Trump's Copper Tariff Threats Trigger Historic Pricing Dislocation: Strategic Implications for Miners & Investors

Trump's 50% copper tariff creates record pricing dislocation, driving capital to Tier-1 mining jurisdictions. Strategic implications for copper investors.

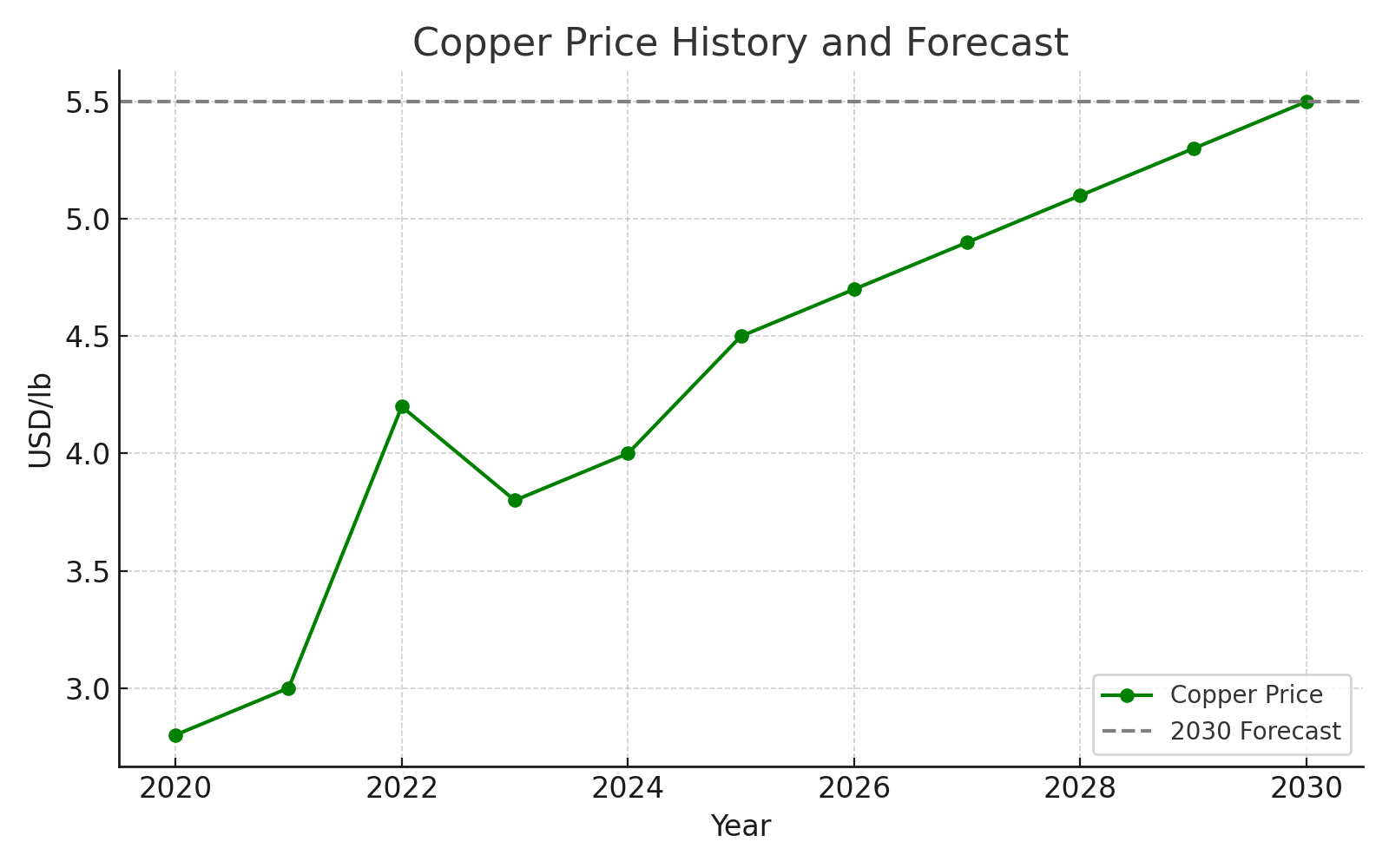

- On 8 July 2025, President Trump announced plans for a 50% tariff on imported copper, sending Comex prices to an all-time high and creating a record 25% domestic premium over LME benchmarks.

- The US relies on imports for 36% of its copper demand, with Chile, Canada, and Mexico as key suppliers, Chile facing the greatest exposure.

- A policy-induced supply squeeze could accelerate capital flows toward Tier-1 jurisdictions and well-advanced development projects, particularly those positioned to feed US or allied markets.

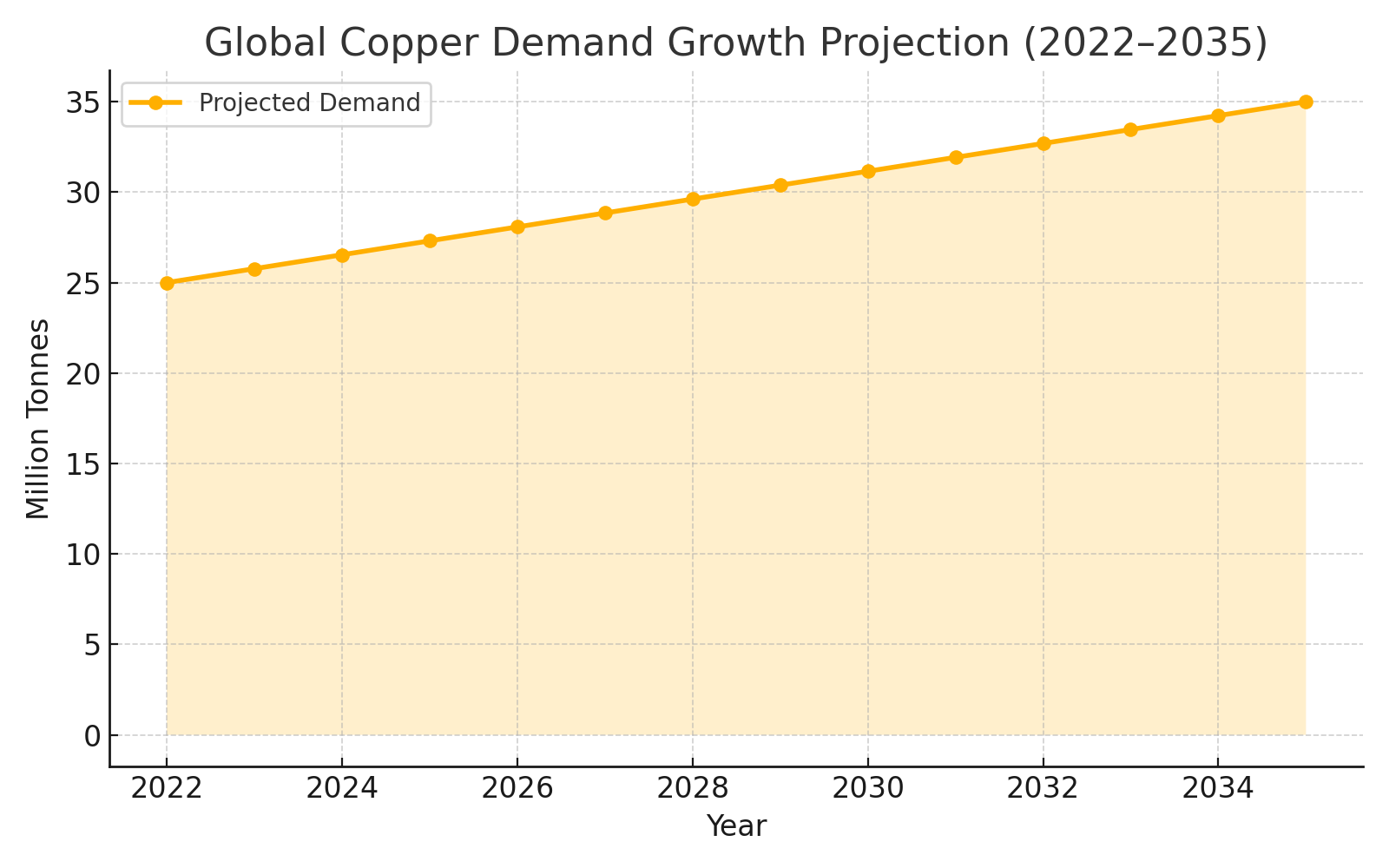

- Medium-term copper demand remains structurally underpinned by electrification, renewable infrastructure, and EV adoption, with a projected 40% increase by 2035.

- Investors may find opportunity in companies with low-cost, high-grade projects in politically stable jurisdictions, particularly those advancing toward near-term production.

Policy Shocks in the Copper Market

President Trump's July 8 announcement of a 50% copper tariff, framed as a Section 232 national security measure, sent immediate shockwaves through global commodity markets. The tariff, set for implementation by August 1, triggered unprecedented price volatility as traders scrambled to position ahead of the policy change. Comex copper futures surged to an intraday high of $5.8955 per pound, representing a 17% single-day gain that obliterated previous resistance levels.

The most striking development was the emergence of a record 25% premium of Comex futures over LME benchmarks, fundamentally disrupting the normal arbitrage mechanisms that typically keep global copper prices aligned. This pricing dislocation reflects not just immediate supply concerns, but a broader reconfiguration of how copper flows through international markets.

Market participants are treating this as more than a temporary trade dispute. The magnitude of the proposed tariff, at 50%, far exceeds the aluminum tariffs of 2018, signals a structural shift toward resource nationalism that could permanently alter copper trading patterns.

Pre-Tariff Front-Loading & Supply Chain Maneuvers

The announcement triggered an immediate rush among traders to accelerate copper shipments to US ports before the August 1 implementation date. Historical precedent from the 2018 aluminum tariffs suggests this front-loading behavior can create artificial scarcity in global markets while building substantial inventory positions in the targeted jurisdiction.

Maritime tracking data indicates a notable increase in copper-carrying vessels redirecting toward US ports, with some traders chartering additional capacity to maximize pre-tariff deliveries. This behavior creates a feedback loop, higher prices incentivize more aggressive inventory building, which further reduces available supply and sustains elevated pricing.

The inventory build-up phase typically lasts several weeks, followed by a period of reduced imports as domestic stockpiles are drawn down. However, the 50% tariff rate is substantial enough that it may permanently alter import economics, forcing US consumers to either accept higher costs or seek alternative supply sources.

Electrification & Decarbonization as Baseline Demand Support

While tariff-induced price volatility captures immediate market attention, the underlying copper demand trajectory remains firmly anchored to long-term electrification trends. The International Energy Agency (IEA) and Wood Mackenzie project global copper demand will increase by approximately 40% through 2035, driven primarily by renewable energy infrastructure, electric vehicle adoption, and grid modernization requirements.

Electric vehicles require approximately four times the copper content of internal combustion vehicles, while offshore wind installations demand significantly more copper per megawatt than traditional power generation. Data centers, whose power requirements continue expanding with artificial intelligence applications, represent another substantial and growing copper consumption category.

The tariff announcement, rather than dampening these structural trends, may accelerate domestic copper-intensive infrastructure development as policymakers seek to reduce import dependency. The Infrastructure Investment and Jobs Act already allocated substantial funding for grid modernization and EV charging networks, projects that will proceed regardless of copper pricing volatility.

Critical Metal Classification & Geopolitical Leverage

Copper's designation under the European Union's Critical Raw Materials Act reflects broader recognition that base metals have become tools of geopolitical leverage. The US tariff aligns with similar resource nationalism policies across multiple jurisdictions, from Indonesia's nickel processing requirements to Chile's lithium partnerships with preferred nations.

This fragmentation of previously globalized commodity markets creates both opportunities and risks for mining companies. Projects in politically aligned jurisdictions may benefit from preferential access and pricing, while those in contested regions face increased uncertainty about long-term market access.

The risk of retaliatory measures adds another layer of complexity. Chile, which supplies approximately 25% of global copper production, has already signaled concerns about the tariff's impact on bilateral trade relations. Codelco, Chile's state-owned copper giant, has indicated it will monitor developments closely and may seek alternative markets if US access becomes economically unviable.

The Case for Politically Stable, Infrastructure-Ready Assets

The tariff announcement has accelerated institutional investor rotation toward mining assets in jurisdictions offering both political stability and infrastructure advantages. Canada, in particular, has emerged as a preferred destination given its membership in the United States-Mexico-Canada Agreement and the established mining regulatory framework.

Gladiator Metals' Whitehorse Copper Project exemplifies the type of asset gaining increased investor attention. Located in Yukon Territory, the project benefits from established highway access, proximity to skilled labor markets, and year-round operational capability. Chief Executive Officer Jason Bontempo positions the company's strategic advantages:

"We have excellent highway and road access and trail access. Excellent draw on labor resource and being so close to the city and we can pretty much work all year round"

The 35-kilometer copper belt has been underexplored for decades, with Gladiator representing the first dedicated technical team and funding commitment in 40 years. The company targets over 100 million tons at above 1% copper grades, with initial focus on the Cowley Park prospect where historical drilling by Hudson Bay Mining suggests potential for 15-20 million tons at 1.5% copper from surface.

Canada's regulatory environment offers additional advantages through established Indigenous consultation processes and environmental assessment frameworks. Gladiator has already secured a Capacity Funding Agreement with the Kwanlin Dün First Nation, demonstrating proactive community engagement that reduces permitting risk.

Europe's Role in Copper Supply Security

Pan Global Resources' Spanish operations represent another strategic positioning in the evolving copper landscape. The company's focus on the Iberian Pyrite Belt and new Cármenes Project in northern Spain provides direct access to European decarbonization markets while avoiding the geopolitical complexities of other copper-producing regions.

Spain's membership in the European Union ensures regulatory alignment with critical materials legislation and renewable energy mandates. The country's established mining history and infrastructure reduce development risk compared to greenfield jurisdictions.

Tim Moody, speaking for Pan Global Resources, emphasizes the untapped potential of their Spanish assets:

"All three holes have hit gold which wasn't known before, wasn't extracted before, but over quite wide intervals, the first hole hit 46 meters of 1.1 grams gold"

The Cármenes discovery includes high-grade zones with channel sampling results of 37 meters at 3 grams per ton of gold that remain undrilled, representing substantial near-term exploration catalyst potential. The combination of copper and gold mineralization provides commodity diversification that enhances project economics across different market conditions.

Cost Structures & Operational Readiness Under Policy Pressure

In an environment of policy-driven price volatility, mining companies with robust cost structures and capital-efficient development pathways hold significant advantages. All-in sustaining costs (AISC) and capital intensity metrics have gained greater prominence as investors seek projects capable of generating positive returns across various price scenarios.

Marimaca Copper's MOD project in Chile demonstrates how operational design can create resilience against both price volatility and regulatory changes. The company's focus on heap leaching processes that are 38% less carbon-intensive than traditional methods while utilizing recycled seawater supply addresses both cost efficiency and environmental considerations.

Chief Executive Officer Hayden Locke highlights the project's strategic positioning:

"Marimaca has the potential to be a low capital intensity, high margin, copper company with heap leaching processes that are 38% less carbon intensive than traditional processing while utilizing recycled seawater supply that avoids fresh water consumption"

The company is nearing completion of its Definitive Feasibility Study, with 86% of total resource tonnes now classified in measured and indicated categories. This advanced technical status positions MOD to capitalize on copper price strength while maintaining operational flexibility if market conditions change.

Marimaca's recent drilling at the Pampa Medina sulphide area has revealed exceptional high-grade intersections, including 6 meters at 12% copper and broader intersections of 42 meters at 1.2% copper with significant molybdenum and gold credits. The potential for an underground mining operation at Pampa Medina could benefit from infrastructure sharing with the MOD heap leaching facility.

Permitting Timelines & First-Mover Advantage

Projects approaching Definitive Feasibility Study completion or resource declaration milestones can capitalize on copper price strength more rapidly than early-stage exploration assets. The current market environment rewards companies with clear pathways to near-term production decisions and established relationships with regulatory authorities.

Fitzroy Minerals' diversified Chilean portfolio demonstrates how active drilling programs can generate continuous news flow and maintain investor engagement during volatile market periods. The company's market capitalization of $37 million provides leverage to copper price movements while maintaining exposure to gold, molybdenum, and rhenium through its IOCG (Iron Oxide Copper Gold) systems.

Chief Executive Officer Merlin Johnson emphasizes the strategic timing of current market conditions:

"The perfect time to explore and discover and industry is competing to own good assets"

Fitzroy's Caballos project has delivered proof-of-concept results including 200 meters of mineralization at 0.46% copper with elevated molybdenum grades of 591 parts per million, well above established porphyry benchmarks. The discovery of a new mineralizing system with high molybdenum grades and gold correlation provides multiple value drivers in a single project.

Equity Market Response & Capital Allocation Trends

The copper tariff announcement triggered immediate outperformance among TSX Venture Exchange and Australian Securities Exchange-listed copper equities, with many companies recording double-digit gains in the days following Trump's announcement. This equity market response reflects both direct leverage to copper pricing and recognition that policy-driven supply constraints could benefit domestic and allied production sources.

Private placement activity has increased substantially, with advanced-stage copper projects receiving renewed institutional attention. Investors are particularly focused on assets in Tier-1 jurisdictions with established infrastructure and clear pathways to production. The premium being placed on political and regulatory certainty has created distinct valuation tiers based on jurisdictional risk assessments.

Resource-based financing has become more accessible for companies with established mineral inventories and technical studies. Banks and resource-focused investment funds are showing increased appetite for development-stage copper projects, particularly those with low capital intensity and favorable cost structures.

M&A as a Strategic Response

The tariff announcement has accelerated merger and acquisition discussions as larger producers seek to secure pipeline projects in preferred jurisdictions. The combination of elevated copper prices and supply chain uncertainty has increased the strategic value of development-ready assets with favorable operational characteristics.

Joint venture structures have emerged as a preferred mechanism for risk sharing and capital efficiency. US and allied smelters are particularly interested in securing long-term supply agreements that bypass potential tariff barriers while providing mining companies with off-take certainty and development financing.

The focus on jurisdictional arbitrage has created premium valuations for assets in Canada, Australia, and select South American jurisdictions with established mining codes and infrastructure. Companies with multiple projects across different jurisdictions are positioning themselves as diversified suppliers capable of serving various regional markets.

Potential Retaliation & Diplomatic Friction

Chile's measured response to the tariff announcement reflects the complex balance between copper export revenues and broader diplomatic relations. Codelco has indicated it will continue evaluating market conditions and may redirect sales to alternative destinations if US market access becomes economically unviable.

The risk extends beyond immediate trade flows to long-term investment decisions. Chilean copper projects with extended development timelines may face increased uncertainty about future market access, potentially affecting project financing and partnership arrangements.

Other copper-producing nations are monitoring the situation closely, with some expressing concern about the precedent set by unilateral trade restrictions on strategic materials. The potential for coordinated responses or alternative trading arrangements could further fragment global copper markets.

Price Cooling Scenarios

Morgan Stanley analysts have suggested that copper prices may normalize following the initial tariff implementation as market participants adjust to new trading patterns. The sustainability of current price premiums depends largely on whether domestic US supply can increase rapidly enough to offset reduced imports.

Companies that scale operations too aggressively based on short-term pricing may face margin pressure if tariff-induced premiums erode over time. The key strategic consideration is maintaining operational flexibility while capitalizing on current price strength.

Historical analysis of previous trade disputes suggests that initial price spikes often moderate as supply chains adapt and alternative sources develop. However, the scale of the proposed copper tariff and its classification as a national security measure suggest this may represent a more permanent shift in trade patterns.

The Investment Thesis for Copper

- Structural demand tailwinds from electrification, decarbonization initiatives, and data center expansion provide fundamental support that outlasts short-term policy volatility.

- Companies operating in Tier-1 jurisdictions with established infrastructure and transparent permitting regimes offer superior risk-adjusted returns in an environment of increased geopolitical uncertainty.

- Near-term operational catalysts including Definitive Feasibility Studies, mineral resource estimates, and drilling results provide multiple opportunities for value realization in volatile markets.

- Low all-in sustaining costs and capital-efficient development pathways improve project economics across various copper price scenarios while reducing financing risk.

- Assets with multi-commodity exposure and operational scalability offer resilience against shifting trade policies and commodity price cycles.

- Strategic optionality through exploration upside, expansion potential, or merger and acquisition possibilities provides additional value drivers beyond base-case production scenarios.

- Balance sheet strength and established management teams reduce execution risk during periods of elevated market volatility and increased investor scrutiny.

- Established community relationships and environmental compliance reduce regulatory risk and support sustainable long-term operations.

The Trump administration's 50% copper tariff represents more than a temporary trade policy adjustment, it signals a fundamental shift toward resource nationalism that will reshape global copper markets for years to come. While short-term price volatility creates both opportunities and risks for mining companies and their investors, the underlying structural demand for copper remains firmly anchored to irreversible electrification trends.

The most significant investment opportunities lie with companies that combine favorable jurisdictional positioning, robust operational metrics, and clear pathways to near-term production. Political stability, infrastructure access, and regulatory transparency have emerged as crucial competitive advantages in a fragmented global marketplace.

The copper market's evolution toward regional trading blocs and strategic partnerships reflects broader geopolitical realignments that extend far beyond commodity markets. Investors who position themselves with companies offering the right combination of operational excellence, jurisdictional advantages, and strategic flexibility will be best positioned to benefit from copper's essential role in the global energy transition.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed