PFS Pathway and District Expansion Drive Oroco Resource Corp Growth Strategy

Oroco advances Santo Tomás copper project to PFS (Q2 2027) with half-industry capital intensity, strong economics, Plan Mexico support. Transaction-ready mid-2027.

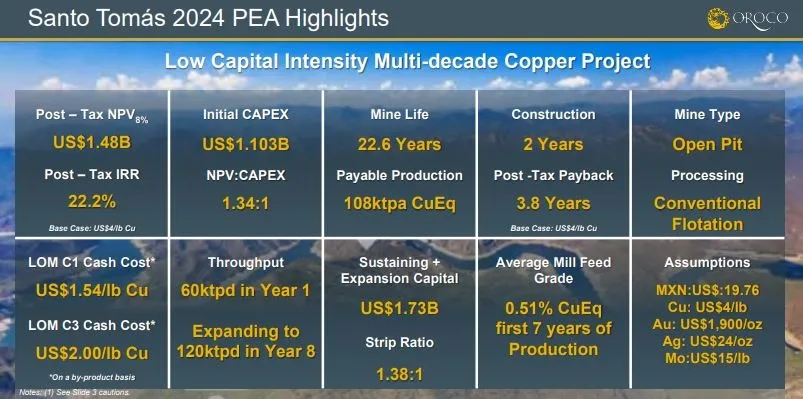

- Santo Tomás porphyry copper project in northwest Mexico delivered August 2024 PEA showing $1.5B NPV, 22%+ IRR, and $1.1B capex at $4 copper - significantly below industry capital intensity

- Pre-Feasibility Study (PFS) targeted for Q2 2027, converting 1 billion ton resource from inferred to indicated category while expanding South Zone potential

- Pursuing porphyry district development with Bahuerachi (north), Santo Tomás (center), and Vainilla exploration project (south) to enhance strategic value for acquirers

- Included on Plan México - President Sheinbaum's list of 40 large capex investment projects - driven by grassroots community support seeking regional economic development

- New CEO Charles Cryer joining mid-June 2026 to lead toward transaction-ready status by next year

Oroco Resources is advancing the Santo Tomás porphyry copper project in northwest Mexico through a critical development phase, targeting completion of a Pre-Feasibility Study in Q2 2027. The company's journey from legal battles over title to publishing positive preliminary economics represents a compelling case study in resource development, particularly given the current copper market dynamics and Mexico's evolving mining policy environment. This analysis examines the project's technical merits, development pathway, and strategic positioning for investors considering exposure to copper through junior developers.

Project Fundamentals and Economic Framework

The Santo Tomás project delivered a Preliminary Economic Assessment (PEA) in August 2024 that established baseline economics using conservative metal price assumptions. At $4.00 copper and $1,900 gold, the study demonstrated an after-tax NPV of $1.48 billion with internal rates of return exceeding 22.2%. The initial capital requirement stands at approximately $1.1 billion for a 60,000 ton-per-day operation, expanding to 120,000 tons per day in year seven through balance sheet financing.

What distinguishes Santo Tomás from peers is its capital efficiency which is roughly half the industry standard. It creates a lower barrier for potential acquirers and reduces development risk in an environment where project capital costs have escalated significantly.

The resource base comprises over one billion tons of combined indicated and inferred material grading just over 0.5% copper equivalent. While grades are at the lower end of the porphyry spectrum, the operation benefits from no initial strip ratio, enabling access to higher-grade material early in the mine life with a projected 3.8-year payback period. Operating costs are projected below $1 per pound at current copper prices near $6, providing substantial operating margins even in a softer commodity environment.

Pre-Feasibility Study Focus and Technical Optimisation

Oroco's immediate technical focus centers on converting the South Zone inferred resource to indicated category - a requirement for overlaying a PFS mine plan. The drilling campaign currently underway also targets South Zone expansion, particularly to the southwest where management sees material upside potential.

Beyond resource conversion, metallurgical optimisation emerged as a key value driver. Whittle Consulting's strategic review identified that 70-80% of the resource comprises softer material than originally tested, suggesting opportunities for reduced crushing energy requirements, enhanced copper liberation, and potentially higher throughput rates. These incremental improvements could materially impact operating costs and production profiles when incorporated into the PFS.

The company raised capital in January 2026 to fund the technical work program, though President Ian Graham acknowledged that additional working capital will likely be required to complete the PFS. This financing is expected to follow the January pattern - institutional rather than retail - and will likely be provided via Canaccord Genuity relationship from the last financing.

District Development Strategy

Oroco's strategic vision extends beyond Santo Tomás as a standalone asset. The company acquired an option on the Vainilla exploration project immediately south of Santo Tomás, which management believes represents another porphyry center. Combined with the Bahuerachi project to the north, this creates potential for a three-deposit porphyry district with shared infrastructure.

Graham articulated the strategic rationale:

"We see this sort of district potential, not just a single porphyry mine, as being part of the greater story for Santo Tomás."

The district concept enhances the asset's attractiveness to potential acquirers by demonstrating longer-term production potential beyond the current Santo Tomás reserve base and providing economies of scale for infrastructure investment. However, Graham noted that proving up Vainilla is not the immediate focus - the priority remains advancing Santo Tomás to PFS completion.

Interview with Ian Graham, President, Oroco Resources

Community Support and Political Environment

Perhaps the most unusual aspect of Oroco's development pathway is the grassroots community support that led to inclusion on Plan México, President Claudia Sheinbaum's prioritised list of 40 large capital investment projects. Graham emphasised that this recognition came entirely from community advocacy rather than company lobbying:

"It was the community that brought us to the federal government through their congressman to have us placed on Plan México, which is the president's list of large capex foreign and domestic investment projects."

This political support carries significance beyond optics. Mexico's mining sector faced uncertainty under previous administration, with permitting backlogs and policy ambiguity. Graham reported that the permitting environment has improved under Sheinbaum, with 60% of the backlog cleared and expectations for additional large permits in 2026. The company is positioning PFS delivery to coincide with restored confidence in Mexican mining development.

The community's motivation stems from regional economic development needs. Operations have been remobilised on the ground with drilling programs underway and the local team reconstituted. Graham characterised the current status as "business as usual" with partners fully re-engaged.

Strategic Transition and Market Positioning

Oroco faces a credibility challenge stemming from its 2020-2021 market run-up followed by significant price correction. The company is working to rebuild institutional confidence through demonstrated execution - publishing assay results, maintaining drilling momentum, and progressing toward PFS milestones.

The appointment of Charlie Cryer as CEO, effective mid-2026, represents a strategic shift toward transaction positioning. Charles Cryer previously covered Santo Tomás as an analyst at RFC Ambrian, publishing research in 2018-2019 identifying copper supply challenges and highlighting Santo Tomás as a potential solution. His M&A experience and industry network are intended to elevate the company's profile with strategic players and position the asset for transaction discussions following PFS completion.

Graham indicated the project will be "transaction ready" by next year, targeting Q2 2027for PFS delivery. The company remains open to various transaction structures that facilitate development, recognising its obligation to deliver on community and political support. The exit strategy centers on selling to growth-oriented copper producers capable of financing the $1.1 billion capex requirement.

Competitive Positioning in the Copper Market

Santo Tomás' competitive positioning rests on several factors. The capital intensity of approximately $10,000 per ton of annual copper production positions it favourably against industry averages which are more than double, expanding the universe of potential acquirers beyond major producers to include mid-tier companies seeking growth assets. The 3.8-year payback period provides attractive risk-adjusted returns for developers willing to navigate Mexican jurisdictional considerations.

The project benefits from polymetallic credits - silver, gold, and molybdenum are all payable, with a dedicated molybdenum circuit included in the PEA mine plan. These by-products enhance unit economics, though Graham noted molybdenum markets exhibit more volatility than copper.

Oroco's investor base has historically skewed retail with a longtime European contingent. The January 2026 financing marked a transition toward institutional capital, which Graham indicated will continue. European investors have been "vocal in recent years around us keeping moving," providing both capital and accountability for execution.

Conclusion

The global copper supply-demand imbalance represents one of the most compelling investment themes in commodities markets. Electrification trends, renewable energy infrastructure, and grid modernisation are driving unprecedented copper intensity per unit of GDP growth. Simultaneously, the project pipeline has failed to keep pace - decades of underinvestment, permitting challenges, declining ore grades, and capital cost inflation have constrained new supply additions. Santo Tomás emerges at a critical inflection point where economically viable, jurisdictionally acceptable copper projects command premium valuations. The capital efficiency demonstrated in Oroco's PEA - roughly half the industry standard per ton of production - positions the asset favorably for development in an environment where $30,000+ per ton capital intensity has rendered many historical resources uneconomic. As Graham noted regarding RFC Ambrian's prescient 2018-2019 research:

"They published a research piece called the ‘Cupboard is bare’ regarding copper. They were quite visionary in terms of where we are today with respect to copper several years ago."

TL;DR: Executive Summary

Oroco Resources is advancing the Santo Tomás porphyry copper project toward Pre-Feasibility Study completion in Q2 2027, targeting transaction-ready status with significantly below-industry capital intensity ($10k vs. $21-33k per ton). The project delivered strong preliminary economics ($1.48B NPV, 22.2%+ IRR at $4 copper) and benefits from unique community-driven political support through inclusion on Mexico's Plan México prioritised investment list. With a new CEO focused on M&A positioning, 1+ billion ton resource base, and strategic district potential, Santo Tomás represents a scalable copper development opportunity in a supply-constrained market.

FAQ's (AI Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).png)

Stay Informed