'Undervalued?' Krakatoa Resources Advances High-Grade Zopkhito Asset as Antimony Supply Crunch Intensifies

-20(1).webp)

Krakatoa's high-grade Georgian antimony-gold project trades at 80-90% discount to peers. Phased development targets lump ore production, JORC resource by year-end.

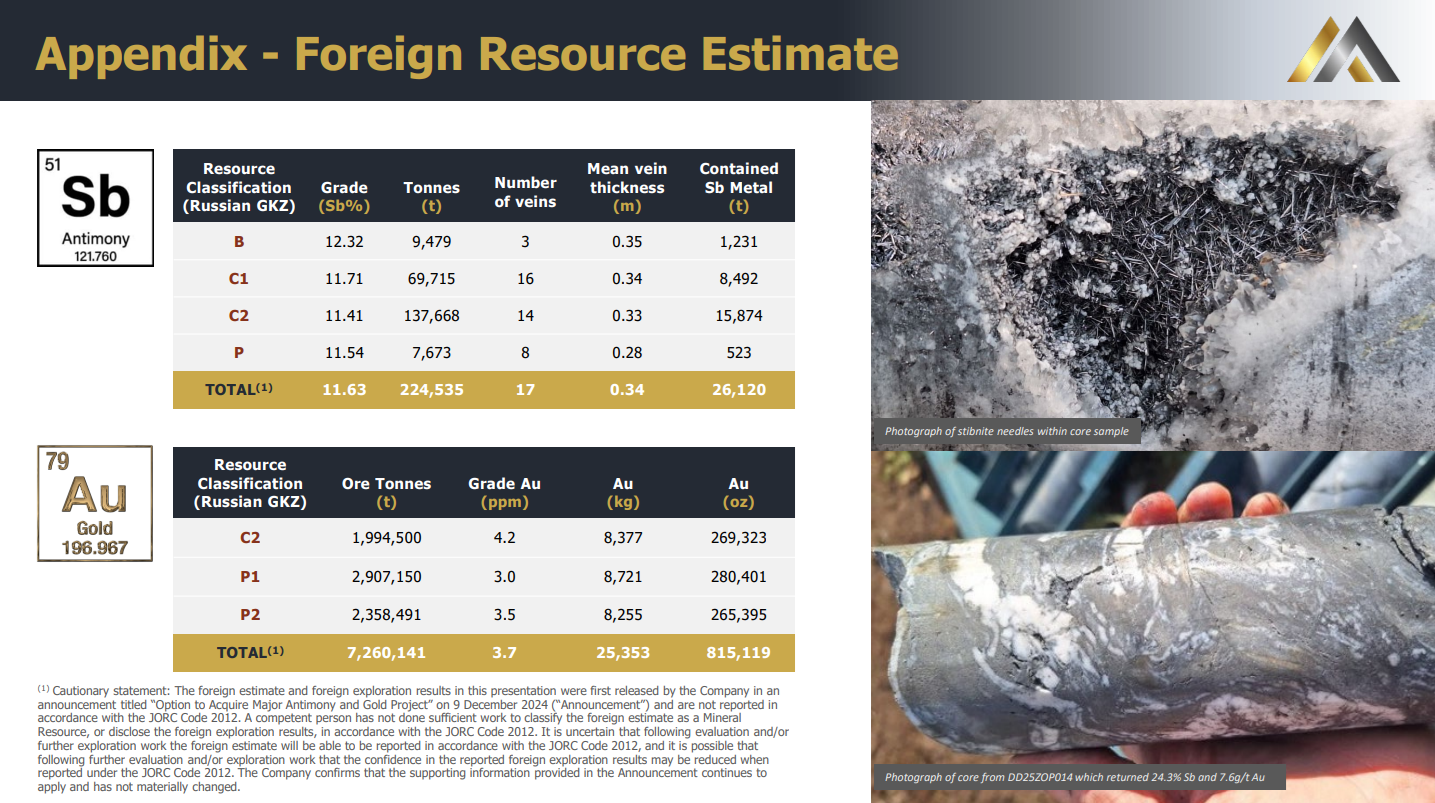

- Krakatoa Resources shows significant undervaluation at $170/ton of antimony resource versus peer companies trading at $750-$1,500/ton, despite maintaining high-grade antimony at 11.6% with 26,000 tons contained and over 800,000 ounces of gold

- Phased development strategy de-risks capital deployment: Phase 1 focuses on lump ore antimony production under existing mining license, Phase 2 adds processing facilities for concentrates, Phase 3 unlocks significant gold upside

- Underground access through existing Soviet-era adits reduces exploration costs by eliminating thousands of meters of surface drilling through host rock, with drilling from inside tunnels to accelerate JORC resource completion

- JORC-compliant resource expected by year-end 2026, supported by 20,000 historical Soviet sample points validated by recent drilling, with metallurgical studies and economic assessment to follow

- Offtake discussions progressing with European, Turkish, UAE, and US parties for critical mineral supply, with strategic consultant engaged to navigate downstream processing limitations in Europe

Krakatoa Resources CEO Mark Major believes the market fundamentally misunderstands the value proposition of the company's Zopkhito antimony and gold project in Georgia. Trading at approximately $170 per ton of contained antimony resource, the company sits at a steep discount to peer antimony developers commanding $750 to $1,500 per ton valuations. Major attributes this gap to market perception of Krakatoa as a speculative exploration company rather than recognising its transition toward development, a positioning he expects to shift as the company delivers key milestones throughout 2026.

Validation of High-Grade Deposit

Last year's drilling campaign, though delayed by logistical challenges including road and camp upgrades to infrastructure untouched for a decade, successfully validated the high-grade nature of the deposit. The company confirmed antimony grades matching or exceeding the historical foreign resource estimate of 11.6% antimony across 26,000 tons of contained metal. Importantly, drilling focused on only two veins within a system containing over 70 identified veins, of which 17 were included in the foreign resource estimate. This limited scope underscores the significant exploration upside remaining within the project area.

The validation extends beyond antimony. The gold component, currently estimated conservatively at over 800,000 ounces in the foreign resource, represents what Major describes as "the blue sky" opportunity that will differentiate Krakatoa from pure antimony plays. Gold mineralisation occurs both within the antimony veins and in the footwall and hanging wall, with the latter often showing higher grades than the vein itself.

Strategic Underground Development Approach

A key differentiator for Zopkhito lies in its mountainside geology, explored historically through adits - horizontal tunnels extending up to one kilometer into the mountain. Krakatoa cleared these tunnels and conducted drone surveys in 2025, establishing a platform for this year's underground drilling campaign. Major explains:

"This year, we intend to actually get inside those tunnels and drill from inside therefore taking away having to drill thousands of meters of host rocks to get to a vein system that's 5 m thick."

This approach dramatically reduces the meterage required to intersect mineralisation, accelerating the path to JORC compliance while managing capital expenditure. The company also plans to widen certain adits as part of pre-mining activities, with bulk samples taken during this process contributing directly to JORC-compliant resource calculations.

JORC Resource Timeline, Historical Data Integration

Krakatoa is targeting completion of a JORC-compliant resource by year end to early 2027. This resource will incorporate over 20,000 sample points from Soviet-era exploration that the company has been quality assuring and quality controlling. Major notes the historical data appears acceptable under JORC code standards, as recent underground drilling returned results consistent with Soviet-era face sampling from the adits.

The company is working with consultants to integrate this historical dataset with modern drilling results. Rather than attempting to define the entire 70-vein system, Krakatoa will focus on specific areas aligned with its phased development strategy, prioritising resources that can move quickly into production rather than chasing the largest possible tonnage estimate.

Interview with Mark Major, CEO of Krakatoa Resources

Phased Development Strategy: Managing Risk and Capital

Krakatoa has structured a three-phase development path designed to generate cash flow early while de-risking subsequent expansion. Phase 1 targets lump ore antimony production, selling direct shipping ore into the market. Because the project sits on an existing mining license, permitting focuses on activation rather than new approvals, which Major characterises as "a straightforward process." Environmental impact assessments and mitigation requirements remain proportional to the smaller initial footprint.

Phase 2 introduces mechanised mining and processing facilities to produce antimony concentrate alongside gold concentrate. This stage requires more substantial permitting for tailings facilities and processing infrastructure. Krakatoa Resources brought in Owen Mihalop, an underground mining engineer with 11 years' experience at Cornish Metals taking a narrow-vein tin mine from abandonment to production with mining widths of 2.5 to 3 meters - comparable to Zopkhito's vein geometry.

Phase 3 addresses the full gold upside, though Major acknowledges this remains less defined than the earlier phases.

Offtake and Market Positioning

The antimony market presents both opportunities and challenges for Krakatoa. Europe has designated antimony as a critical mineral, but downstream processing capacity remains limited. Major is evaluating options across Turkey, the UAE, the US, and potentially China, though Chinese offtake would undermine the European critical minerals narrative.

The company recently engaged a strategic consultant specializing in sales and trading to navigate these complexities. Major acknowledges a "chicken and egg" dynamic: offtakers want proof of economic production before committing, while proving economics requires understanding offtake terms. He expects clarity on placement in early 2027, following completion of the JORC resource.

Small-scale operations in Morocco and Turkey provide precedent for the lump ore strategy, though Major emphasises the need for Krakatoa to demonstrate extraction capability and economics before partners will fully engage.

Regional Context and Financing Considerations

Georgia's position bordering Russia raises questions about western capital accessibility, particularly given current geopolitical tensions. Major counters that significant European and US investment continues flowing into Georgian energy, infrastructure, and real estate. He draws a parallel: if investors are comfortable buying apartments in Georgia, they should be comfortable with mining investment.

European development banks have identified Georgia as a priority jurisdiction, and Major sees alignment opportunities once the project reaches appropriate technical and economic milestones. The phased approach serves partly to avoid massive upfront capital deployment in a jurisdiction where permitting timelines for large-scale projects could extend a decade or more. Major notes:

"It's not a market where you can sort of go and build the biggest project overnight. We could spend 10 years doing bankable feasibility studies over the full project only to be waiting another 10 years to get it permitted, if we don't do small bits at the start."

2026 Milestones: Moving the Needle

Major identifies several deliverables that will drive revaluation. The JORC resource classification provides recognition and confidence, moving the project from conceptual to defined. Metallurgical studies and mining viability work will feed into an economic assessment at year-end, likely at preliminary assessment or pre-feasibility study level. Underground development and continued drilling will further validate the model.

Critically, Major emphasises this is not a single-event catalyst story:

"It's not just one single event, ultimately it's the series of those events which will really dictate where we end up at the end of the day."

The Investment Thesis for Krakatoa Resources

- Extreme valuation dislocation: Trading at $170/ton antimony resource versus peer average of $750-$1,500/ton despite comparable or superior grade quality

- High-grade antimony (11.6%) in a critical minerals supply-constrained market where European buyers have designated antimony for strategic stockpiling but lack domestic production

- Dual commodity optionality with significant gold upside: 800,000+ ounce conservative gold resource provides downside protection and upside leverage beyond antimony-only peers

- Existing infrastructure and mining license reduce permitting risk: Soviet-era adits provide underground access, project sits on active mining license requiring activation permits rather than greenfield approvals

- Capital-efficient underground drilling strategy eliminates need to drill thousands of meters of waste rock, accelerating JORC timeline while managing exploration expenditure

- Proven narrow-vein mining expertise with Owen's hire from Cornish metals, bringing 11 years of experience in similar geology and mining widths (2.5-3m mechanised operations)

- Phased development de-risks capital deployment: Lump ore production (Phase 1) generates early cash flow before committing to processing infrastructure, avoiding binary execution risk

- Multiple near-term catalysts through 2026: JORC resource, metallurgical results, viability studies, economic assessment, and offtake clarity all expected within 12 months

- 20,000 historical sample points validated by recent drilling provide extensive geological database, reducing exploration risk and supporting rapid resource definition

- Geographic positioning in European critical minerals supply chain addresses strategic antimony shortage while maintaining access to development bank financing for Georgia-based projects

Macro Thematic Analysis

The antimony market exemplifies the West's critical minerals vulnerability. China controls approximately 60% of global antimony production and has recently implemented export restrictions, triggering supply concerns across defense, energy storage, and semiconductor applications. European nations have designated antimony as strategically critical, yet lack domestic production capacity or downstream processing infrastructure. This creates demand for regional suppliers like Krakatoa's Georgian project that can deliver into European supply chains without Chinese dependencies. The phased lump ore approach addresses immediate European antimony needs while the company develops processing capabilities. As Major notes:

"Europe's a bit unique. [Antimony is a] metal that Europeans need. They've earmarked it on the list, but the problem is that they don't have the ability to process it."

TL;DR: Executive Summary

Krakatoa Resources trades at an 80-90% discount to antimony peers ($170/ton vs. $750-$1,500/ton) despite high-grade mineralisation (11.6% antimony), 800,000+ ounces of gold upside, and existing mining infrastructure that reduces permitting and development risk. The company's phased approach prioritises rapid lump ore production to generate early cash flow while validating economics before committing major capital to processing facilities, with JORC resource and economic assessment expected by year-end 2026. Multiple near-term catalysts and the critical minerals supply shortage position the company for significant revaluation as it transitions from exploration to development.

FAQs (AI Generated)

Grade is the key differentiator—11.6% antimony versus peers at 1% grade with larger tonnages. Additionally, Krakatoa has significant gold upside (800,000+ ounces) that pure antimony plays lack, plus existing underground access reducing development costs.

: Phased development de-risks capital deployment, generates early cash flow from lump ore, and avoids decade-long permitting timelines for large operations in Georgia. It allows the company to prove economics before major infrastructure investment.

Limited European downstream processing capacity creates uncertainty around offtake terms. The company must first demonstrate economic extraction capability before partners will commit. China offers processing but undermines the European critical minerals narrative.

Drilling from inside existing kilometer-long tunnels eliminates thousands of meters of surface drilling through waste rock to reach 5-meter-thick veins. This accelerates resource definition, reduces drilling costs, and enables bulk sampling for JORC compliance.

JORC-compliant resource completion, metallurgical study results, mining viability assessment, preliminary or pre-feasibility economic assessment, offtake agreement clarity, and continued drilling results validating grade continuity and gold content.

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

.jpg)

Stay Informed