Analyst's Notes: 2 Gold Companies. 2 Strategies. Who wins?

This week, the Analysts have chosen to focus on the performance of two gold companies (Newmont & Barrick) since the last gold super-cycle in 2011.

We are committed to helping investors, new and old, to come to grips with the resources sector and learn how to interpret news releases made by companies. In these Analyst’s Notes we illustrate how news from companies affects the investment case for the stock, and how it can affect peers as well. The topics are selected based on what the analysts think is both relevant and informative to you, the investor.

Before making comments, please ensure you have read the whole article and the FAQs at the bottom.

This week, we have chosen to focus on the performance of two gold companies since the last gold super-cycle in 2011.

Introduction

Six weeks ago, on 18 February 2021 Newmont Corporation (“Newmont”) published its production and financial performance for Q4/20. Given that it is a good length of time (about 9 years) since the previous gold super-cycle came to an end in 2011, we thought it would be a good opportunity to analyse Newmont’s financial and production history and see if any lessons could be learned. To avoid looking at Newmont’s performance in isolation, we look at Barrick Gold over the same period.

The Big Picture

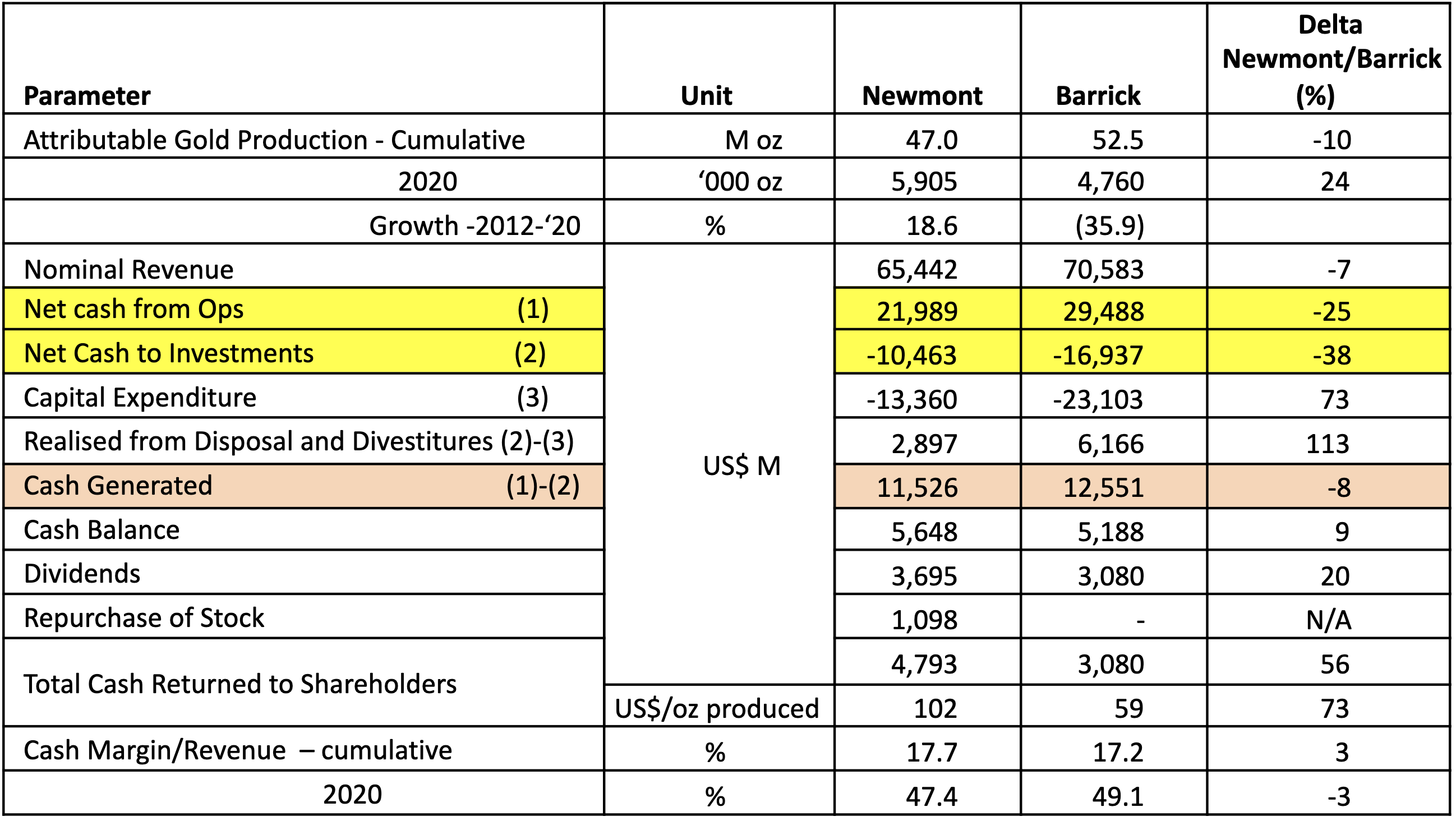

By collating 9 years of financial statements for the 2 companies we managed to produce an over-arching review and comparison, which is shown in Table 1.

Some of the more salient observations from the comparison in the table are as follows:

- Barrick produced 52.5 million ounces (“Moz”) over the 9 years, which in absolute terms is 10% more ounces than Newmont. Barrick has, however, seen a 36% fall in attributable gold production since 2012, whereas Newmont’s attributable production has grown by almost 19%. The result of these trends means that in 2020 Newmont produced 24% more ounces than Barrick, reaching almost 6Moz last year, whereas Barrick produced 4.76Moz in 2020.

- Because of its higher overall production, it is not surprising Barrick had higher cumulative cash generated from operations, but it has been more aggressive in investing to replenish depleted ounces.

- The orange highlighted cells indicate the cash generated net of investments. The amounts generated are remarkably similar for the two companies at between US$11.5Bn and US$12.5Bn. Again, Barrick made more cash from operations, but has reinvested more back in. However, the “Investment” amounts are much less than capital expenditure over the period, greatly benefiting from disposals and divestitures that are credited against capital expenditure. Barrick generated US$6.2Bn compared to Newmont’s US$2.9Bn from disposals and divestitures.

- Newmont could afford to be much more generous returning cash to its shareholders than Barrick having declared US$4.8Bn in dividends compared to Barrick’s US$3.1Bn, plus Newmont buying back US$1.1Bn worth of shares. The total cash returned to shareholders was therefore 56% higher for Newmont. It should be mentioned here that Barrick has just announced it intends to distribute US$0.75Bn in 2021 as special dividends, subject to shareholder approval.

- Expressed per ounce produced Newmont could return US$102 to shareholders compared to Barrick’s US$59.

- The cash margin expressed as proportion of revenue is remarkably similar over the life of mine being for both companies around 17.5%. However, during 2020 Barrick edged Newmont by having a margin of 49.1% compared to 47.4% for Newmont.

- Not captured in the above table are the major transactions carried out: the acquisition of Randgold by Barrick, effective 1 January 2019, and Goldcorp by Newmont, effective 18 April 2019. In both cases of the shareholders of the companies being acquired ended up holding 1/3 of the shares in the enlarged company. The effect of this is not immediately evident in the performance figures in the table, but will be evident in the dividends declared per share as we will see below.

- The transactions resulted in an increase in attributable gold production for both Newmont and Barrick of 21% compared to a year earlier.

The above conclusions are for cumulative numbers over the period and do not reveal much about trends. The next section will look into these.

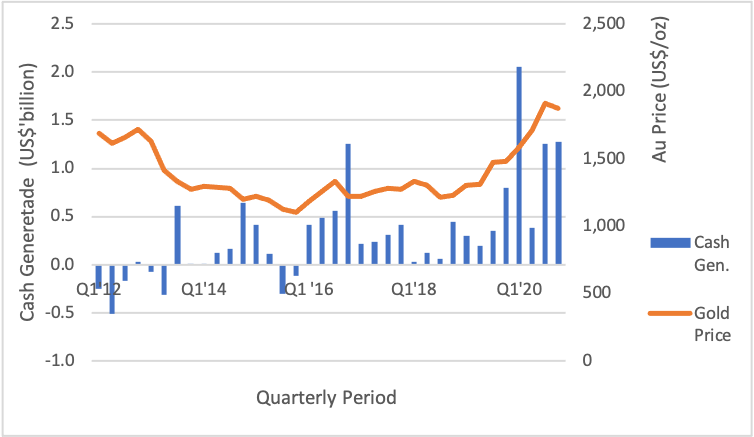

Cash Generated as Function of the Gold Price

Figures 1 and 2 have been drawn up to determine what the cash generation (before financing activities) were since 1 January 2012, plotted against the gold price. Although both companies have some by-product revenue, gold accounts for the vast majority of revenue.

The graphs show that there is a much better correlation between cash generation and gold price for Newmont than for Barrick. The explanation can be found in Barrick much more aggressively re-organising and divesting from assets and companies it no longer deemed to fit the investment criteria of the company.

Note also that 2012 and 2013, with relatively high gold prices, neither company was cash generative. This is a curious late cycle phenomena. Not only were operations not very efficient at the end of the previous gold super-cycle, but an aggressive investment attitude more than consumed whatever cash was generated by operations. The difference is very noticeable in the much higher net free cash flow numbers for 2020 when the gold price reached similar levels as in 2012.

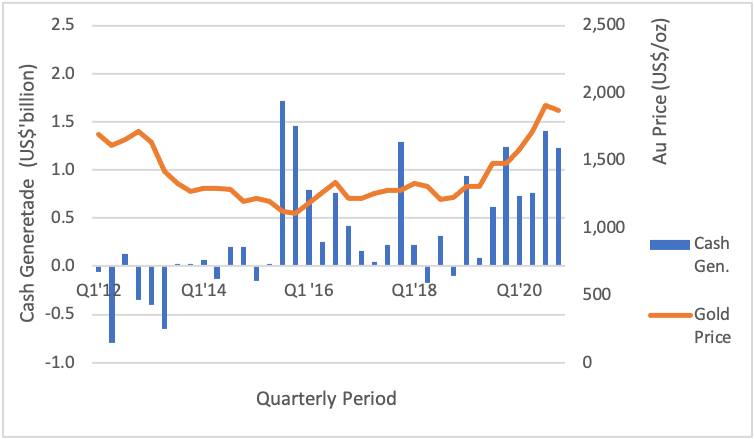

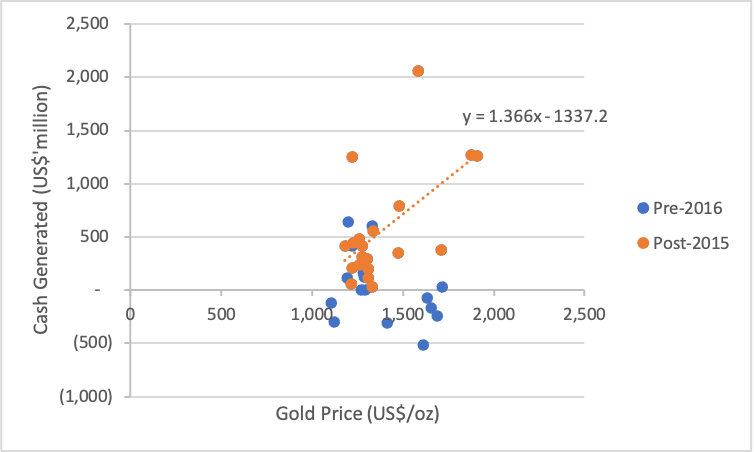

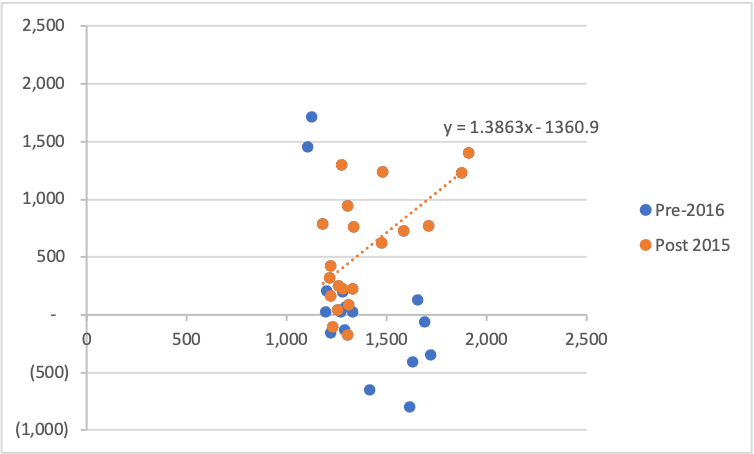

Looking at the gold graph in Figures 1 and 2, you can see that prices bottomed out in late 2015, and have been rising since then. Accordingly, we have separated the difference in cash generation efficiency of the 2 companies into 2 periods, pre-2016 (still in the downturn, blue dots), and post-2015 (in the new upturn, orange dots). Figures 3 and 4 were generated which shows the relationship of quarterly cash generation relative to the gold price.

In the period pre-2016, Newmont had quarters up to the end of 2013 that were cash negative or approximately cash neutral, despite generating US$3.9Bn from operations, reflecting the very aggressive attitude of management in seeking production growth. This attitude must have been caused by the expectation that the gold price super cycle would continue for a much longer time. During 2014 and 2015 the financial performance saw wild fluctuations with the Newmont cutting investments sharply and benefiting in certain quarters from divestitures. After 1 January 2016, cash generation shows a rough relationship to the gold price with approximately US$1.4M additional net free cash flow for each US Dollar increase in gold price.

Exactly the same pattern is evident for Barrick, but with wider fluctuations. Despite generating US$9.7Bn from operations between 1 January 2012 and 31 December 2013, net cash flow before financing activities were substantially negative at minus US$2.1Bn. During 2014 and 2015, Barrick initially broke even cash wise except for 2 large cash positive quarters in H2/15 when it disposed of a number of assets which generated US$3.2Bn during 2015 alone. After 1 January 2016, cash generation shows a rough relationship to the gold price with approximately US$1.4M additional net free cash flow for each US$/oz increase in gold price, exactly the same as for Newmont.

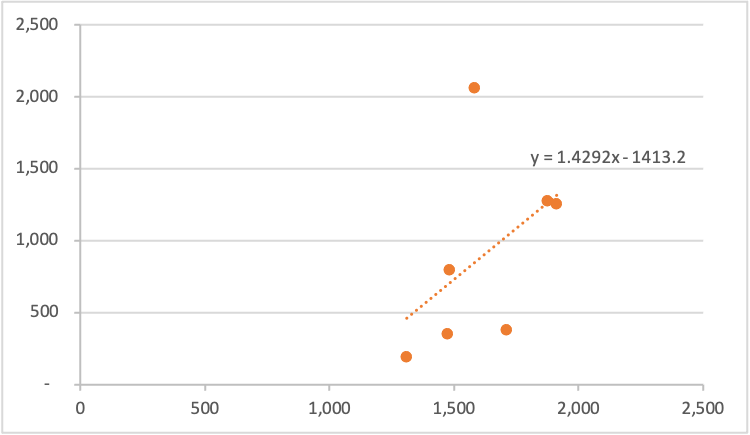

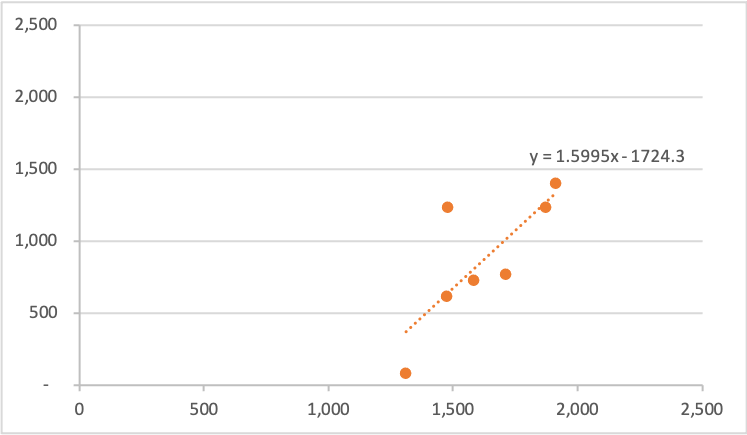

The same type of relationships as in Figures 3 and 4 have been drafted in Figures 5 and 6, but now from 1 January 2019 onwards after the major mergers were completed or almost completed.

The sensitivity of the cash generation performance has remained constant for Newmont at US$1.4M per US$/oz increase in gold price, but risen to US$1.6M for Barrick. However, the fixed cost component (the constant in the formula’s in the illustrations) has risen only slightly for Newmont, remaining at US$1.4Bn, but risen from US$1.4Bn to US$1.7Bn for Barrick.

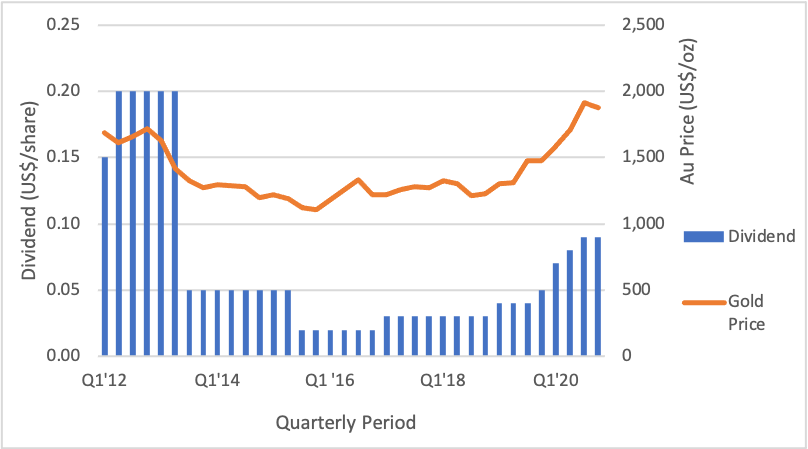

Cash Returned to Shareholders

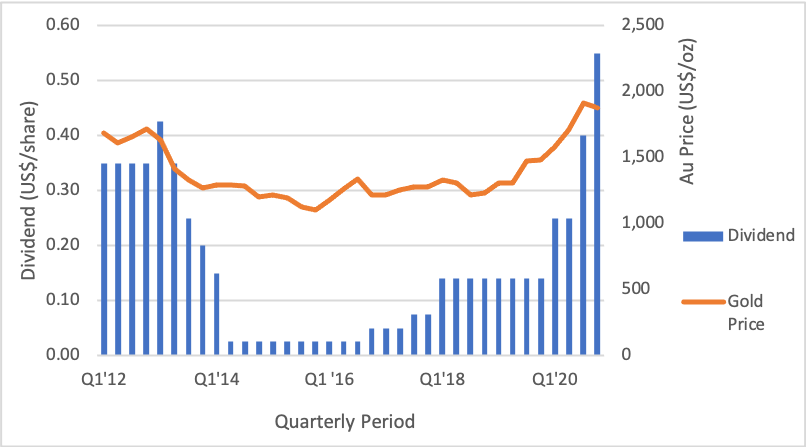

We showed in Table 1 that shareholders had more cash returned to them by Newmont than Barrick, plus they had benefited from US$1.1Bn in share repurchases. Figures 7 and 8 look at what this has meant for the dividend per share owned for each company.

It is interesting to note how both companies maintained their dividends during 2012 and 2013, even though both companies were substantially cash negative at the time.

Management was distributing dividends by doing a mixture of things. Firstly, cash balances were run down. Secondly, both companies took on debt: Newmont US$1.5Bn in 2012 and US$0.4Bn in 2013, and Barrick US$0.5Bn in 2012. Thirdly and finally, shares were issued, e.g. US$2.9Bn in 2013 by Barrick. In Q3/13 both companies started cutting dividends, Barrick more abruptly and deeper than Newmont, but the latter company eventually more drastically to a level that was 1/14th of the level in 2012.

Newmont dividend increases in recent history have been more generous than Barrick’s, exceeding 2012 quarterly dividend in Q3/20. Barrick is lagging its pre-crisis levels with dividends declared for Q4/20 at less than half of 2012 levels.

Conclusions

Both Newmont and Barrick seem to have learned from the mistakes made at the end of the previous gold super cycle and have kept cash invested well below cash generated by operations. Thus far at least! There is always the danger that management becomes ambitious as gold prices hold at current levels.

What surprised us as we did this work is that there is so little to choose between the 2 companies. Whereas Newmont seems to be better at distributing funds back to the shareholders while maintaining production, it seems as if Barrick is rapidly catching up. In terms of leverage to the gold price, Barrick seems to outperform Newmont, but Newmont has a lower fixed cost component relative to the net cash generating capacity.

As a final word, please note that this exercise has very much been a top-down review over the past 9 years. We have not done a deep dive into the relative merits of the development pipeline, or of the current management personalities. We have looked at some of the data to see what we could see, this is not a major, in-depth report on either company.

Want to hear more from the Analysts?

Are you looking for consistent returns for more confident investing? That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge, overall, all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork. Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed