Solar Demand Falls 19% & Silver Deficit Widens, Shifting Focus to Mine Supply

Solar demand fell 19%, yet the silver deficit widened to 46.3 million ounces as limited mine supply and rising investment demand reshaped the market.

- Solar photovoltaic silver demand fell 19% in 2026, from 186.6 million ounces to approximately 151 million ounces, marking the largest annual decline on record for silver's largest industrial end market.

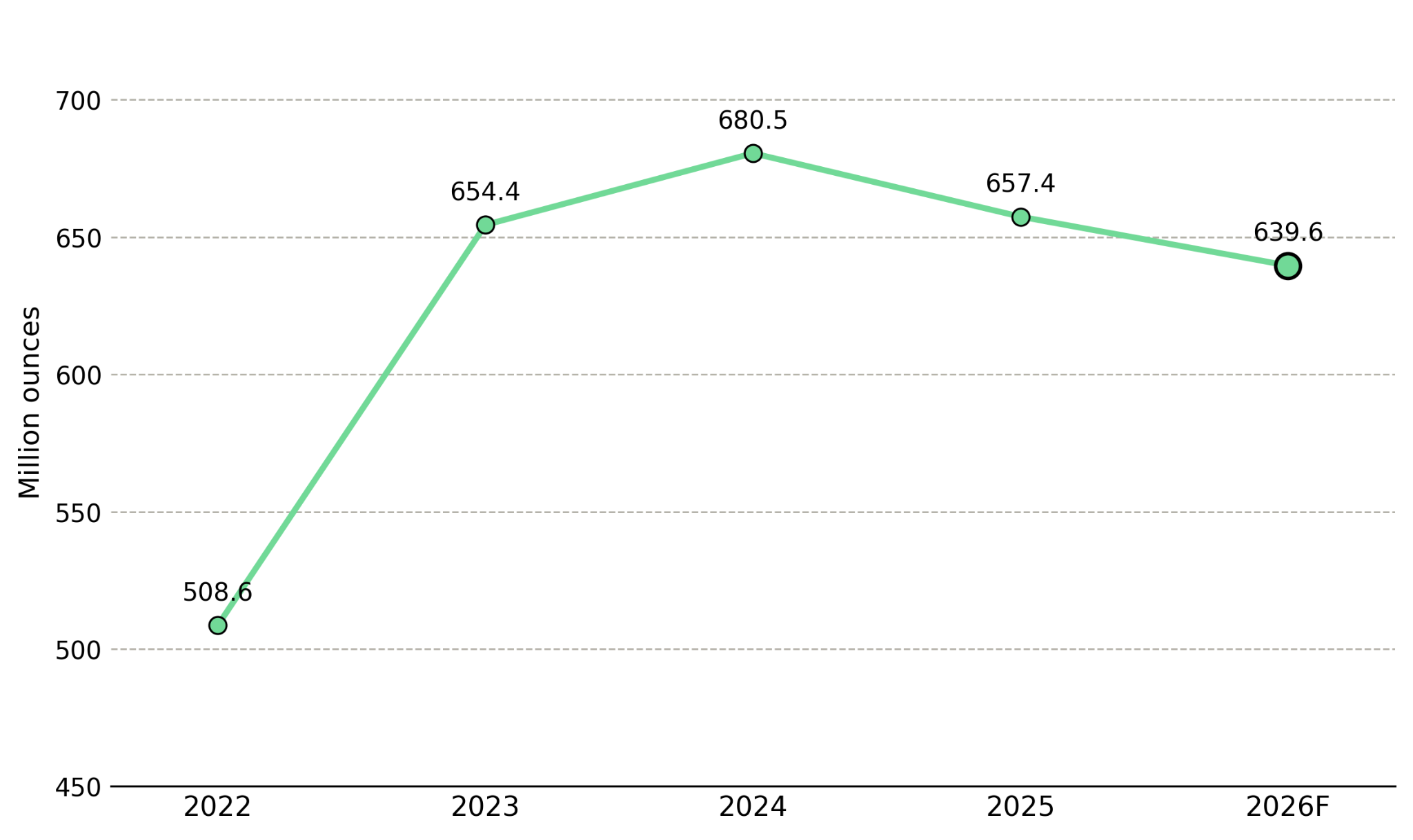

- Total industrial silver offtake fell 3% to 657.4 million ounces in 2025 and is forecast to decline another 3% to 639.6 million ounces in 2026.

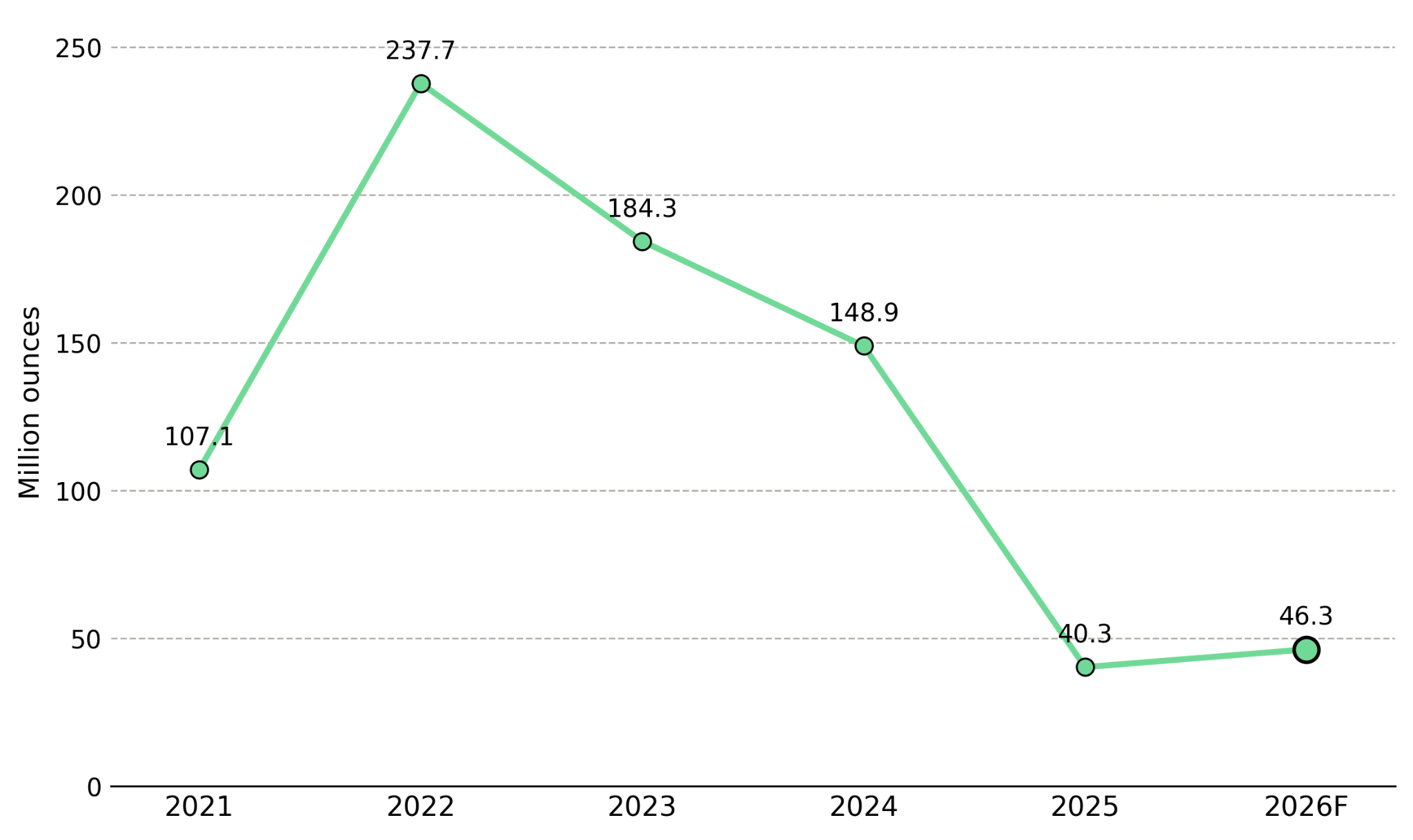

- The global silver deficit widened for a sixth consecutive year, increasing from 40.3 million ounces in 2025 to 46.3 million ounces in 2026 despite weaker industrial demand, according to the Silver Institute's World Silver Survey 2026.

- Physical investment demand is forecast to rise 20% to a three-year high of 227 million ounces in 2026, while US retail demand is forecast to rebound 57% after three consecutive years of decline, shifting the market's incremental demand toward investment buying.

- Global mined silver supply grew 3% to 846.6 million ounces in 2025, insufficient to offset the widening silver deficit despite weaker industrial demand.

Solar Thrifting & Lower Silver Demand

For much of the past decade, rising solar photovoltaic demand has been viewed as the primary driver of silver's recurring market deficit. According to the Silver Institute's World Silver Survey 2026, produced with Metals Focus, photovoltaic silver demand fell 6% to 186.6 million ounces in 2025 and is forecast to decline another 19% to approximately 151 million ounces in 2026, the largest annual reduction on record for the sector.

The decline reflects thrifting rather than substitution, meaning manufacturers are using less silver per solar cell instead of replacing the metal altogether. Thrifting reduces the amount of silver used in each solar cell through thinner paste layers and more efficient cell printing, as higher silver prices continue to compress solar module margins. Substitution would replace silver with another conductive material at commercial scale, but that shift has not occurred in 2026. Thrifting reduces the amount of silver used per solar cell but does not eliminate silver from the manufacturing process, allowing photovoltaic production to remain a significant source of silver demand even as per-unit consumption declines.

Total industrial silver offtake, which includes electronics, automotive, and photovoltaic demand, fell 3% to 657.4 million ounces in 2025 and is forecasted to decline another 3% to 639.6 million ounces in 2026. Taken alone, this decline suggests weaker industrial demand should reduce pressure on the silver market. However, mine supply did not increase enough to eliminate the widening deficit.

Limited Mine Supply & A Widening Silver Deficit

Falling industrial demand would normally be expected to reduce the market deficit if mine supply increased enough to offset the decline. Instead, mine supply increased only modestly while the deficit widened. Global mined silver supply increased 3% to 846.6 million ounces in 2025, but the global silver deficit still widened to 46.3 million ounces in 2026 from 40.3 million ounces in 2025, according to the Silver Institute's World Silver Survey 2026.

The widening deficit despite weaker industrial demand indicates that limited mine supply growth, rather than industrial consumption, is driving the market imbalance. Global average all-in sustaining costs for primary silver producers fell 1% to US$12.21 per ounce in 2025, while higher silver prices improved operating margins without a comparable increase in mine output. Lower production costs and limited output growth indicate that existing mines are generating higher cash flow instead of delivering significant new supply to the market.

The deficit continued to widen despite weaker industrial demand, indicating that new mine supply, whether from primary or byproduct production, cannot be added quickly enough to balance the market. Developing new mine supply requires years of exploration, permitting, financing, and construction, making supply far slower to respond than manufacturers reducing silver use through thrifting.

Industrial Silver Demand Broadens Beyond Solar

Lower solar demand has been partly offset by growth in other industrial applications of silver. Demand from AI data centers, electrical transmission equipment, and automotive electronics continues to grow, although the World Silver Survey 2026 says these sectors do not yet offset the decline in solar demand. Industrial silver demand is becoming more diversified even as total demand declines, supporting production growth at existing mines that can supply multiple end markets.

Americas Gold and Silver’s flagship Galena Complex in Idaho completed a Phase 2 upgrade, increasing hoisting capacity by 150%, from 42 to 105 short tons per hour, for approximately US$1.1 million. The upgrade targets total hoisting capacity of approximately 1,350 metric tons per day and average ore production of about 650 metric tons per day by the end of 2026, nearly 50% above current levels.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold and Silver, frames how solar and AI demand converge industrially in the current market:

"The themes, of course, are solar panel investing. We've seen massive growth globally in solar panel construction… layering on top of that from the industrial side is the AI rollout, where there's a lot of these data centers going all over the place. The old adage is copper is the highway, but silver is the glue."

Investment Demand Strengthens the Silver Market

As industrial demand weakened, physical investment demand became a larger source of silver buying. Physical investment demand, including coins, bars, and exchange-traded product accumulation, is forecast to rise 20% to a three-year high of 227 million ounces in 2026, while US retail demand is expected to rebound 57% after three consecutive years of decline. Global exchange-traded product holdings total an estimated 1.31 billion ounces, highlighting the scale of investment capital already committed to the silver market.

Vizsla Silver is advancing its flagship Panuco silver-gold project in Sinaloa. A November 2025 Feasibility Study outlines average annual production of 17.4 million silver-equivalent ounces over an initial 9.4-year mine life, with an after-tax net present value of US$1.8 billion at a 5% discount rate, an internal rate of return of 111%, and a seven-month payback using base-case prices of US$35.50 per ounce silver and US$3,100 per ounce gold. The company has awarded key process equipment contracts and begun engineering work to advance the project toward construction. The mine plan also provides for a future Phase 2 expansion to 4,000 metric tons per day and the integration of the Napoleon deposit.

Michael Konnert, President and Chief Executive Officer of Vizsla Silver, highlights investment demand as a key silver price driver:

"We're supposed to see about a 7% increase in investment demand for silver. The market's much smaller than gold, so any increase in consumer or retail investment demand, hedge funds, family offices and other investors could have a very material impact on the price of silver."

Exploration Success & Future Silver Supply

GR Silver Mining is advancing the San Marcial deposit within its Plomosas project on the Sinaloa-Durango border, which hosts a 134-million-ounce silver-equivalent resource under a 2023 National Instrument 43-101 estimate. Its active 20,000-meter drill program recently intersected 45.1 meters true width grading 1,623 grams per metric ton silver, including 8.25 meters at 8,579 grams per metric ton silver, supporting further resource expansion at San Marcial. The company is targeting four milestones: completing its drill program, beginning bulk-sample test mining at Plomosas after Mexico's environmental regulator confirmed no additional impact authorization is required, publishing an updated mineral resource estimate in the second half of 2026, and completing a maiden preliminary economic assessment in the first half of 2027. The company reported approximately C$28.5 million in cash and no debt as of late May 2026.

Eric Zaunscherb, Executive Chair and Interim President and Chief Executive Officer of GR Silver Mining, outlines the discovery economics behind the resource growth:

"We have 134 million ounces of silver equivalent, and we feel that has a significant chance to grow through our 20,000 meter drill program. Historically, we've added ounces at 12 cents US per ounce and we're currently trading at over a dollar 20 US per ounce."

Mine Supply, Not Demand, Drives the Silver Deficit

The 2026 data shows that changes in industrial demand no longer explain changes in the overall silver market balance on their own. Record thrifting in the solar industry shows that manufacturers reduce silver use per solar cell as higher prices compress module margins, demonstrating that industrial demand responds to price signals. The deficit still widened, indicating that limited mine supply growth, rather than industrial demand, has become the primary driver of the silver market balance.

This changes the assumptions used to evaluate how the silver market could evolve over the coming years. A deficit driven primarily by stronger demand would narrow if industrial consumption weakened because manufacturers have already demonstrated they reduce silver use when higher prices compress margins. A deficit that widens even as demand declines indicates that mine supply cannot increase quickly enough to balance the market, regardless of short-term changes in consumption.

The Investment Thesis for Silver

- The widening deficit despite a record decline in solar photovoltaic demand indicates that limited mine supply, rather than industrial demand, has become the primary driver of the silver market deficit.

- Falling all-in sustaining costs alongside limited mine production growth indicate that existing producers are expanding operating margins without delivering a comparable increase in silver supply.

- Rising investment demand, led by a sharp rebound in US retail buying, is absorbing more of the silver deficit, making investment flows as important as industrial demand when evaluating the market balance.

- Growth in AI data centers, automotive electronics, and electrical transmission equipment is reducing industrial silver demand's reliance on photovoltaic applications, although these sectors remain too small to fully offset the decline in solar demand.

- Brownfield expansions at existing, permitted operations offer the shortest timeline for adding near-term silver supply because they build on existing infrastructure and regulatory approvals rather than requiring new mine development.

- Development-stage projects with completed feasibility studies represent the medium-term source of new silver supply, provided favorable market conditions continue to support project financing and development.

- Early-stage exploration assets represent the longest-term source of future silver supply, but the time required for resource conversion, technical studies, permitting, and construction means they cannot address the current market deficit.

Silver's 2026 market data shows that weaker industrial demand alone no longer explains the market deficit. The solar sector, long the largest source of industrial silver demand, recorded its sharpest demand decline on record, yet the global silver deficit still widened. The evidence points to mine production growth, resource conversion, and permitting timelines as the primary factors determining how quickly the silver deficit can narrow, rather than changes in industrial demand. The key question is no longer whether industrial demand will remain strong, but how quickly new mine supply can reach the market while industrial and investment demand continue to absorb available silver.

TL;DR

Solar photovoltaic demand recorded its largest annual decline on record in 2026, yet the global silver deficit widened for a sixth consecutive year because mine supply failed to keep pace with demand. While manufacturers reduced silver use through thrifting, physical investment demand strengthened and industrial demand broadened into AI infrastructure, electrical transmission equipment, and automotive electronics. The data suggests that mine production growth, permitting timelines, and project development now deserve greater attention than industrial demand forecasts when assessing how long the silver market deficit could persist.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed