US Import Reliance Reaches 31% & Higher Capital Costs Constrain New Salt Supply

Higher financing costs are slowing new salt supply, making access to capital the key factor determining which projects advance.

- A policy-rate environment near 3.75% has increased the cost of capital, raising the hurdle rate that new mining projects must exceed to secure financing and reducing the number of projects that meet investors' return requirements.

- Salt is more sensitive to higher financing costs than most mined commodities because USGS 2026 data show domestic rock salt averages about US$54 per tonne while new mines still require hundreds of millions of dollars in upfront capital, making fewer projects financeable as hurdle rates rise.

- Higher financing costs favor projects with strong after-tax returns, access to capital, and advanced permitting, while weaker projects face dilution, delays, or cancellation.

- Higher financing costs favor projects with strong after-tax returns, access to capital, and advanced permitting, while weaker projects face dilution, delays, or cancellation.

- In a policy-rate environment near 3.75%, financing risk, not geology, is the primary constraint on new mine development and the key risk factor for new supply.

Fed Policy Rates & Higher Financing Hurdles Reprice Mine Development

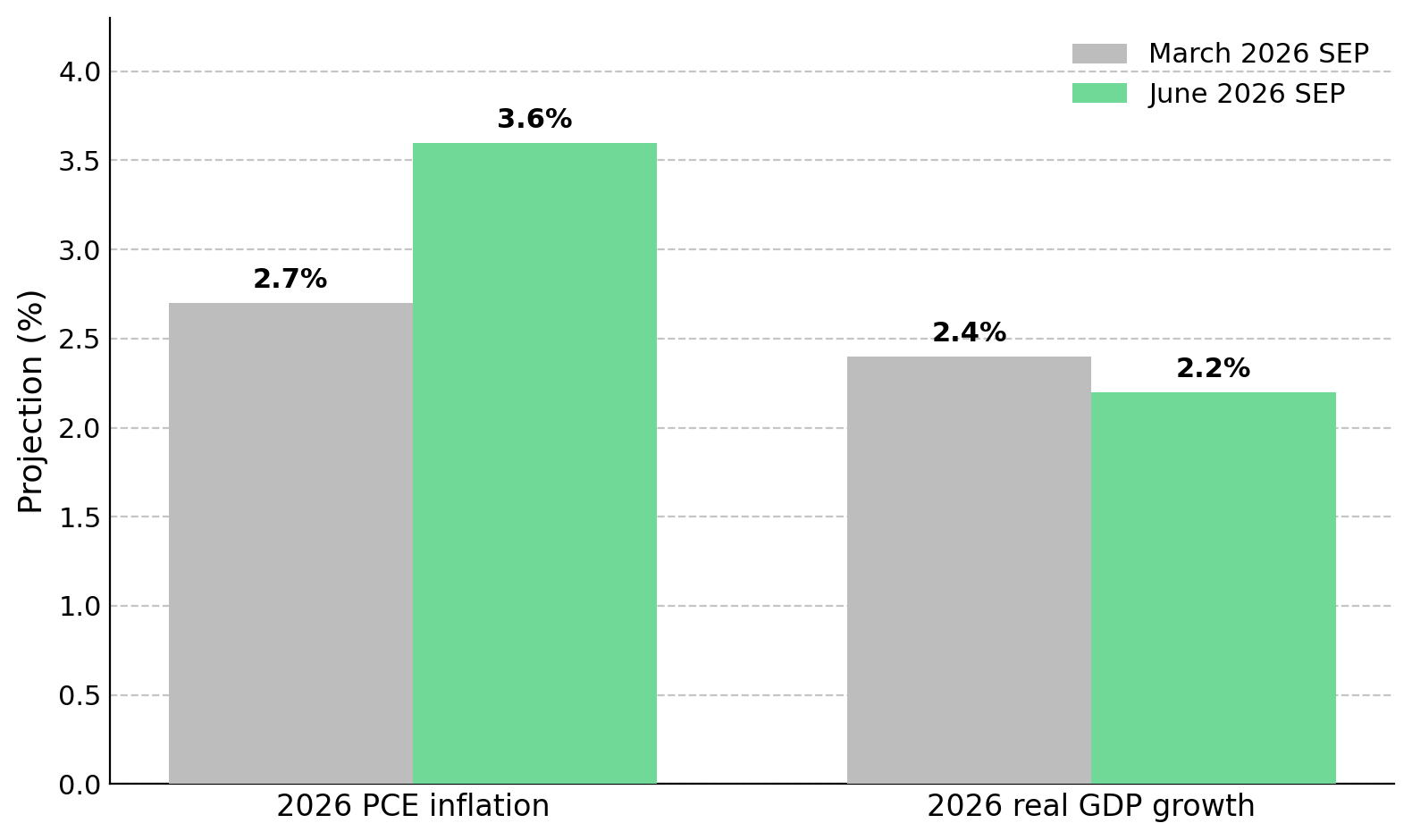

The key variable shaping new mine development in 2026 is the cost of capital. At its June 2026 meeting, the Fed held its policy rate at 3.50%-3.75%, while its Summary of Economic Projections raised the year-end inflation forecast to 3.6% and lowered expected economic growth to 2.2%, reinforcing expectations that borrowing costs will remain elevated. Following the meeting, interest-rate markets increased the probability of an additional rate hike, raising the prospect of higher financing costs for capital-intensive projects.

The policy rate influences the cost of capital, increasing the return that lenders and equity investors require before funding a project. Higher rates reduce the present value of future cash flows and raise the hurdle rate projects must exceed to secure financing.

A higher discount rate reduces net present value because future cash flows are worth less when discounted at a higher rate. Higher interest rates increase borrowing costs and reduce the pool of capital available for new mine development. Because mines require large upfront investment and generate cash flow over decades, changes in the cost of capital can re-rate an entire development pipeline without any change in the underlying orebody.

Rising Mine-Build Costs & New Salt Supply Becomes Harder to Finance

Since 2021, inflation in steel, labor, engineering, and mining equipment costs has increased the upfront capital required to build new mines. Higher financing costs and rising construction budgets reduce project returns simultaneously, making fewer development projects attractive to lenders and equity investors.

Because salt generates less revenue per tonne than most metals, investors focus on capital-efficiency metrics such as initial capex, internal rate of return, and capital intensity. The USGS 2026 Mineral Commodity Summaries estimate the average value of domestic rock salt at about US$54 per tonne. With revenue per tonne limited and new underground mines requiring substantial upfront capital, financing hurdles are higher than for many higher-value metals. As a result, few companies are willing or able to commit the capital required to develop new salt mines.

Capital-Intensive Salt Supply & Barriers to New Mine Development

Atlas Salt serves as an example of how a development-stage project must meet increasingly demanding financing requirements. Its September 2025 feasibility study prepared by SLR Consulting models initial construction capital of approximately C$589 million, a design capacity of 4.0 million tonnes per year, and a mine life of 24.3 years. These figures are study projections rather than operating results.

A prior 2023 study reportedly estimated construction capital near C$480 million, compared with C$589 million in the September 2025 feasibility study, consistent with higher mine-development costs. The increase aligns with broader inflation in construction, labor, and equipment costs, which has raised the capital required to develop new mines.

Atlas Salt Chief Executive Officer Nolan Peterson believes the scarcity of capital willing to fund new salt projects strengthens the project's position within the North American market:

"We aim to supply de-icing road salt to the North American market. We will be the first new salt mine built in North America in 25 years."

Higher Hurdle Rates & How Capital Selects New Supply

As the cost of capital rises, projects require a larger spread between their modeled internal rate of return and investors' required return to remain attractive. Projects with a large return spread can absorb higher discount rates, while projects with narrow margins can become uneconomic after even a modest increase in financing costs.

Investors test project valuations across multiple discount-rate assumptions because higher discount rates reduce the value of projects with long construction and ramp-up periods. Rather than relying on a single net present value estimate, they assess whether project returns remain attractive as financing costs rise.

Assessing Financing Risk Across Developers & Producers

Atlas Salt's September 2025 feasibility study models an after-tax internal rate of return of 21.3% and an after-tax net present value of approximately C$920 million at an 8% discount rate. Based on the feasibility study, the modeled return remains above the financing thresholds investors typically require for capital-intensive projects. The investment case still depends on securing the full construction-financing package required to fund the C$589 million initial capital cost. Because construction financing has not been secured, investors face financing and dilution risk, and the valuation remains tied to feasibility-study assumptions rather than operating cash flow.

Higher financing costs affect funded producers differently than development-stage projects. Because funded producers generate cash flow, investors typically value them on operating earnings rather than future development assumptions. When financing costs are high, the market assigns higher valuations to funded producers and lower valuations to unfinanced developers, widening the valuation gap between the two and making financing the key catalyst for projects such as the Great Atlantic Salt Project.

The Financing Shift from Banks to Strategic & Private Capital

Higher rates and tighter credit conditions have made traditional project-finance debt more expensive and less available for single-asset developers. As a result, developers increasingly rely on multiple funding sources to finance construction. Vendor finance, offtake agreements, and equity financings help reduce funding gaps and improve access to capital when bank lending becomes more restrictive.

A signed offtake agreement can reduce perceived revenue risk, improving access to debt financing and lowering borrowing costs. Vendor finance reduces the amount of equity a developer must raise, limiting shareholder dilution. Together, these financing tools can help projects secure funding when traditional project-finance debt is difficult to obtain.

In February 2026, Atlas Salt agreed with Sandvik Mining for approximately C$132 million of underground mining equipment, including a potential financing component that remains subject to Sandvik's approval. If approved, the financing component would reduce the amount of equity the company needs to raise, lowering potential dilution for existing shareholders.

The Capital Stack Supporting a Development-Stage Salt Project

In a policy-rate environment near 3.75%, permitting delays carry a higher financial cost. Every quarter of permitting delay extends the period before a project generates cash flow, prompting lenders and equity investors to demand higher returns to compensate for the additional uncertainty. As a result, permitting delays increase a project's cost of capital, making permitting progress a direct determinant of financeability.

Reducing project risk can improve financing terms and increase project value. Stable jurisdictions, advanced permitting, and government support can reduce the return investors require to finance a project. A completed feasibility study supported by a well-defined resource and reserve base can also improve lender and investor confidence. Together, these factors can lower a project's cost of capital and improve access to financing.

Government Support & Permitting Progress Lower Financing Risk at Great Atlantic

Atlas Salt's development-stage position benefits from concrete jurisdictional support. In February 2026 the Government of Newfoundland and Labrador approved the company's work plan, signed a community and employment agreement following a Cabinet-level vote, and confirmed that environmental requirements had been satisfied, with site preparation beginning the same month. Operating within the Canadian securities framework, including National Instrument 45-106 and full disclosure on SEDAR Plus, adds a layer of transparency that institutional buyers can audit.

Government support reduces financing risk but does not eliminate it. Cabinet-level support reduces the risk of political or community delays, which can improve access to construction financing and lower financing costs, but the project must still secure a complete funding package. Investors should distinguish between a lower financing risk premium and a fully funded mine.

The Financial Value of De-Risking

The cost of capital has become a primary determinant of whether capital-intensive projects advance across commodities, not just salt. When financing costs and construction budgets are high, some projects that would have secured funding in a lower-rate environment do not advance, increasing the value of assets that reach production. The result is slower supply growth across capital-intensive industries despite strong underlying demand.

Salt amplifies this dynamic because demand remains relatively insensitive to price changes and the United States Geological Survey reports that net import reliance reached roughly 31% of apparent consumption in 2025. When demand is non-discretionary and a significant share of supply is imported, constrained domestic supply can provide stronger price support during periods of elevated demand.

The Investment Thesis for Salt

- Financing risk, more than geology, is now the binding constraint on new supply in a policy-rate environment near 3.75 percent, so the cost of capital determines which projects are financeable.

- Funded producers typically command higher valuations than pre-financing developers because producing cash flow carries less financing risk than unfinanced development projects.

- Projects with modeled after-tax returns well above investors' required return are generally better positioned to secure financing, although feasibility-study returns are not guaranteed outcomes.

- Vendor finance, offtake agreements, and equity financing have become increasingly important as project-finance debt becomes harder to secure. For developers, a completed construction-financing package is often the key valuation catalyst.

- Stable jurisdictions, advanced permitting, and government support can reduce the return investors require to finance a project, improving access to capital and financing terms.

- The thesis would weaken if financing costs fell enough to make previously uneconomic projects financeable, if advanced developers failed to secure funding despite strong modeled returns, or if lower salt prices and higher operating costs reduced projected project returns.

A cut-off grade, the minimum ore grade that can be mined profitably, determines which material within a deposit is economic to extract. In 2026, the cost of capital serves a similar function by determining which projects can secure financing. The key screening test has shifted from the orebody to the balance sheet.

Elevated borrowing costs and construction inflation mean that access to capital, not resource scarcity alone, increasingly determines which salt projects advance. Projects with returns well above financing thresholds, access to non-dilutive funding, and advanced permitting are better positioned to secure financing. Investors should evaluate development-stage projects based on financing structure and the spread between modeled returns and financing requirements, rather than relying solely on headline net present value. A strong feasibility study does not guarantee a funded mine. Pre-financing developers carry financing and dilution risk, and securing a construction-financing package remains the key milestone that determines whether a project advances toward production.

TL;DR

Higher-for-longer interest rates and rising mine-construction costs have made financing the primary constraint on new salt supply. Because salt generates relatively low revenue per tonne but requires substantial upfront capital, fewer projects can meet investor return requirements as borrowing costs rise. This environment favors funded producers and advanced developers with strong project economics, permitting progress, and access to capital. Investors should focus less on resource size and more on financing structure, return margins, and funding pathways, as securing construction capital has become the key milestone separating projects that reach production from those that remain on the drawing board.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

.jpg)

%20(1).jpg)

Stay Informed