Strait of Hormuz Disruptions and Federal Reserve Rate Compress Silver Prices from January 2026 Highs

Silver has dropped ~44% from its January 2026 all-time high as Fed rate pressure overrides safe-haven demand, here's what investors need to know.

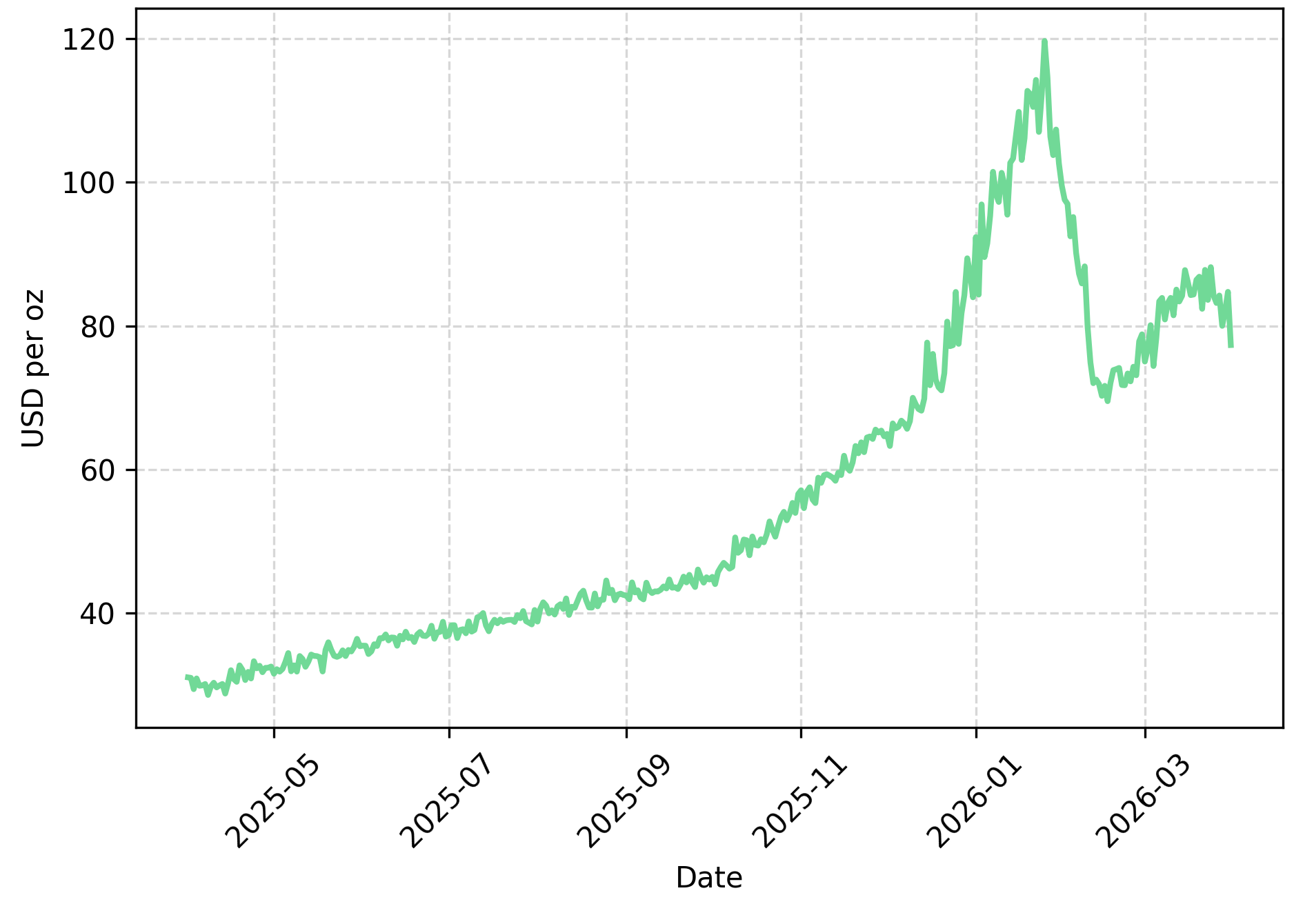

- Silver has fallen approximately 44% from its January 2026 all-time high of approximately $121.64/oz to approximately $67/oz as of March 26, 2026, with a further decline of approximately 27.9% recorded over the past month, reflecting interest rate pressure rather than weakening industrial or investment fundamentals.

- Energy supply disruptions linked to Iran-related geopolitical risk are elevating oil prices and forcing central banks into a prolonged hawkish stance that raises the opportunity cost of holding non-yielding assets.

- Higher real interest rates are accelerating capital rotation away from silver into yield-bearing instruments, compressing near-term price performance despite unchanged long-term demand drivers.

- Short-term liquidity dynamics are overriding safe-haven demand, a pattern consistent with behavior observed at the onset of the Russia-Ukraine conflict in early 2022, when gold initially rose before falling as the inflation shock fed through to rate expectations.

- Silver's recovery depends on one of two conditions: a central bank pivot toward rate cuts, which reduces the opportunity cost of holding the metal, or stagflation in which high inflation coincides with slowing economic growth

Why Geopolitical Tensions May Not be Supporting Silver Prices

The current silver market presents an apparent contradiction: escalating geopolitical tension, particularly around Iran's rejection of ceasefire proposals and risks to Strait of Hormuz shipping lanes, has produced sustained selling pressure rather than safe-haven inflows. Silver is trading at approximately $67/oz, down approximately 44% from its January 2026 all-time high of approximately $121.64/oz and approximately 27.9% over the trailing month.

This reflects a shift in how the market is pricing competing risk factors. In prior cycles, geopolitical instability increased demand for precious metals through a direct safe-haven mechanism. In the current cycle, inflation and monetary policy expectations are dominating investor decision-making, overriding that traditional relationship. The transmission mechanism is direct: energy supply disruption raises oil prices, feeding into elevated inflation expectations, reinforcing central bank hawkishness, and increasing the opportunity cost of holding non-yielding assets like silver.

This highlights a critical misconception, geopolitical crises are not universally bullish for silver, particularly when the primary policy response to that instability is monetary tightening.

Rate Sensitivity & the Opportunity Cost Framework in a High-Inflation Regime

Silver's price behavior is a direct function of real interest rates, which determine the opportunity cost of holding a non-yielding asset. When real rates rise, capital reallocates toward bonds and cash instruments that generate measurable returns. Silver, which carries no coupon, dividend, or cash flow, faces direct valuation compression under this mechanism.

The current environment is characterized by persistent central bank guidance toward higher-for-longer rates, driven by energy-driven inflation that is proving resistant to conventional tightening cycles. Each upward revision to inflation forecasts extends the period during which silver underperforms yield-bearing alternatives.

Liquidity Over Safety: Crisis Behavior & Its Effect on Silver

During periods of acute market stress, institutional investors sell liquid assets, including silver and gold, to raise cash for margin calls or portfolio rebalancing. This is not a reflection of changed views on precious metals' long-term value; it is a consequence of risk management frameworks that prioritize liquidity over asset class preference. This pattern was observable at the onset of the Russia-Ukraine conflict in February 2022, when gold prices initially rose but fell back as the inflation shock fed through to rate expectations. Distinguishing between a liquidity-driven dislocation and a fundamental deterioration in demand is the most consequential analytical task facing investors assessing entry timing.

Company Positioning in a Weak Price Environment: Cost Discipline & Asset Quality Matter

Macro factors set the price environment, but company-level fundamentals determine which producers sustain margins and which developers preserve optionality through the cycle. In a declining silver price environment, the critical variables are all-in sustaining cost per ounce and the capital efficiency of resource growth.

Margin Resilience at the Production Stage

Americas Gold & Silver operates the Galena Complex in Idaho's Silver Valley, ranked the third-highest-grade active primary silver mine globally with a 2025 estimated average head grade of approximately 490 g/t silver. The Cosalá EC120 Mine in Sinaloa, Mexico carries a forward-guided all-in sustaining cost of approximately $10.80/oz per the same presentation, with Cosalá having achieved a record 1.2 million ounces silver in 2025. The company has executed a systematic transition from underhand cut-and-fill mining to long-hole stoping, reducing cost per tonne through economies of scale while targeting higher-grade zones.

Oliver Turner of Americas Gold & Silver describes the operational logic:

"Your cost per ton comes down due to economies of scale. How do we increase the amount or the number of ounces in each one of those tons we have? That's where we go after grade... We're focused on expanding high-margin ounces and high-margin tons."

A joint venture formed in February 2026 to establish an antimony processing facility within Galena's existing permit boundary is targeting construction completion in under 18 months. The Crescent Mine, acquired December 12, 2025, is being integrated into the Galena complex using existing processing capacity. T. Rowe Price and BlackRock are confirmed institutional shareholders as of December 17, 2025, per the March 2026 Corporate Presentation. The management team's track record spans comparable operational turnarounds at Klondex, sold to Hecla for C$740 million, and Karora, where a comparable strategy preceded a C$2.1 billion merger, per company filings and S&P Capital IQ.

Macro Triggers Driving Volatility: Energy Markets, Policy Signals & Capital Flows

Iran's continued rejection of ceasefire proposals and its insistence on maintaining influence over the Strait of Hormuz has elevated energy supply risk. Increasing U.S. military presence in the region raises the probability of supply disruption scenarios that feed directly into oil price forecasts and inflation expectations.

Central banks are responding by reinforcing guidance toward sustained elevated rates, with particular concern about second-round effects, wage growth and core inflation persistence, that would delay any rate reduction. Quarter-end forecasts place silver at approximately $68/oz, with 12-month targets at approximately $82/oz contingent on central banks cutting rates or inflation decelerating without further tightening.

The Investment Thesis for Silver

- Current price weakness reflects monetary policy transmission rather than structural demand deterioration, creating a potential positioning opportunity for investors with multi-year time horizons aligned with a macro regime shift.

- Low all-in sustaining cost producers such as Americas Gold & Silver, with Cosalá EC120 carrying forward-guided all-in sustaining cost of approximately $10.80/oz and Galena ranked third globally among active primary silver mines by head grade, maintain operating margins at current spot prices and provide direct leverage to price recovery.

- Americas Gold & Silver's antimony joint venture, operating under existing Galena permits with construction targeting completion in under 18 months, provides critical minerals exposure and a cost offset that reduces net silver price sensitivity while aligning with active U.S. supply chain policy priorities.

- Developers with low discovery costs and strong balance sheets, such as GR Silver Mining at approximately CAD$0.17/oz discovery cost and C$28.2 million cash with no debt, retain capital optionality through the current downcycle without requiring dilutive equity issuance at compressed valuations.

- GR Silver Mining's planned H2 2026 resource update and maiden preliminary economic assessment provide idiosyncratic return drivers independent of macro price direction, with a five-year drilling permit and 46 permitted sites supporting multi-year resource growth.

- The structural sequencing of institutional capital re-entry, large-cap producers first, developers second, explorers third, means current developer valuations may represent the most asymmetric positioning available for investors establishing exposure ahead of the institutional re-entry phase.

Silver's decline of approximately 44.4% from its January 2026 all-time high to approximately $67.64/oz as of March 26, 2026 is not a signal that the metal's investment thesis has deteriorated. It is a signal that monetary policy, specifically the rate response to energy-driven inflation, is currently the dominant price mechanism, temporarily overriding safe-haven demand.

The practical implication is a reframing of what to monitor: interest rates and energy prices, not geopolitical headlines, are the proximate drivers of near-term price direction. When the policy headwind fades, through rate normalization, energy price stabilization, or a stagflation-driven shift in asset allocation, silver's supply scarcity, the operating leverage of low-cost producers, and the resource upside of well-capitalized developers are positioned to reassert their investment case across institutional and sophisticated retail portfolios alike.

TL;DR

Silver's decline from its January 2026 all-time high of approximately $121.64/oz to approximately $67/oz is driven by monetary policy transmission, not deteriorating industrial or investment fundamentals. Energy supply disruptions tied to Strait of Hormuz geopolitical risk are sustaining elevated inflation expectations, keeping central banks in a hawkish stance that raises the opportunity cost of holding non-yielding assets. Recovery hinges on rate cuts or stagflation-driven asset reallocation. Low-cost producers like Americas Gold and Silver, with Cosalá EC120 carrying a forward-guided all-in sustaining cost of approximately $10.80/oz, maintain margins at current spot prices, while well-capitalized developers like GR Silver Mining retain capital optionality without requiring dilutive equity issuance through the downcycle.

FAQs (AI-Generated)

Geopolitical instability around the Strait of Hormuz is elevating oil prices, which feeds directly into inflation expectations and reinforces central bank hawkishness. Higher real interest rates increase the opportunity cost of holding non-yielding assets like silver, causing capital to rotate into yield-bearing instruments. In the current cycle, monetary policy is the dominant price mechanism, overriding the traditional safe-haven relationship between geopolitical risk and precious metals demand.

Silver's recovery depends on one of two macro conditions: a central bank pivot toward rate cuts, which would reduce the opportunity cost of holding the metal, or the emergence of stagflation, in which high inflation coincides with slowing economic growth and forces a shift in asset allocation away from yield-bearing instruments. Near-term forecasts place silver at approximately $68/oz, with 12-month targets around $82/oz contingent on one of these conditions materializing.

Margin resilience in a weak price environment is determined by all-in sustaining cost per ounce and the capital efficiency of resource growth. Low-cost producers such as Americas Gold and Silver—operating the Galena Complex, ranked third-highest-grade active primary silver mine globally, and the Cosalá EC120 Mine with a forward-guided all-in sustaining cost of approximately $10.80/oz—maintain operating margins at current spot prices and retain direct leverage to any price recovery.

The opportunity cost framework refers to the return an investor forgoes by holding a non-yielding asset like silver instead of a yield-bearing instrument such as a bond or cash equivalent. When real interest rates rise, silver faces direct valuation compression because it generates no coupon, dividend, or cash flow. Understanding this mechanism is essential for assessing entry timing, since silver's price weakness in the current cycle reflects monetary conditions rather than any structural deterioration in demand.

Institutional capital historically re-enters the silver sector sequentially—large-cap producers first, developers second, explorers third. In a downcycle, well-capitalized developers with low discovery costs and no debt, such as GR Silver Mining at approximately CAD$0.17/oz discovery cost and C$28.2 million cash, retain capital optionality without requiring dilutive equity issuance at compressed valuations. Planned catalysts such as resource updates and maiden preliminary economic assessments provide return drivers independent of macro price direction, potentially offering asymmetric positioning for investors establishing exposure ahead of the institutional re-entry phase.

Analyst's Notes

Subscribe to Our Channel

Stay Informed