China's Strategic Critical Mineral Classification of Platinum & Its Investment Implications for Global PGM Supply, Pricing, and Emerging Developers

China's platinum reclassification and GFEX futures launch tighten PGM markets. Supply risks and hydrogen demand favor diverse developers like ValOre Metals in Brazil.

- China's designation of platinum as a strategic critical mineral marks a structural inflection point in global PGM supply chains, driven by greater than 95 percent import dependency and intensifying energy transition needs.

- The early December 2025 launch of platinum and palladium futures on the Guangzhou Futures Exchange (GFEX) formalizes institutional investment demand and creates new physical inventory requirements that tighten markets.

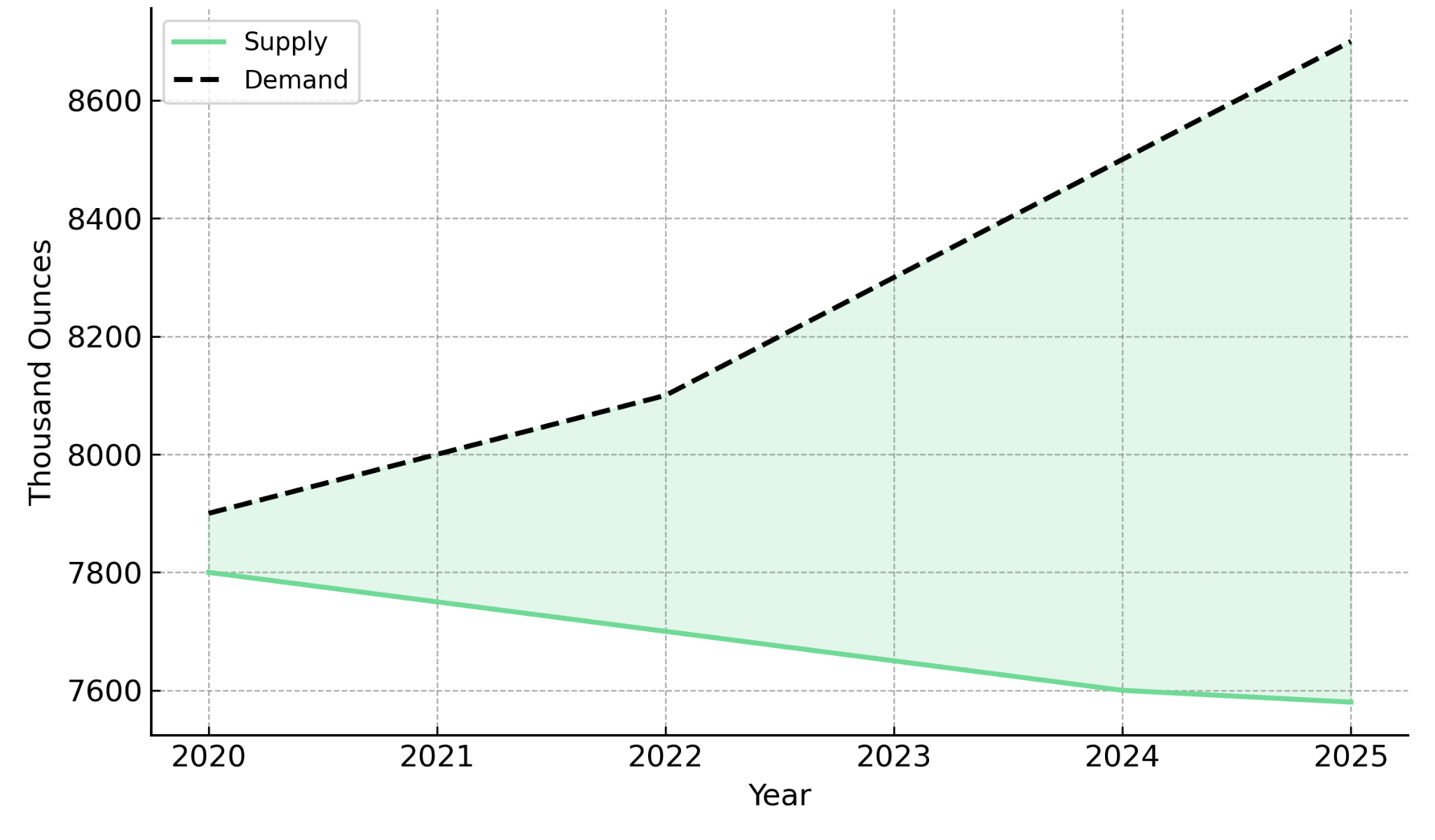

- Structural deficits in global PGM supply, compounded by South African production constraints and Russian geopolitical risk, elevate the role of new jurisdictions, including Brazil.

- ValOre Metals (exploration stage) demonstrate how non-traditional PGM regions may benefit from China's diversification push.

- Investors should monitor policy signaling, futures market liquidity, and new supply nodes as catalysts that influence long-term platinum price stability and equity valuation.

China's Policy Reclassification & the Structural Shift in Platinum Market Dynamics

China's elevation of platinum to "strategic critical mineral" status represents a materially important shift for global resource security, industrial policy, and investment flows. The classification captures extreme import dependency, negligible domestic mine supply, low substitutability, and platinum's alignment with long-term technological pathways, particularly hydrogen and advanced manufacturing.

This designation reflects Beijing's recognition that its industrial future depends on secure access to platinum group metals. Platinum's status now mirrors that of rare earths, tungsten, and antimony, resources where China has historically prioritized supply chain control through policy coordination and strategic stockpiling.

The classification signals long-term demand visibility that underpins project finance, supports price floors during cyclical downturns, and accelerates capital flows toward diversified supply sources.

Nick Smart, Chief Executive Officer of ValOre Metals, articulates the supply-side pressure:

"The last few years with prices as low as they have been has not incentivized new supply to come on… As a result you've got the situation of steady demand declining supply so older mines particularly in South Africa which become more and more challenging to operate, more costly to operate and you have a drop off in terms of supply and it leads to that deficit situation that we're seeing today right now."

The Supply Chain Exposure Beijing Seeks to Correct

Geographic concentration in South Africa and Russia creates structural vulnerability. South Africa holds 90 percent of the world's platinum resources and dominates global mine production, while Russia maintains the secondary position. This concentration exposes China to declining ore grades, rising all-in sustaining costs, power supply constraints in South Africa's Bushveld Complex, and sanctions-related disruptions to Russian metal flows.

Why Import Dependency Exceeds 95 Percent, and Why It Matters for Investors

China's import dependency for platinum group metals exceeds 95 percent, according to Weibin Deng, World Platinum Investment Council (WPIC) Regional Head Asia Pacific. This structural reliance stems from industrial-scale consumption in chemicals, catalysts, auto manufacturing, and hydrogen electrolyser development, while domestic platinum mine production remains negligible.

China lacks the geological formations that host economic platinum deposits. This geological reality means China will remain a net importer for the foreseeable future. For investors, this dynamic supports long-term investment confidence in platinum by signaling that demand will persist across commodity cycles.

The Energy Transition as the Strategic Demand Engine Behind China's Policy

Platinum's reclassification is inseparable from China's national decarbonization strategy. Hydrogen plays a central role in Beijing's 2030 carbon peak and 2060 carbon neutrality targets, and platinum is indispensable in proton exchange membrane (PEM) electrolysers, fuel cell stacks, and catalytic applications.

China has operational hydrogen refueling stations, commercial fuel cell vehicle deployments, and industrial hydrogen projects integrated into steel, chemical, and refining operations. As electrolyser capacity scales toward gigawatt levels, cumulative platinum demand increases correspondingly.

Hydrogen Fuel Cells & Electrolysers

PEM technology's dependence on platinum and palladium creates inelastic demand tied to electrolyser and fuel cell deployments. China's hydrogen mobility pilots are expanding beyond buses and trucks into marine applications, port equipment, and industrial forklifts. Provincial and municipal governments in Guangdong, Shandong, and Shanghai support hydrogen fuel-cell vehicle development through subsidy programs and refueling-infrastructure initiatives, though only selected jurisdictions, such as Shandong, have issued clear numerical adoption targets.

China's steel sector is piloting hydrogen direct reduction processes to replace coal-based blast furnaces, requiring large-scale electrolyser capacity. Chemical plants are integrating green hydrogen into ammonia synthesis and methanol production. These industrial applications represent multi-decade demand streams that exceed transportation sector consumption.

Industrial Catalysts & Advanced Manufacturing: Persistent, Irreversible Demand

Chemical catalysts require platinum group metals due to high-temperature stability, oxidation resistance, and selectivity in complex reaction pathways. Platinum catalyzes nitric acid production, petroleum refining processes, and pharmaceutical synthesis, applications where substitution is technically infeasible or economically prohibitive.

Auto catalytic converters still represent major platinum loadings in internal combustion engine (ICE) and hybrid vehicles. Even under aggressive electric vehicle transition scenarios, catalytic demand declines slower than expected due to hybrid market share persisting through the 2030s.

Nick Smart, Chief Executive Officer of ValOre Metals, emphasizes the breadth of industrial demand drivers:

"Our general view is that the demand drivers are pretty strong for both platinum and palladium. The chemical and physical properties of platinum and palladium have a lot of advantages for more generalist industrial catalysts as well. What makes them useful as autocatalysts makes them useful in an industrial context as well. "

GFEX: How China Is Rewiring Global Price Discovery & Institutionalizing Platinum as an Investment Asset

The early December 2025 launch of platinum and palladium futures on the Guangzhou Futures Exchange (GFEX) represents a watershed moment. It gives China its first domestic PGM price discovery mechanism, shifting influence away from London and New York markets.

Key innovations distinguish GFEX from existing exchanges. The platform accepts platinum ingots and sponge as deliverable grades, a unique global feature tailor-made for industrial manufacturing flows. Contracts are RMB-denominated, enabling natural currency hedging for domestic users.

The Financialization of Platinum Inside China

Physical bar and coin investment demand in China is forecast to reach 453,000 ounces by 2026, according to World Platinum Investment Council forecasting. This represents structural demand growth driven by wealth accumulation and platinum's positioning as a strategic metal hedge.

Platinum's classification as a critical mineral elevates its status beyond industrial commodity to national security asset. This perception shift supports long-term accumulation behavior that provides price floor support during cyclical downturns.

Physical Demand Effects: Why Futures Markets Tighten the Real Supply Chain

Margin requirements create mandatory physical inventory warehousing at GFEX-approved facilities. As open interest grows, warehoused platinum increases proportionally, removing material from immediately available supply and tightening the physical balance. Rising contract volumes translate into higher underlying metal demand through arbitrage mechanisms.

Global Supply Chain Repercussions: Winners, Losers, & the Capital Flows Likely to Follow

China's reclassification triggers a global recalibration of supply chains. The policy creates clear beneficiaries among established producers and emerging developers in jurisdictions that offer diversification benefits.

Emerging developers in Brazil, Australia, and Canada represent strategic diversification targets for Chinese capital. These regions offer regulatory stability, transparent permitting processes, and developed mining sectors with technical expertise.

Nick Smart, Chief Executive Officer of ValOre Metals, contextualizes the extreme concentration risk:

"South Africa holds 90 percent of the world's resources of platinum and not just production resources. It's the dominant space for that. Secondary position being Russia."

South Africa: The Immediate Beneficiary but Still Constrained by Cost Pressures

South Africa hosts the world's largest platinum endowment, positioning South African producers as essential suppliers to Chinese industrial users. However, operating cost inflation continues due to deeper mining levels, power sector constraints, and rising labor costs.

Brazil, Australia, & Canada: New Frontiers for PGM Diversification

Brazil offers particular advantages: established mining code with innovative frameworks like trial mining programs, deepwater port infrastructure, established mining workforce, and proximity to Atlantic shipping lanes.

Nick Smart, Chief Executive Officer of ValOre Metals, highlights jurisdictional advantages:

"When we look at where we are interested in developing projects, our project Pedra Branca in Brazil is in a stable jurisdiction with fantastic infrastructure, good access to electricity, and a supportive government in terms of permitting and bringing that forward. That's a huge advantage for us in that space… One thing worth talking about is the sheer level of talent that exists within Brazil, particularly on the mining side."

ValOre Metals & the Rise of Brazilian PGM Development

ValOre Metals represents an exploration-stage PGM company operating in Brazil. The company's Pedra Branca project contains 2.2 million ounces of inferred two platinum group elements plus gold (2PGE+Au) resources at near-surface depths with an average grade of 1.08 grams per tonne. The project is located in Ceará state, approximately a four-hour drive via paved highway from the Port of Pecém, a deepwater facility.

Pedra Branca sits in a jurisdiction with established mining infrastructure, access to electricity from the national grid, and a skilled workforce. Brazil's mining code provides transparent permitting processes and fiscal certainty. The country's trial mining regulatory program allows companies to acquire preliminary licenses and build demonstration plants at smaller scale, a framework that aligns with preliminary economic assessment requirements.

Metallurgical testwork at Pedra Branca encompasses flotation, leaching, and bio-extraction processes designed to optimize recoveries and minimize processing costs. Early-stage metallurgical clarity is critical for PGM projects given complex mineralogy and the economic sensitivity of recovery rates to project returns.

Key Risks & Counterpoints Investors Must Monitor

Volatility in hydrogen adoption curves remains the primary demand-side risk. If electrolyser deployments lag policy targets due to cost overruns or technology delays, platinum intensity forecasts may prove optimistic. Investors should monitor electrolyser capacity additions and hydrogen infrastructure investment levels as leading indicators.

South African supply dynamics represent ongoing uncertainty. New shaft development could add supply, though cost pressures and infrastructure constraints limit near-term expansion potential.

Metallurgical complexity risks for early-stage developers cannot be dismissed. PGM projects frequently encounter process challenges that increase capital intensity or reduce recoveries. Investors should scrutinize metallurgical testwork quality and management team track records.

Chinese regulatory adjustments that could alter GFEX liquidity represent policy risk. Investors should monitor GFEX trading volumes and regulatory commentary as indicators of policy effectiveness.

Investment Thesis for Platinum

- China's strategic reclassification creates a structurally higher floor for long-term platinum demand, reducing downside price risk and improving project finance economics across the development pipeline.

- Hydrogen sector growth accelerates platinum intensity across electrolysers and fuel cell stacks, anchoring demand in multi-decade industrial buildouts that represent long-cycle commitments once capital is deployed.

- GFEX futures market institutionalizes investment demand and increases physical collateral requirements, tightening inventories and providing new transparency into Chinese purchasing patterns that improve market forecasting accuracy.

- Geopolitical concentration risk in South Africa and Russia supports price resilience and incentivizes alternative supply development, creating capital allocation opportunities toward developers in jurisdictions offering regulatory stability and operational predictability.

- Developers in geopolitically stable jurisdictions such as Brazil through ValOre Metals provide new optionality for investors seeking exposure to long-cycle PGM growth without the operational constraints and geopolitical risks associated with concentrated traditional supply sources.

How China's Strategic Positioning Rewrites the Long-Term Outlook for Platinum

China's policy signaling represents the defining macro driver reshaping platinum markets for the next decade. The strategic classification, GFEX futures launch, and hydrogen infrastructure buildout create demand visibility that supports higher price floors and reduces cyclical volatility.

This transition occurs amid persistent supply constraints in South Africa, geopolitical risks affecting Russian flows, and limited pipeline development in traditional producing regions. This creates opportunities for developers in new jurisdictions offering jurisdictional stability, metallurgical clarity, and infrastructure access. ValOre Metals and similar exploration-stage companies in Brazil, Australia, and Canada fit into a structurally changing supply narrative where diversification carries strategic premium.

China's strategic positioning rewrites the investment framework for platinum. The metal's role in energy transition technologies, combined with supply chain vulnerabilities Beijing seeks to correct, creates a multi-year investment thesis supported by policy coordination, capital allocation, and infrastructure development.

TL;DR

China's designation of platinum as a strategic critical mineral marks a structural shift in global platinum group metals markets, driven by greater than 95 percent import dependency and hydrogen energy transition requirements. The December 2025 launch of platinum futures on the Guangzhou Futures Exchange creates domestic price discovery mechanisms and increases physical inventory requirements that tighten supply. Structural deficits intensify as South African production faces cost pressures and Russian supply carries geopolitical risk. China's policy signals long-term demand visibility that supports higher price floors and accelerates capital toward diversified supply sources in stable jurisdictions. Developers like ValOre Metals in Brazil benefit from infrastructure access, regulatory transparency, and jurisdictional stability as alternatives to concentrated traditional supply regions.

FAQs (AI-Generated)

China designated platinum as strategic due to extreme import dependency exceeding 95 percent, negligible domestic mine production, and platinum's essential role in hydrogen electrolysers, fuel cells, and industrial catalysts required for China's 2030 carbon peak and 2060 carbon neutrality targets. The classification reflects Beijing's recognition that secure platinum access is critical for industrial competitiveness and energy transition execution.

GFEX launched platinum and palladium futures in early December 2025, providing China's first domestic PGM price discovery mechanism. The exchange accepts platinum ingots and sponge as deliverable grades and operates with RMB-denominated contracts, enabling natural currency hedging. Physical inventory requirements for margin collateral remove material from available supply, tightening physical balances as trading volumes increase.

Geographic concentration creates structural vulnerability, with South Africa holding 90 percent of global platinum resources and Russia maintaining secondary position. South African producers face declining ore grades, rising all-in sustaining costs, power supply constraints in the Bushveld Complex, and deeper mining requirements. Russian supply carries sanctions-related disruption risks that compound supply chain uncertainty.

Platinum is indispensable in proton exchange membrane (PEM) electrolysers and fuel cell stacks used for hydrogen production and mobility applications. China's hydrogen infrastructure includes operational refueling stations, commercial fuel cell vehicle deployments, and industrial applications in steel, chemicals, and refining. As electrolyser capacity scales toward gigawatt levels, cumulative platinum demand increases correspondingly, creating multi-decade demand streams.

These jurisdictions offer regulatory stability, transparent permitting processes, developed mining sectors, and reduced geopolitical risk compared to concentrated supply sources. Brazil specifically provides established mining infrastructure, skilled workforce, deepwater port access, and innovative regulatory frameworks like trial mining programs. ValOre Metals' Pedra Branca project exemplifies Brazilian advantages with near-surface resources, electricity grid access, and proximity to export infrastructure.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

Stay Informed