US Copper Import Tariff Takes Effect Causing Shock, Arbitrage Opportunities, & Disruption

US 50% copper import tariff creates 30% domestic premium, $1.37/lb arbitrage spread. Mining stocks in Canada, Chile benefit from supply chain shifts.

- A US copper import tariff is set to fundamentally alter global copper trade, leading to unprecedented arbitrage opportunities and localized supply shortages.

- This tariff is accelerating deglobalization in base metals, creating distinct markets based on tariff exposure and stimulating domestic production.

- Exploration companies in top-tier jurisdictions with imminent production potential, such as Gladiator Metals and Marimaca Copper, are well-positioned to gain from revalued US copper markets and increasing investor caution.

- Supply constraints, widening regional price discrepancies, and strategic inventory accumulation by traders present both long-term growth and immediate event-driven risks.

- Copper's strategic importance is growing due to its critical role in electrification, infrastructure, and national security, driving greater investment into select copper equities.

Structural Trends & Natural Resource Markets

Deglobalization & Strategic Commodity Policy

The August 1 implementation of the 50% US copper import tariff represents more than trade policy, it signals a fundamental realignment in how critical materials are valued within national security frameworks. Copper now joins steel and aluminum as a Section 232-targeted commodity, elevating its status from industrial input to strategic resource. This policy shift has already generated a 30% domestic premium over LME copper, creating the largest sustained arbitrage spread in base metals history.

The tariff's immediate impact extends beyond price discovery to supply chain architecture. Traditional trade routes from Chile and Peru face new economic barriers, while domestic producers and proximate suppliers gain competitive advantages. As Jason Bontempo, CEO & Director of Gladiator Metals observes:

"Yukon's Tier-1 status gives the company leverage in a fragmented copper market."

This highlights how jurisdictional positioning has become a primary valuation driver in the new policy environment.

Market bifurcation is accelerating as US traders pivot toward strategic inventory accumulation, anticipating sustained price differentials. This dynamic mirrors earlier commodity nationalism trends but operates at unprecedented scale given copper's centrality to electrification infrastructure.

Energy Transition as a Secular Demand Engine

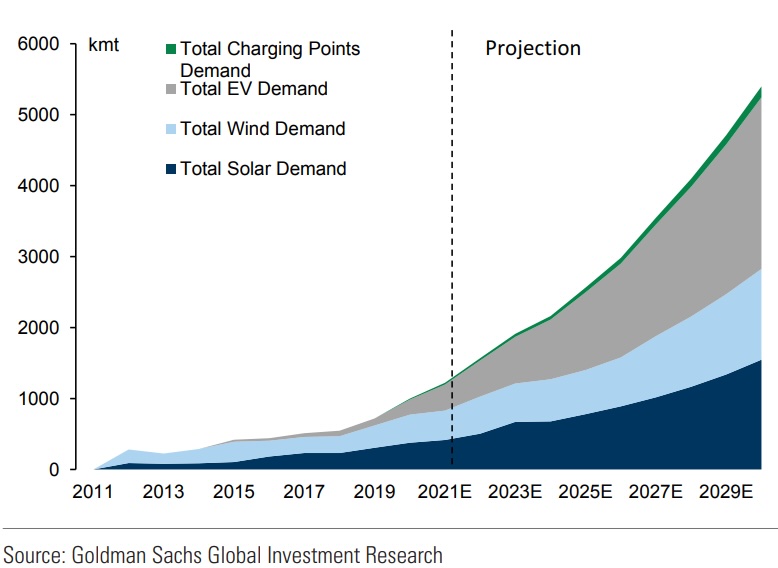

The International Energy Agency and CRU project a 40% increase in copper demand by 2035, driven primarily by electric vehicle adoption, renewable energy deployment, and grid modernization. This secular growth trajectory intersects with the tariff regime to create compound pressure on domestic supply chains.

High-conductivity applications demand lower impurity profiles, favoring oxide deposits with reduced deleterious elements. Marimaca Copper's project design exemplifies this trend as Chief Executive Officer Hayden Locke notes:

“The company's focus is on "high acid soluble" mineralization that delivers better recoveries than at Marimaca through our integrated processing approach”

The technical superiority of low-impurity copper becomes magnified in tariff-protected markets where substitution options diminish.

Infrastructure bottlenecks compound these dynamics as grid reinforcement projects accelerate under federal electrification mandates. The convergence of policy support, technical requirements, and supply constraints creates multiple expansion vectors for strategically positioned copper assets.

Systemic Risk & Asset Repricing Across Cycles

Copper as a Risk Asset Amid Monetary & Fiscal Tightening

Copper's evolution from industrial commodity to macro proxy intensifies under tariff conditions. Currency dislocations amplify pricing volatility as FX-adjusted arbitrage opportunities emerge between regional markets. The Federal Reserve's monetary stance intersects with trade policy to create complex hedging requirements for industrial consumers and financial speculators alike.

Dollar strength historically pressures copper pricing through purchasing power dynamics, but tariff-induced domestic premiums partially insulate US markets from currency effects. This decoupling creates new correlation patterns that institutional portfolios must navigate, particularly for funds with global commodity exposure.

Arbitrage Opportunities & Market Dislocation

Current arbitrage dynamics reveal the magnitude of policy-induced distortion: COMEX copper trades at $5.87/lb versus LME at approximately $4.50/lb. This $1.37 spread represents the largest sustained differential in base metals markets, creating immediate profit opportunities for traders with inventory capacity and financing access.

Physical flow disruption extends beyond pricing to logistics infrastructure. Traditional shipping routes face new economic barriers while inland transportation networks strain under redirected volumes. These bottlenecks particularly impact companies developing in non-tariff jurisdictions, as Gladiator Metals' northern Canadian assets benefit from proximity to US markets without tariff exposure.

Strategic inventory accumulation by major trading houses suggests market participants expect sustained price differentials rather than temporary dislocations. This behavior indicates structural rather than cyclical market changes, supporting longer-term investment themes around domestic copper production.

Capital Formation & Strategic Deployment in Mining

Valuation Differentials Across Jurisdictions

Jurisdictional arbitrage emerges as a primary investment theme as Canadian and Chilean assets with stable permitting regimes command valuation premiums over projects in politically uncertain territories. Gladiator's proximity to Yukon's hydroelectric grid and Whitehorse infrastructure provides cost advantages that become more pronounced under tariff conditions.

Pan Global Resources exemplifies European positioning advantages, with Chief Executive Tim Moody explaining:

"European permitting clarity and regional copper relevance under the EU Green Deal creates value through regulatory predictability.”

The company's Iberian Pyrite Belt projects align with the EU's Critical Raw Materials Act, providing policy tailwinds that mirror US domestic preferences.

Geographic positioning extends beyond political stability to include infrastructure access, labor availability, and environmental permitting timelines. Projects near established mining centers benefit from shared services and technical expertise that reduce development risks and capital requirements.

Financial Health & Capital Access

Balance sheet strength becomes critical as project development timelines accelerate under policy pressure. Gladiator Metals maintains C$15 million in treasury alongside institutional backing from sophisticated resource investors including Aimco and Macquarie Bank. This capital position supports aggressive exploration programs while providing optionality during market volatility.

Marimaca Copper's US$14.9 million treasury, supported by Greenstone and Assore, enables the company to advance its definitive feasibility study while maintaining exploration flexibility at satellite projects. The company's integrated development strategy allows for production scaling from 50,000 to potentially 75,000 tons annually, positioning it among the ASX's largest copper projects by production capacity.

Fitzroy Minerals' C$5 million position, while smaller, supports focused programs on its low-cost heap leach profile. The company's by-product portfolio including molybdenum and rhenium aligns with critical minerals funding themes and provides revenue diversification.

Project Readiness in a Dynamic Market Environment

Permitting Timelines & Development Visibility

Tariff implementation creates urgency around domestic project advancement as supply chain security concerns override traditional cost optimization. Gladiator targets a maiden resource by Q1 2026 for its Cowley Park prospect while maintaining a 30,000-meter drill program across multiple targets. The company's systematic approach, with CEO & Director Jason Bontempo noting:

“We are targeting over 100 million tons at above 1% copper, not including any credits."

Marimaca's definitive feasibility study, due Q3 2024, advances permitting for a 70-75 thousand ton per annum operation positioned to capture peak copper pricing. The project's "simple, low strip ratio, open pit operation" design minimizes execution risk while maximizing capital efficiency.

Development timelines increasingly favor projects with established infrastructure access and regulatory clarity. Companies operating near existing mining districts benefit from proven permitting pathways and reduced community engagement complexity.

Exploration Momentum & Milestone Catalysts

Fitzroy Minerals and Pan Global maintain active drilling programs totaling over 19,000 meters across IOCG and VMS targets, providing near-term catalyst potential during heightened market attention. Pan Global's upcoming NI 43-101 for La Romana expected to establish the project's resource base within Spain's permitting-friendly corridor.

Technical programs focus increasingly on metallurgical characteristics as processing flexibility becomes crucial for supply chain optimization. Pan Global's quality advisor Alvaro Merino provides insight on La Romana's "metallurgical profile and recovery metrics aligning with EU offtake demand," highlighting how regional processing capabilities create additional value layers.

Thematic Exposure & Resource Allocation Strategies

How Institutional Capital is Repositioning in Copper

Institutional sentiment shifts toward viewing copper as a multi-cycle thematic investment comparable to uranium and lithium in strategic importance. Early-stage exposure to scalable exploration assets in policy-insulated geographies attracts capital seeking asymmetric upside with reduced geopolitical risk.

Investment flows prioritize projects with clear development pathways and technical advantages over pure exploration plays. The combination of resource scale, jurisdictional stability, and infrastructure access creates screening criteria that favor established players with proven management teams and institutional backing.

ESG, Carbon Metrics, & the Rise of "Green Copper"

Environmental performance differentiates projects as institutional mandates increasingly require carbon intensity metrics. Marimaca's recycled seawater utilization and heap leaching approach delivers 38% lower carbon intensity compared to traditional SX-EW processing, attracting ESG-focused capital allocation.

Fitzroy's by-product profile including molybdenum and rhenium aligns with critical minerals funding initiatives and circular economy narratives. As VP Exploration Sergio Rivera of Marimaca notes:

“The project's carbon intensity advantages of the metallurgical design create competitive positioning within institutional investment frameworks.”

Renewable energy integration becomes a project selection criterion as copper producers seek to minimize scope 2 emissions while maintaining cost competitiveness. Projects with access to hydroelectric or solar power gain valuation premiums reflecting both operational advantages and ESG compliance.

The Investment Thesis for Copper

- The convergence of tariff-induced supply fragmentation, secular electrification demand, and institutional capital reallocation creates multiple expansion vectors for strategically positioned copper assets. Key investment drivers include:

- Exposure to macroeconomic realignment via tariffs and supply chain fragmentation provides direct leverage to policy-driven price premiums. Jurisdictional positioning in Canada, Chile, and Spain offers permitting and regulatory stability while avoiding tariff exposure. Favorable cost structures including oxide leaching, low strip ratios, and renewable energy access enhance project economics under elevated price scenarios.

- Clear visibility on development catalysts including definitive feasibility studies, maiden resources, and expanded drilling campaigns creates near-term value inflection points. High asset scarcity value emerges as markets face multiyear structural deficits while new project development faces extended timelines. Strong balance sheets enhance exploration flexibility and provide capital discipline during market volatility.

- Carbon-smart development strategies align with institutional mandates while reducing operational risks. Companies positioned to absorb capital flows redirected from tariff-risk jurisdictions benefit from portfolio reallocation trends toward domestic supply security.

Strategic Metals, Strategic Positioning

The US copper tariff represents more than trade policy, it catalyzes fundamental sector realignment around supply chain security and strategic resource control. For investors, optimal positioning requires alignment with jurisdictionally insulated, technically advanced, and capital-strong copper plays.

Companies like Gladiator, Marimaca, Pan Global, and Fitzroy illustrate how asset quality, project readiness, and strategic geography define competitive advantage in the new policy environment. As demand surges and policy intervention accelerates, copper transitions from commodity to strategic asset class, and selective equities offer concentrated exposure to this structural transformation.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed