Silver's Structural Bull Market: Investment Opportunities in a Supply-Constrained Market

Silver prices hit 14-year highs at $39.40/oz, up 36% YTD. Structural deficits, industrial demand, and strategic metal exposure create compelling investment opportunities.

- Silver prices have surged to 14-year highs at $39.40 per ounce, delivering a remarkable 36% year-to-date gain that has outperformed gold's 31% advance, driven by structural supply deficits and accelerating industrial demand.

- US tariff policies and trade tensions are creating supply chain disruptions that extend beyond copper into silver markets, widening premiums between US and London futures while tightening spot market conditions through increased leasing activity.

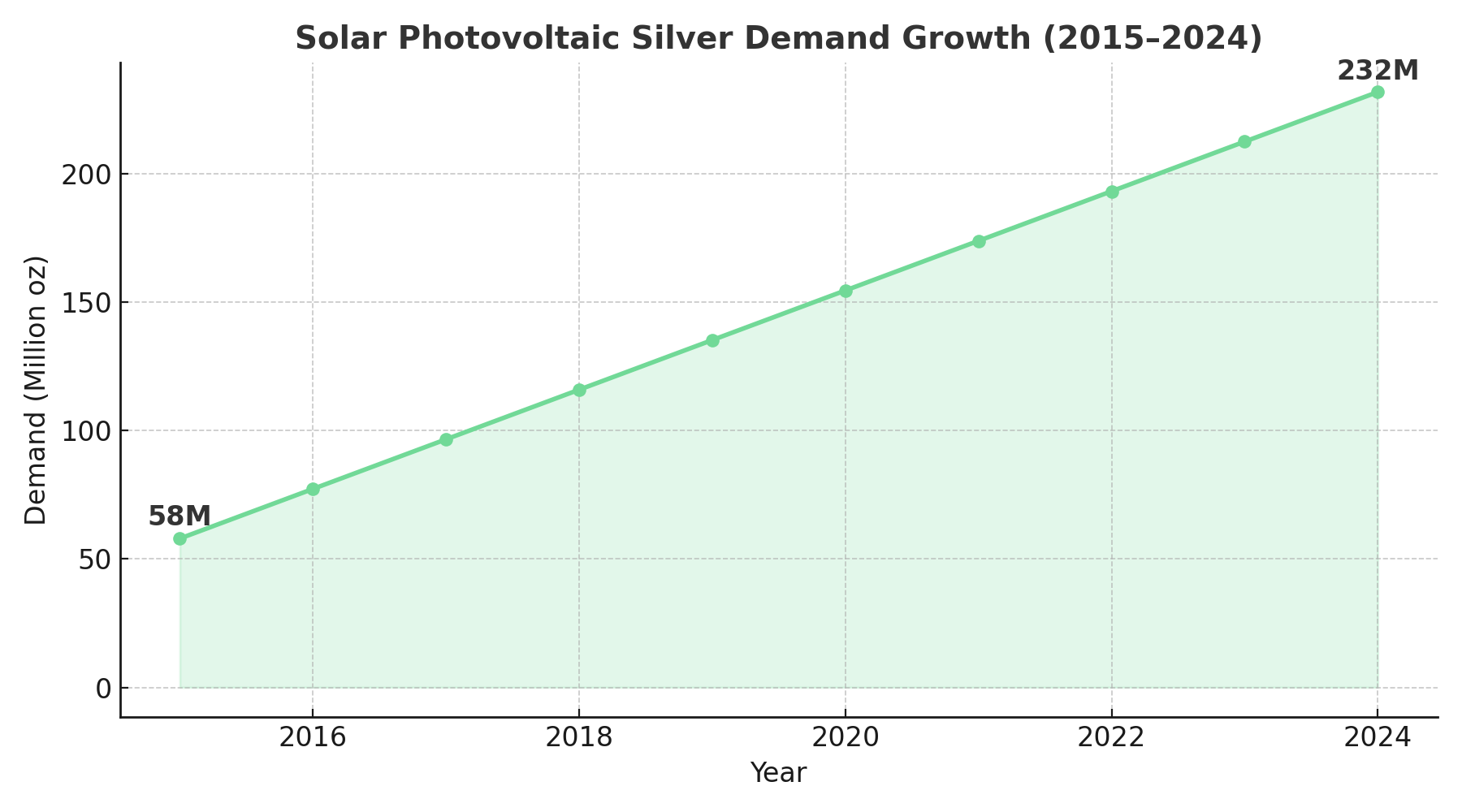

- Industrial silver consumption is permanently removing metal from available supplies, with solar photovoltaic demand alone projected to reach 232 million ounces in 2024, representing a fourfold increase from 2015 levels as renewable energy adoption accelerates globally.

- Strategic metals including gallium and indium found alongside silver deposits are creating additional value drivers, particularly as 98% of global gallium supply originates from China, making North American silver projects with these co-products increasingly valuable for supply chain security.

- Analyst forecasts suggest silver could reach $42-45 per ounce in the near term, with mining company valuations offering significant leverage to price appreciation as equity values typically move 2-3 times the percentage change in underlying silver prices.

The Silver Surge: Breaking Down 14-Year Highs

Silver's recent performance has captured the attention of commodity markets worldwide. Spot silver reached $39.40 per ounce, matching levels not seen since September 2011, representing a remarkable 36% year-to-date gain that has even outpaced gold's impressive 31% advance. This surge reflects more than just speculative momentum; it signals a fundamental shift in silver market dynamics that savvy investors are positioning to capitalize on.

The current rally builds on a foundation of structural changes that have been developing over several years. Unlike previous silver bull markets driven primarily by investment speculation, today's market is supported by genuine supply-demand imbalances that appear sustainable. The gold-silver ratio has compressed from approximately 105:1 in April to around 87:1 currently, suggesting silver is beginning to close its historical valuation gap relative to gold.

Market positioning data reveals that while long positions have extended, the underlying fundamentals supporting higher prices remain intact. This creates an environment where short-term volatility should be viewed as opportunity rather than cause for concern, particularly for investors with longer investment horizons.

Industrial Demand: The Foundation of Structural Deficits

Silver's industrial applications continue to expand, creating a demand floor that distinguishes it from purely investment-driven precious metals. Solar photovoltaic demand alone is projected to reach 232 million ounces in 2024, representing a fourfold increase from 2015 levels. This growth trajectory shows no signs of slowing as global renewable energy adoption accelerates.

Beyond solar applications, silver's unique properties make it irreplaceable in numerous industrial processes. Electronics manufacturing, medical devices, automotive components, and emerging technologies all require silver's superior conductivity and antimicrobial properties. This industrial demand base provides price stability and creates predictable consumption patterns that support long-term investment theses.

The structural nature of silver's supply deficit becomes apparent when examining the mathematics of industrial consumption. Unlike gold, where above-ground inventories can theoretically satisfy demand for decades, silver's industrial consumption permanently removes metal from the available supply. This consumption dynamic, combined with limited new mine production, creates the foundation for sustained higher prices.

Companies operating in high-grade silver districts are particularly well-positioned to benefit from these dynamics. Vizsla Silver, currently in the development stage with first silver production targeted for H2 2027, exemplifies this opportunity through its Panuco project in Mexico. Simon Cmrlec, Chief Operating Officer notes:

"We're targeting production for 2027 and pretty confident we're going to get there."

The company boasts resources of 222.4 million ounces of silver equivalent in measured and indicated categories at grades of 534 grams per tonne. With robust preliminary economic assessment economics showing an 86% internal rate of return and nine-month payback period, and a feasibility study expected in H2 2025, such projects demonstrate the economic attractiveness of high-grade silver development in the current price environment.

Strategic Metals: The Hidden Value Proposition

One of the most compelling aspects of modern silver investments lies in the strategic metals often found alongside silver deposits. Gallium, indium, and other critical materials essential for semiconductor manufacturing, 5G infrastructure, and military applications are frequently present in silver-bearing deposits. With 98% of global gallium supply originating from China, supply chain vulnerabilities create additional value drivers for silver projects containing these materials.

The strategic metal component adds a geopolitical dimension to silver investments that extends beyond traditional precious metal considerations. As nations seek to secure critical material supply chains, domestic sources of these metals become increasingly valuable. This dynamic is particularly relevant for North American silver producers, who benefit from both geographic proximity to major consuming markets and political stability.

Americas Gold & Silver exemplifies this strategic positioning through its operational Galena Complex in Idaho's historic Silver Valley. Currently in a strategic turnaround phase following 100% ownership acquisition in October 2024, the company operates existing infrastructure including 2 mills, 4 shafts, and 55 miles of underground development. Recent operational improvements are already showing results, with Paul Huet, Chairman and CEO, noting:

"We're skipping at about 42 tons per hour at the moment. We need to get that to over 100 tons per hour and we're going to do that this year."

The operation not only produces silver but also targets antimony recovery, with historical production of 18 million ounces of antimony and current testwork showing 90-96% recovery rates. Given that zero primary antimony mines currently operate in the United States, this represents a potentially strategic national asset in addition to silver production capability.

Tariff Impacts & Supply Chain Disruptions

Recent US trade policy developments have created additional tailwinds for silver prices through multiple channels. Trump's planned 50% copper import tariffs, effective August 1, have already begun influencing silver market dynamics by widening the US-London premium on silver futures. This premium differential has encouraged increased leasing activity in the spot silver market, contributing to tighter supply conditions and higher lease rates.

The interconnected nature of metals markets means that disruptions in one area quickly spread to others. Copper tariffs not only affect copper itself but create ripple effects through silver and other metals markets as investors seek alternatives and supply chains adapt. These policy-driven market distortions often create opportunities for domestic producers and investors positioned in the right assets.

Beyond immediate price impacts, tariff policies signal a broader shift toward supply chain localization that could benefit North American silver producers for years to come. Companies with domestic production capacity may command premium valuations as industrial consumers seek supply security over cost optimization.

Investment Strategies & Market Positioning

The current silver market presents multiple investment approaches, each suited to different risk profiles and investment objectives. Direct exposure through physical silver or exchange-traded funds provides straightforward commodity exposure, while silver mining equities offer leveraged exposure to price movements along with operational upside potential.

Mining company valuations currently present attractive entry points relative to silver prices and long-term fundamentals. Many established producers trade at significant discounts to net asset value, creating opportunities for investors willing to accept operational risks in exchange for potential multiple expansion as silver prices rise.

Development-stage projects offer the highest leverage to silver price appreciation but require careful evaluation of management teams, project economics, and execution risk. Vizsla Silver Corp, with its development timeline targeting first production in H2 2027 and robust economics combined with significant exploration upside across only 30% of known veins drilled, represents the type of quality development opportunity available in the current market.

Cerro de Pasco presents another compelling silver opportunity through its integrated approach to precious metals extraction and environmental remediation in Peru's historic mining district. The company's strategy of reprocessing tailings while simultaneously producing silver and other metals demonstrates the potential for sustainable, profitable operations in established mining regions. Guy Goulet, Chief Executive Officer, highlights the significant valuation opportunity the company represents:

"We are only $150 million Canadian market cap. From our model, we're at $630 million profit a year. So this market cap should be adjusted at some point."

Meanwhile, Americas Gold & Silver Corp offers exposure to an operational turnaround story, with recent infrastructure upgrades increasing shaft capacity and expanded mobile fleet enhancing production capability at the Galena Complex.

The key to successful silver investing lies in understanding the different risk-return profiles available and matching investment selection to individual circumstances and market outlook. Given silver's current momentum and fundamental support, a diversified approach incorporating both established producers and quality development projects may optimize risk-adjusted returns.

Market Structure

Silver's market structure differs significantly from other precious metals in ways that create both opportunities and risks for investors. The relatively small size of the silver market compared to gold means that capital flows can create outsized price movements in both directions. This characteristic contributed to silver's dramatic outperformance year-to-date but also suggests potential for continued volatility.

Lease rates in the silver market have increased substantially, indicating tightness in the physical market that often precedes sustained price advances. When combined with the widening basis between US and London silver futures, these technical indicators suggest underlying supply stress that supports higher price levels.

The concentration of silver production among a relatively small number of mines worldwide creates additional supply vulnerability. Unlike gold, where production is more geographically diversified, silver often comes as a byproduct from base metal mines, making supply responsive to factors beyond silver price alone. This supply structure can amplify price movements during periods of strong demand growth.

Sustainable Mining

Environmental, social, and governance factors increasingly influence investment decisions across all sectors, and silver mining is no exception. Modern silver operations emphasize sustainable mining practices, community engagement, and environmental stewardship as core business requirements rather than regulatory afterthoughts.

Tailings reprocessing represents one of the most environmentally positive approaches to silver production, offering the dual benefits of metal recovery and environmental remediation. These operations typically require significantly lower capital expenditures and operating costs compared to traditional mining while providing valuable environmental cleanup services.

Companies demonstrating strong ESG credentials often command valuation premiums and attract capital from institutional investors with sustainability mandates. Americas Gold & Silver operational focus on local hiring, competitive wages, and community infrastructure investment demonstrates how mining companies can create shared value while pursuing commercial objectives. The company's recent $100M term debt funding and Teck investment in June 2025 reflects institutional confidence in both the asset quality and management execution capability.

Regional Advantages

Geographic location plays an increasingly important role in mining investment evaluation as supply chain security becomes a strategic priority. North American silver producers benefit from political stability, established regulatory frameworks, and proximity to major consuming markets. These advantages become more valuable as global trade tensions increase and supply chain resilience gains importance.

Mexico's position as a major silver-producing jurisdiction offers particular advantages through established mining expertise, favorable geology, and trade relationships with the United States. Projects like Vizsla Silver’s Panuco district benefit from excellent infrastructure access including federal highways, deepwater ports, and reliable power supply, reducing both development risk and operating costs.

The concentration of high-grade silver deposits in politically stable jurisdictions creates natural advantages for investors seeking exposure to silver price appreciation without excessive geopolitical risk. This geographic premium likely persists as long as global trade tensions remain elevated and supply chain security maintains strategic importance.

Valuation Frameworks

Silver mining investments require sophisticated valuation approaches that account for commodity price volatility, operational leverage, and development risk. Net present value calculations become highly sensitive to silver price assumptions, making scenario analysis essential for investment decision-making.

Current silver prices near $40 per ounce validate project economics that appeared marginal at lower price levels. Projects with all-in sustaining costs below $15 per ounce generate substantial free cash flow at current prices, creating opportunity for dividend payments, debt reduction, or growth investment. Companies achieving costs in the $9-12 per ounce range, like several operations targeting these levels, demonstrate exceptional economic returns.

The relationship between silver prices and mining company valuations typically demonstrates significant leverage, with equity values often moving 2-3 times the percentage change in underlying silver prices. This sentiment is perhaps best captured by Paul Huet, Chairman and CEO of Americas Gold & Silver’s observation:

"If we did nothing, the share price couple triple based on where most of us believe silver is heading."

This leverage relationship creates an opportunity for substantial returns during bull markets but requires careful position sizing and risk management.

Future Catalysts

Several catalysts could drive silver prices significantly higher over the next 12-24 months. Continued industrial demand growth, particularly from renewable energy and electronics applications, provides fundamental support for higher prices. Investment demand appears to be accelerating as investors recognize silver's attractive risk-return profile relative to other precious metals.

Supply constraints will likely intensify as existing mines mature and new development projects face increasingly complex permitting and development challenges. The long lead times required for new mine development mean that current supply tightness could persist for several years even if silver prices remain elevated.

Analyst forecasts suggest silver could reach $42-45 per ounce in the near term, with some projecting sustained higher prices through 2026. MKS PAMP's Nicky Shiels expects approximately $42 per ounce this year, while WisdomTree's Nitesh Shah sees potential for $45 per ounce by 2026 following a possible interim dip to $35 per ounce.

Central bank policies and currency debasement concerns could provide additional support for precious metals generally, with silver potentially benefiting disproportionately due to its industrial demand component and relative affordability compared to gold.

Portfolio Considerations

Silver investments carry distinct risks that require careful evaluation and management. Price volatility exceeds that of most other commodities, creating potential for significant short-term losses even in favorable long-term market conditions. Operational risks at mining companies can quickly impact investment returns, particularly for development-stage projects.

Regulatory changes, environmental compliance costs, and social license issues represent ongoing risks for mining operations worldwide. These factors can affect both individual company performance and broader sector sentiment, influencing investment returns beyond fundamental silver market dynamics.

Currency fluctuations add additional complexity for international operations, as many silver producers operate in countries with currencies that may not move in correlation with silver prices. This currency risk can either amplify or dampen investment returns depending on exchange rate movements.

However, these risks must be balanced against the potential for substantial returns in a favorable silver price environment. Proper diversification, position sizing, and risk management can help investors capture silver's upside potential while managing downside risks effectively.

For Investors: Positioning for the Silver Bull Market

Silver's current bull market appears fundamentally different from previous cycles, driven by genuine supply-demand imbalances rather than purely speculative factors. Industrial demand growth shows no signs of slowing, while supply constraints intensify due to resource depletion and development challenges. Strategic metal co-products add additional value dimensions that enhance investment attractiveness beyond silver price appreciation alone.

The combination of structural deficits, industrial demand growth, strategic metal exposure, and attractive mining company valuations creates a compelling investment opportunity for investors seeking exposure to silver's bull market potential. While risks remain significant, the fundamental case for higher silver prices appears stronger than at any point since the 2011 peak.

Investors considering silver exposure should evaluate their risk tolerance, investment timeline, and portfolio objectives carefully. The current market environment favors companies with high-grade deposits, low-cost operations, and strong management teams positioned in favorable jurisdictions. With silver prices at 14-year highs and fundamental support appearing sustainable, the silver investment opportunity warrants serious consideration from institutional and retail investors alike.

The silver market's structural transformation creates opportunities for substantial wealth creation over the coming years. Investors positioned appropriately for this transition may benefit from one of the most compelling commodity investment themes of the decade.

Analyst's Notes

Subscribe to Our Channel

Stay Informed