Why West Red Lake Gold Mines Offers Investors Rare Access to a New High-Grade Gold Producer in a Historic Bull Market

West Red Lake Gold: New producer in gold bull market with high-grade Madsen Mine, strong ramp-up progress, and significant exploration upside potential.

- West Red Lake Gold enters the rare category of new gold producers during a bull market, with new and growing miners outperforming major gold indices by over 100%

- The company successfully restarted the high-grade Madsen Mine after addressing previous operator's technical and infrastructure failures through $350M in improvements and 140,000 meters of definition drilling

- West Red Lake Gold currently demonstrates strong production momentum, ramping up production with 10,000 ounces produced through July 2025, successful bulk sample reconciliation at 96.1% accuracy and increasing mill throughput

- The investment offers significant valuation upside with a pre-feasibility study showing C$496M NPV and potential for substantial increases through larger stopes, additional deposits (Rowan, Fork), and exploration discoveries

- The management team led by CEO Shane Williams brings 25 years of mine-building experience across multiple jurisdictions with proven track record of operational success

The Gold Bull Market & Company Vision

The investment thesis for West Red Lake Gold Mines (TSX-V: WRLG) begins with a fundamental market observation that has driven exceptional returns for investors who positioned early. As VP of Communications Gwen Preston explains:

"What you're seeing right now is evidence of how already in this gold bull market we're seeing a pattern that we see reliably in gold bull markets. And that pattern is that the companies that generating new gold production outperform the rest of the gold equities."

The data supports this thesis compellingly. New and growing gold miners have generated average returns of 154% over the past 12 months, significantly outpacing the GDX's 45% and GDXJ's 53% returns. This outperformance reflects investor appetite for companies that can deliver immediate production growth rather than distant development promises.

West Red Lake Gold positioned itself specifically to capitalize on this opportunity. Preston notes:

"West Red Lake was founded a few years ago on exactly that premise. The idea that projects had stopped in their tracks and the understanding that that would mean that when the expected gold bull market did get underway, there wouldn't be very many options in this new and growing gold miner category."

The company's strategic vision extends beyond simply offering new production. Management sees a clear path to mid-tier miner status, targeting the valuation premium that comes with producing over 150,000 ounces annually. The valuation multiple expansion is significant - while smaller producers trade at certain multiples, companies producing 200,000+ ounces per year command substantially higher market capitalizations relative to their production profiles.

All Known Questions Answered, with Gwen Preston, VP of Communications

The Madsen Mine: History & Strategic Acquisition

The Madsen Mine represents both the opportunity and the challenge that West Red Lake Gold was designed to address. Located in Ontario's famous Red Lake district, the mine has a distinguished history dating back to the 1930s-1960s when it produced 2 million ounces at an impressive 10 grams per ton average grade.

The modern chapter began in 2014 when Pure Gold recognized the potential to restart operations. After 180 kilometers of drilling, they defined a substantial resource of 1.7 million indicated ounces at 7.4 grams per ton, plus nearly 400,000 ounces of inferred resources. Pure Gold successfully permitted, engineered, and built the mine, investing approximately $350 million in the process.

However, as Preston candidly explains:

"Unfortunately, that group lacked experience in specifically building and operating narrow vein, high grade underground gold mines. And so that lack of experience means that they cut some corners. Unfortunately, the corners that they cut meant that the mine went bankrupt after 14 months of commercial operations."

This failure created the acquisition opportunity that West Red Lake Gold had been seeking. The company purchased the distressed asset in June 2023, recognizing that the fundamental problems were solvable with proper technical expertise and adequate capital. Rather than rushing to restart production, management committed to spending two years addressing the root causes of the previous failure.

The acquisition price was modest relative to the previous investment, allowing West Red Lake Gold to acquire a fully permitted, constructed mine with substantial infrastructure already in place. This dramatically reduced the typical development timeline and capital requirements that would face a greenfield project.

Technical & Operational Improvements

West Red Lake Gold's approach to restarting Madsen focused on addressing two critical categories of errors that caused the previous operator's failure: technical mining approach and infrastructure deficiencies.

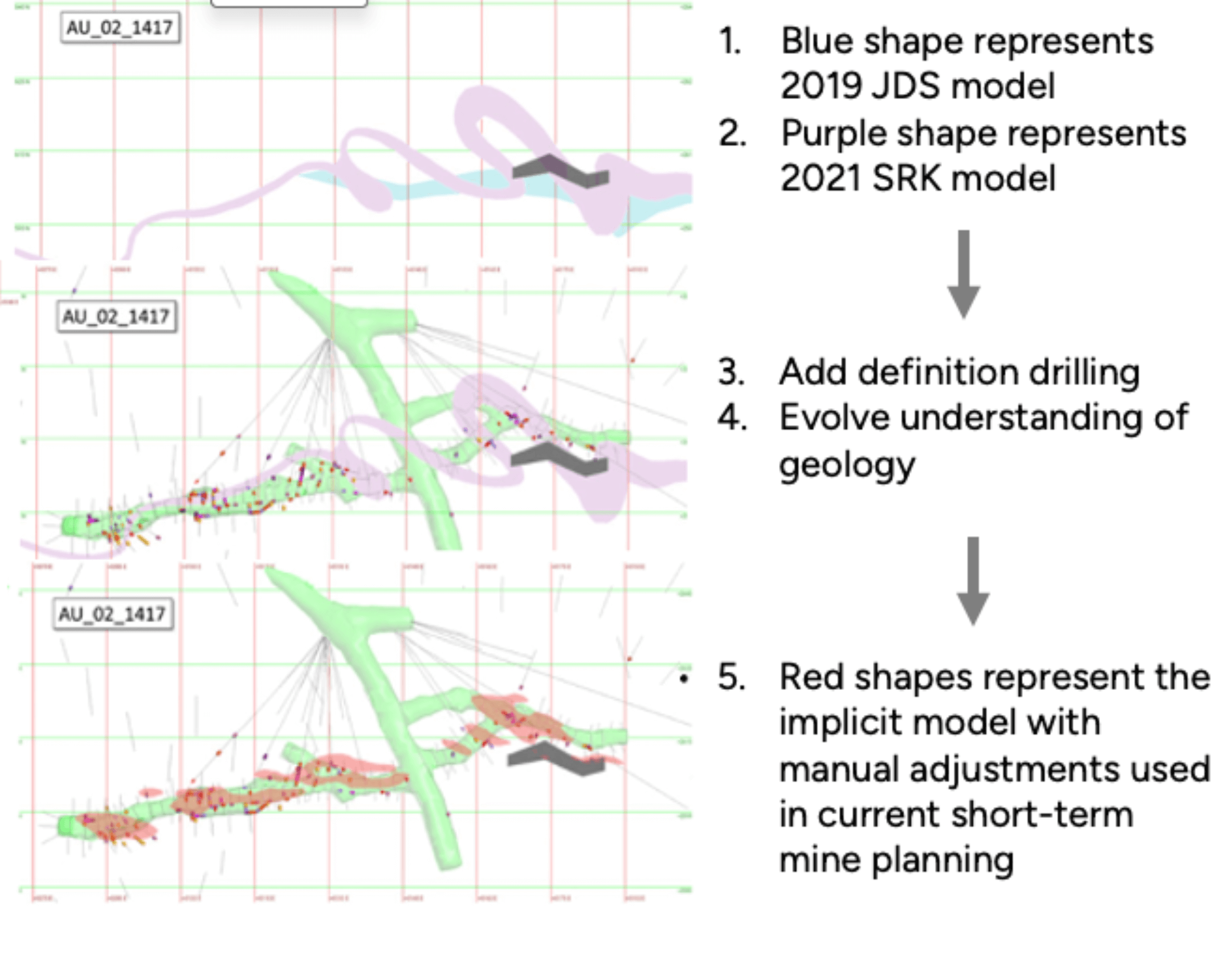

The technical solution centered on developing what Preston describes as "geology-engineering workflow to support accurate modeling and effective mining." The challenge at Madsen, common throughout Red Lake, is that while gold mineralization is high-grade and pervasive, it is not continuous. "The gold does not evenly spread throughout that purple ribbon. Instead it's in pockets, it's in a lens here and a lens there and then there's areas in between that have no gold at all."

The solution required intensive definition drilling to achieve the Red Lake standard of seven-meter drill hole spacing. West Red Lake Gold has completed over 140,000 meters of definition drilling since acquisition, compared to Pure Gold's 20-meter spacing that proved inadequate for precise mining. This tight drilling pattern enables accurate resource modeling and ensures miners extract high-grade ore rather than waste rock.

The company validated this approach through a comprehensive bulk sample program, mining 15,170 tonnes from six stopes across three resource areas. The reconciliation results were exceptional: actual tonnage came in at 95.5% of predictions, grade at 100.7%, and contained ounces at 96.1%.

On the infrastructure side, West Red Lake Gold invested in numerous capital projects that the previous operator had deferred. Key improvements included a 1.4-kilometer Connection Drift that serves as an underground highway for efficient material transport, a 114-person on-site camp, tailings dam lift, underground development, mine dewatering, and 19 major pieces of underground equipment.

These infrastructure investments address the cost structure problems that plagued the previous operator. By creating efficient material movement systems and proper operational facilities, the company positioned itself to achieve the low-cost, high-throughput operations necessary for profitability.

Ramp-Up Phase & Operational Stability

West Red Lake Gold commenced mining operations in May 2025, entering the critical ramp-up phase that determines long-term operational success. The initial results demonstrate the effectiveness of the company's technical approach and infrastructure investments.

Through July 2025, the mine produced approximately 10,000 ounces of gold, with the mill averaging 650 tonnes per day and achieving 95% gold recovery. The operational metrics show steady improvement as mining transitions from bulk sample stockpiles to fresh stope production, with grades increasing from around 4 grams per ton to over 6 grams per ton.

Preston explains the ramp-up trajectory:

"In general in ramp up, your crews, your personnel are getting more up to speed, you're adding equipment... and therefore you're increasing output. And so in general, your costs are coming down, your output is coming up, that's the goal of ramp up."

The company continues adding mining equipment to support increased production, including R1300G Caterpillar scoop loaders, Epiroc 42-tonne haul trucks, Komatsu 4-yard scoops, and Maclean bolters. This equipment acquisition supports the goal of reaching commercial production and achieving the design capacity of 800 tonnes per day.

The ramp-up phase is particularly critical for West Red Lake Gold given Madsen's history. As Preston notes:

"We went out there and told everyone that we were going to put this mine back into production. And we had lots of reasons why we were going to be able to put this mine into production successfully. We had rationale for that. But absolutely, understandably, the market needed evidence. The market wanted proof that our approach was going to work."

The bulk sample results provided initial evidence, and the successful ramp-up continues building the case for sustainable operations.

Monthly production updates demonstrate management's commitment to transparency during this critical phase. Each month of successful operations further validates the technical approach and builds investor confidence in the long-term operational outlook.

Valuation & Market Potential of Madsen Mine

The valuation case for West Red Lake Gold begins with the official pre-feasibility study, which established a C$496 million NPV for the Madsen Mine. Based on a US$2,640 per ounce gold price assumption, the study projects average annual free cash flow of C$94 million over six full production years, producing 67,600 ounces annually at an all-in sustaining cost of US$1,681 per ounce.

However, Preston argues this represents only a base case:

"I really do believe that the pre-feasibility study is only a base case for that valuation."

The study's conservative assumptions create significant upside potential through several mechanisms.

First, the PFS used a three-year trailing gold price of less than US$1,700 per ounce to determine economic viability, resulting in a highly selective mine plan focused on only the highest-grade portions of the deposit. With current long-term consensus gold prices around US$2,350 per ounce, substantially more of the resource becomes economically viable.

Second, the definition drilling program continues discovering additional high-grade mineralization. Recent intercepts include exceptional results such as 12.1 meters at 61.51 grams per ton gold, including 1 meter at 725 grams per ton. These discoveries often fill gaps between existing drill holes, adding both tonnage and grade to mining areas.

The impact of tighter drill spacing and higher gold price assumptions creates dramatically larger and more efficient mining areas.

From a market valuation perspective, developers typically trade at 0.4 times net asset value while producers command 0.7-1.0 times NAV. Similarly, producers often trade at 6-8 times annual free cash flow. With West Red Lake Gold's current market capitalization around C$300 million, the company trades below these producer multiples even on the base case PFS metrics.

Exploration Potential & Future Projects

Beyond the base case Madsen operation, West Red Lake Gold offers investors exposure to multiple value creation opportunities through exploration and additional deposits within the company's land package.

The Rowan Project, located 80 kilometers from Madsen, represents the most advanced additional opportunity. The deposit contains 195,746 indicated ounces at 12.87 grams per ton plus 115,719 inferred ounces at 8.76 grams per ton. A preliminary economic assessment envisions a toll-milling operation producing 35,200 ounces annually for five years with a 42% internal rate of return and C$125 million NPV.

Preston emphasizes Rowan's attractive mining characteristics:

"Rowan is a deposit that's designed to be mined. It is almost vertical. It starts at surface. It's relatively wide and the gold is pretty continuous within the deposit."

These geological features typically translate to lower mining costs and more predictable operations.

The Fork deposit, located directly adjacent to Madsen workings, offers near-term production potential. While historically ignored due to its 5.2 grams per ton grade - considered low-grade by Red Lake standards - West Red Lake Gold has identified a high-grade core containing an estimated 130-150 thousand tonnes at 8-9 grams per ton. The deposit's proximity to existing infrastructure makes it highly accessible, requiring only 250 meters of tunnel development.

Exploration potential extends throughout the property, with management maintaining two drill rigs and dedicating roughly half a drill to exploration beyond definition drilling requirements. Key targets include North Shore, where 2024 drilling returned broad zones of Madsen-style alteration and a till sampling program identified strong geochemical signatures coincident with favorable geological contacts.

The Upper 8 discovery demonstrates the property's exploration upside. This new high-grade shoot, discovered by drilling up-dip from the known 8 Zone, returned 15 gold intersections from 17 holes, including 1.3 meters at 44.17 grams per ton. Preston notes:

"There hasn't been real exploration work at Madsen from inside the deposit since the 1960s... The best way to find mineralization in an underground deposit is to drill from underground."

Team & Share Structure Overview

West Red Lake Gold's management team brings extensive mine building and operational experience, led by President and CEO Shane Williams. Preston highlights his background:

"He's built mines all around the world for 25 years. He spent a bunch of years with El Dorado Gold... being on the leadership teams for their mine builds in Turkey and in Greece, and then in Quebec at the Lamaque mine."

The management team was specifically assembled for operational expertise rather than promotional skills. This focus on technical competence reflects the company's strategy of creating value through operational excellence rather than market promotion. The team includes VP Technical Services Maurice Mostert (P.Eng), VP Exploration Will Robinson (P.Geo), and VP Operations Hayley Halsall-Whitney, all bringing direct underground mining experience.

The company's share structure reflects the capital raising required to restart Madsen, with 343.2 million shares outstanding and 165.3 million warrants. While this creates a relatively high share count, Preston emphasizes the company's strong trading liquidity: "we trade one to four million shares a day. We're very proud of that. So for big funds that want to get in and out, they absolutely can do that."

A significant catalyst exists in the 43 million warrants exercisable at C$1.00 expiring in May 2026. With the stock trading near C$0.93, warrant exercises could provide substantial additional capital for growth initiatives. Preston notes: "should we get above $1 and get exercise of some good portion of those... there's a lot that this team could do... with the proceeds from $43 million."

The shareholder base includes approximately 9% held by Sprott Resource Lending, 30% by gold-focused institutions, and 10% by management and insiders. This institutional backing provides stability while the management ownership aligns interests with shareholders.

The Investment Thesis For West Red Lake Gold Mines

- Market Timing Advantage: Rare entry point into new gold production during confirmed bull market, with new producers outperforming indices by 100%+ margins

- Proven Asset Revival: Successfully restarted high-grade mine through systematic addressing of previous technical and infrastructure failures, validated by 96.1% bulk sample reconciliation

- Strong Production Trajectory: 10,000 ounces produced in first months of ramp-up with steadily improving grades and throughput approaching design capacity

- Valuation Disconnect: Trading at C$300M market cap versus C$496M base case NPV, with multiple upside catalysts through larger stopes, higher gold prices, and additional deposits

- Diversified Growth Pipeline: Rowan project offers 35,200 oz/year additional production potential, Fork deposit provides near-term expansion, exploration targets offer discovery upside

- Experienced Leadership: Management team with 25+ years of mine building experience and proven track record of operational success in similar geological environments

- Financial Optionality: C$43M in near-the-money warrants provide growth capital if stock exceeds C$1.00, enabling acceleration of development plans

The combination of immediate cash flow generation, multiple expansion catalysts, and exploration upside creates a compelling risk-adjusted return profile for investors seeking gold sector exposure during the current bull market cycle.

West Red Lake Gold Mines represents a rare opportunity to invest in a new gold producer during a historic bull market, backed by proven management, a high-grade asset, and multiple growth catalysts. The company's systematic approach to restarting Madsen, combined with strong initial operational results and significant exploration potential, positions it as a compelling investment for those seeking leveraged exposure to rising gold prices through operational excellence rather than promotional activities.

Macro Investment Thematic Analysis

The gold bull market currently underway reflects a fundamental shift in monetary and geopolitical conditions that favor precious metals as both store of value and portfolio insurance. Central bank gold purchases have reached historic levels, with emerging market central banks leading accumulation efforts as they diversify away from dollar-dominated reserves. This institutional demand creates a structural bid for gold that supports higher price levels regardless of shorter-term market fluctuations.

Simultaneously, persistent inflationary pressures across developed economies, combined with elevated government debt levels, create an environment where real interest rates remain suppressed despite nominal rate increases. This financial repression makes non-yielding assets like gold more attractive relative to bonds offering negative real returns. The Federal Reserve's eventual pivot toward lower rates will likely accelerate gold's appeal as opportunity costs decline.

Within this macro environment, equity markets have begun recognizing the scarcity value of gold producers, particularly those offering immediate production growth. The decade-long underinvestment in new mine development during gold's bear market from 2011-2020 created a supply shortage that higher prices alone cannot quickly remedy given the multi-year development timelines for new projects.

West Red Lake Gold benefits from this scarcity by offering investors access to new production without the typical development risks and capital requirements. The company's timing appears optimal, entering production as institutional investors rotate toward gold equities and specifically favor companies demonstrating operational momentum rather than development promises. This macro backdrop suggests the valuation premium for new producers may persist longer than typical commodity cycles, providing sustained multiple expansion opportunities for companies executing successful production growth strategies.

Analyst's Notes

Subscribe to Our Channel

Stay Informed