Resource Nationalism Tightens Critical Metals Supply & Rewards Ex-China Assets as China Refines 70% of Strategic Minerals

Battery and critical-metals prices are increasingly driven by government supply controls, making low-cost, well-financed projects outside China more attractive to investors.

- Battery and critical-metals prices are now driven more by sovereign supply controls than electric-vehicle demand, with the International Energy Agency reporting that China leads refining for 19 of 20 strategic minerals at an average market share of roughly 70%.

- A more hawkish United States Federal Reserve and a firmer dollar are a near-term headwind for dollar-priced metals, even as structural supply tightness builds, leaving investors with a genuinely two-sided market.

- Export controls and quotas have increased the premium for battery and critical metals sourced outside China, supporting higher valuations for low-cost assets in Western-aligned jurisdictions.

- The main constraint on new battery and critical-metals supply has shifted from geology to financing, with government-backed capital from the US, Canada, Australia and the World Bank Group helping developers fund projects with less reliance on new equity.

- The main risks to this thesis are China relaxing its export controls, faster-than-expected adoption of sodium-ion and cobalt-light battery chemistries, and delays in permitting or project financing.

Supply Controls Replace EV Demand in Battery Metals Pricing

For most of the past decade, battery and critical metals were priced as a clean-energy demand bet. Lithium, nickel, cobalt, graphite and the rare earths rose and fell with forecasts for electric-vehicle adoption. That relationship has weakened as government policy has become a larger driver of supply and pricing than demand forecasts. In 2026, spot and term prices are driven more by export bans, quotas, royalties and processing mandates imposed by the small number of countries that dominate global supply than by demand forecasts. This shift reflects resource nationalism, where governments use control over critical mineral supply to capture more value or advance strategic interests, making policy decisions a larger driver of project economics than demand alone.

The concentration data explains why a policy lever works. The International Energy Agency reports that China is the leading refiner for 19 of 20 strategic minerals, with an average market share of about 70%, and that it produces roughly 94% of the world's sintered permanent magnets. When one country controls that much of a processing step, an administrative decision in Beijing can reset a global price faster than any shift in the demand curve. The same logic now applies to mined supply in the Democratic Republic of Congo for cobalt and in Indonesia for nickel. For investors, the consequence is that jurisdiction and cost position, rather than headline resource size, have become the primary levers of value.

The complicating factor is the macro backdrop, which pulls the other way in the near term. At its June 2026 meeting the United States Federal Reserve, under new Chair Kevin Warsh, held its policy rate at 3.50 to 3.75%, dropped its prior easing bias and lifted the median projection for year-end to 3.8%, according to the Federal Reserve and reporting from CNBC. A firmer dollar raises the cost of dollar-priced metals for overseas buyers. At the same time, a de-escalation in the United States and Iran conflict pushed oil to its lowest level since that war began, with West Texas Intermediate briefly below 70 dollars a barrel, per CNN. The result is a market in which structural scarcity and soft near-term prices coexist. That is an entry-timing problem, not a contradiction..

Export Controls & Quotas Drive Battery Metals Pricing

Governments use different supply controls across battery and critical metals, but each policy increases their influence over global prices. In rare earths, China's dual-use export licensing remains a constraint despite a partial suspension under the late-2025 Busan trade truce through roughly November 2026. The Center for Strategic and International Studies reports that some heavy rare-earth shipments to the US remain well below pre-restriction levels and have collapsed year over year.

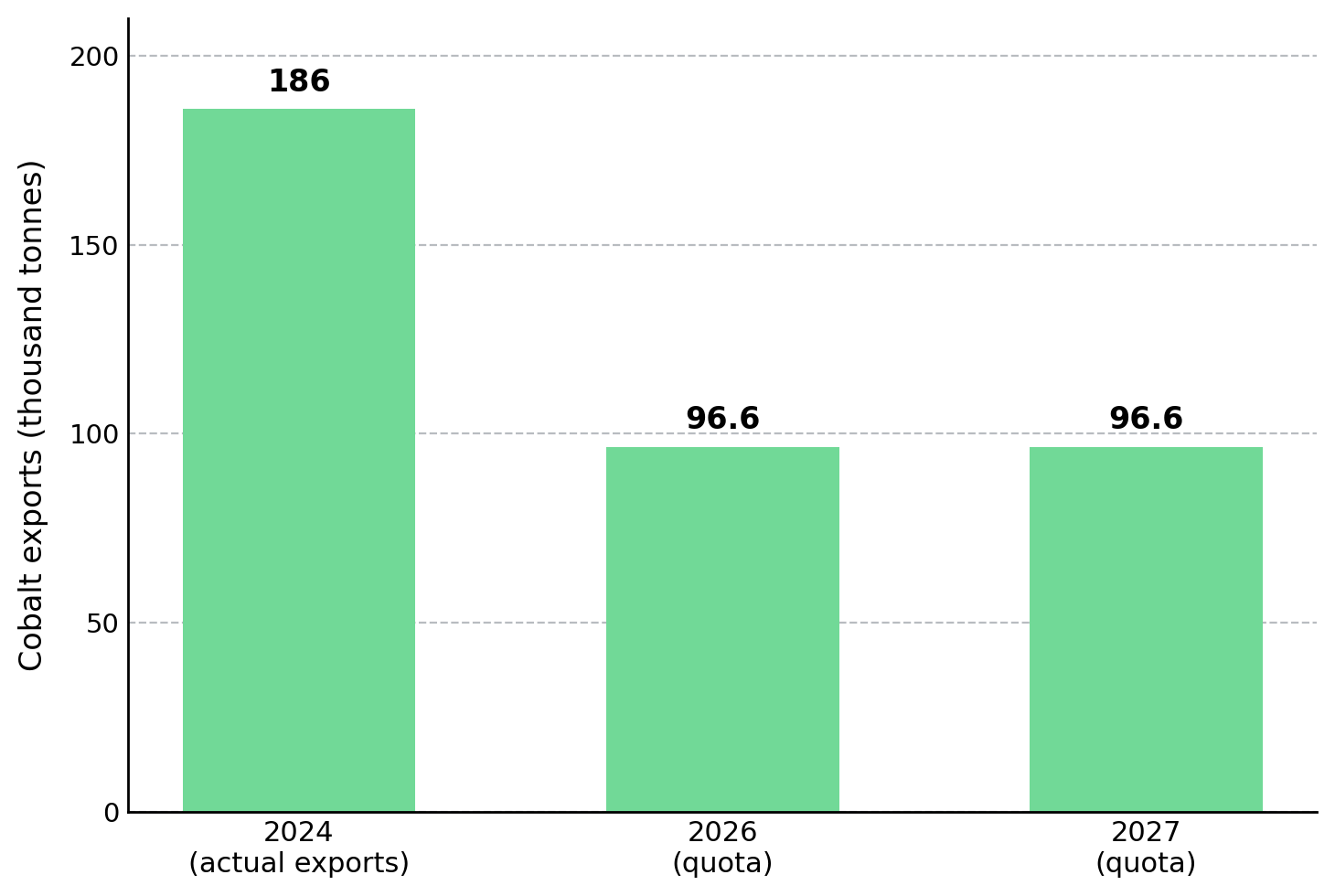

In cobalt, the Democratic Republic of Congo replaced its 2025 export ban with annual quotas capped near 96,600 tonnes for 2026 and 2027, roughly half of 2024 export levels, according to S&P Global. In nickel, Indonesia's annual RKAB mining quotas can tighten or expand global supply with a single policy revision, making government decisions as important as production growth.

Government control over supply changes how battery and critical-metals projects should be valued. When a single state controls more than half of mined or refined supply, its policy choices, not marginal demand, set the clearing price. As a result, low-cost projects and processing assets outside those jurisdictions can command higher valuations because they offer buyers a more secure supply chain.

China's Rare Earth Magnet Dominance & the Vertical Integration Response

Supply concentration is highest in the permanent magnets used in electric motors, wind turbines, robotics and guided-weapons systems, making this one of the most strategically important parts of the critical-minerals supply chain. The International Energy Agency projects demand for neodymium-iron-boron magnets in North America and Europe to grow by more than 50% over the next decade, while almost all qualified production remains concentrated in China. Western producers are responding by integrating the supply chain from mine to finished magnet, reducing reliance on Chinese processors and capturing more value across production.

Energy Fuels is pursuing vertical integration through the White Mesa Mill in Utah, the only commercial-scale US facility that separates rare-earth oxides from monazite. Its agreed US$1.9 billion acquisition of magnet manufacturer Vacuumschmelze would extend the company from oxide production into finished magnets through a customer-qualified manufacturing plant in South Carolina, giving Energy Fuels exposure to more of the value chain. Owning more of the supply chain makes it easier to compete with established Chinese producers than supplying only one stage of production.

Mark Chalmers, Chief Executive Officer of Energy Fuels, explains why vertical integration is essential for Western producers competing with China's rare-earth supply chain:

"The big problem the US government has to solve is competing against the ex-China supply when it comes to rare earths. To really compete with China, you have to have all those steps; you can't be missing a step in the middle of it."

Nickel & Cobalt Quotas Favor Non-Indonesian Supply

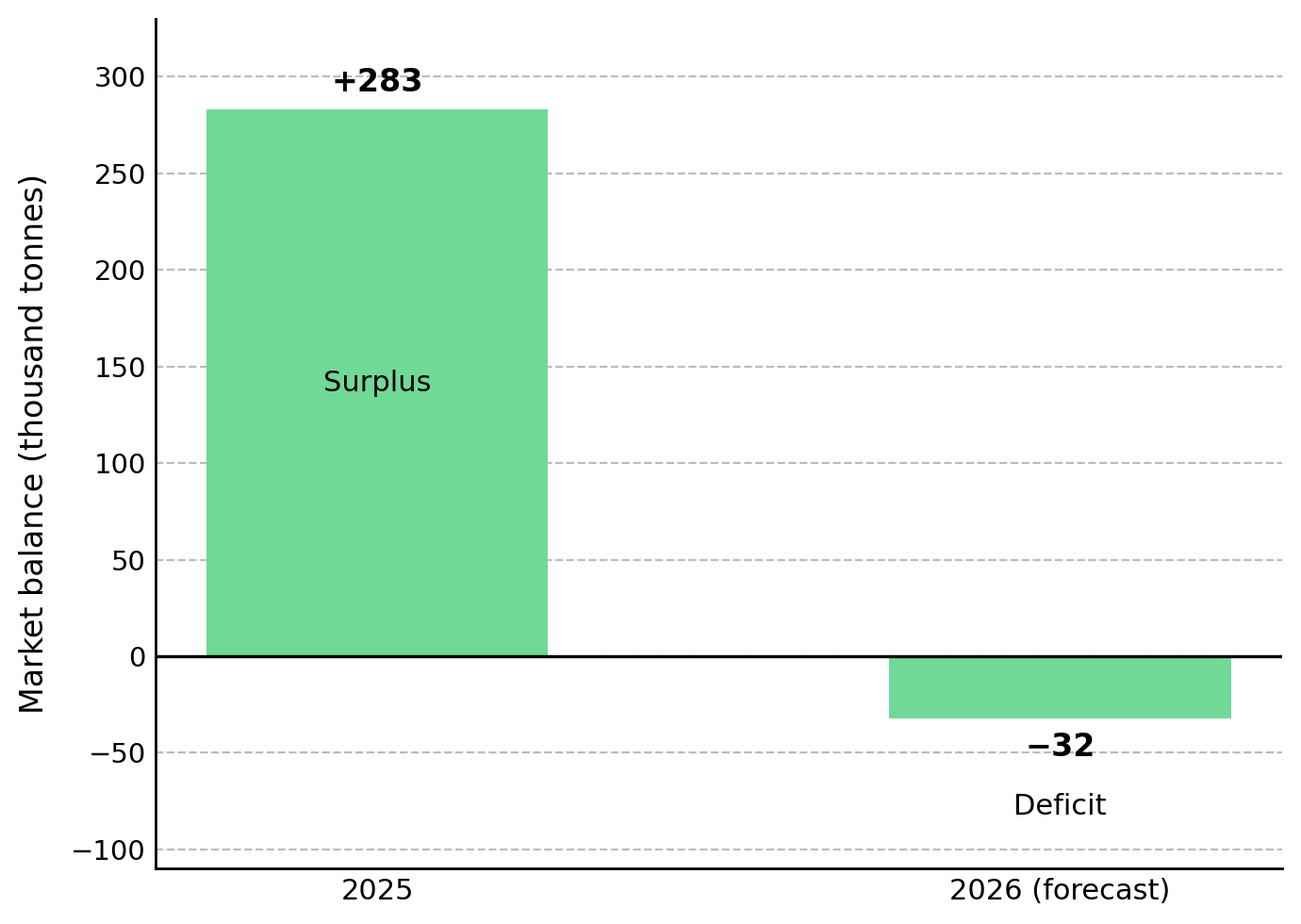

Government production quotas can quickly shift battery metal markets. Forecasts cited by Crux Investor project nickel moving into a modest 32,000-tonne deficit in 2026 after a large 2025 surplus, while cobalt has remained near US$56,000 a tonne following export quotas in the Democratic Republic of Congo. Although forecasts are not guaranteed, they show how policy can rapidly reverse market balances. For nickel producers, sulphide deposits typically offer lower processing costs and emissions than Indonesia's laterite ores, which require energy-intensive smelting or high-pressure acid leaching.

Indonesia, which supplied roughly 60% of mined nickel in 2024, is reinforcing this shift through policy. In December 2025, Energy and Mineral Resources Minister Bahlil Lahadalia confirmed plans to cut 2026 nickel output to support prices and government revenue, and the Ministry (ESDM) subsequently set the 2026 RKAB mining quota at 260-270 million wet tonnes of ore, roughly a third below the 379 million tonnes approved for 2025. Jakarta also reverted from three-year to one-year quota validity, giving it tighter, more frequent control over production.

Lifezone Metals combines a development-ready nickel sulphide project in Tanzania with a US platinum-group metals recycling platform to supply traceable nickel outside Indonesia. Canada Nickel is advancing the Crawford nickel-cobalt sulphide project in Ontario, one of relatively few large sulphide projects that could enter production before 2030. Both investment cases depend on demand for secure, traceable supply outside the dominant producing countries

Ex-China Scarcity Premium Depends on Cost & Jurisdiction

Supply controls can create a premium for material sourced outside dominant producing jurisdictions. Ex-China rare-earth oxide prices have traded at multiples of Chinese domestic prices, while demand for traceable nickel and cobalt suggests buyers increasingly value secure, non-Indonesian supply. Only a subset of projects can capture that premium. It favors assets that combine low production costs with jurisdictions that Western investors are willing to finance and buyers are willing to source from.

In a policy-driven market, an asset's operating cost and the stability of its host jurisdiction matter more than resource size. A high-grade deposit in a contested jurisdiction can be worth less than a modest deposit in a stable one because changes in government policy can quickly remove location-based valuation premiums. Cost-curve position is what protects margin when prices fall.

Cost-Curve Leadership Protects Margins

Sovereign Metals’ deposit sits in a soft, weathered layer that can be mined without drilling, blasting or a hard-rock crushing and grinding circuit, helping deliver low operating costs and a pre-tax net present value of about US$2.2 billion at an 8% discount rate in the company's definitive feasibility study. Kasiya is primarily a rutile and graphite project, with a heavy rare-earth monazite stream recoverable from existing tailings at minimal additional capital cost.

The by-product opportunity is credible but remains unproven and should not be treated as part of the base investment case. An independent forecaster has modelled a monazite concentrate price well above the current benchmark, reflecting an unusually heavy rare-earth basket, but that uplift is not yet included in the base case and requires further metallurgical work. The investment case ultimately depends on Kasiya's low operating cost, which helps protect margins even if additional Chinese supply pressures prices.

Ben Stoikovich, Chairman of Sovereign Metals, explains how cost-curve leadership helps producers remain profitable even when Chinese supply pressures prices:

"What's important for Sovereign is that Kasiya is right at the bottom end of the real cost curve, and we'll always be able to sell graphite into the market at healthy margins. We are a mining company, not a chemistry company."

Financing Now Determines Which Projects Get Built

When policy has a greater influence on prices and long-term demand is already established, the key question is no longer whether an orebody exists. It is whether a developer can secure financing and reach a final investment decision without issuing enough new equity to significantly reduce existing shareholders' ownership. Developers that can secure financing on attractive terms are more likely to reach production and capture the benefits of tighter supply.

As producing countries tighten control over critical minerals, Western governments are increasingly financing alternative supply chains. Western governments are using loans, grants, refundable tax credits, export-credit support and defence-stockpile offtake to turn national-security policy into project financing. This support lowers borrowing costs and reduces the amount of new equity developers must issue, helping protect existing shareholders' ownership and per-share value.

Government Financing Reduces Equity Dilution

Canada Nickel has mandated an arranger for a debt facility of up to US$600 million backed by refundable investment tax credits under Canada's critical-minerals framework, a structure designed to fund more than half of Crawford's equity requirement without issuing new shares. The financing depends on a federal construction permit targeted for the second half of 2026. If approved, Crawford would become the first project permitted under Canada's 2019 Impact Assessment Act, marking an important regulatory milestone.

Mark Selby, Chief Executive Officer of Canada Nickel, explains how investment tax credits can replace a significant share of equity financing for new mine development:

"This bridge financing is central to Crawford's overall capital structure. It allows us to deploy Canada's generous investment tax credits available for critical mineral projects in Canada to fund more than half of the equity capital we need to build Crawford."

What Could Undermine the Battery Metals Investment Case

The investment thesis depends on policy support and resilient demand, making both important downside risks. The Busan suspension of China's strictest export controls expires around November 2026, and a decision by Beijing to lift restrictions or release inventories could quickly reduce the ex-China premium. Advances in sodium-ion batteries and cobalt-light cathodes could reduce demand for some battery metals, while Chinese new-energy-vehicle sales fell 7.5% year over year in May, showing that demand growth can slow.

A higher-for-longer Fed and a stronger dollar can cap dollar-priced metals even if supply fundamentals improve. Pre-construction valuations rely on modelled economics rather than operating cash flow, and inferred resources carry much greater geological uncertainty than indicated or measured resources. Permits can slip, financings can fail to close, and development-stage and exploration-stage equities are higher-risk, less liquid and prone to dilution. Investors should distinguish between projects supported by modelled economics and those backed by financing and permits.

Industrial Policy Reshapes the Critical Metals Market

Battery and critical metals have become central to industrial, energy and defence policy as governments compete to secure supply chains. Supply is concentrated, producing countries increasingly manage it for revenue and strategic leverage, and importing economies are subsidising alternative supply rather than waiting for market forces to rebalance production. Battery and critical metals are now shaped as much by industrial policy and national security as by clean-energy demand. For investors, project economics now depends as much on government policy and financing as on resource quality.

Short-term price moves and long-term supply-chain changes should be evaluated separately. Battery and critical-metals prices are likely to remain volatile in the near term as the dollar, Chinese policy decisions and quota changes in Indonesia and the Democratic Republic of Congo continue to influence supply expectations. The longer-term trend remains a slow and costly rebuild of supply chains outside China, regardless of short-term price swings. Investors should distinguish between short-term price volatility and the longer-term shift toward diversified supply chains when evaluating battery and critical-metals investments.

The Investment Thesis for Battery & Critical Metals

- Resource nationalism and supply concentration favor low-cost producers and developers outside the dominant producing countries, where secure and traceable supply can command a valuation premium.

- The lowest-cost developers and producers are best positioned to protect margins when dominant refiners increase supply and pressure prices.

- Government-backed financing allows explorers and developers to reach construction with less dilution by replacing part of their equity needs with loans, tax-credit facilities and offtake support.

- Vertical integration into processing and finished components allows producers to capture more value and reduce reliance on third-party processors, improving margins across the supply chain.

- Development and permitting timelines aligned with multi-year demand growth in power grids, electric vehicles and defence support long-term investment by bringing new supply into expanding markets.

- Balance-sheet strength and financing progress separate developers that reach a final investment decision from those that stall, making financing more important than resource size when assessing development-stage companies.

- Tight supply alongside a hawkish Fed and a stronger dollar supports building positions gradually and maintaining diversified exposure rather than concentrating capital in a single company.

Battery and critical metals no longer trade primarily on electric-vehicle demand. Government policy now has as much influence on valuations as geology, with quotas in Kinshasa, export rules in Beijing and tax credits in Ottawa often shaping project economics more than a drill result. The next cycle will favor developers that can finance and permit projects within Western-aligned supply chains before government priorities change. For investors, the strongest opportunities combine low operating costs, secure financing and permitting progress, because modelled economics create value only when projects reach construction and production.

TL;DR

Battery and critical metals no longer trade primarily on electric-vehicle demand. Export controls, production quotas and government financing increasingly determine prices, project economics and capital allocation. China's dominance in refining and processing has increased the value of secure, low-cost supply outside concentrated jurisdictions, while Western governments are supporting alternative supply chains through loans, tax credits and other financing tools. For investors, cost position, jurisdiction, financing progress and execution now matter more than resource size. Near-term price volatility from a stronger dollar and tighter Fed policy may create entry opportunities, but long-term value depends on projects that can secure funding, permits and competitive operating costs.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed