Tier-1 Gold Asset is Undervalued versus Peers, with Multiple Near-Term Catalysts to Drive Re-Rating

Banyan Gold holds ~7.6Moz at AurMac, trades at $43/oz vs peers, with a Q2 resource update, maiden PEA, and Franco-Nevada royalty deal signalling deep undervaluation.

- Banyan Gold's AurMac project in Yukon hosts approximately 7.6 million ounces of gold resources and only trades at roughly US$43 per resource ounce serves a significant discount to Yukon peers and to the valuation implied by Franco-Nevada's recent US$52.2 million royalty acquisition on the property.

- A Victoria Gold receivership overhang which had suppressed Banyan's share price through 2024-2025 has been fully resolved following a court order confirming 100% clear title and the complete divestment of Victoria Gold's 8.6% equity position.

- Banyan's 2026 programme includes a 40,000-metre drill campaign on the AurMac deposit and 10,000 metres on regional targets, with results expected from May, a Q2 resource update, and a maiden Preliminary Economic Assessment targeted for the second half of the year.

- AurMac benefits from year-round road access and grid-connected hydroelectric power — infrastructure advantages that management argues meaningfully reduce both capital costs and permitting timelines relative to greenfield Yukon projects, but which remain underreflected in the company's current market valuation.

- A bonanza-grade silver discovery on the property is being followed up in 2026, with management identifying potential for early cash flow through direct shipping ore or toll milling at the adjacent Hecla mill, which currently has capacity.

With gold trading above $4,400/oz, junior developers with large, advanced-stage deposits are attracting renewed investor attention. Banyan Gold (TSXV:BYN) sits in a specific subset of that universe: companies with resource bases approaching or exceeding the threshold scale of roughly eight to ten million ounces that major gold producers typically seek for transformational acquisitions. Yet the company's current market valuation, at approximately $43 per resource ounce, sits well below the range commanded by several Yukon peers and far below historical acquisition benchmarks set at comparable gold prices.

President & CEO, Tara Christie made a structured case for why that discount exists, why she believes it is closing, and what milestones investors should monitor through the remainder of 2026.

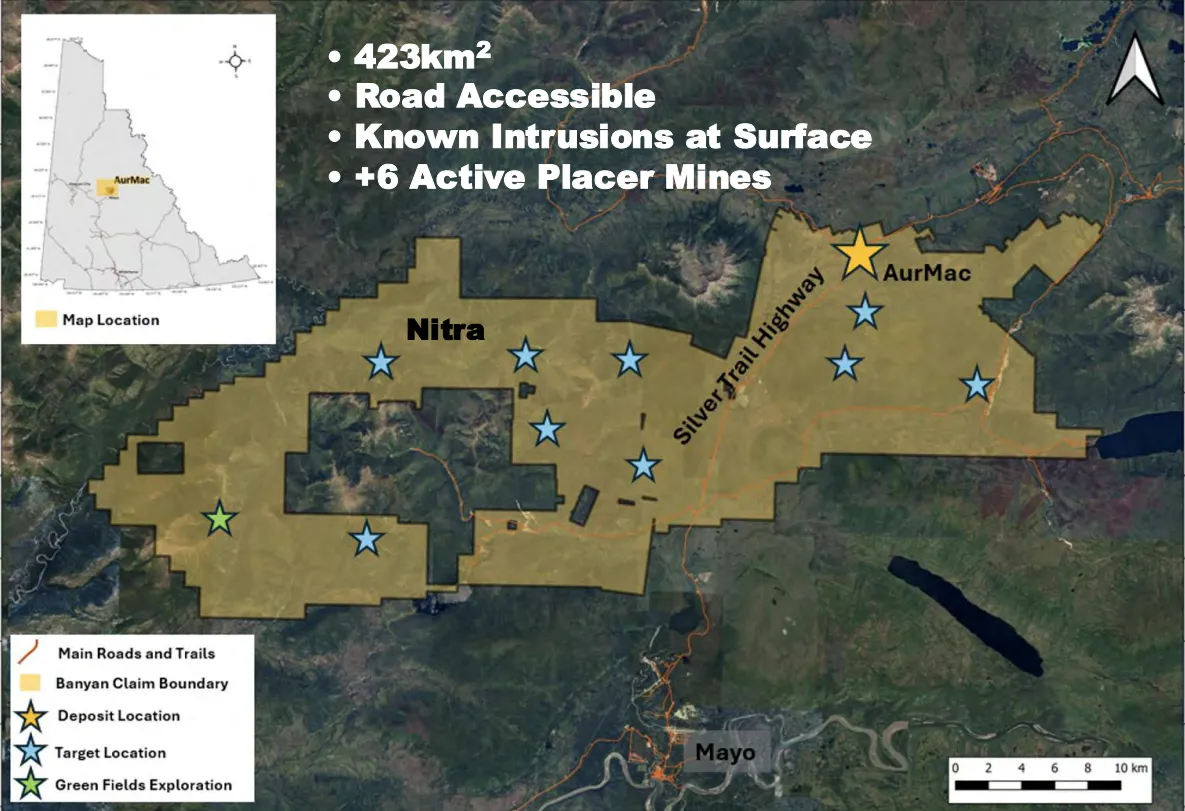

AurMac Scale, Grade and Infrastructure

AurMac, located in Yukon's Mayo Mining District, currently hosts 2.2 million ounces of indicated resources and 5.4 million ounces of inferred resources calculated using a $2,050/oz gold price assumption. Since the resource was published, the company has drilled approximately 43,000 metres focused specifically on improving the economics of the deposit in preparation for its forthcoming PEA. Christie expects the updated resource due in Q2 2026.

The deposit is open at depth and in multiple directions, with drilling to 650 metres returning high-grade intersections and geochemical signatures that Christie says may indicate proximity to an intrusive heat source. The company believes the deposit has the scale to support production in excess of 300,000 ounces of gold per year over a mine life of 20 to 30 years which are characteristics that place it in rare company among undeveloped gold deposits globally.

"Our project has a huge infrastructure advantage and that's been severely discounted in the market," Christie said. "Not only is that a lower capital and operating cost for us, but it means that our permitting timeline is much faster because we don't have to build roads into pristine areas."

Beyond resource size, AurMac's infrastructure position distinguishes it from many Yukon peers. Year-round road access crosses the property, and grid-connected hydroelectric power removes two of the most capital-intensive and permitting-sensitive requirements for northern development projects.

Interview with Tara Christie, President & CEO of Banyan Gold Corp.

The Valuation Gap: How It Formed

Banyan's current per-ounce market valuation sits at a material discount to Yukon peers such as Snowline Gold, which was trading near $260/oz prior to broader sector pressure from geopolitical uncertainty. Christie attributes this gap to three overlapping factors:

- Victoria Gold held a 25% interest in the AurMac property alongside an 8.6% equity position in Banyan. The uncertainty created by that situation, combined with forced selling pressure from the receivership process, effectively suppressed Banyan's share price through 2024 and into early 2025. By late September 2025, Banyan had secured a court order confirming 100% clear title to the property. Shortly after, the receiver fully divested the equity position. Christie acknowledges that clearing an overhang of that nature takes time to register fully with the market.

- The second factor is a jurisdiction perception discount that affected Yukon explorers more broadly, tied to concerns about permitting timelines and infrastructure investment. Christie argues that the new Yukon government's business-oriented posture and its stated commitments to power and road infrastructure have materially improved the regulatory outlook yet that the market has been slow to reprice that shift.

- The third factor is what Christie terms a grade perception problem. AurMac has historically been characterised as a low-grade bulk-tonnage deposit, and that framing has proved difficult to shift despite drilling that demonstrates a substantial high-grade core. The company's 2025 drill program of 43,000 metres was specifically designed to define the geometry and continuity of the plus-one-gram material, information that will be incorporated into the PEA pit designs.

Franco-Nevada Royalty Acquisition

One of the clearest external signals of AurMac's embedded value came from Franco-Nevada's decision to acquire the underlying royalty on the property for $52.2 million. The royalty structure involved a 6% gross royalty that can be reduced to a 1% NSR for a $10 million buydown payment. Christie's analysis is that the practical value Franco-Nevada acquired, stripping out the likely buydown, implies a $42 million price for a 1% NSR on the project.

"They think that our royalty is going to pay them back probably in an order of magnitude from what they've paid," Christie said. "It's a pretty great signal for us."

The argument is straightforward: if a royalty company of Franco-Nevada's calibre is willing to pay $52.2 million for a royalty interest based on current resource size and gold price, the implied project valuation does not appear to be reflected in Banyan's current market capitalisation.

2026 Catalysts & Drill Program

Banyan entered 2026 with five drills active at AurMac and approximately 7,000 metres completed, with a 40,000-metre program underway on the main deposit. An additional 10,000 metres is allocated to ten regional exploration targets across the broader property, along with the company's bonanza-grade silver discovery, which Christie flagged as a potential source of near-term cash flow through high-grade direct shipping ore or toll milling at the adjacent Victoria Gold mill, which is currently for sale.

Drill results are expected to begin flowing starting May 2026. Key milestones for the year include the Q2 resource update, maiden PEA results in the second half, and possible clarity on the Victoria Gold mill and mine assets which Christie views as a potential benchmark-setting event for AurMac's own valuation.

The company recently added Patrick Langford to its corporate development team, bringing experience from the Probe and Angus Gold transactions, to support strategic positioning as the asset matures toward development decisions.

THE INVESTMENT THESIS FOR BANYAN GOLD

- Tier one scale at a junior price. At approximately $43 per resource ounce, AurMac's ~7.6 million-ounce resource base is valued at a fraction of what peers trade at and well below historical M&A acquisition prices at comparable gold prices.

- Defined catalysts with near-term timing. A Q2 2026 resource update and H2 2026 maiden PEA provide two discrete re-rating events within the current calendar year, with drill results expected from May onward.

- Overhang fully resolved. The Victoria Gold property interest and equity overhang causing Banyan's share price underperformance through 2024 is now completely cleared, removing the technical selling pressure that suppressed the stock.

- Infrastructure advantage is real and underprice. Year-round road access and grid hydroelectric power reduce both capital requirements and permitting timelines relative to greenfield Yukon developments; this advantage is not reflected in current per-ounce valuations.

- Franco-Nevada's royalty acquisition provides a credible external valuation reference. A $52.2 million royalty purchase by a blue-chip royalty company implies a project valuation materially above Banyan's current market capitalisation.

- Silver optionality adds upside not in current consensus. A bonanza-grade silver discovery is being drilled in 2026 with potential for standalone economic development or early cash flow generation.

- Jurisdiction risk has improved. The new Yukon government's stated commitment to permitting reform and infrastructure investment reduces a discount that has weighed on the sector broadly.

- Management has meaningful skin in the game. Christie holds a 3.5% stake purchased in the open market for over C$2.8 million, aligning management incentives directly with shareholders.

- M&A optionality is credible at this scale. Deposits above eight million ounces capable of sustaining 300,000-ounce-per-year production are rare; at current gold prices, major producers are generating cash at a rate that supports transformational acquisitions.

Gold Price, Junior Valuations and the M&A Cycle

Gold maintaining above $4,000/oz represents a structural shift in the economics of gold mining, not simply a cyclical price event. At these levels, major and mid-tier producers are generating free cash flow at historically elevated rates, rebuilding balance sheets that were constrained during lower-price periods and rebuilding reserve bases that have been drawn down through years of underinvestment in exploration.

The scarcity factor compounds this dynamic. Deposits above eight million ounces capable of supporting 300,000-plus ounce annual production are genuinely rare. The pipeline of projects at that scale that are not already controlled by a major or mid-tier producer is short. Junior developers that occupy that space, particularly those with infrastructure advantages and in jurisdictions accessible to international capital, represent a structurally limited supply of potential acquisition targets.

As Banyan Gold's President & CEO Tara Christie puts it:

"This is a generational scale opportunity. Whenever you have a deposit this large, that's the generational asset big companies are looking for."

Retail and institutional investors in the junior sector are increasingly recognising that the gap between resource-stage valuations and what producers are willing to pay in acquisitions is wide. Companies that can demonstrate credible economics through PEAs and feasibility studies tend to see the most pronounced re-ratings. The current environment, with gold prices providing a historically favourable backdrop, makes that repricing cycle more likely to accelerate.

TL;DR

Banyan Gold holds a ~7.6 million-ounce gold resource in Yukon that management argues is deeply undervalued at US$43 per ounce. Victoria Gold receivership overhang affecting both property title and share register of Banyan Gold has been fully resolved. Franco-Nevada paid $52.2 million for a royalty on the project, implying a valuation that Banyan's market cap does not currently reflect. Five drills are turning in 2026, with a resource update due Q2, maiden PEA in H2, and silver discovery drilling also underway. The setup is catalyst-rich heading into the second half of the year.

Frequently Asked Questions (FAQs) AI-Generated

Banyan's share price was materially suppressed through 2024 and into early 2025 by the Victoria Gold receivership, which created both title uncertainty over 25% of the AurMac property and forced selling from Victoria's 8.6% equity position in Banyan. That situation has now been fully resolved through a court order and the complete divestment of the equity position. The market has been slow to reprice the resolution, which management argues is the primary source of the current valuation gap.

Franco-Nevada paid $52.2 million to acquire a royalty on AurMac that carries a 6% gross rate, buyable down to 1% NSR for $10 million. Stripping out the likely buydown scenario, management's analysis implies Franco-Nevada effectively paid $42 million for a 1% NSR. The argument is that a sophisticated royalty company of that calibre, deploying capital at that scale into a single junior project, reflects a project valuation that is not captured in Banyan's current market capitalisation.

There are four primary milestones: drill results from the active 50,000-metre program beginning approximately May 2026; a Q2 resource update that is expected to grow both indicated and inferred ounces; a maiden PEA in the second half of 2026 that will provide the first published economic benchmark for AurMac; and potential clarity on the adjacent Victoria Gold mill and mine assets, which Christie views as a valuation reference point for AurMac itself.

AurMac has year-round road access across the property and is connected to the Yukon's grid hydroelectric network via power lines that pass the Mayo hydro dam. For a northern development project, these two factors — road and power — are typically among the largest capital cost line items and the most complex permitting challenges. Having them already in place materially reduces both upfront capital requirements and the permitting timeline, advantages that management argues are not currently reflected in the company's per-ounce market valuation relative to peers that lack equivalent infrastructure.

AurMac has historically been framed as a low-grade, bulk-tonnage deposit, a characterisation that tends to attract lower per-ounce valuations in the market. Banyan's 43,000-metre 2025 drill program was specifically designed to define the extent and geometry of a high-grade core within the deposit — material grading above one gram per tonne that the company believes represents a substantial portion of the overall resource. The maiden PEA, which will incorporate this drilling into pit designs, is expected to quantify the economic contribution of that high-grade component for the first time.

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed