US Trade Policy Uncertainty & Supply Disruptions Push Copper Beyond $13,000

Copper breaks $13,000/t on U.S. tariff uncertainty and Chilean supply disruptions. Low inventories and constrained pipelines favor permitted development projects.

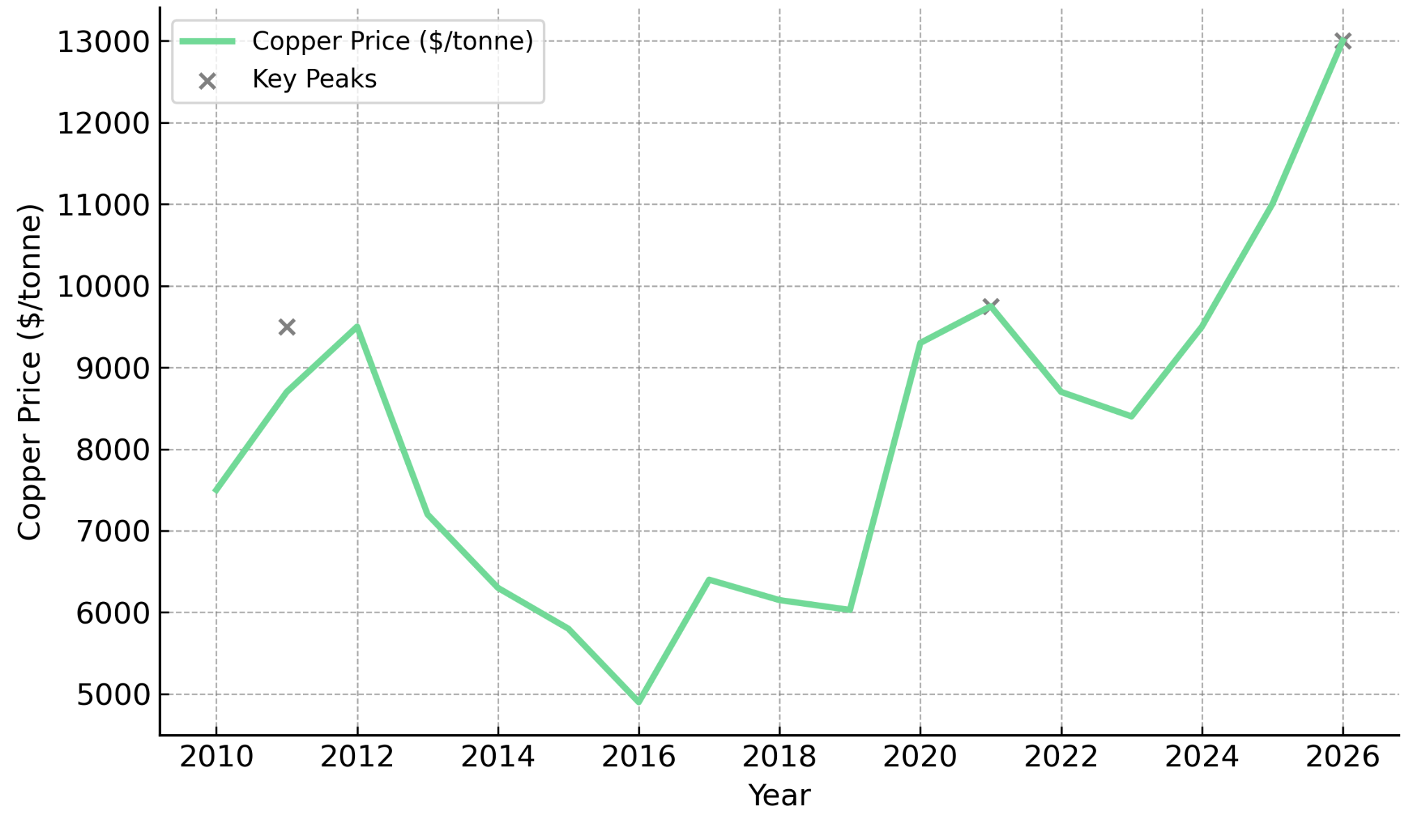

- Copper prices have broken through $13,000/t, marking a structural inflection driven by trade policy uncertainty rather than cyclical demand alone.

- Existing US tariffs on semi-finished copper and the prospect of additional duties on refined copper have triggered aggressive stockpiling, tightening availability across global markets.

- Chilean supply disruptions, including the ongoing Mantoverde mine strike, combined with low exchange inventories, have amplified price sensitivity to even marginal shocks.

- The rally is reinforcing the strategic value of low-cost, permitted copper projects and exposing fragilities in the global refining system.

- For investors, the focus is shifting from price participation to asset quality, execution certainty, and jurisdictional resilience.

Copper's Break Above $13,000: Structural Context for the Price Move

The copper market's breach of $13,000 per tonne in early January 2026 represents more than a nominal price record. Unlike previous peaks in 2011 or the post-COVID stimulus cycle of 2021, this rally is characterized by policy-driven supply constraints rather than demand-side acceleration. The distinction matters for how investors evaluate exposure across producers, developers, and explorers.

In prior cycles, copper rallies were typically supported by aggressive Chinese stimulus, inventory restocking, or coordinated infrastructure spending. Exchange inventories provided a buffer against supply disruptions, and the permitting pipeline, while slow, was not yet structurally impaired. Today, the conditions are fundamentally different. London Metal Exchange and Shanghai Futures Exchange inventories remain at low levels, permitting timelines have extended materially, and capital discipline among major miners has constrained new project sanctioning.

The current price environment reflects copper's evolving role as a strategic material rather than a purely industrial input. Electrification mandates, grid expansion requirements, and data center proliferation have reframed copper demand as structural and policy-supported. At the same time, supply-side constraints have intensified. The result is a market where price signals increasingly reflect scarcity and geopolitical risk rather than short-term demand fluctuations.

The implications for capital allocation are significant. Major producers have underinvested in greenfield development for over a decade, prioritizing shareholder returns and balance sheet repair over reserve replacement. According to industry estimates, the lead time from discovery to production for a major copper deposit now exceeds fifteen years on average, compared to seven to ten years in previous cycles. This structural lag means that supply responses to current price strength will not materialize until well into the next decade.

How Tariff Implementation Is Rewiring Global Copper Flows

US trade policy has materially altered global copper flows. In August 2025, the Trump administration imposed 50 percent Section 232 tariffs on semi-finished copper products and intensive copper derivatives, while exempting raw copper, concentrates, and cathodes. The tariff structure has triggered sustained arbitrage activity, with traders shipping refined copper to the US to capture the premium over LME prices.

A Commerce Department review due by June 30, 2026, will inform whether additional phased tariffs on refined copper, 15 percent starting in 2027 and 30 percent in 2028, will be implemented, maintaining uncertainty in the market. The forward-buying behavior has compressed spot availability in Europe and Asia while inflating US premiums.

This policy asymmetry introduces a new layer of complexity for project developers. Financing assumptions, offtake negotiations, and capital allocation decisions must now account for trade policy risk in ways that were previously unnecessary. Projects with geographic flexibility, multiple offtake pathways, or domestic market exposure are increasingly favored.

Development-stage operators are responding by accelerating execution timelines and prioritizing risk mitigation. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, describes the company’s operational focus in this environment:

"We're starting to turn our attention to the execution strategy right now and in fact we're in the planning phase of all of the key hires that we need to make in the short and medium term."

Chilean Disruptions & the Inventory Problem

Chile, which accounts for approximately 24 percent of global copper mine production based on 2024 data, has experienced a series of operational disruptions that have exposed the fragility of the current supply system. The ongoing strike at the Mantoverde mine, water constraints in the Atacama region, and grade declines at aging assets have collectively constrained output growth. The timing of these disruptions, against a backdrop of low exchange inventories, has amplified price sensitivity to marginal supply shocks.

The inventory situation is particularly acute. Combined LME and SHFE stocks remain at levels that provide minimal buffer against supply interruptions. In previous cycles, exchange inventories served as a shock absorber, allowing the market to weather temporary disruptions without significant price volatility. That buffer has largely been depleted.

Cost-curve dynamics further complicate the supply picture. Marginal production is increasingly sourced from higher-cost, lower-grade operations with extended permitting timelines. New greenfield projects face regulatory scrutiny, community engagement requirements, and capital costs that have escalated significantly over the past decade. The implication is that supply responses to elevated prices will be slower and more capital-intensive than in previous cycles. Projects with low all-in sustaining costs, high reserve confidence, and existing permits are positioned to benefit disproportionately from this structural imbalance.

What Higher Copper Prices Change for Mining Economics

Sustained copper prices above $13,000 per tonne materially alter project economics across the development pipeline. Net present values expand, internal rates of return increase, and payback periods compress, improving financing optionality for projects that can demonstrate execution certainty. The shift in economic assumptions is reordering capital allocation priorities across the sector.

At current prices, projects that were previously marginal become economically viable, while already robust projects generate significantly enhanced returns. The sensitivity is particularly pronounced for development-stage assets with defined resources, completed feasibility studies, and clear permitting pathways. For these projects, price strength translates directly into improved financing terms, expanded strategic optionality, and accelerated development timelines.

The market's emphasis has shifted from exploration optionality toward execution certainty. Investors are increasingly prioritizing projects with measured and indicated resources, low capital intensity, and infrastructure access over early-stage exploration with theoretical upside. Oxide projects utilizing heap leach processing, which typically feature lower capital requirements and faster construction timelines, have moved up the capital allocation queue.

Development-Stage Positioning in a Tight Copper Market

The structural conditions favoring development-stage assets are evident in how the market is valuing projects with near-term production visibility. Marimaca Copper illustrates the characteristics that have gained relevance: an oxide-focused project in Chile with definitive feasibility study economics published in August 2025, a life-of-mine strip ratio of 0.8:1, and environmental approval secured in November 2025. The project's heap leach configuration, proximity to the Port of Mejillones, secured recycled seawater supply, and access to certified renewable electricity offer capital efficiency and execution advantages that are increasingly scarce in the copper development pipeline.

For projects approaching construction decisions, the current price environment demands rigorous risk assessment. Capital cost discipline and operational de-risking have become prerequisites for financing conversations. Hayden Locke articulates the approach:

"I’m up on site about optimization. Finding the areas where we think we've overblown the capex, focusing on the area of risk, which risks we haven't identified properly and how do we mitigate those before we go into a build."

The emphasis on pre-construction risk identification reflects broader market expectations. Investors and lenders are differentiating between projects based on management credibility, capital cost confidence, and operational track records. In an environment where copper scarcity is structural, the ability to deliver new supply on time and on budget commands a significant premium.

Exploration-Stage Considerations: Discovery Leverage & Capital Efficiency

Exploration-stage companies face a different set of considerations in the current market. While elevated copper prices increase the strategic value of discovery, capital markets remain selective in funding early-stage exploration. The distinction between speculative drilling programs and capital-efficient exploration strategies has become more pronounced.

Fitzroy Minerals represents an approach that addresses this capital constraint through structured partnerships. The company's strategy involves leveraging oxide resources through joint venture arrangements to generate near-term cash flow while preserving exposure to larger sulphide targets. Fitzroy initiated a Preliminary Economic Assessment in December 2025 for its Buen Retiro Heap Leach joint venture with Pucobre S.A., the only primary copper producer listed on the Santiago Stock Exchange. Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, explains the rationale:

"We are working on terms with Pucobre to do a heap leach joint venture. That operation gives us the potential for near-term non-operated cash flow which we think will distinguish us from many other explorers in the market."

The model addresses a fundamental challenge for exploration companies: maintaining operational momentum and shareholder interest during extended discovery timelines. Cash-generating assets provide funding optionality and reduce dilution risk, while porphyry-style exploration targets offer scale potential that becomes increasingly valuable as supply constraints intensify.

The macro environment supports this strategic positioning. As Merlin Marr-Johnson notes regarding the broader market dynamics:

"Vast amounts of money going just to maintain production, metal prices have to rise as demand is strong... The coming crunch is actually driving value in existing companies."

Currency, Volatility & Capital Allocation Effects

Copper price strength transmits into commodity-linked currencies, particularly the Chilean peso and Australian dollar, creating secondary effects for project economics denominated in local currencies. For development-stage projects with peso-denominated operating costs and dollar-denominated revenues, currency appreciation can partially offset copper price gains at the margin level.

Volatility transmission between the underlying metal and copper equities has diverged in the current cycle. While copper prices have demonstrated relative stability at elevated levels, equity valuations have exhibited greater sensitivity to broader market risk-off events, financing conditions, and company-specific execution updates. The decoupling creates opportunities for investors who can distinguish between metal price exposure and equity-specific factors.

Portfolio construction in the copper sector requires balancing producers with predictable cash flows, developers with execution leverage, and explorers with discovery optionality. Each category exhibits different risk-return characteristics and responds differently to macro conditions. In the current environment, the risk-adjusted case for permitted development assets has strengthened relative to both producing majors, where valuation premiums are already embedded, and early-stage explorers, where capital access remains constrained.

The Investment Thesis for Copper

- Copper's price strength reflects structural supply constraints and policy-driven trade uncertainty rather than transient demand factors, suggesting durability in elevated price levels.

- Development-stage projects with completed feasibility studies, secured environmental approvals, and low all-in sustaining costs offer asymmetric leverage to sustained price strength with defined execution timelines.

- Exploration assets with scale potential and capital-efficient funding mechanisms gain strategic relevance as major producers seek to replace depleted reserves through acquisition.

- Jurisdictional stability and permitting transparency have become differentiating factors as regulatory timelines extend and community engagement requirements intensify globally.

- Low inventory levels and constrained supply pipelines reduce the market's ability to absorb disruptions, creating conditions where marginal supply additions command premium valuations.

- Projects with oxide resources and heap leach configurations offer capital efficiency and faster development timelines that align with market demand for near-term supply solutions.

- Elevated prices increase merger and acquisition optionality as major producers prioritize de-risked growth over greenfield development in an environment of capital discipline.

Copper's Price Signal Reflects System Constraints

Copper trading above $13,000 per tonne is not a speculative phenomenon but a reflection of structural system stress. The combination of implemented tariffs, pending policy decisions, low inventories, and constrained supply pipelines has created conditions where price signals increasingly reflect scarcity rather than cyclical demand.

Capital allocation is shifting toward assets that can realistically deliver new supply within this decade. Projects with execution certainty, jurisdictional resilience, and favorable cost structures are commanding premiums, while early-stage exploration requires differentiated capital strategies to compete for funding. The investment landscape favors those who can distinguish between price participation and asset quality in an environment where copper's strategic importance continues to expand.

TL;DR

Copper's breach of $13,000/t reflects structural constraints rather than cyclical demand. U.S. Section 232 tariffs on semi-finished copper products, pending policy reviews due June 2026, and Chilean supply disruptions including the Mantoverde mine strike have tightened global availability while exchange inventories remain critically low. The rally favors development-stage projects with completed feasibility studies, secured environmental approvals, and low capital intensity over early-stage exploration. Supply response timelines now exceed fifteen years from discovery to production, meaning meaningful new supply won't materialize until the 2030s. For investors, asset quality, execution certainty, and jurisdictional resilience have become more important than simple price exposure.

FAQs (AI-Generated)

The price surge is driven by U.S. trade policy uncertainty, specifically existing 50% tariffs on semi-finished copper and potential additional duties on refined copper, combined with Chilean supply disruptions and historically low exchange inventories.

Section 232 tariffs have triggered arbitrage activity, with traders shipping refined copper to the U.S. to capture premiums. This has compressed spot availability in Europe and Asia while inflating U.S. prices.

The lead time from discovery to production for major copper deposits now exceeds fifteen years on average, compared to seven to ten years in previous cycles, due to extended permitting timelines and regulatory requirements.

Development-stage projects with completed feasibility studies, secured permits, low all-in sustaining costs, and oxide resources using heap leach processing are favored for their capital efficiency and faster construction timelines.

A Commerce Department review due by June 30, 2026 will determine whether phased tariffs on refined copper—15% starting in 2027 and 30% in 2028—will be implemented.

Analyst's Notes

Subscribe to Our Channel

Stay Informed