Sulfur Costs, Indonesian Policy, and US Capital Qualification Re-Rate Low-Cost Battery Metals Developers

Geopolitics, cost curves, and policy now determine battery metals winners, favoring low-cost, integrated projects aligned with US and Canadian support.

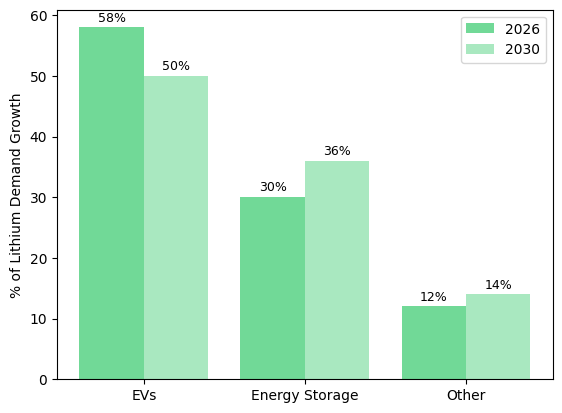

- High Pressure Acid Leach (HPAL) nickel laterite unit cost is a direct function of delivered sulfuric acid price, with operator technical disclosures reporting consumption of 2.5 to 4.0 tonnes of sulfuric acid per tonne of nickel in mixed hydroxide precipitate. Middle East sulfur logistics disruption transmits into Indonesian unit costs through this reagent channel, while sulfide operators with native orebody sulfur bypass the transmission entirely.

- Indonesian policy has shifted mined nickel clearance from volume to value maximization across the largest single-country source per United States Geological Survey 2025 Mineral Commodity Summaries, repricing institutional price decks anchored to the 2020 to 2024 Indonesian ramp-up thesis.

- Non-Chinese graphite developers compete against a supply base concentrated in China per United States Geological Survey 2025 Mineral Commodity Summaries, with flake graphite clearing below the operating cost of most third and fourth-quartile non-Chinese developers. First-quartile cost positioning is the survivability variable, not an optimization variable.

- US industrial-policy capital under the Inflation Reduction Act of 2022 and Department of Defense Defense Production Act Title III conditions non-dilutive funding on domestic processing to separated-oxide or battery-grade specification, creating a cost-of-capital differential between concentrate producers and integrated developers.

- Canadian federal and provincial critical-minerals frameworks deliver non-dilutive capital through refundable tax credits and strategic-offtake alignment with qualified original equipment manufacturers, making jurisdictional eligibility a direct Net Present Value input rather than a separate risk overlay.

Geopolitical Reagent Disruption & Policy-Driven Supply Discipline Re-Rate Low-Cost Battery Metals Developers

Macroeconomic realignments spanning Middle East logistics corridors, Indonesian administrative export policies, and United States industrial capital deployment protocols structurally bifurcate the funding window available to development-stage battery metals equities. These three distinct mechanisms force institutional investors to reprice project cost curves, shifting valuation models away from theoretical resource scale and toward margin survivability under constrained operating environments. Capital allocation data through the first quarter of 2026 demonstrates that projects failing to secure first-quartile operating profiles or jurisdictional qualification for non-dilutive federal capital face prohibitive weighted average cost of capital penalties.

Sulfur logistics bottlenecks dictate unit costs by elevating reagent procurement expenses. Sovereign administrative decrees dictate the physical clearing price of mined output by restricting export volumes. Federal industrial policy dictates capital structures by awarding non-dilutive grants exclusively to operations capable of producing separated-oxide or battery-grade materials. These factors require fund managers to apply higher discount rates to projects exposed to reagent inflation or foreign supply chain dependencies.

Consequently, development-stage entities possessing first-quartile All-In Sustaining Cost profiles, finalized Definitive Feasibility Studies, and jurisdictional qualification for federal capital frameworks secure financing tranches, while operations lacking these attributes suffer structural capital starvation. The analytical standard for capital deployment now mandates that project economics remain robust when benchmarked against Chinese or Indonesian clearing prices rather than consensus forward price decks. This operating reality establishes cost curve positioning and downstream processing integration as the primary determinants of equity survivability.

Middle East Sulfur Logistics Differentiate Nickel Unit Costs

High Pressure Acid Leach flowsheets deployed across Indonesian nickel laterite operations require continuous inputs of sulfuric acid as the primary metallurgical leach reagent. Operator technical disclosures and definitive feasibility documentation indicate that these processing facilities consume 2.5 to 4.0 tonnes of sulfuric acid to precipitate one single tonne of nickel contained within mixed hydroxide precipitate. Because sulfuric acid derives primarily from elemental sulfur recovered as a byproduct of hydrocarbon processing, pricing remains inextricably linked to global petrochemical supply chains.

Native Sulfur Advantage Insulates Sulfide Operations

Sulfide nickel extraction projects possessing sulfur native to the host orebody bypass the external reagent procurement transmission mechanism entirely. Flowsheets designed for sulfide mineralization utilize flotation and subsequent smelting or hydrometallurgical refining processes that leverage the internal chemical composition of the rock, eliminating the requirement to import bulk sulfuric acid. Lifezone Metals holds the Kabanga nickel sulfide project in Tanzania, with company technical disclosures reporting a concentrate grade of 17 to 18 percent nickel produced from a 2 percent nickel feedstock.

To quantify the input-cost position against Indonesian laterite peers, Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, identifies native sulfur as a direct operating-margin variable:

“30% of our rock is sulfur, we do not have to add or transport sulfur, while Indonesian operations suffer from high sulfur prices.”

The sensitivity to external sulfur logistics establishes a permanent variable separating the economic viability of the two distinct development paths. During periods of Middle East logistical disruption, the operating-cost spread between native-sulfur sulfide projects and acid-dependent laterite operations widens substantially, generating superior free cash flow profiles for the insulated assets without requiring a proportional rise in base metal commodity prices.

Indonesian Supply Policy Reprices the Nickel Clearing Price

The US Geological Survey 2025 Mineral Commodity Summaries records Indonesia as the largest single-country source of mined nickel production by a substantial margin over the next-largest producer. When a single sovereign controls the majority of mined nickel supply and exercises administrative discretion over export permit volumes, royalty structures, and domestic benchmark pricing, the nickel clearing price is no longer determined solely by the intersection of global supply and demand at marginal cost. It is also determined by Indonesian administrative policy.

For developers sitting outside Indonesian supply, including Canadian and East African sulfide projects, the consequence is a widening premium between physical-market realization and benchmark LME price. That premium flows directly into NPV calculations through the long-term realized-price input, and is the single variable that most compresses the market-cap-to-Net-Asset-Value discount on non-Indonesian nickel developers.

First-Quartile Cost Positioning Clears Against Chinese Supply Discipline

Non-Chinese graphite developers compete against a supply base that, per US Geological Survey 2025 Mineral Commodity Summaries, concentrates natural graphite mine output and spherical purified anode material production in China. Most non-Chinese flake graphite development projects disclosed in public filings operate at costs that do not clear the market against Chinese supply without either a tariff wedge or a cost restructuring.

Cost Curve Positioning Determines Market Survivability

Sovereign Metals' Kasiya rutile-graphite project in Malawi, per the Pre-Feasibility Study dated September 2023, targets incremental graphite production cost of $241 per tonne against natural flake graphite pricing that has historically traded above that level in benchmark index publications.

Ben Stoikovich, Chairman of Sovereign Metals, frames the operating-margin survivability this cost position delivers:

“Our incremental cost to produce a ton of graphite will be only $241 per ton. We’re at the very bottom of the cost curve, where other projects can’t make money.”

The screening implication is that operating cost per tonne benchmarked against the Chinese supply clearing price, rather than against consensus forecast, is the variable separating non-Chinese graphite developers that deliver return of capital through commodity price cycles from those that do not.

Processing Integration Unlocks Industrial-Policy Capital

US critical minerals industrial policy, including provisions of the Inflation Reduction Act of 2022 and Department of Defense Defense Production Act Title III awards, conditions access to non-dilutive capital on domestic processing capability, not on mined supply alone. A mining project exporting concentrate to a Chinese refinery captures only the mining margin, remains exposed to refiner-side pricing decisions, and does not qualify for United States industrial-policy programs that require domestic content at the refined-product level.

Energy Fuels operates the White Mesa Mill in Utah, the only conventional uranium mill operating in the US as of 2025, and has expanded the facility to produce separated terbium and dysprosium oxides for non-Chinese rare earth supply chains.

Mark Chalmers, Chief Executive Officer of Energy Fuels, identifies mine-to-oxide integration as the condition required to compete with Chinese midstream dominance:

“To really compete with China, you have to have all those steps, you can’t be missing a step in the middle of it. We’ve cracked the code by putting all these pieces together.”

Product-Level Qualification Drives Capital Access

Chalmers quantifies the capital access position directly, identifying approximately $2 billion as the total capital required to complete the integrated critical-minerals build-out and current deployable capital approaching $1 billion:

“Now we’re pushing a billion dollars of deployable capital, the $2 billion doesn’t look so far off. That’s a big reason why we’ve had the re-rate in our stock.”

The screening criterion is whether a project's product specification matches the domestic-content thresholds in United States and Canadian industrial-policy programs. Concentrate producers do not qualify. Producers of separated oxides, battery-grade nickel sulphate, or qualified anode material do, and the differential translates directly into both equity cost of capital and non-dilutive funding access.

Jurisdictional Alignment Converts Into Non-Dilutive Funding Access

Canadian critical-minerals policy deploys non-dilutive capital through refundable tax credit programs targeting qualifying critical-mineral projects, including nickel. Canada Nickel's Crawford project in Ontario holds both federal and provincial endorsement, qualifies for two refundable tax credit programs, and has a 10 percent direct strategic investment commitment from Samsung SDI.

Mark Selby, Chief Executive Officer of Canada Nickel, identifies the funding-visibility consequence of this policy alignment:

“We’re the only project in Canada that’s got both federal and provincial endorsement. We qualify for two refundable tax credit programs, and we have Samsung SDI there to buy 10% of the project.”

A project with government-endorsed funding pathways, contracted strategic offtake, and a completed Feasibility Study reduces the financing-risk discount institutional investors apply to the equity. A project with equivalent resource economics without these features does not. Junction toward Net Asset Value parity is driven by three specific milestones, namely nickel price realization against the price deck used in the Feasibility Study, permitting delivery on disclosed timelines, and closing of non-dilutive funding tranches that remove balance-sheet execution risk.

The Investment Thesis for Battery Metals

- Middle East sulfur logistics disruption transmits directly into Indonesian HPAL nickel unit costs through the sulfuric acid reagent channel, widening the operating-cost spread against sulfide nickel operators with native sulfur in the orebody during disruption events and compressing back only partially between events.

- Indonesian administrative discretion over export permit volumes, royalty structures, and domestic benchmark pricing has replaced marginal cost as the clearing-price mechanism for mined nickel, supporting a widening premium between physical-market realization and benchmark London Metal Exchange pricing that flows directly into Net Present Value through the long-term realized-price input.

- First-quartile operating cost benchmarked against the Chinese supply clearing price rather than consensus forecast is the variable determining which non-Chinese graphite and rare earth developers deliver return of capital through commodity price cycles, with third and fourth-quartile developers unable to clear the market without a tariff wedge.

- United States domestic-content thresholds under the Inflation Reduction Act of 2022 and Department of Defense Defense Production Act Title III condition non-dilutive capital access on processing to separated-oxide or battery-grade product specification, creating a cost-of-capital differential between concentrate producers and integrated mine-to-refined developers.

- Canadian refundable critical-mineral tax credit programs and federal-provincial project endorsement frameworks deliver identifiable non-dilutive funding channels that flow directly into Net Present Value calculations for qualifying development-stage projects, with uncovered peers applying a higher financing-risk discount to the same underlying resource economics.

- Completed Definitive Feasibility Studies, contracted strategic offtake, and disclosed non-dilutive funding pathways are the three variables now clearing institutional capital for development-stage battery metals equities, replacing resource size and grade as the dominant valuation drivers.

The battery metals market structures valuations upon verifiable input-cost insulation, localized processing capabilities, and strict jurisdictional qualification for federal capital. Operations capable of clearing global markets at prices dictated by dominant sovereign producers, while simultaneously securing the non-dilutive capital programs underwriting the Western midstream build-out, generate mathematically superior risk-adjusted return profiles. In a macroeconomic environment where industrial policy dictates supply chain viability, processing integration and base-quartile cost positioning represent the ultimate drivers of institutional capital formation.

TL;DR

Geopolitics and industrial policy, not just commodity price, are now determining which battery metals projects attract capital and generate returns. Sulfur logistics exposure raises Indonesian HPAL nickel costs while sulfide projects avoid this entirely. Indonesian policy is actively influencing global nickel pricing, and US and Canadian industrial policies are directing non-dilutive capital toward projects with downstream processing capability and jurisdictional alignment. At the same time, Chinese supply dominance forces non-Chinese graphite developers to operate in the first cost quartile to remain viable. The result is a clear screening framework: only projects with low-cost positioning, integrated processing, policy alignment, and completed feasibility pathways are clearing capital, while others are structurally excluded.

FAQs (AI-generated)

Sulfur logistics directly affect the cost of sulfuric acid, which is a core input in HPAL nickel processing. Indonesian laterite operations require large volumes of sulfuric acid, so disruptions in Middle East sulfur supply chains immediately increase operating costs. In contrast, sulphide nickel projects with naturally occurring sulfur in the orebody bypass this dependency, making their cost structures more stable and often structurally lower during disruption periods.

Indonesia, as the dominant global nickel producer, has shifted from volume-driven exports to value-maximizing policies, including export controls and domestic pricing mechanisms. This means nickel prices are no longer purely determined by global marginal cost but are increasingly shaped by Indonesian administrative decisions. As a result, non-Indonesian producers can benefit from a premium between realized prices and benchmark LME pricing, directly improving project economics.

China dominates graphite supply and effectively sets the clearing price. Most non-Chinese developers operate above this cost threshold, meaning they cannot compete without subsidies or tariffs. Only first-quartile cost producers, those operating at the lowest end of the global cost curve, can sustainably generate returns across commodity cycles, making cost positioning the key survivability factor rather than a simple efficiency metric.

US industrial policy, including the Inflation Reduction Act and Defense Production Act, prioritizes funding for projects that produce refined, battery-grade materials domestically. Projects that only mine and export concentrate do not qualify for this support and remain exposed to foreign refining markets. Integrated projects that process materials into final or near-final products can access non-dilutive capital, lowering their cost of capital and improving overall project valuation.

Jurisdiction has become a direct financial variable rather than just a risk factor. In Canada, for example, projects aligned with federal and provincial critical-minerals strategies can access refundable tax credits and strategic offtake agreements, which reduce financing risk and improve Net Present Value. Projects outside these frameworks must rely more heavily on equity or debt markets, often at higher costs, leading to valuation discounts.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed