ValOre Metals: Strategic Positioning in a Tightening Platinum Market Signals Major Investment Opportunity

ValOre's 2.2M oz PGE resource and Brazilian operational base position it to capitalize on structural platinum deficits projected through 2026 as supply remains constrained.

- The company holds a 2.2 million ounce platinum-palladium-gold resource as platinum markets transition from a projected 692,000 oz deficit in 2025 to near-balanced conditions in 2026, with structural tightness persisting due to constrained supply and limited inventory rebuilding.

- Leadership team has delivered CAD$1.7 billion in M&A transactions across five major discoveries, with direct experience bringing projects from exploration through to production and acquisition by major mining companies including Rio Tinto, Goldcorp, and Royal Gold.

- The 100%-owned Pedra Branca asset in Brazil's Ceará State benefits from established infrastructure, streamlined regulatory frameworks, and access to one of the world's fastest-growing mining talent pools—Brazil now graduates more mining engineers than the USA and Canada combined.

- Comprehensive metallurgical testwork completion expected Q4 2025, with Preliminary Economic Assessment targeted for Q4 2026, alongside an active M&A strategy targeting advanced-stage gold projects to accelerate production timelines.

- Platinum and palladium markets face structural supply deficits driven by historic underinvestment, with 2025 supply among the weakest in recent history while demand remains robust, creating sustained price support with platinum up 48% year-to-date and palladium advancing 25%.

Introduction: Platinum Market Dynamics Create Strategic Window

The platinum group metals sector stands at an inflection point. After years of underinvestment in new supply, the market faces a projected deficit of approximately 692,000 ounces in 2025, one of the most significant imbalances in recent history. While forecasts suggest a return to near-balanced conditions in 2026, this projection depends heavily on improved trade flows and normalized investment behavior. Critically, even under optimistic scenarios, above-ground stocks are not expected to rebuild, meaning structural tightness will persist.

For investors seeking exposure to this supply-constrained environment, ValOre Metals Corp. presents a compelling opportunity. The company's 2.2 million ounce resource at its 100%-owned Pedra Branca project positions it to benefit from sustained price support in platinum and palladium markets, while its experienced management team and strategic Brazilian operational base provide the execution capacity needed to advance the asset through critical development milestones.

The convergence of favorable market fundamentals, proven leadership, and near-term technical catalysts establishes a risk-reward profile that warrants serious consideration from mining-focused investment portfolios. The company's positioning in Brazil, a jurisdiction that is actively investing in its mining future, further enhances the strategic value proposition.

Company Overview: Discovery Group Pedigree Meets Brazilian Opportunity

ValOre Metals operates under the stewardship of the Discovery Group, a collective of mining professionals whose track record speaks to systematic value creation. The team has participated in over CAD$2.6 billion in M&A activity and raised $300 million in equity capital across multiple successful ventures. This includes transactions that resulted in acquisitions by Rio Tinto at $650 million, Goldcorp at $520 million, Royal Gold at $200 million, and Coeur Mining at $117 million.

Chairman Jim Paterson brings 27 years of executive leadership experience as co-founder and principal of the Discovery Group. His career encompasses five major discoveries, while CEO Nick Smart contributes 21 years of operational expertise from Anglo American and De Beers, with direct experience in the design, construction, and operation of large-scale mining projects spanning platinum and zinc in South Africa, nickel in Brazil, and diamonds in Canada.

The corporate structure reflects confidence from insiders and institutional participants, with 20% ownership by insiders and advisors, 10% by close associates, and 25% by resource-focused funds. This alignment of interests between management and shareholders reduces agency risk and ensures decision-making remains focused on long-term value creation. VP Exploration Thiago Diniz, who holds a Master of Science in Economic Geology from Queen's University, leads the on-the-ground Brazilian team with extensive experience in fertilizer, base metals, and precious metals exploration across Brazil and Canada.

Asset Quality: Pedra Branca Offers Scale & Development Optionality

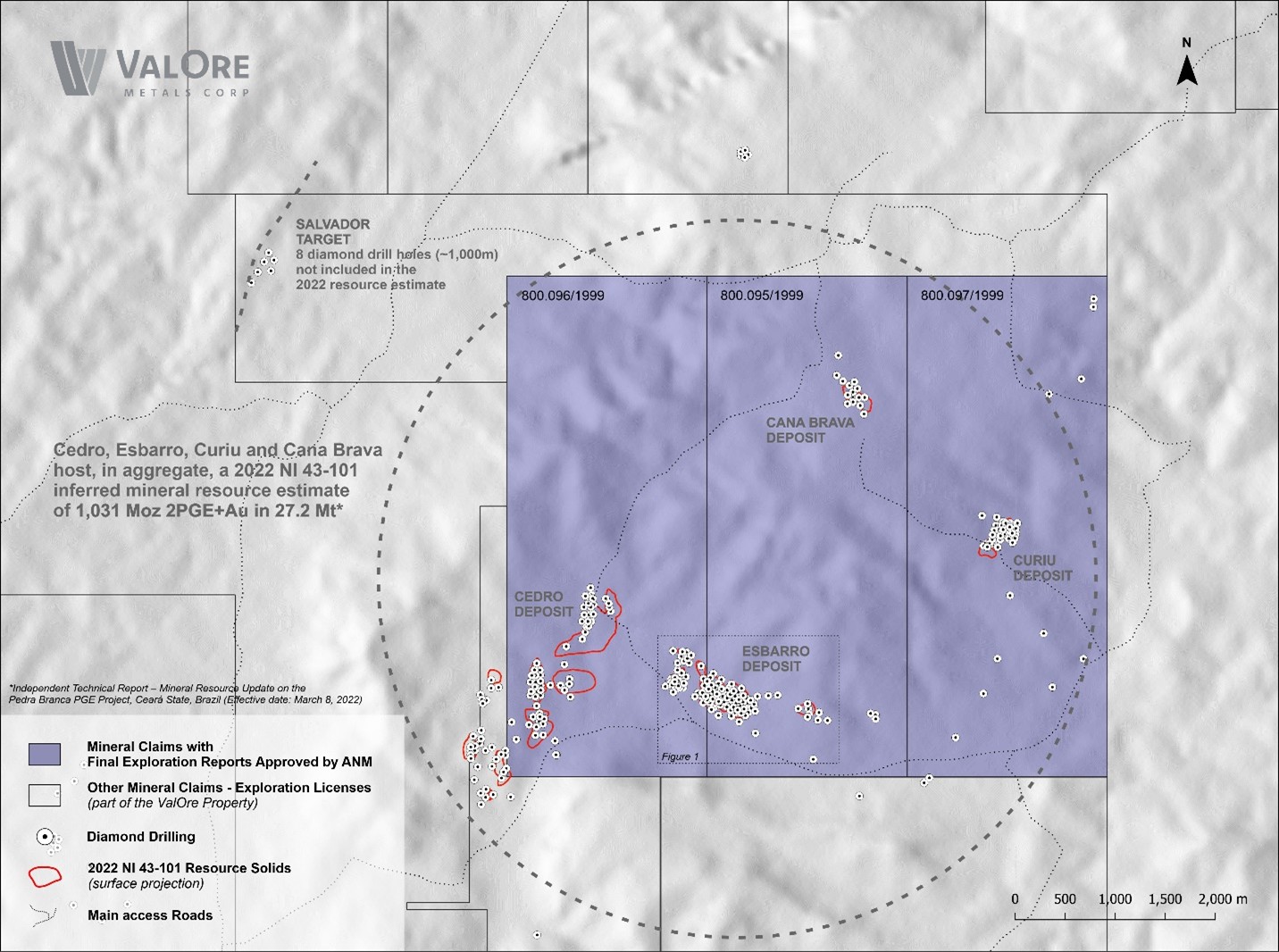

The Pedra Branca project in northeastern Brazil represents ValOre's flagship asset. The property comprises 51,096 hectares in Ceará State and hosts an NI 43-101 compliant inferred resource of 2.2 million ounces of platinum, palladium, and gold at a grade of 1.08 g/t across seven near-surface resource zones. This resource was established through USD$30 million in historical investment by previous operators covering 30,000 meters of drilling, with ValOre having invested CAD$10 million in exploration including 23,534 meters of additional drilling.

The geological setting features multiple near-surface orebodies with excellent regional infrastructure access. Four core deposits anchor the resource base, while exploration drilling in 2023 identified five new zones not included in the current resource estimate, including the Salvador Target discovery. This suggests significant resource expansion potential along an emerging north-south exploration trend extending over 80 kilometers of prospective and underexplored PGE territory.

Development economics will be informed by comprehensive metallurgical testwork currently underway in partnership with the University of Cape Town. This work includes both conventional flotation processes and innovative bacteria-based bioextraction techniques that could deliver more efficient, lower-cost, and lower-impact processing routes. Infrastructure advantages are substantial, with the project located a four-hour drive from Fortaleza via paved highway, which hosts both a major international airport and a deep-water port capable of handling concentrate exports.

Market Fundamentals: Structural Deficits Support Price Floor

The platinum and palladium markets face supply-side constraints that have created persistent deficits and are expected to support prices through the medium term. Total platinum supply in 2025 is forecast at approximately 7.1 million ounces, with primary mining contributing around 5.5 million ounces. Against this, demand is projected at approximately 7.8 million ounces, creating the substantial deficit that represents one of the weakest supply years in recent history.

The 2026 outlook projects modest supply improvements, with total platinum supply expected to reach approximately 7.4 million ounces, representing roughly 4% growth driven by mining output projected at around 5.6 million ounces and increased recycling volumes. However, demand is forecast to moderate to approximately 7.4 million ounces, resulting in a near-balanced market with an estimated surplus of only around 20,000 ounces. This balance assumes improvements in trade flows and investment market normalization, conditions that remain uncertain given geopolitical tensions.

Even under the balanced scenario, above-ground inventory rebuilding is not expected. This means the market will remain structurally tight, with limited buffer stocks to absorb supply disruptions or demand surges. Internal combustion engine and hybrid vehicle production continues to account for over 50% of platinum group metal demand, providing sustained baseline consumption. For producers and development-stage companies, this environment translates to sustained price support, particularly given that palladium has risen 25% year-to-date while platinum has advanced 48%.

Strategic Initiatives: M&A Focus Accelerates Production Timeline

Beyond the Pedra Branca development path, ValOre has articulated a clear acquisition strategy targeting advanced-stage gold projects in northeastern Brazil. This approach serves multiple strategic objectives: it diversifies commodity exposure, accelerates the timeline to production revenue, and leverages the team's in-country operational expertise and local relationships. According to the company's stated strategy, acquisition targets focus on high-quality precious metals assets with district-scale potential and significant prior investment demonstrating clear upside.

The company's all-Brazilian operational team provides execution capacity to advance multiple projects in parallel, a capability that many junior explorers lack. Financing for M&A activity will be supported by ValOre's access to international capital markets via TSX and potential Bovespa listings, backed by an experienced board of directors. Strategic equity partnerships with resource-focused funds further enhance the company's ability to deploy capital efficiently.

The M&A strategy also incorporates advanced data analytics through a partnership with VRIFY, enabling reprocessing of legacy geophysical and geological datasets using modern interpretation techniques. Given that less than 30% of Brazil has been mapped to high-resolution geological or geophysical standards, this approach offers asymmetric upside in identifying overlooked opportunities. The first M&A announcement is targeted for Q1 2026, with production from acquired assets expected to commence in Q3 2026, establishing cash flow generation ahead of the Pedra Branca development decision.

Current Activities & Near-Term Milestones

ValOre's operational focus centers on de-risking the Pedra Branca project through comprehensive metallurgical testwork while simultaneously advancing the acquisition pipeline. The metallurgical program includes both conventional flotation and innovative bioextraction techniques being developed in partnership with academic institutions. According to the company's growth trajectory, completion of Pedra Branca metallurgical testwork is scheduled for Q4 2025 to demonstrate the optimal process route, with bacteria-based bioextraction showing high potential for efficient, lower cost, and lower impact processing.

The exploration team continues to evaluate the Salvador Target and other zones identified in the 2023 drill program. These targets, not included in the current 2.2 million ounce resource, represent near-term growth opportunities that could materially increase the project's scale ahead of the PEA. On the corporate development front, management is actively evaluating advanced-stage gold opportunities in northeastern Brazil, with the region hosting numerous projects that now face capital constraints or lack the technical capacity to advance assets through permitting and feasibility stages.

Permitting and environmental impact assessment work for Pedra Branca is scheduled to commence in Q1 2027, following publication of the PEA in Q4 2026. Brazil's regulatory environment has improved significantly, with stable regulatory frameworks supporting investment and streamlining approvals. The country is now among the top 10 gold producers globally, producing approximately $3.8 billion annually and targeting growth to over $6 billion by 2030. Community engagement remains a priority, with strong local support evident in workforce participation and collaborative relationships with regional stakeholders, reducing permitting risk.

Financial Position & Capital Structure

As of November 1, 2025, ValOre reported 254.9 million shares outstanding, a market capitalization of approximately CAD$29.3 million at a share price of $0.115, and cash of CAD$1.3 million. The 52-week trading range spanned $0.050 to $0.155, reflecting both sector volatility and the typical valuation compression experienced by pre-revenue development companies in junior mining markets.

The ownership structure shows 20% held by insiders and advisors, 10% by close associates, 25% by resource and mining funds, and 45% by retail and other investors. This distribution indicates both management confidence and growing institutional recognition. Capital requirements for near-term objectives are manageable, with metallurgical testwork completion and PEA preparation requiring funding through Q4 2026, while M&A activity will be structured to minimize dilution through strategic partnerships.

The company's Discovery Group affiliation provides access to capital networks and co-investment opportunities that are not available to most junior explorers. For investors evaluating entry points, the current valuation implies a substantial discount to peer companies with comparable asset quality or management teams. This valuation gap reflects both the inferred resource classification and the company's pre-feasibility stage, but also creates meaningful upside as technical studies advance and resource categories are upgraded.

Investment Thesis for Platinum Group Metal Exposure Through ValOre Metals

- Establish exposure to supply-constrained PGE markets through a development-stage asset with 2.2M oz resource and near-term technical catalysts including metallurgical testwork completion (Q4 2025) and PEA publication (Q4 2026).

- Leverage proven management track record evidenced by CAD$1.7B in successful M&A transactions and five major discoveries, reducing execution risk relative to peer companies without comparable experience.

- Access Brazilian mining sector growth through strategically located assets benefiting from improved regulatory frameworks, established infrastructure, and a deepening talent pool that now exceeds North American mining engineering graduate rates.

- Diversify commodity exposure and accelerate production timeline through active M&A targeting advanced-stage gold projects, with first transaction expected Q1 2026 and production initiation Q3 2026.

- Monitor platinum market fundamentals closely, as forecasted 2026 balance remains conditional on trade normalization and investment flows; structural tightness persists even under optimistic scenarios, suggesting limited downside price risk.

- Consider position sizing that reflects development-stage risk profile while recognizing upside optionality from resource expansion at Pedra Branca, technology advantages in metallurgical processing, and multiple near-term catalysts.

ValOre Metals offers institutional and sophisticated retail investors exposure to a tightening platinum group metals market through a well-managed, strategically positioned development asset. The convergence of favorable market fundamentals, characterized by structural supply deficits and limited inventory buffers, with near-term technical catalysts creates a defined pathway to value realization over an 18-to-24-month horizon. The management team's proven track record in discovery, development, and M&A execution distinguishes ValOre from the broader universe of junior exploration companies.

The company's Brazilian operational focus provides access to an underexplored geological environment with improving regulatory certainty and deepening technical talent pools. Near-term catalysts include metallurgical testwork completion in Q4 2025, the first M&A announcement in Q1 2026, production initiation from acquired assets in Q3 2026, and PEA publication in Q4 2026. Each of these milestones offers a discrete opportunity for valuation rerating as technical and commercial uncertainty is reduced.

For mining-focused portfolios, ValOre represents a mid-risk, high-reward exposure that complements both operating producers and pure-play exploration companies. The 2.2 million ounce resource provides scale sufficient to support meaningful production profiles, while exploration upside and acquisition optionality create multiple pathways for resource growth and value creation. The platinum market outlook supports a constructive view on PGE-leveraged equities, with structural constraints on supply expansion suggesting that even optimistic supply forecasts may prove difficult to achieve, creating upside asymmetry for developers positioned to benefit from sustained market tightness.

TL;DR

ValOre Metals (TSX-V: VO) holds a 2.2M oz platinum-palladium-gold resource in Brazil as PGE markets face structural deficits through 2026. Proven management with CAD$1.7B in M&A success is advancing metallurgical studies (Q4 2025) and targeting production via gold acquisitions (Q3 2026). At current valuations, the stock offers leveraged exposure to tight platinum fundamentals with multiple near-term catalysts.

FAQs (AI-Generated)

The Pedra Branca project in Brazil holds a 2.2 million ounce NI 43-101 inferred resource of platinum, palladium, and gold grading 1.08 g/t across seven near-surface zones.

Platinum faces a projected 692,000 oz deficit in 2025 due to constrained supply and robust demand, with prices up 48% year-to-date, supporting economic viability for PGE developers.

Metallurgical testwork completion in Q4 2025, first M&A announcement in Q1 2026, production from acquisitions in Q3 2026, and Pedra Branca PEA in Q4 2026 provide sequential catalysts.

The Discovery Group team has delivered five major discoveries and participated in CAD$1.7B in M&A transactions, demonstrating systematic value creation and operational execution capability.

Brazil offers stable regulatory frameworks, established infrastructure near Pedra Branca, and graduates more mining engineers than the USA and Canada combined, reducing operational and permitting risks.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed