. However, the emergence of structural industrial demand combined with traditional safe-haven flows is forcing a revaluation of this framework. Institutional allocations are shifting from gold-dominant portfolios toward silver as a higher beta inflation hedge with embedded industrial leverage.

Environmental, Social & Governance Alignment and Circular Economy Premium

Projects integrating environmentally, socially, and governance-friendly production models, such as reprocessing tailings or utilizing low-carbon energy inputs, are gaining valuation premiums. Cerro de Pasco Resources is positioned at the intersection of environmental, social, and governance restoration and metal recovery, benefiting from policy shifts favoring circular economy approaches.

Vizsla Silver, with its 361 million ounces silver-equivalent Panuco Project having a completed PEA by July 2025 with all-in sustaining costs at $9.40 per ounce and internal rate of return of 86%. This reflects scalability in a rising-price environment, supported by robust resource expansion and efficient mine planning.

Jesus Velador, Vice President of Exploration at Vizsla Silver, outlines the resource progression:

"What we accomplished is over 60,000 meters of infill drilling, which resulted in a 43% increase in the measured and indicated category."

Capital Flows, Leverage & Institutional Positioning

Silver ETFs and futures open interest have surged in tandem with the physical squeeze. Institutional allocations are shifting from gold-dominant portfolios toward silver as a higher beta inflation hedge, while hedge funds are re-establishing long positions as volatility increases and momentum builds.

The structural shift in capital flows reflects a broader recognition that silver offers asymmetric exposure to both monetary debasement and industrial growth themes. Unlike gold, which functions primarily as a monetary asset, silver provides embedded leverage to the energy transition while maintaining its traditional role as an inflation hedge. This dual exposure is attracting capital from both traditional commodity investors and thematic investors focused on decarbonization and electrification.

Renewed Investor Participation

Inflows into major silver ETFs reflect investor conviction that the current price environment is sustainable. Sharp increases in ETF holdings have strained physical supply, as fund managers compete with industrial buyers and refiners for deliverable metal. This dynamic has pushed premiums on physical bars and coins to multi-year highs, signaling robust retail demand alongside institutional interest.

Producers, Developers & Explorers Gaining Market Recognition

Equity valuations are beginning to reflect silver's new price base, though many producers and developers remain undervalued relative to their operating leverage and growth potential. Americas Gold & Silver's balance sheet recapitalization, including C$50 million in equity and US$35 million in debt reduction, positions the company for leverage to silver's upside without the dilution risk that typically constrains junior miners.

GR Silver Mining, under exploration, trades at a significant discount to peers on an enterprise value per ounce basis. This valuation gap offers substantial re-rating potential as new zones like San Marcial Southeast advance. The company's permitted status and jurisdictional advantage in Mexico reduce long-term risk and enable rapid progression toward pilot-scale production.

Marcio Fonseca, President and Chief Executive Officer of GR Silver Mining, emphasizes the company’s strategic positioning:

"People are becoming more aware of the value of Plomosas as a permitted asset… We want to concentrate the remaining funding on resource expansion because that's going to be fundamental for the upcoming PEA."

Risk Factors: Volatility, Policy Lag & Correction Scenarios

While the structural bull case remains intact, silver's volatility is a double-edged sword. Prices can swing 1.7 times gold's volatility, and corrections often exceed 10% within short windows. Investors must acknowledge the potential for sharp pullbacks even as the long-term trajectory remains constructive.

Monetary risk represents a key downside scenario. Delayed Federal Reserve easing or unexpected rate hikes could pressure short-term sentiment and trigger profit-taking among leveraged investors. Speculative positioning amplifies correction risk, as thin liquidity in physical markets can magnify downside moves when momentum reverses.

Fiscal and industrial demand sensitivity also warrants attention. A slowdown in global manufacturing or a delay in renewable energy buildouts could moderate physical demand, reducing support for prices. However, the structural nature of industrial consumption, particularly in solar photovoltaics, suggests that demand is relatively inelastic to short-term economic fluctuations.

High-cost producers with all-in sustaining costs above $25 per ounce remain vulnerable to pullbacks, reinforcing the investment edge for low-cost producers like Americas Gold & Silver. Companies with strong balance sheets, operational flexibility, and low production costs are best positioned to weather volatility while capitalizing on structural price support.

The Investment Thesis for Silver

The convergence of structural deficits, policy-driven industrial expansion, and monetary hedge appeal creates a compelling case for silver exposure through quality producers and developers.

- Structural deficit persistence through 2025 and beyond, with inventories near decade lows and consumption outpacing supply for the fifth consecutive year.

- Policy-driven industrial expansion in solar photovoltaics, electric vehicles, and 5G infrastructure creating multi-year demand visibility that is largely inelastic to economic cycles.

- Monetary and inflation hedge appeal as real yields turn negative and investors seek tangible stores of value amid fiscal uncertainty and currency debasement risks.

- Undervaluation versus gold, with the current 90-to-1 ratio implying 30% to 40% potential upside on mean reversion toward historical norms.

- Operational leverage through operators like Americas Gold & Silver and Vizsla Silver exhibiting sub-$11 per ounce all-in sustaining costs, positioning for high free cash flow generation at current spot prices.

- Environmental, social, and governance alignment and circular recovery premiums for developers like Cerro de Pasco Resources that integrate resource recycling and low-carbon production models.

- Exploration upside through juniors like GR Silver Mining offering asymmetric exposure to price momentum with low enterprise valuations relative to resource potential.

- Development timelines aligned with multi-year demand growth trends, as feasibility studies and permitting milestones coincide with peak industrial consumption and investor inflows.

Monetary Metal for the Decarbonized Age

Silver's breakout above $52.50 per ounce represents more than a cyclical rally, it signals a structural repricing of a metal central to both the global financial hedge narrative and the green industrial revolution.

With forecast prices nearing $78 per ounce by late 2026, investors are re-evaluating silver's role as both an industrial necessity and a monetary reserve asset. Low-cost, well-capitalized producers and developers with scalable resources are emerging as prime beneficiaries of this dual dynamic, offering exposure to both inflation protection and decarbonization themes.

As the market transitions from scarcity-driven panic to strategic accumulation, silver stands as a bellwether for the next phase of commodity revaluation, one grounded in real assets, renewable infrastructure, and systemic inflation hedging. The confluence of tight physical supply, accelerating industrial demand, and macroeconomic uncertainty positions silver as a core holding for investors seeking resilience and growth in an increasingly volatile global landscape.

TL;DR

Silver's breakthrough above $52.50 per ounce marks a structural repricing driven by acute physical shortages, surging industrial demand, and macroeconomic dislocation. London lease rates exceeding 30% signal unprecedented tightness as deliverable inventories decline over 20% year-to-date. The fifth consecutive annual deficit reflects accelerating consumption from solar photovoltaics—232 million ounces in 2024 alone—while Federal Reserve rate cuts and persistent inflation drive safe-haven flows. Trading at a 90-to-1 ratio versus gold despite a 7-to-1 supply ratio, silver remains fundamentally undervalued. With forecast prices targeting $78 per ounce by late 2026, low-cost producers with sub-$11 all-in sustaining costs are positioned to capture exceptional margins as the energy transition and monetary hedge demand converge in a secular bull market.

FAQs (AI-Generated)

The rally is driven by a combination of structural supply deficits (the fifth consecutive year consumption exceeds production), extremely tight physical liquidity in London and New York with lease rates above 30%, Federal Reserve rate cuts weakening the dollar, persistent inflation driving safe-haven demand, and accelerating industrial consumption from solar photovoltaic installations. These factors have created unprecedented upward pressure on prices.

Solar photovoltaic installations consumed 232 million ounces of silver in 2024—up fivefold from 2015—making it the largest industrial growth driver. Silver's superior electrical conductivity is essential for maximizing photovoltaic efficiency, and as governments accelerate renewable energy buildouts under Net Zero policies, this demand is expected to outpace supply through 2027 and beyond, creating multi-year structural support for prices.

Silver offers leveraged exposure to both monetary hedge themes and industrial growth, particularly the energy transition. Despite a 7-to-1 physical supply ratio with gold, silver trades near 90-to-1, suggesting 30-40% upside potential on mean reversion. Silver's smaller market capitalization means it moves 1.7 times faster than gold in both directions, offering higher beta exposure for investors seeking inflation protection and industrial demand leverage, though with greater volatility risk.

Key risks include high volatility (silver can swing 1.7 times gold's volatility with corrections often exceeding 10%), monetary policy uncertainty (delayed Federal Reserve easing or unexpected rate hikes), slowdowns in global manufacturing or renewable energy buildouts, and speculative positioning that amplifies downside moves in thin liquidity conditions. High-cost producers with all-in sustaining costs above $25 per ounce remain particularly vulnerable to pullbacks.

Investors can access silver through physical bullion, exchange-traded funds like iShares Silver Trust (SLV), Global X Silver Miners ETF (SIL), and abrdn Physical Silver Shares ETF (SIVR), or through equity positions in silver producers and developers. Low-cost producers with all-in sustaining costs below $11 per ounce offer leveraged exposure to price appreciation, while developers with scalable resources and strong feasibility economics provide growth-oriented positioning in the structural bull market.

Analyst's Notes

Subscribe to Our Channel

Stay Informed