Wallbridge Mining Outlines 4‑Year Plan to Advance Fenelon Gold Project in Quebec

.webp)

Wallbridge Mining: 4.25M oz Quebec gold, $1.4B NPV at $3K gold, $100M market cap. Near-term catalysts: met testing, Martiniere drilling. Clear path to 107K oz/yr production.

- Wallbridge Mining controls 3.5 million ounces at Fenelon (half indicated, half inferred) and 750,000 ounces at Martiniere in Quebec's Abitibi region, representing substantial resource scale in a premier mining jurisdiction

- March 2025 PEA for Fenelon demonstrates $1.4 billion NPV, 34% IRR, and 2.4-year payback at $3,000 gold, with 107,000 ounces annual production over 15-year mine life (127,000 ounces/year in first five years)

- Management requires $50-60 million for pre-feasibility study with focus on right-sized 3,000 ton-per-day operation, targeting four-year timeline to construction readiness including permitting and Indigenous agreements

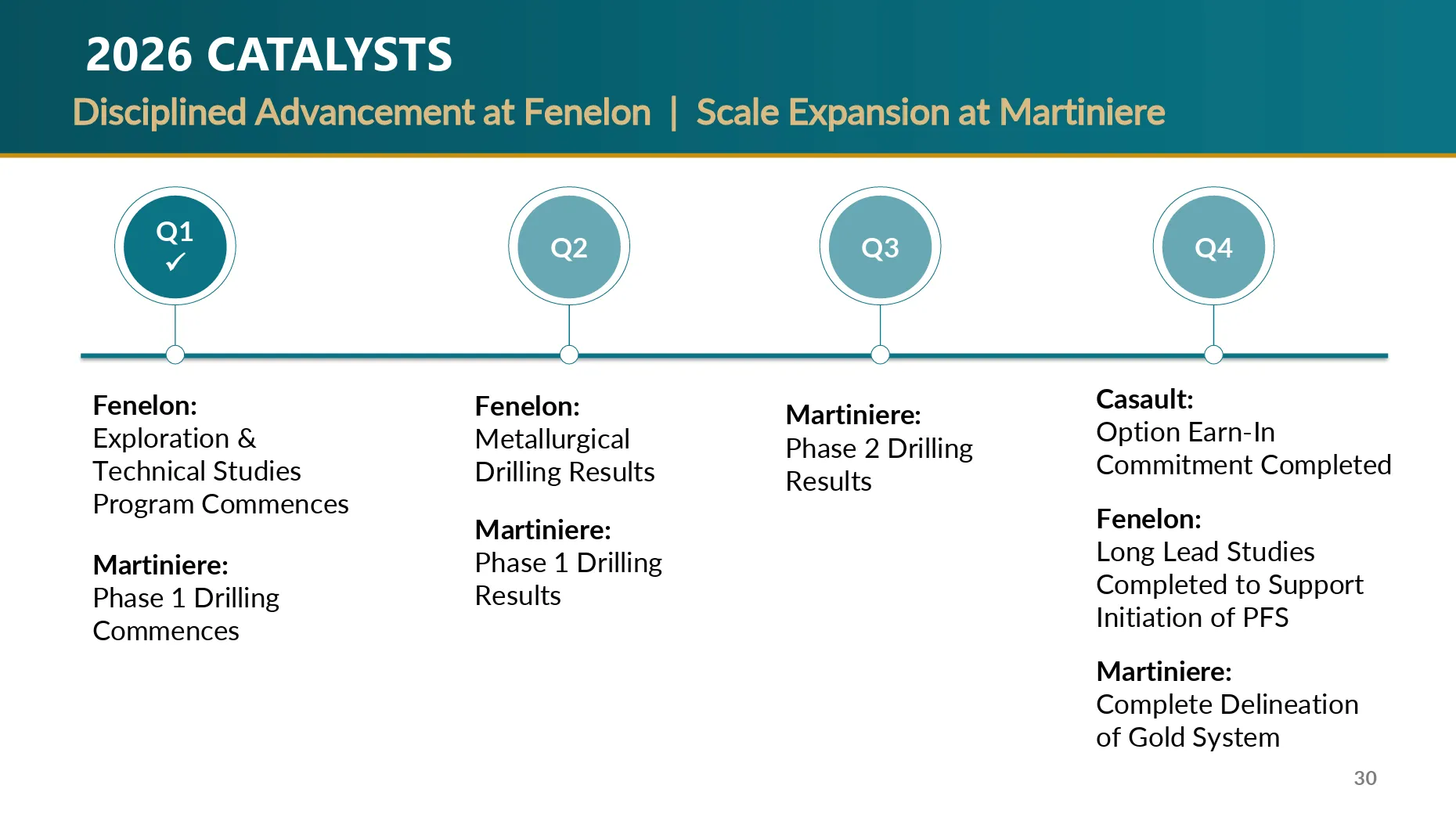

- Metallurgical testing results expected to confirm recovery assumptions and dry-stack tailings viability; Martiniere drilling program targeting 2km strike length with results providing exploration upside throughout 2026

- Current $100 million market capitalisation creates potential re-rating opportunity as company advances through de-risking milestones toward pre-feasibility and feasibility studies

Wallbridge Mining Company is advancing two gold projects in Quebec's established Northern Abitibi mining district at a time when gold market fundamentals are strengthening. CEO Brian Penny, speaking at the 121 Mining Investment conference in London, outlined a methodical development approach focused on converting a substantial resource base into production while managing capital efficiency. With gold prices significantly higher than the $3,000 base case used in the company's preliminary economic assessment, Wallbridge's projects are positioned to benefit from improved sector conditions while the company works through critical de-risking milestones.

The Northern Abitibi Resource Portfolio

Wallbridge controls approximately 600 square kilometers of property across two main projects separated by 30 kilometers. The more advanced Fenelon project hosts a resource of 3.5 million ounces, evenly split between indicated and inferred categories. The earlier-stage Martiniere project contains 750,000 ounces, also divided equally between indicated and inferred. Management is evaluating both projects on a standalone basis, with Martiniere required to demonstrate independent viability before considering any integrated development scenario.

The Fenelon deposit has evolved significantly from its origins. Initial exploration identified a high-grade gabbro zone that yielded 18 grams per ton in a 2018-2019 bulk sample, but subsequent drilling revealed this zone to be finite with much of it extracted during the bulk sample program. Further exploration discovered multiple zones including Area 51, Tabasco/Cayenne, and various contact zones that now comprise the current resource estimate. This geological evolution influenced management's decision to move away from earlier concepts of large-scale open pit mining toward a focused underground operation.

Preliminary Assessment Demonstrates Strong Returns

The preliminary economic assessment completed in March 2025 used resource estimates current as of December 31, 2024, providing investors with recent data. At $3,000 per ounce gold, the study generated a net present value of $1.4 billion, an internal rate of return of 34%, and notably, a payback period of 2.4 years. Penny emphasised the importance of rapid capital recovery: "I'm a financial guy, a payback of 2.4 years, very attractive to invest in."

The production profile contemplates 107,000 ounces annually over a 15-year mine life. However, by front-loading higher-grade material from the deposit core, the first five years would produce 127,000 ounces per year, enabling the accelerated payback. This sequencing strategy directly supports the project's financial metrics while maintaining a substantial resource tail for potential expansion or extended mine life.

Strategic Right-Sizing Philosophy

A critical strategic decision involved determining optimal project scale. Rather than pursuing maximum throughput, management analysed various tonnage-grade scenarios to identify the appropriate mill size for Wallbridge's corporate profile and risk tolerance. The team settled on 3,000 tons per day, a deliberate choice that Penny described by reference: "I view Fenelon as an underground version of Artemis."

This right-sizing philosophy incorporates multiple strategic considerations. A smaller operation reduces permitting complexity, minimises surface disturbance to support Indigenous community agreements, and creates a more manageable financing requirement. Importantly, the 3,000 ton-per-day scenario utilises approximately half the current resource base, providing substantial reserve life cushion and optionality for future expansion if conversion drilling exceeds expectations or additional resources are discovered.

The mine planning employed raised cutoff grades to optimise economics in a higher gold price environment. While the resource estimate used a 1.5 gram cutoff, mine planning tested scenarios at 2.0 and 2.5 grams without materially impacting results. This allowed selective mining of higher-grade zones while maintaining project economics, contrasting with industry trends toward lower cutoffs.

Interview with Brian W. Penny, CEO and Director, Wallbridge Mining

The Path to Pre-Feasibility Study

Advancing Fenelon to pre-feasibility stage requires an estimated $50-60 million, predominantly allocated to infill drilling to convert resources from inferred to indicated categories. Management has identified a realistic four-year pathway to construction readiness, encompassing pre-feasibility study, feasibility study, Indigenous impact benefit agreements, and permitting processes. Penny acknowledged the capital requirement is substantial for a $100 million market capitalisation company but framed it within value creation context: "Everybody talks about dilution. If dilution leads to accretion, you win."

Rather than building an extensive internal technical team that requires ongoing overhead, Wallbridge plans to augment with a COO or senior engineer while contracting most technical work. This lean structure aligns with the company's single objective of advancing through development stages without creating permanent cost burdens that would persist beyond project delivery.

Near-Term Catalysts: Metallurgical Testing and Martiniere Drilling

Before committing to the full pre-feasibility drilling program, Wallbridge is completing long-lead-time studies that will validate PEA assumptions and inform detailed engineering. A revised metallurgical testing program is underway using representative samples from planned mining phases across the 15-year mine life. Previous metallurgical work from five years ago indicated 96% recovery, but the current program will provide comprehensive data across the expanded resource base.

The metallurgical testing will also verify assumptions regarding dry-stack tailings and paste backfill technologies, which are critical for minimising surface disturbance. Management expects favourable results given the absence of clay content that typically complicates dry-stack tailings, but confirmation will tick an important box for pre-feasibility engineering and permitting discussions.

Martiniere represents the company's primary near-term exploration catalyst. A drilling program is targeting a prospective mineralised zone with 2 kilometers of strike, 800 meters width, and 800 meters depth. Importantly, none of the previous year's drilling results are incorporated into current resource estimates, and management noted several high-grade intersections warrant follow-up. Results from this program should provide news flow throughout the year while the longer-term Fenelon advancement continues.

Valuation Disconnect and Strategic Optionality

The company's $100 million market capitalisation stands in stark contrast to the $1.4 billion PEA net present value. Penny acknowledged this disconnect directly, noting the market understands the company's dual-asset strategy but hasn't reflected project economics in the share price. The management team believes executing on near-term catalysts - particularly metallurgical test results and Martiniere drilling - will help close this valuation gap and improve equity positioning for the eventual pre-feasibility financing.

Regarding strategic options, management maintains flexibility while advancing on the assumption of independent development. Penny stated the approach directly:

"We will continue on building it. Ultimately, we may build it, but if something comes in, we're in business for our shareholders and we do what's right."

The disciplined de-risking strategy positions the company to either build the project or potentially attract acquisition interest at valuations that reflect reduced development risk and advanced permitting.

The Investment Thesis for Wallbridge Mining

- Substantial resource base in premier jurisdiction: 3.5 million ounces at Fenelon plus 750,000 ounces at Martiniere located in Quebec's established Abitibi mining district with supportive regulatory framework and mining infrastructure

- Compelling project economics with upside: $1.4 billion NPV and 34% IRR at $3,000 gold provides significant margin of safety at current gold prices exceeding $4,500, with 2.4-year payback reducing investor capital risk

- Right-sized development strategy: 3,000 ton-per-day operation optimized for Wallbridge's scale reduces permitting complexity, surface disturbance, and capital requirements while utilising only half of current resource base for future optionality

- Clear near-term catalysts: Metallurgical testing results expected to confirm recovery assumptions and tailings management approach; Martiniere drilling program throughout 2025 provides exploration upside outside current resource estimates

- Strategic flexibility preserved: Disciplined advancement creates optionality for either independent development or potential acquisition by mid-tier producers seeking ounces in safe jurisdiction, with further de-risking potentially commanding premium valuations

- Infrastructure advantages: Proximity to Hydro-Quebec power reduces operating cost assumptions; existing 29km power line and transfer station provide foundation for low-cost green energy from James Bay system

- Resource conversion opportunity: Approximately 50% of current resource in inferred category provides substantial upside as infill drilling converts to indicated/measured categories during pre-feasibility work, potentially expanding mineable inventory

Macro Thematic Analysis

The gold market is experiencing renewed institutional interest as traditional investors develop better understanding of the sector's fundamentals. Wallbridge's CEO noted the rapid sentiment shift within a two-week period from retracement concerns to renewed bullishness as gold pushed higher. Having experienced $250 gold as CFO of Kinross in the 1990s, Penny maintains conviction that current market dynamics support a sustained bullish environment. The structural drivers supporting gold - including central bank buying, geopolitical uncertainty, and monetary policy concerns - have created conditions where projects with strong economics at $4,500 gold are now operating in a market exceeding those assumptions. As Penny stated:

"We got a great project at $3,000 gold and it only gets better at these higher prices."

This macro backdrop provides tailwinds for development-stage companies like Wallbridge that can demonstrate clear pathways to production in favorable jurisdictions.

TL;DR: Executive Summary

Wallbridge Mining controls 4.25 million ounces across two Quebec gold projects with a PEA demonstrating $1.4 billion NPV and 34% IRR at $3,000 gold, significantly below current market prices. The company's $100 million market cap creates potential re-rating opportunities as near-term catalysts materialise including metallurgical test results and Martiniere drilling. Management's disciplined approach focuses on right-sized 3,000 ton-per-day development requiring $50-60 million for pre-feasibility, with a clear four-year pathway to construction while maintaining strategic optionality.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

.png)

Stay Informed