Serabi Gold Reports Strong Financial Performance in 2024 with 321% Profit Growth

Serabi Gold reports strong 2024 results with 321% profit growth, announces shareholder return policy, and targets production growth to 100,000 oz.

- Serabi Gold reported a 321% increase in post-tax profit to $27.8 million for the year ended December 31, 2024, compared to $6.6 million in 2023, driven by higher gold production and favorable gold prices.

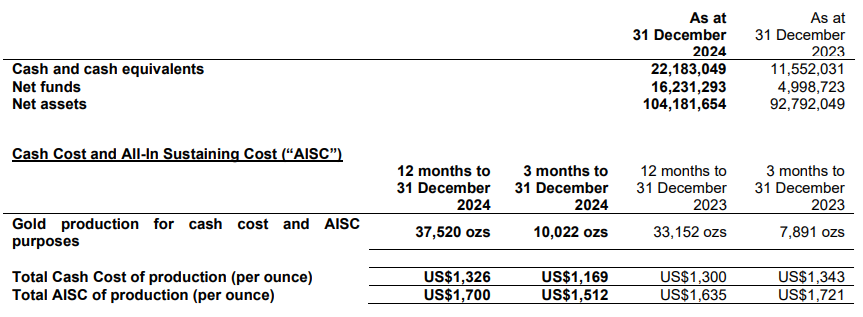

- The company achieved gold production of 37,520 ounces in 2024, a 13% increase from 33,153 ounces in 2023, with robust production continuing into Q1 2025 with 10,013 ounces.

- Revenue increased by 48% to $94.5 million (2023: $63.7 million), benefiting from both increased production and a higher average gold price of $2,407 per ounce.

- Cash holdings nearly doubled to $22.2 million by year-end 2024 (2023: $11.6 million), further increasing to $26.5 million by March 31, 2025.

- The Board announced a new shareholder return policy targeting returns of 20-30% of free cash flow, with production guidance of 44,000-47,000 ounces for 2025 and plans to reach 60,000 ounces by 2026 and over 100,000 ounces thereafter.

Serabi Gold plc (LSE:SRB), a Brazilian-focused gold mining and development company, has released its audited results for the year ended December 31, 2024, showcasing substantial growth across all key financial metrics. The company operates in Brazil with a primary focus on gold mining and development, particularly at its Palito Complex and Coringa mine. For investors considering Serabi Gold, the 2024 results demonstrate strong operational execution and financial discipline, with significant production growth potential and the introduction of a shareholder return policy suggesting management confidence in sustainable cash generation.

Financial Performance Highlights

Serabi Gold achieved remarkable financial results in 2024, with revenue reaching $94.5 million, representing a 48% increase from $63.7 million in 2023. This growth was driven by a combination of increased production volume and a favorable gold price environment, with the average realized gold price rising to $2,407 per ounce, up 24% from $1,945 in 2023.

Colm Howlin, CFO of Serabi, commented on the financial performance:

"While gold production improved by 13% YOY, sales revenue was up by almost 48% as a result of the strengthening of the gold price during 2024 with the average gold price achieved during 2024 being up 24% in comparison to the previous year. At the same time, total operating expenses only increased by 10% resulting in Post-Tax Profit being up by $21.2 million, a 321% increase, and EBITDA of $35.9 million being up by $22.1 million, a 160% improvement YOY."

The company's balance sheet strengthened considerably, with cash holdings almost doubling from $11.6 million at the end of 2023 to $22.2 million by December 31, 2024. This positive cash trend continued into 2025, with cash balances further increasing to $26.5 million by March 31, 2025. Net cash (after interest-bearing loans and lease liabilities) stood at $16.2 million at year-end 2024, a significant improvement from $5.0 million at the end of 2023.

Operational Performance

Serabi's operational results were equally impressive, with gold production reaching 37,520 ounces for the full year 2024, a 13% increase from 33,153 ounces in 2023. The positive momentum continued into 2025, with first quarter production of 10,013 ounces, positioning the company well to achieve its 2025 production guidance of 44,000-47,000 ounces.

Despite the increased production, cost control remained effective. Cash costs for the full year were $1,326 per ounce (2023: $1,300), while All-In Sustaining Costs (AISC) were $1,700 per ounce (2023: $1,635). The modest increase in costs, particularly when compared to the significant rise in gold prices, contributed to the substantial improvement in profit margins.

Net cash inflow from operations more than tripled to $24.5 million after mine development expenditure of $6.3 million, compared to $7.7 million in 2023 after accounting for mine development of $4.4 million. This strong operational cash flow reflects the company's ability to efficiently translate increased production and higher gold prices into improved financial results.

Growth Strategy and Outlook

Serabi's growth strategy focuses on both organic expansion and potential inorganic opportunities. The company is targeting production of 60,000 ounces by 2026 and aims to become a +100,000 ounces producer thereafter through its 2025 and 2026 brownfield exploration programs at the Palito Complex and Coringa.

Significant progress was made at the Coringa mine in 2024, including the renewal of the three-year trial mining permit, the successful build and commissioning of the Coringa classification plant, and the issuing of a new Technical Report for the Coringa mine with 180,000 ounces of Measured and Indicated Resources. Development work at Coringa continued with increased activity at the Serra vein, as well as the commencement of portal and ramp development at the Meio vein.

Michael Lynch-Bell, Chair of Serabi, provided insight into the company's strategic direction:

"Whilst 2024 was a remarkable year for Serabi, I am pleased to report that the momentum in our growth has continued into 2025, as the company remains on track to execute its growth strategy, ramping up annual production to a potential run rate of 60,000 oz per annum by 2026 year-end and ultimately growing into a +100,000 oz per annum producer thereafter through our 2025 and 2026 brownfield exploration programmes at the Palito Complex and Coringa."

The company's 2025 exploration program has already commenced, involving two diamond drill rigs at both the Palito Complex and the Coringa mine, which management believes will contribute to the company's growth objectives.

Market and Macroeconomic Environment

The favorable gold price environment played a significant role in Serabi's financial performance. The company benefited from record gold prices in 2024, a trend that has continued into 2025. According to the Chair's statement, multiple factors contributed to the higher-than-expected realized gold price, including interest rate cuts by the US Federal Reserve, geopolitical uncertainty in Eastern Europe and the Middle East, the US Presidential Election, increased global central bank demand for gold, and market volatility.

Looking ahead, while the company does not provide specific gold price forecasts, management noted that operations remain robust at current gold price levels. With no significant capital investment required for 2025, the cash flow generation of operations is expected to remain strong, provided gold prices maintain their elevated levels.

Conclusion and Investment Perspective

Serabi Gold's 2024 results demonstrate strong operational execution and financial discipline, with significant improvements across all key metrics. The company's ability to increase production while maintaining cost control, combined with favorable gold prices, has translated into substantial improvements in profitability and cash flow.

For investors, Serabi presents a compelling growth story with clear production targets: 44,000-47,000 ounces in 2025, 60,000 ounces by 2026, and ambitions to exceed 100,000 ounces thereafter. The introduction of a shareholder return policy further enhances the investment case, signaling management's confidence in sustainable cash generation.

The company's strong balance sheet, with increasing cash holdings and minimal debt, provides financial flexibility to pursue growth opportunities while managing operational risks. The ongoing brownfield exploration programs at the Palito Complex and Coringa offer potential for resource expansion and production growth beyond current targets.

While commodity price volatility always presents a risk for mining companies, Serabi's relatively low-cost production profile provides some protection against potential gold price fluctuations. Additionally, the company's focus on Brazil exposes it to country-specific risks, including regulatory changes and currency fluctuations.

Overall, Serabi Gold's 2024 performance demonstrates the company's potential to deliver shareholder value through production growth, cost control, and potentially direct returns through its newly announced shareholder return policy. The company appears well-positioned to achieve its near-term objectives and progress toward its longer-term goal of becoming a mid-tier gold producer.

Analyst's Notes

Subscribe to Our Channel

Stay Informed