Revival Gold Secures $33M Funding to Unlock High-IRR Mercur Gold Project

Revival Gold: $208M to production by 2029, generating $300-350M/year free cash flow. $180M market cap, 0.15x NAV. Clear 3-4x rerating plus Beartrack-Arnett upside could double NAV.

- Revival Gold raised $33M (oversubscribed) plus $15M in warrant proceeds, providing full funding through to a construction decision on Mercur in early 2028

- 1.4M oz resource requiring $208M capex to produce 100K oz/year at $1,400 AISC, generating $300-350M/year free cash flow with nearly 100% IRR at $4,000 gold

- PFS by Q1 2027, feasibility and state permitting completed by end 2027, construction decision early 2028, production by early 2029 - all on private land with streamlined state-level permitting

- 4.6M oz resource with high-grade underground potential at Beartrack-Arnett currently receiving zero market valuation; doubled drill program underway with expectation of "game-changing" results by September

- $180M market cap versus path to $300-350M annual free cash flow in coming years; trading at 0.15x P/NAV with potential 3-4x rerating to developer peers before underground expansion could double NAV

Revival Gold is positioned at a critical inflection point as a US-focused gold developer with two assets poised to deliver significant value creation over the next three years. Speaking at a 121 Mining Investment Conference, CEO Hugh Agro outlined a fully-funded development strategy that prioritises the company's Mercur Gold Project in Utah for near-term production while simultaneously advancing the substantial exploration upside at Beartrack-Arnett in Idaho. With institutional ownership reaching 60% of the share register and recent oversubscribed financing providing a clear runway to a construction decision at Mercur, the company represents a relatively low-risk pathway to meaningful free cash flow generation in an amenable gold price environment.

Recent Financing Strengthens Balance Sheet

Revival Gold recently completed a $33 million financing that was oversubscribed from its initial $30 million target, demonstrating strong market demand for the company's equity. Management capped the offering despite additional interest. This capital, combined with approximately $15 million in anticipated warrant proceeds over the next 18 months, provides full funding through to a construction decision on the Mercur Project in early 2028. The financing represents a strategic milestone, eliminating near-term dilution risk and allowing the company to advance systematic derisking activities across both project portfolios without capital constraints.

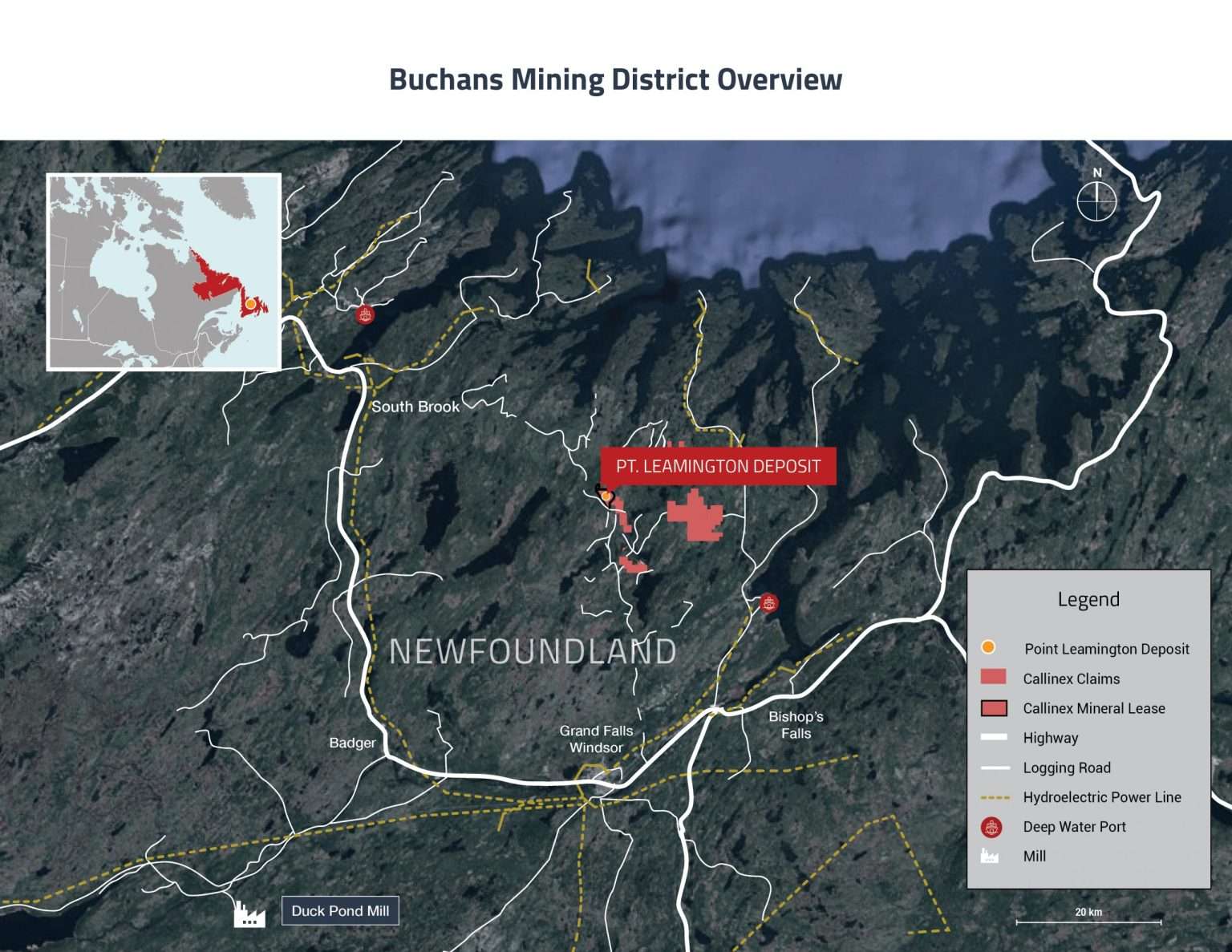

Mercur Project: Robust Economics in a Tier-One Jurisdiction

The Mercur Gold Project in Utah forms the cornerstone of Revival Gold's near-term value proposition. The project hosts 1.4 million ounces of gold and requires only $208 million in capital expenditure to reach production of 100,000 ounces annually at all-in sustaining costs of approximately $1,400 per ounce. At $4,000 gold, the project delivers nearly 100% internal rate of return - a remarkable metric for a development-stage asset.

"At current gold prices, we're talking about a project that's going to generate $300 to $350 million a year of free cash flow. That's a really interesting price for a market cap today of about $180 million US."

The project benefits from several derisking factors uncommon among development-stage gold assets. Mercur sits entirely on private land, eliminating many permitting complexities and timelines associated with federal land management. The operation will utilise open-pit heap leach processing, a proven technology previously employed at the site. Existing infrastructure includes refurbished water wells with new pumps, eliminating the need for construction of camps, power lines, or access roads. These factors collectively derisk the capital expenditure estimate and execution timeline.

Accelerated Development Timeline with State-Level Permitting

Revival Gold has outlined a clear development pathway with specific milestones. The company plans to deliver a Prefeasibility Study (PFS) by the end of the first quarter of 2027, with optimisation work focused on crush size to leverage demonstrated high kinetics (90% recovery within five days) and potential throughput expansion from 20,000 tons per day to higher rates. The PFS will transition directly into feasibility study work without significant intermediate trade-off technical studies, with both feasibility and permitting targeted for completion by the end of 2027.

Critically, Mercur's permitting process operates at the state level in Utah rather than requiring federal approvals. Agro emphasised this distinction:

"Unlike a lot of our peers who are depending on a Trump administration, a fast 41 program, all of those bells and whistles, we are not engaged in federal permitting here. This is state permitting."

The company has received positive indications from Utah state officials, including the governor, regarding support for the project. With a construction decision targeted for early 2028 and approximately one year of construction, gold production is anticipated in early 2029 - representing a remarkably short timeline from current position to cash generation.

Interview with Hugh Agro, CEO, Revival Gold

Beartrack-Arnett: Substantial Exploration Upside

While Mercur provides near-term cash flow visibility, the Beartrack-Arnett project in Idaho represents significant exploration upside currently receiving minimal market valuation. The project hosts 4.6 million ounces of gold, including over one kilometer of strike length in underground high-grade zones. Revival Gold has doubled its drill program at the site, deploying two drill rigs to extend depth and strike, with results expected by the Beaver Creek Conference in September.

The company is systematically testing expansion potential while advancing engineering for a phased development approach. Agro indicated the underground potential could "double our NAV," representing substantial value creation beyond the already robust Mercur economics.

"When an investor buys Revival Gold today, they're getting all of the infrastructure for free. They're getting the move to $300 to $350 million of free cash flow in the next couple of years, and they're getting a Beartrack-Arnett with this massive underground opportunity."

Production Strategy: Cash Flow Drives Pipeline

Revival Gold's strategy prioritises free cash flow generation as the mechanism to fund subsequent development phases. The $208 million capital requirement for Mercur positions it as the initial production asset, generating cash to fund the Beartrack-Arnett development sequence. The company envisions a phased approach at Beartrack beginning with open-pit heap leach operations followed by underground mining. Combined, the three phases - Mercur open pit, Beartrack open pit, and Beartrack underground - target approximately 300,000 ounces per year of gold production from a 6 million ounce resource base across both projects.

Management retains flexibility to adjust sequencing based on underground exploration results, potentially advancing high-grade underground development ahead of open-pit phases if value accretion warrants. This strategic optionality reflects confidence in the Beartrack-Arnett drilling program and allows for dynamic capital allocation as results emerge.

US Jurisdiction Provides Strategic Advantage

Revival Gold's exclusive focus on United States assets provides meaningful advantages in the current market environment. Agro noted a structural shift among senior and intermediate gold producers toward North American exposure, driven by investor preferences for lower-risk jurisdictions. Major producers including Centerra, SSR Mining, Kinross, Hecla, and Barrick Gold are all increasing their US operational footprints in response to challenges in higher-risk geographies.

This jurisdictional focus extends to capital access. As senior gold producers pay down debt and improve balance sheets, lending institutions previously servicing these credits are seeking new development-stage projects - but specifically in Tier 1 geographies.

"They've had their issues in Africa and in parts of South America with expropriation, with changing of tax policies, and they're looking for opportunities in the cleaner jurisdictions: Australia, Canada, and the United States."

Revival Gold is positioned to access this capital on favourable terms for projects of appropriate scale.

Valuation and Merger & Acquisition Positioning

Revival Gold trades at a market capitalisation of approximately $180 million US, representing 0.15 times price-to-net asset value. According to Agro, this valuation appears disconnected from near-term free cash flow generation potential and peer comparisons. Agro identified a 3-4x rerating opportunity simply by reaching peer developer valuations for companies approaching first production, achievable within 18-24 months as Mercur advances through feasibility and permitting. The addition of underground resource expansion at Beartrack-Arnett could potentially double net asset value, suggesting a 6-8x return pathway from current levels.

The company referenced the Rupert Resources acquisition by Agnico Eagle at approximately $500 per ounce as a potential valuation framework, which would imply a $3 billion market capitalisation for Revival Gold's resource base. While acknowledging this as an aspirational target, the comparison illustrates the substantial value gap between current trading levels and potential strategic value to larger producers seeking US production platforms. Management's strategy focuses on systematic derisking through engineering advancement, production demonstration, and resource expansion to create competitive tension among potential acquirers while building shareholder value through organic development.

The Investment Thesis for Revival Gold

- Fully-Funded Near-Term Producer: $33M financing plus $15M warrant proceeds provides complete funding through construction decision in early 2028, eliminating dilution risk during critical development phase

- Exceptional Project Economics: Mercur's nearly 100% IRR at $4,000 gold with $208M capex to reach $300-350M annual free cash flow represents rare risk-reward profile in development sector

- Accelerated, Low-Risk Timeline: State-level permitting on private land with proven technology and existing infrastructure provides clear 2029 production pathway with minimal execution risk

- Substantial Exploration Upside: 4.6M oz Beartrack-Arnett resource with high-grade underground potential currently receiving zero market valuation; doubled drill program targeting transformational results

- Strategic Jurisdiction: Exclusive US focus aligns with sector-wide migration to lower-risk geographies and positions company for favorable debt financing and strategic interest

- Compelling Valuation Disconnect: 0.15x P/NAV with clear 3-4x near-term rerating pathway to developer peers, plus potential NAV doubling from underground expansion

- Scalable Production Platform: Clear pathway to 300K oz/year production from 6M oz resource base positions company as meaningful mid-tier US producer

- Experienced Management with Institutional Backing: 60% institutional ownership and oversubscribed financing demonstrates market confidence in execution capability

Macro Thematic Analysis

The gold sector is experiencing a fundamental shift as investors and producers alike prioritise jurisdictional quality over purely geological merit. Revival Gold exemplifies this trend, offering exclusive exposure to United States gold development at a time when major producers are systematically rebalancing portfolios away from higher-risk geographies following expropriation events and policy changes. This "reshoring" of gold production creates structural demand for US-focused platforms, particularly as lending institutions redirect capital from deleveraging seniors toward development projects in cleaner jurisdictions. The convergence of near-record gold prices, institutional capital availability for North American mining, and investor appetite for domestic exposure creates an optimal environment for Revival Gold's transition from developer to producer. As Agro noted:

"Their owners are looking for exposure in North America and in the United States. That's where they want to take their investment."

TL;DR

Revival Gold offers a fully-funded pathway to 2029 production at Mercur (100K oz/year, $300-350M annual free cash flow, $208M capex) with exceptional economics (nearly 100% IRR) on an accelerated state permitting timeline. Current $180M market cap trades at 0.15x NAV with clear 3-4x rerating to developer peers before Beartrack-Arnett's 4.6M oz underground upside potentially doubles NAV, creating 6-8x return pathway. Exclusive US jurisdiction focus positions company for favorable financing and strategic interest amid sector migration to lower-risk geographies.

FAQ's (AI Generated)

Analyst's Notes

Subscribe to Our Channel

%20(2)%20(2).jpg)

Stay Informed