AI-Driven Power Demand & the Repricing of Nuclear Fuel Markets

Uranium prices rebound to ~US$82/lb as AI-driven data center demand reshapes baseload energy economics. US policy accelerates domestic supply chains while physical funds re-engage.

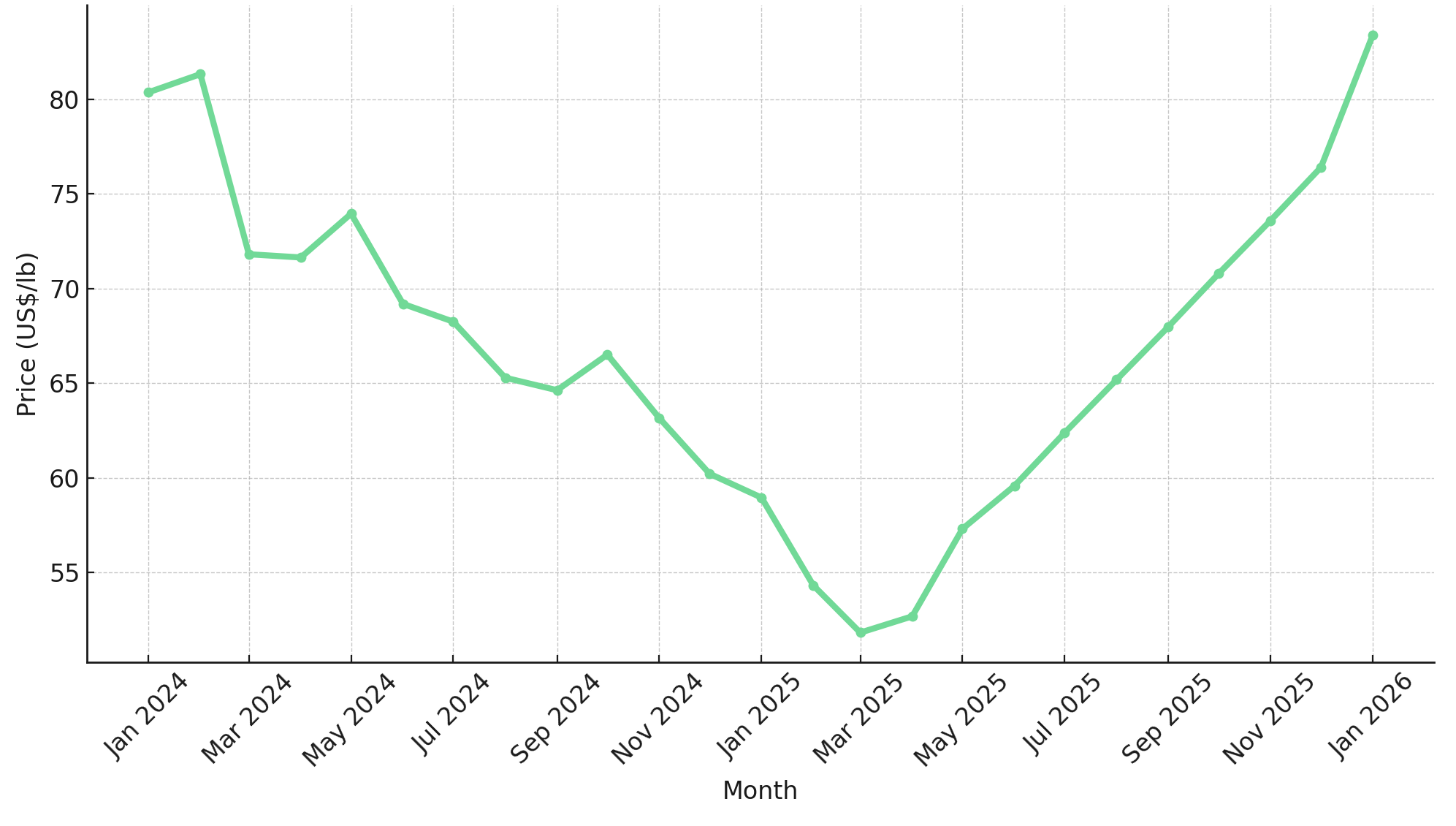

- Uranium prices have recently traded near US$82 per pound, recovering from a dip below US$76 in late November 2025 to reach multi-month highs in early January 2026, reflecting renewed confidence in nuclear energy's role in global power security.

- The artificial intelligence and data center energy buildout is emerging as a structural, not cyclical, driver of nuclear fuel demand.

- United States policy is accelerating domestic uranium supply chains through High-Assay Low-Enriched Uranium funding, regulatory easing, and reactor deployment partnerships.

- Physical uranium funds and institutional investors are re-engaging, with Sprott's physical uranium fund adding 100,000 pounds of yellowcake in late December 2025.

- Select uranium producers, developers, and explorers are positioned to benefit based on jurisdiction, asset quality, and execution readiness rather than price alone.

Uranium's Price Recovery & the Shift in Energy Market Assumptions

Uranium futures rising back to approximately US$82 per pound in early January 2026 mark more than a short-term rebound from November's pullback below US$76. The move reflects a reassessment of nuclear power's role in global energy systems, particularly as electricity demand forecasts are revised upward. Unlike previous uranium rallies driven primarily by supply disruption or financial speculation, the current recovery is rooted in structural demand visibility. Investors are increasingly linking uranium pricing to long-duration energy demand rather than marginal reactor restarts.

This repricing is occurring against a backdrop of persistently tight global uranium inventories, limited near-term mine supply elasticity, and a widening gap between long-term contracting needs and available production. Secondary supply sources that buffered the market during previous decades have largely been depleted. Utility stockpiles, government inventories, and underfeeding programs no longer provide the supply cushion that historically moderated price volatility.

For investors, the key question is no longer whether uranium prices can move higher, but what price level is required to sustain new supply investment and which companies can operate profitably within that range. The incentive price for greenfield development remains above current spot levels, suggesting that sustained price strength will be necessary to bring sufficient new capacity online to meet projected demand growth.

Artificial Intelligence, Data Centers & the Return of Baseload Energy Economics

The most consequential macro driver underpinning uranium's recent strength is the rapid expansion of artificial intelligence-driven electricity demand. Hyperscale data centers require continuous, high-load power, a demand profile poorly matched to intermittent renewables alone. These facilities require reliable baseload generation that can deliver consistent output regardless of weather conditions or time of day.

This operational reality has re-elevated nuclear energy as a scalable baseload solution, a politically acceptable low-carbon option, and a strategic asset in national energy planning. The technology's high capacity factors, long operating lifetimes, and minimal land footprint align well with the requirements of energy-intensive computing infrastructure. Major technology companies are increasingly pursuing direct power purchase agreements with nuclear facilities and investing in next-generation reactor development.

The US$80 billion contract between the United States government and Westinghouse Electric Company to build reactors supporting AI energy demand represents a turning point. It signals that nuclear buildouts are no longer speculative policy aspirations but commercially anchored infrastructure responses. For uranium markets, this shift matters because reactor commitments precede fuel procurement by several years. Many investors appear to be pricing in expectations of future contracting cycles, not just spot price movements. The structural nature of this demand shift distinguishes the current uranium cycle from previous episodes driven by supply-side disruptions or short-term financial flows.

Policy Acceleration & the Strategic Re-Localization of Uranium Supply Chains

United States energy policy is reinforcing this demand signal through direct intervention across the nuclear fuel cycle. Key developments include US$2.7 billion in Department of Energy contracts awarded to American Centrifuge Operating, General Matter, and Orano Federal Services to establish domestic High-Assay Low-Enriched Uranium supply, regulatory easing for uranium conversion and enrichment facilities, and government-backed reactor deployment partnerships. These measures address long-standing bottlenecks that previously discouraged capital investment in uranium mining and processing.

For investors, this policy backdrop shifts risk calculus in meaningful ways. Jurisdictional risk premiums compress for United States and allied projects. Permitting timelines may become more predictable under current policy frameworks, with select projects receiving Fast-41 federal permitting designation to increase timeline certainty. Strategic assets gain scarcity value independent of spot prices as national security considerations increasingly influence procurement decisions.

Energy Fuels occupies a distinctive position within this policy landscape. The company's White Mesa Mill in Utah is the only conventional uranium mill currently operating in the United States, providing strategic processing capacity at the center of domestic nuclear and critical mineral supply chains. The mill recently resumed processing, with plans to run low-cost Pinyon Plain material well into 2026. Mark Chalmers, Chief Executive Officer of Energy Fuels, frames the company's geographic advantage:

"If the United States wants to reshore the ability to be independent of China particularly on rare earth or reduce dependency on Russia, we have a facility in the United States that's constructed, permitted, and operating to do that."

This positioning extends beyond uranium into the broader critical minerals landscape. The company's rare earth separation circuit produced separated neodymium-praseodymium in 2024, with heavy rare earth oxide production capacity for dysprosium and terbium being installed for 2026.

Capital Flows & Physical Uranium Market Dynamics

The price recovery has been reinforced by renewed physical fund participation. Sprott's physical uranium fund increased its yellowcake holdings by 100,000 pounds in late December 2025. Physical accumulation matters because it removes material from the spot market, increases price sensitivity to marginal demand, and accelerates utility contracting urgency. Unlike speculative equity flows, physical fund buying directly tightens available supply, amplifying the impact of policy and demand signals.

This dynamic supports higher incentive pricing for miners and increases optionality value for projects with near-term production or restart capability. The convergence of financial flows and physical tightness creates conditions favorable to companies with operational assets capable of responding to market signals without extended development timelines. Industry participants note that utilities are now recognizing the difficulty of securing pounds and that procurement may take longer than initially anticipated.

Translating Macro Signals into Operational Execution

While uranium prices provide the macro tailwind, execution capability determines equity outcomes. Investors are increasingly differentiating between producers, developers, and explorers based on timing, cost structure, and jurisdiction. The ability to convert favorable market conditions into shareholder value depends on operational readiness and capital discipline rather than price exposure alone.

Producers: Immediate Leverage to Policy & Price

In-situ recovery operations offer particular advantages in the current environment due to their lower capital intensity, shorter development timelines, and operational flexibility. enCore Energy operates ISR production at its Rosita and Alta Mesa processing plants in South Texas, providing low-capital expenditure scalability and direct exposure to domestic policy support. William Sheriff, Executive Chairman of enCore Energy, describes the company’s production dynamics:

"Our uranium comes out of the ground quicker than most. We don't have the typical problems that you see on restarts... Your cash flow is coming in quicker but so is your need to stay ahead of that in terms of drilling and development drilling."

This accelerated production profile creates both opportunity and operational discipline requirements. The company's Dewey Burdock project has also received Fast-41 federal permitting designation, supporting development timeline visibility.

Developers: Optionality on Contracting Cycles

Advanced development companies offer leverage to higher long-term contract prices rather than spot volatility. IsoEnergy positions itself as a diversified uranium company with a dual focus: leveraging its high-grade Hurricane deposit in Saskatchewan's Athabasca Basin for mineral endowment while executing a near-term production strategy with its Utah assets, including Tony M Mine, Daneros Mine, and Rim Mine. The company is fast-tracking restart timelines for Tony M.

Explorers: Scarcity & Discovery Premium

Exploration companies offer discovery leverage as major producers seek future supply pipelines to replace depleting reserves. ATHA Energy controls large-scale land positions in Saskatchewan's Athabasca Basin, where it holds the largest land package at 3.8 million acres, and in Nunavut's Thelon Basin, where its Angilak project represents Tier-1 exploration scale. Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the company's positioning:

"We're a group that not only has discovery success and results off the drill, but from a unique perspective we're in control of an entire district... At this stage in a market, being in control of a district like we're in has us in a very good position of strength relative to the market and relative to our strategic opportunities."

The company maintains sole control of the Anjukuni basin, providing optionality that extends beyond individual discovery outcomes.

Risk Factors & Investment Considerations

Despite constructive macro signals, uranium investments remain sensitive to several variables that warrant continued monitoring. Permitting and regulatory execution risk can delay project timelines even in favorable policy environments. Timing mismatches between price signals and project financing may create capital constraints for development-stage companies. Currency exposure, geopolitical shifts, and changes in nuclear sentiment also remain relevant variables. Investors should distinguish between price optimism and project readiness when allocating capital.

The Investment Thesis for Uranium

Several factors support renewed investor attention to the uranium sector and distinguish the current market environment from previous cycles.

- Artificial intelligence-driven power demand is structurally increasing baseload electricity requirements, creating durable demand growth independent of short-term economic cycles.

- Nuclear energy is re-entering national energy strategies with direct policy backing, reducing regulatory uncertainty and compressing development timelines for domestic projects.

- Uranium supply remains constrained with limited near-term elasticity, supporting incentive pricing for new production capacity.

- Producers with operating assets benefit from immediate pricing leverage and alignment with domestic supply security initiatives.

- Developers and explorers offer asymmetric upside as contracting cycles restart and utilities extend procurement horizons.

- Jurisdictional positioning in the United States and allied nations provides regulatory stability and access to policy-driven procurement channels.

- Physical uranium fund accumulation continues to tighten spot market availability, reinforcing price support.

Uranium's Role in the Next Energy Investment Cycle

Uranium's rebound to multi-month highs reflects more than price volatility. It signals a re-rating of nuclear fuel's strategic importance within global energy systems. As artificial intelligence infrastructure reshapes power demand and governments prioritize energy security, uranium markets are transitioning from recovery to reinvestment.

The opportunity lies not in chasing spot prices, but in identifying companies with the jurisdictional advantage, operational readiness, and capital discipline to convert macro tailwinds into durable value. Selective investment across producers, developers, and explorers allows portfolio construction that balances near-term cash flow generation with longer-duration growth optionality.

TL;DR

Uranium prices have recovered to approximately US$82 per pound in early January 2026, driven by structural shifts rather than speculation. AI and data center expansion is creating sustained baseload power demand that favors nuclear energy. The US$80 billion Westinghouse reactor contract signals nuclear buildouts are now commercially anchored infrastructure responses. US policy is accelerating domestic uranium supply chains through HALEU funding and regulatory easing. Physical uranium funds like Sprott are tightening spot market supply. Investors should focus on companies with jurisdictional advantage, operational readiness, and execution capability rather than price exposure alone. Producers, developers, and explorers each offer distinct risk-reward profiles within this macro environment.

FAQs (AI-Generated)

Uranium prices rebounded to approximately US$82 per pound due to structural demand visibility from AI-driven electricity requirements, persistently tight global inventories, limited near-term mine supply elasticity, and renewed physical fund buying. Secondary supply sources that historically buffered the market have largely been depleted.

Hyperscale data centers require continuous, high-load baseload power poorly matched to intermittent renewables alone. Nuclear energy's high capacity factors, long operating lifetimes, and reliable output align with energy-intensive computing infrastructure needs, driving technology companies toward nuclear power purchase agreements.

The Department of Energy has awarded US$2.7 billion in contracts to establish domestic High-Assay Low-Enriched Uranium supply. Additional measures include regulatory easing for conversion and enrichment facilities, government-backed reactor partnerships, and Fast-41 federal permitting designations for select uranium projects.

Physical uranium funds like Sprott's remove material from the spot market, increasing price sensitivity to marginal demand and accelerating utility contracting urgency. Unlike speculative equity flows, physical buying directly tightens available supply, amplifying policy and demand signals.

Key risks include permitting and regulatory execution delays, timing mismatches between price signals and project financing, currency exposure, geopolitical shifts, and changes in nuclear sentiment. Investors should distinguish between price optimism and actual project readiness when allocating capital.

Analyst's Notes

Subscribe to Our Channel

Stay Informed