Why Serabi Gold Merits Serious Consideration Now

Serabi Gold scales to 60koz output by 2026 with minimal capex, strong cash flow, and exploration upside as gold tops $4,000/oz for first time.

- Serabi is executing a fully-funded expansion from current 44-47 koz annual production to 60 koz by H2 2026, requiring less than US$10 million in initial capital expenditure.

- Trading at 5.3x EV/EBITDA versus industry research suggesting 5.7x average multiples and 0.9x P/NAV versus analyst benchmarks of 0.6x, the company appears undervalued relative to its production profile and asset quality.

- Proprietary classification plants at both Palito and Coringa enable grade upgrades from sub-6 g/t to over 12 g/t with 98% waste rejection, driving exceptional transport and processing economics.

- Net cash position of US$25 million (US$30.4M cash against US$5.4M debt) with positive free cash flow supports organic growth without dilutive equity raises.

- With gold futures surpassing US$4,000/oz amid safe-haven demand from U.S. government uncertainty, tariff concerns, and rate cut expectations, Serabi's revenue potential has expanded materially.

Introduction: Timing Matters in Gold Equities

The breach of US$4,000 per troy ounce in gold futures on 7 October 2025 represents more than a psychological milestone. For gold producers, this environment creates a rare convergence: elevated spot prices, proven operational leverage, and investor appetite for exposure beyond physical metal or ETFs.

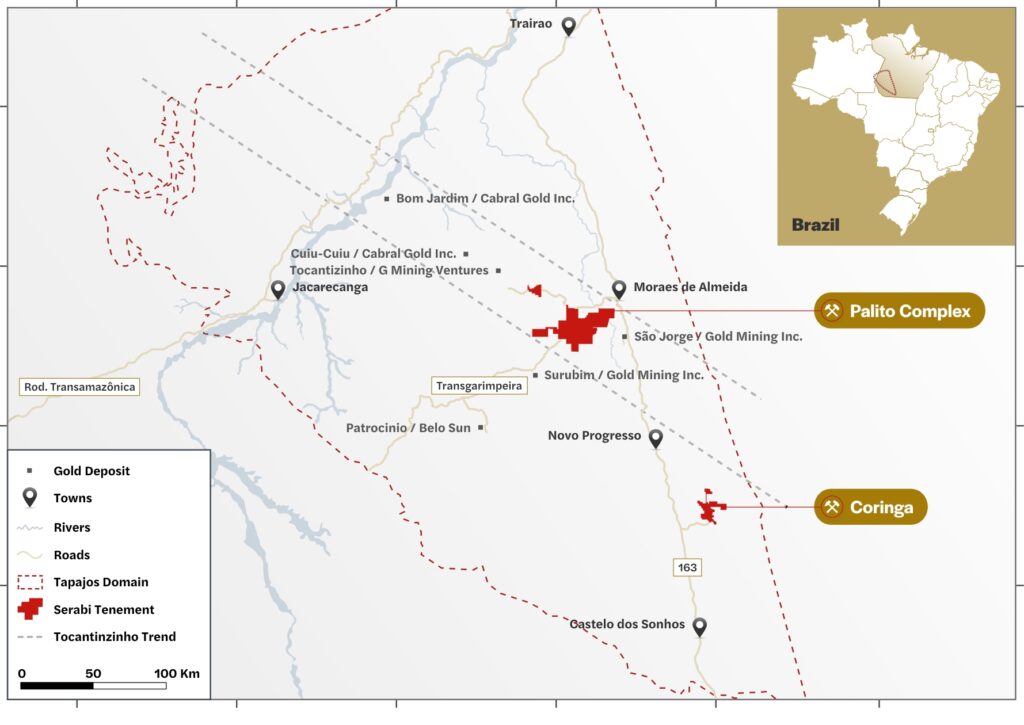

Serabi Gold, a Brazil-focused underground gold miner with a 20-year operational track record, stands at an inflection point. The company operates two wholly-owned assets in the Tapajós region of Pará State the established Palito Complex and the recently acquired Coringa project with a clear path to scaling annual output by 35% within 18 months. With a market capitalization of approximately US$275 million and enterprise value of US$250 million as of September 2025, Serabi presents institutional and retail investors with a compelling risk-reward proposition in a sector increasingly starved of growth stories that require neither large capital calls nor multi-year permitting delays.

This analysis examines why Serabi merits consideration now, grounded in operational metrics, balance sheet strength, technological differentiation, exploration optionality, and the favorable macroeconomic backdrop for gold producers.

Company Overview: Two Decades of Consistent Production

Serabi Gold has established itself as a sustainable mid-tier producer in Brazil's Tapajós mining district, delivering 30-40 koz annually from the Palito Complex since 2015. The company's 2025 production guidance of 44-47 koz represents the high end of this historical range, underpinned by steady resource replacement drilling that has replenished 444 koz cumulatively mined over the asset's life.

The Palito Complex encompasses 64,709 hectares of prospective ground with underground selective stoping methods feeding a 650-tonne-per-day processing plant utilizing flotation, carbon-in-pulp (CIP), and ore sorting technologies. As of the April 2025 NI 43-101 update, the property hosts Measured and Indicated resources of 350 koz at 9.9 g/t gold, with an additional 162 koz Inferred at 7.4 g/t. The ore bodies remain open at depth along an eight-kilometer northwest-southeast mineralized trend, providing multi-year exploration runway within the existing mining license.

Serabi's transformative acquisition came in 2023 when it purchased the Coringa project for US$22 million, securing a three-year exploitation license and a completed bankable feasibility study. The 2024 Preliminary Economic Assessment outlined an 11-year mine life producing 363 koz at an all-in sustaining cost of US$1,241 per ounce, yielding a post-tax net present value (5% discount) of US$184 million and an internal rate of return approximating 27%. Critically, Coringa ore will be trucked approximately 200 kilometers to Palito for processing following road infrastructure upgrades completed in 2024, eliminating the need for a standalone processing facility in the near term.

Key Development: The Ore Sorting Advantage

Serabi's competitive differentiation lies in its deployment of advanced ore sorting technology at both operations, a capability that fundamentally alters project economics in ways rarely seen among junior and mid-tier producers. At Coringa, the classification plant commissioned in December 2024 upgrades run-of-mine feed grading below 6 g/t to concentrates exceeding 12 g/t, rejecting over 98% of waste material before transport.

This technological edge solves what would otherwise be a prohibitive logistical challenge: moving low-grade ore 200 kilometers by truck. By doubling the head grade and reducing tonnage by 98%, Serabi transforms a marginally economic satellite deposit into a high-return asset feeding existing mill capacity at Palito. The company projects first full-year ROM processing from Coringa in 2026, with final environmental permits (LI license) expected imminently following completion of all technical requirements.

At Palito, ore sorting has been operational since 2019, primarily processing low-grade development material that would otherwise dilute mill feed. The system upgrades sub-2 g/t ore to above 10 g/t with more than 85% waste rejection, exemplifying management's "Tonnes Cost, Grade Pays" operational philosophy. This strategy maximizes mill utilization while minimizing processing costs per recoverable ounce a lever that becomes increasingly powerful as gold prices rise. With fixed processing infrastructure, every dollar increase in the gold price flows disproportionately to operating margins, and Serabi's AISC of US$1,792 per ounce in 2025 year-to-date positions the company to capture substantial margin expansion at current US$4,000+ spot prices.

Strategic Significance: The Path to 60 koz & Beyond

Serabi has articulated a three-phase growth strategy targeting 100 koz annual production, with Phase 1 execution already underway. The ramp-up to 60 koz per year by H2 2026 requires less than US$10 million in incremental capital predominantly working capital for increased mining rates at Coringa and minor processing plant modifications at Palito. This capital efficiency stems from the ore sorting infrastructure already in place and the decision to leverage existing mill capacity rather than building new processing facilities.

Phase 2, running concurrently through 2025-2026, comprises a US$9 million brownfield exploration program drilling 30,000 meters across both Palito and Coringa with the objective of expanding total resources from current levels to 1.5-2.0 million ounces. Recent drilling at Coringa's Serra Norte target intercepted 0.87 meters grading 137.48 g/t gold, 0.25 meters at 67.91 g/t, and 0.53 meters at 151.00 g/t grades that underscore the district's high-grade nature and potential for resource growth. The Coringa mineralized system extends to approximately 250 meters depth and remains open along strike within a 30-kilometer soil anomaly corridor historically worked by artisanal miners.

Phase 3, tentatively scheduled for 2027-2028 subject to Phase 2 drilling results, contemplates expansion to 100+ koz annually through either increasing Palito plant throughput or constructing a standalone processing facility at Coringa. Management has indicated this decision will be informed by resource definition success and prevailing gold prices. At US$4,000 per ounce, the economic hurdle for greenfield processing infrastructure declines materially, potentially accelerating Phase 3 timing.

Current Activities: Exploration as Value Creation

Beyond the near-term production growth story, Serabi controls a portfolio of earlier-stage exploration targets across the broader Tapajós region that offer option value rarely reflected in current valuation multiples. The company's São Domingos prospect gained attention in 2021 when drilling intersected 7.15 meters grading 258 g/t gold the seventh-highest intercept reported on the TSX that year. While this asset requires additional definition drilling before advancing to development studies, it demonstrates the district-scale prospectivity of Serabi's 64,709-hectare land package.

The Matilda copper-gold porphyry discovery, made through systematic exploration in 2022-2023, represents a different commodity exposure with an inferred resource of 81 million tonnes at 0.28% copper, including a higher-grade core of 21 million tonnes at 0.40% copper. While Serabi's primary focus remains gold production growth, the Matilda asset provides strategic optionality in a market where copper fundamentals are increasingly driven by electrification and energy transition demand. Management has flagged this as a potential joint venture or sale opportunity to unlock value without diverting capital from core gold operations.

Additional targets including Calico, Cinderella, Ganso, Forquilha, and Juca remain at early reconnaissance stages but benefit from Serabi's established regional infrastructure, permitting relationships, and geological understanding. The Tapajós district remains comparatively underexplored relative to more established Brazilian gold camps, offering genuine discovery potential. For investors seeking leverage to exploration success beyond reserve replacement drilling, this portfolio provides asymmetric upside that does not require success for the core investment thesis to work but could meaningfully re-rate valuation if discoveries emerge.

Financial Performance: Cash Flow & Balance Sheet

Serabi generated US$35.9 million in EBITDA during 2024 on post-tax profit of US$27.8 million, demonstrating the operational leverage inherent in its cost structure. Through the first nine months of 2025, the company reported US$26.3 million in EBITDA at an AISC of US$1,792 per ounce. With gold averaging approximately US$3,500 per ounce during this period, Serabi's operating margin exceeded US$1,700 per ounce a figure that expands to approximately US$2,200 per ounce at current US$4,000 spot prices.

The company maintains a net cash position of US$25 million (US$30.4 million cash against US$5.4 million debt) as of September 2025, providing substantial financial flexibility for the planned production expansion without requiring equity dilution. Industry research indicates Serabi's free cash flow yield of 11% compares favorably to sector benchmarks of approximately 6%, highlighting the company's efficiency in converting production into distributable cash, though management has prioritized reinvestment in growth over dividend initiation to date.

Relative valuation metrics suggest meaningful upside potential. At 5.3x EV/EBITDA compared to research-based sector averages of 5.7x and 0.9x P/NAV versus analyst benchmarks of 0.6x, Serabi trades at a discount despite a clearer near-term growth profile than many comparable mid-tier producers. The market appears to underweight both the production growth visibility and the exploration optionality embedded in the asset base a disconnect that typically narrows as expansion milestones are achieved and resource growth is demonstrated through drilling results.

ESG Profile: Social License & Environmental Stewardship

In an era where environmental, social, and governance factors increasingly influence investor allocation decisions and mining permit approvals, Serabi's operational profile merits attention. The company employs a workforce that is 68% sourced from Pará State and 24% from communities immediately adjacent to operations, fostering local economic participation and reducing social friction that has derailed projects elsewhere in Latin America.

Serabi invested 37,599 hours in safety training during 2024 and maintains a procurement profile where 46% of goods and services are sourced locally, multiplying the economic benefit of operations beyond direct employment. The company has committed US$1 million to community programs and biodiversity initiatives, operating under a strict policy of zero mining activity in primary forest areas and utilizing dry-stack tailings management to minimize water contamination risks.

From a carbon intensity perspective, Serabi reports emissions of 0.53 tonnes CO2-equivalent per ounce produced well below the 0.90 tonne industry average cited in research reports. This advantage is expected to improve further in 2025 as the Palito Complex transitions from diesel generation to grid-sourced power, reducing both operating costs and greenhouse gas emissions. For institutional investors operating under ESG mandates or facing pressure to decarbonize mining exposure, Serabi's profile compares favorably to sector standards while maintaining strong operational economics.

The Investment Thesis for Serabi Gold

- Purchase shares before 60 koz production run-rate is achieved and re-rating occurs.

- Every US$100 gold price increase adds ~US$4.7M annual EBITDA at 47 koz output.

- If gold holds above US$3,800, Brazilian producers offer jurisdiction discount with production growth.

- Coringa LI approval represents near-term catalyst for production acceleration confirmation.

- São Domingos and Matilda updates could drive 15-25% valuation uplift independent of gold prices.

Serabi Gold offers a rare combination in today's gold equity market: immediate production growth without major capital requirements, strong free cash flow at elevated gold prices, balance sheet strength that eliminates financing risk, and exploration optionality in an underexplored district. The company's ore sorting technology provides a structural cost advantage that competitors cannot easily replicate, while management's three-phase roadmap to 100 koz annual production establishes a multi-year growth narrative.

For investors seeking exposure to gold's current bull market beyond physical metal or large-cap producers, Serabi presents a compelling case. The stock trades at a discount to research-based sector benchmarks despite superior growth visibility and cash generation metrics, creating potential for multiple expansion as the 60 koz production target is achieved and resource growth is demonstrated. In an environment where gold futures have crossed US$4,000 per ounce driven by safe-haven demand, macroeconomic uncertainty, and expectations for lower interest rates, mid-tier producers with operational leverage and financial stability are positioned to outperform. Serabi Gold merits serious consideration as a core holding in gold-focused portfolios.

TL;DR

Serabi Gold is a Brazil-focused mid-cap gold producer positioned to scale from 44-47 koz to 60+ koz annually by 2026 with minimal capital requirements, strong cash flow generation, and significant exploration upside in the underexplored Tapajós region all while gold futures breach $4,000/oz for the first time.

FAQs (AI-Generated)

Serabi produces 44-47 koz annually now and targets 60 koz by H2 2026 with less than US$10M additional capital.

Classification plants upgrade feed from sub-6 g/t to over 12 g/t while rejecting 98% waste, drastically reducing transport and processing costs.

Net cash of US$25M (US$30.4M cash vs US$5.4M debt) with 11% free cash flow yield and positive EBITDA.

Both Palito Complex and Coringa project are in Brazil's Tapajós region of Pará State, approximately 200km apart.

[Answer 5]

Analyst's Notes

Subscribe to Our Channel

Stay Informed