Tariff Shock & Dollar Strength Undermine Nickel Viability, Forcing Global Supply Recalibration

US tariffs & dollar strength force nickel supply recalibration. 50%+ production unprofitable. Institutional capital shifts to secure jurisdictions like Canada

- United States tariffs on imported nickel and a stronger dollar environment are intensifying price pressure, pushing nickel below key cost thresholds

- Over 50% of global nickel supply is now unprofitable, accelerating closures and exposing jurisdictional risk in dominant producers like Indonesia

- Despite oversupply, China's strategic Class 1 stockpiling indicates long-term conviction in nickel's role in electrification and energy transition

- The market is shifting toward ESG-compliant, jurisdictionally secure nickel sources, with Canada emerging as a standout destination

- Projects like Canada Nickel's Crawford offer rare, scalable sulphide resources positioned to meet Class 1 demand under stricter environmental and trade constraints

Macroeconomic Shocks Reshape the Nickel Landscape

The nickel market has entered a phase of forced recalibration, driven by macroeconomic headwinds that extend far beyond traditional supply-demand fundamentals. The August 1 implementation of United States tariffs on metal imports from 150+ countries, including top nickel exporters Indonesia and Russia, has injected a wave of uncertainty across the sector, fundamentally altering cost structures and trade flows.

Simultaneously, the United States dollar has strengthened in response to persistent inflation and shifting Federal Reserve expectations, applying additional downward pressure on nickel, which is priced in USD. The dollar's appreciation makes nickel more expensive for buyers in local currencies, dampening global demand and creating a compounding effect on already stressed markets.

These dual pressures have created what analysts describe as a "macro-induced compression" that extends beyond cyclical market dynamics. The result has been immediate and severe: nickel futures have dipped below US$15,000 per tonne, with London Metal Exchange spot prices around US$14,932 as of August 21, levels that threaten the economic viability of over half of global production.

Trade Disruption & Investment Implications

The tariff implementation specifically targets high-volume exporters, creating immediate disruption in established trade relationships. Indonesia, which accounts for approximately 35% of global nickel production, faces particular pressure as United States importers seek alternative sources or absorb higher costs. This shift is compounding existing concerns about Indonesia's production sustainability and environmental compliance.

For institutional investors, these macroeconomic shifts represent more than temporary market volatility. They signal a structural repricing of geopolitical and jurisdictional risk that is likely to persist as trade tensions escalate and currency volatility remains elevated. The compression in nickel prices is now reverberating through supply chains and cost curves, forcing a fundamental reassessment of project economics across the sector.

The implications extend to capital allocation decisions, where institutional mandates increasingly favor projects that can demonstrate resilience to trade disruptions and currency volatility. This macro-induced stress test is separating operationally robust projects from those dependent on favorable external conditions, creating clear winners and losers in the investment landscape.

Global Production Rationalisation Underway

Weak spot pricing is triggering a painful but necessary market correction that is exposing fundamental weaknesses in the global nickel supply base. According to Q3 2025 data, 32% of global nickel production is currently offline, representing the most significant production curtailment in over a decade. This rationalisation is particularly acute in Indonesia, where producers face mounting losses yet continue to operate due to government subsidies and policy inertia.

The ongoing oversupply, with a 198,000 metric ton surplus forecast for 2025, reflects a disconnect between supply momentum and real-time demand signals. Elevated London Metal Exchange inventories further underscore this imbalance, with stockpiles reaching levels not seen since the 2008 financial crisis. The divergence is especially pronounced in demand from sluggish stainless steel and electric vehicle sectors, which together account for over 75% of global nickel consumption.

Producers with higher-cost pyrometallurgical operations are facing severe margin compression, with all-in sustaining costs (AISC) for many operations now exceeding current spot prices by 15-25%. This cost pressure is particularly evident in laterite operations, where energy-intensive processing requirements make operations vulnerable to both commodity price weakness and rising energy costs.

Indonesian Supply Management Challenges

The market correction is prompting analysts to forecast a potential rebalancing by 2027-2028, contingent on unsustainable output being fully rationalized. However, this timeline assumes rational economic behavior from producers, which has not always been evident in markets where state intervention and strategic considerations override pure economics.

Indonesian production specifically faces scrutiny as government efforts to maintain output levels conflict with economic reality. Despite announced quota reductions of 120-150 million tonnes, most smelters remain online, supported by state financing that masks underlying unprofitability. This disconnect between announced policy and operational reality is creating skepticism among analysts about the timeline for meaningful supply curtailment.

The rationalisation process is also revealing structural inefficiencies in the global nickel supply chain, where geographic concentration in Indonesia has created vulnerabilities to both operational disruptions and policy changes. As these inefficiencies become apparent, institutional capital is beginning to rotate toward more diversified and operationally robust supply sources.

China Bets on Long-Term Strategic Value

Despite near-term market softness, major consumers like China are demonstrating conviction in nickel's long-term strategic importance. China has doubled its Class 1 nickel reserves since late 2024, underscoring the metal's critical role in electric vehicle batteries and the broader energy transition. This state-led accumulation suggests Beijing views current prices as a strategic buying window, reinforcing the perspective that current market pessimism is cyclical rather than structural.

The Chinese stockpiling strategy reflects sophisticated market analysis that looks beyond current price volatility to fundamental demand drivers. Electric vehicle production in China is expected to grow 25-30% annually through 2030, requiring substantial increases in high-grade nickel sulphate for battery cathodes. Similarly, grid-scale energy storage deployment is accelerating, creating additional demand for nickel-rich battery chemistries.

Chinese state-owned enterprises are also increasing direct investment in overseas nickel projects, particularly those that can deliver Class 1 material with reliable supply chain security. This investment strategy indicates recognition that current market conditions represent a window for acquiring strategic assets at attractive valuations.

Strategic Accumulation & Investment Implications

For institutional investors, this signals a fundamental divergence between short-term price action and long-term demand conviction. The Chinese accumulation strategy provides validation for the investment thesis that current market conditions create opportunities for selective accumulation of high-quality assets positioned to benefit from structural demand growth.

The strategic nature of Chinese accumulation also highlights the geopolitical dimensions of nickel supply security. As trade tensions escalate and supply chain resilience becomes a policy priority, countries and companies with secure access to high-grade nickel resources are likely to command premium valuations.

This dynamic is particularly relevant for North American projects, which offer both supply chain security and alignment with domestic content requirements under legislation like the United States Inflation Reduction Act. The combination of Chinese strategic buying and Western supply chain security concerns is creating a two-tier market where jurisdictionally secure projects command significant premiums.

Policy & Jurisdiction Are Redefining Supply Chain Value

As geopolitical risk intensifies, the market is systematically repricing jurisdictional security and Environmental, Social, and Governance (ESG) compliance. Tariff regimes and export restrictions are making it increasingly difficult for manufacturers to rely on single-origin, high-volume suppliers, particularly those concentrated in politically sensitive regions like Indonesia and Russia.

Indonesia's efforts to manage production through quota systems have been met with market skepticism. Despite announced reductions of 120-150 million tonnes, London Metal Exchange inventories remained at elevated levels in August 2025, having climbed significantly over the preceding months, and most smelters remain operational. This credibility gap between policy announcements and operational reality is undermining confidence in Indonesian supply management and highlighting the risks of over-reliance on state-controlled production.

Meanwhile, North America is emerging as a preferred supply base, offering advantages that extend beyond jurisdictional security to include ESG compliance and processing capability. Projects capable of delivering Class 1 nickel from sulphide deposits under net-zero or carbon-negative frameworks are drawing institutional attention from investors with specific mandates around sustainability and supply chain transparency.

Regulatory Support for Domestic Processing

The policy landscape is also shifting to favor domestic processing capabilities. The United States Inflation Reduction Act includes provisions that effectively require battery manufacturers to source materials from domestic or allied nation suppliers to qualify for tax incentives. This creates structural demand for North American nickel processing capacity, which has been limited despite substantial resource endowments.

Canadian federal and provincial governments have responded with targeted support for critical minerals projects, including refundable tax credits, infrastructure funding, and expedited permitting processes. Ontario specifically has designated certain nickel projects as provincial priorities, providing regulatory clarity and development support that contrasts sharply with the uncertainty facing projects in other jurisdictions.

The European Union is implementing similar policies through the Critical Raw Materials Act, which establishes strategic autonomy targets for critical minerals sourcing. These policies create effective market segmentation, where projects in allied jurisdictions with strong ESG credentials can command premium pricing and secure long-term offtake agreements.

Case Study: Canada Nickel & the Strategic Shift to Sulphide Supply

The shift away from high-risk, carbon-intensive sources is highlighting rare opportunities in Tier-1 jurisdictions. Canada Nickel's Crawford project in Ontario exemplifies this trend, offering a combination of scale, ESG alignment, and jurisdictional security that positions it uniquely in the evolving market landscape.

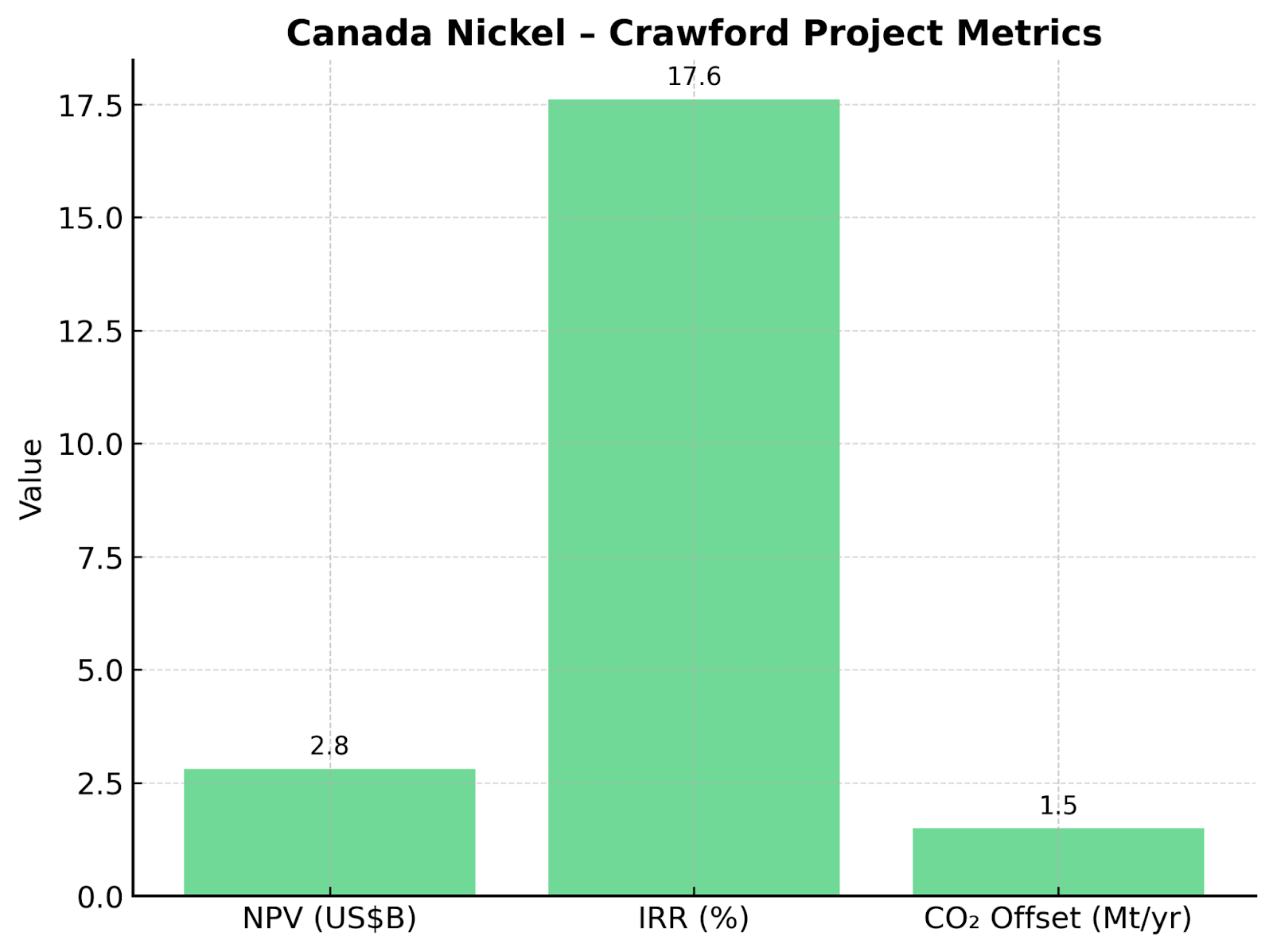

The Crawford project presents compelling economics with a Feasibility Study Net Present Value of US$2.8 billion (8% discount rate) and an Internal Rate of Return of 17.6%. These metrics demonstrate robust project economics even under current depressed pricing, suggesting significant upside potential as markets rebalance. The proprietary In-Process Tailings (IPT) Carbonation process positions Crawford as a carbon-negative operation capable of sequestering 1.5 million tonnes of CO₂ annually.

Strategic Capital & Government Support

This scale advantage is already attracting strategic capital from major industry participants including Samsung SDI, Agnico Eagle, and Anglo American. The project is also backed by C$1 billion in indicative government financing, demonstrating unprecedented public sector support for critical minerals development.

Crawford addresses critical supply chain gaps through its integrated approach to processing and production. The company's NetZero Metals subsidiary plans to establish North America's largest Class 1 nickel processing facility, offering domestic downstream capacity previously absent in the United States and Canada. This vertical integration strategy reduces supply chain risk while capturing higher-margin processing revenues.

Chief Executive Officer of Canada Nickel Mark Selby highlights the execution momentum:

"We're on track to get that federal permit before the end of the year, which would be just over six years from the fifth drill hole to getting that main permit in place, and then be in production well before the end of the decade, 2027-2028."

Infrastructure & Operational Advantages

The project's development timeline represents a significant acceleration compared to traditional mining project schedules. With federal permits expected by Fall 2025 and production targeted for 2027-2028, Canada Nickel is fast-tracking development in an industry typically characterized by decades-long timelines.

The Crawford project also benefits from exceptional infrastructure advantages, including proximity to established mining communities, existing electrical grid connections, and transportation networks. These factors contribute to what management describes as a "low-cost, highly productive operation" with residential workforce capabilities that enhance both cost structure and operational stability.

This infrastructure positioning, combined with strong community support and established supplier networks, creates operational advantages that extend well beyond pure resource quality to encompass the full spectrum of development and production risk factors.

Capital Markets & Investor Positioning in a Rebalancing Market

The current nickel market environment offers contrarian entry points for institutional investors willing to look beyond near-term volatility toward structural rebalancing opportunities. As low-cost, ESG-aligned projects become increasingly scarce, companies that meet institutional mandates on jurisdiction, ESG compliance, and offtake readiness are likely to command valuation premiums as markets recover.

Equity markets may remain subdued in the short term as macro headwinds persist and production rationalization continues. However, forward-looking capital is already rotating into permitted, funded, and strategically located projects that demonstrate resilience to current market pressures. Nickel equities with strong Internal Rate of Return and Net Present Value metrics, combined with demonstrated ESG pathways, are emerging as future-proof supply solutions.

The market is witnessing a clear bifurcation between projects dependent on favorable external conditions and those with structural advantages. Projects in secure jurisdictions with strong Environmental, Social, and Governance credentials, established infrastructure, and government support are maintaining access to capital markets while others face increasing financing constraints.

Strategic Asset Value & Financing Access

This capital reallocation reflects broader institutional mandates that prioritize supply chain security and sustainability compliance over pure cost optimization. The result is emerging premium valuations for projects that can demonstrate alignment with these evolving investment criteria.

Mark Selby notes the strategic positioning advantage:

"For investors, having something that is nine separate resources in a district is the kind of scale that a BHP or Rio Tinto, once they decide they want to get into nickel at some point in the future, is exactly the kind of asset that those very large companies are looking for."

The financing landscape for qualified projects remains robust despite broader market challenges. Export Development Canada and other government agencies are providing substantial debt financing for strategic projects, while private institutional capital seeks exposure to permitted, de-risked development opportunities.

The Investment Thesis for Nickel in a Reshaped Market

- Macroeconomic pressure is cleansing the supply base, forcing unsustainable producers offline and creating space for more efficient operations with superior cost structures and operational resilience.

- Tariffs and trade frictions are elevating jurisdictional risk premiums, redirecting institutional capital toward secure, low-risk regions like Canada and Australia that offer regulatory stability and permitting transparency.

- The United States Inflation Reduction Act is accelerating battery manufacturing and Class 1 nickel demand within protected supply zones, creating structural demand for domestically processed materials.

- Long-term demand from electric vehicles and grid storage remains intact despite near-term stainless steel weakness, with projected growth rates of 15-20% annually through 2030.

- Companies like Canada Nickel are positioned for revaluation, offering district-scale resources, ESG compliance, and government support in Tier-1 jurisdictions with established infrastructure and community acceptance.

- Development timelines aligned with multi-year demand growth trends position qualified projects to capture market share as supply rationalization creates capacity constraints by 2027-2028.

- Strategic partnerships with technology companies and government backing provide both offtake security and capital access advantages that enhance project execution capabilities and reduce financing risk.

Repricing Risk, Rebuilding Supply Chains

The current nickel downturn reflects a broader repricing of geopolitical, ESG, and macroeconomic risk that extends well beyond traditional commodity cycle dynamics. Yet amid this volatility lies opportunity for investors willing to navigate the macro overhang and position ahead of a long-anticipated market rebalancing.

Projects that combine operational scale, ESG integrity, and jurisdictional safety, exemplified by Canada Nickel's Crawford development, offer rare alignment with the future structure of global nickel demand. In this recalibrated landscape, strategic capital is not fleeing nickel exposure but rather refining its focus toward assets that can demonstrate resilience to trade disruptions, regulatory changes, and environmental compliance requirements.

The market transformation underway suggests that successful nickel investments will increasingly be differentiated by jurisdictional security, operational efficiency, and ESG compliance rather than pure cost leadership. This shift creates sustainable competitive advantages for projects positioned in stable regulatory environments with strong government support and community acceptance.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed