Nuclear Energy Summit Signals Long-Term Demand Growth: Global Nuclear Policy Coordination and Uranium Market Expectations

The March 2026 Nuclear Energy Summit formalized commitments to triple global nuclear capacity by 2050, reshaping uranium markets and supply chain strategies.

- Global nuclear policy coordination reached a new threshold at the March 2026 Nuclear Energy Summit in France, where governments formally endorsed a declaration to triple nuclear energy capacity by 2050, establishing one of the clearest long-term demand signals the uranium market has seen in decades.

- Electricity demand driven by artificial intelligence infrastructure, data centers, and broader electrification is reshaping how governments and utilities evaluate baseload power, with Small Modular Reactors emerging as a scalable solution for energy-intensive industries.

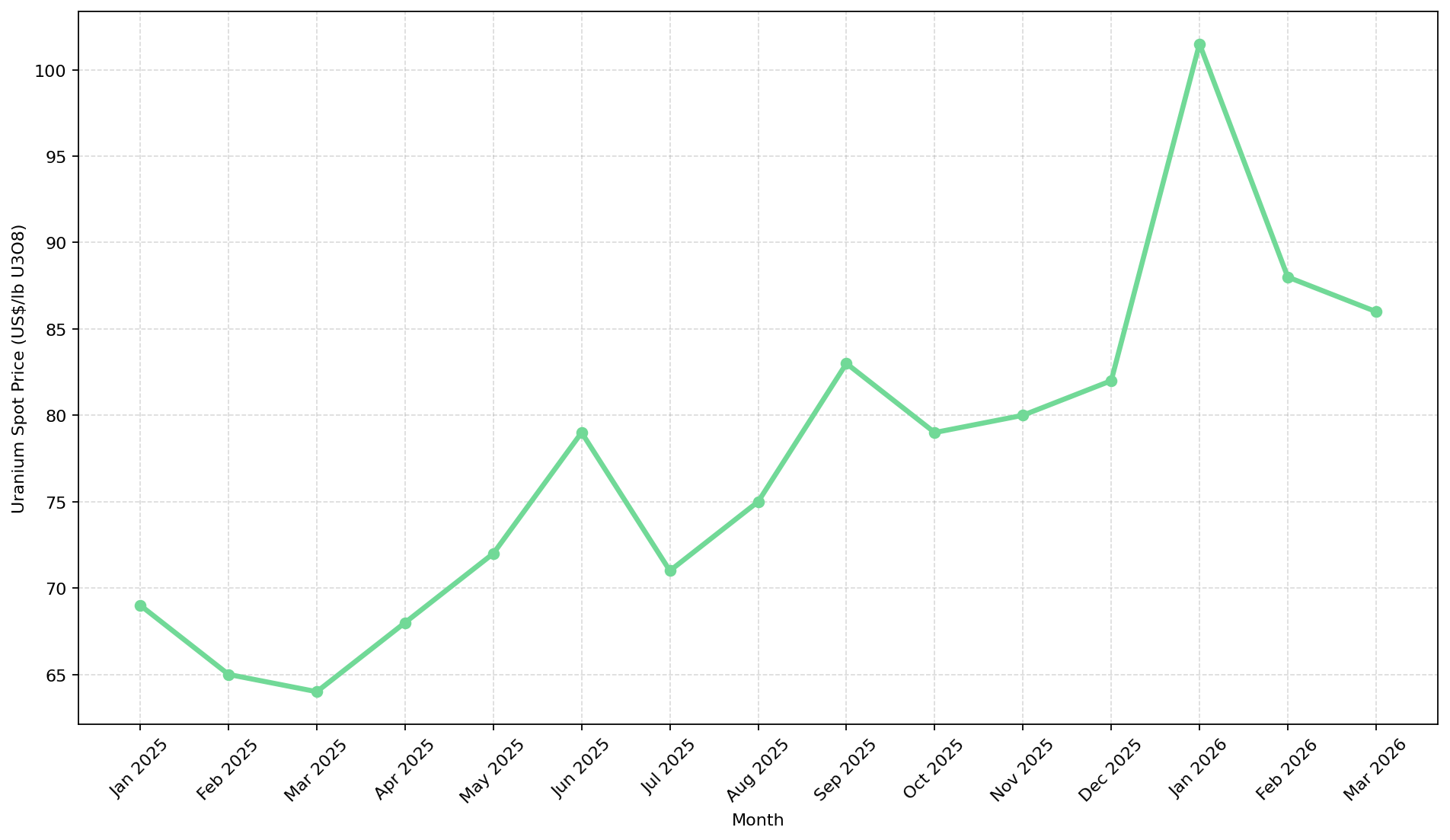

- Uranium spot prices declined from $101.50/lb in January 2026 to approximately $85.90/lb by mid-March, a movement driven primarily by unexpected supply increases from Uzbekistan rather than any deterioration in long-term demand fundamentals.

- The US Department of Energy awarded $2.7 billion in contracts in January 2026 to rebuild domestic uranium enrichment capacity over the next decade, creating jurisdictional advantages for producers operating within allied supply chains.

- Across the uranium development pipeline, companies ranging from conventional producers to in-situ recovery operators and development-stage explorers are positioning for the demand cycle expected to emerge as reactor construction timelines solidify.

The Nuclear Energy Summit & Its Position in the Policy Cycle

The March 2026 Nuclear Energy Summit, organized by the French Ministry of Europe and Foreign Affairs, represented the most coordinated expression of political support for nuclear energy in at least two decades. Governments formally endorsed a declaration to triple global nuclear energy capacity by 2050.

Nuclear fuel procurement operates on 3- to 10-year contracting cycles, meaning utilities make purchasing commitments years before the fuel is consumed. A policy signal today - a reactor extension, a new build approval, a strategic reserve mandate - does not increase uranium demand this quarter. It shifts the volume of long-term contracts utilities will need to place over the next several years, which is what moves the term price and the investment case for producers holding uncontracted pounds.

Three conditions have changed how governments classify nuclear power.

- Geopolitical disruptions to energy supply have made baseload reliability a security question rather than an economic one.

- Decarbonization targets have narrowed the list of technologies capable of delivering large-scale, dispatchable, zero-emission power, and nuclear is on that list where it was previously excluded from policy frameworks.

- Electricity demand from data centers, AI infrastructure, and electrification is growing faster than grids can absorb variable renewable generation alone.

Each of these conditions pushes toward the same policy conclusion: nuclear capacity is now treated as critical infrastructure, and that reclassification affects the regulatory and financing environment in which uranium producers and developers operate.

Electricity Demand Growth & the Structural Case for Nuclear Baseload

One of the central discussions at the summit focused on the acceleration of global electricity consumption. Data centers, artificial intelligence training workloads, and cloud computing infrastructure are placing pressure on electricity grids in North America and Europe at a pace that planning assumptions have not fully absorbed. Unlike wind and solar generation, which are intermittent by nature, nuclear reactors provide continuous baseload power, a characteristic increasingly valued by technology companies evaluating long-term energy procurement.

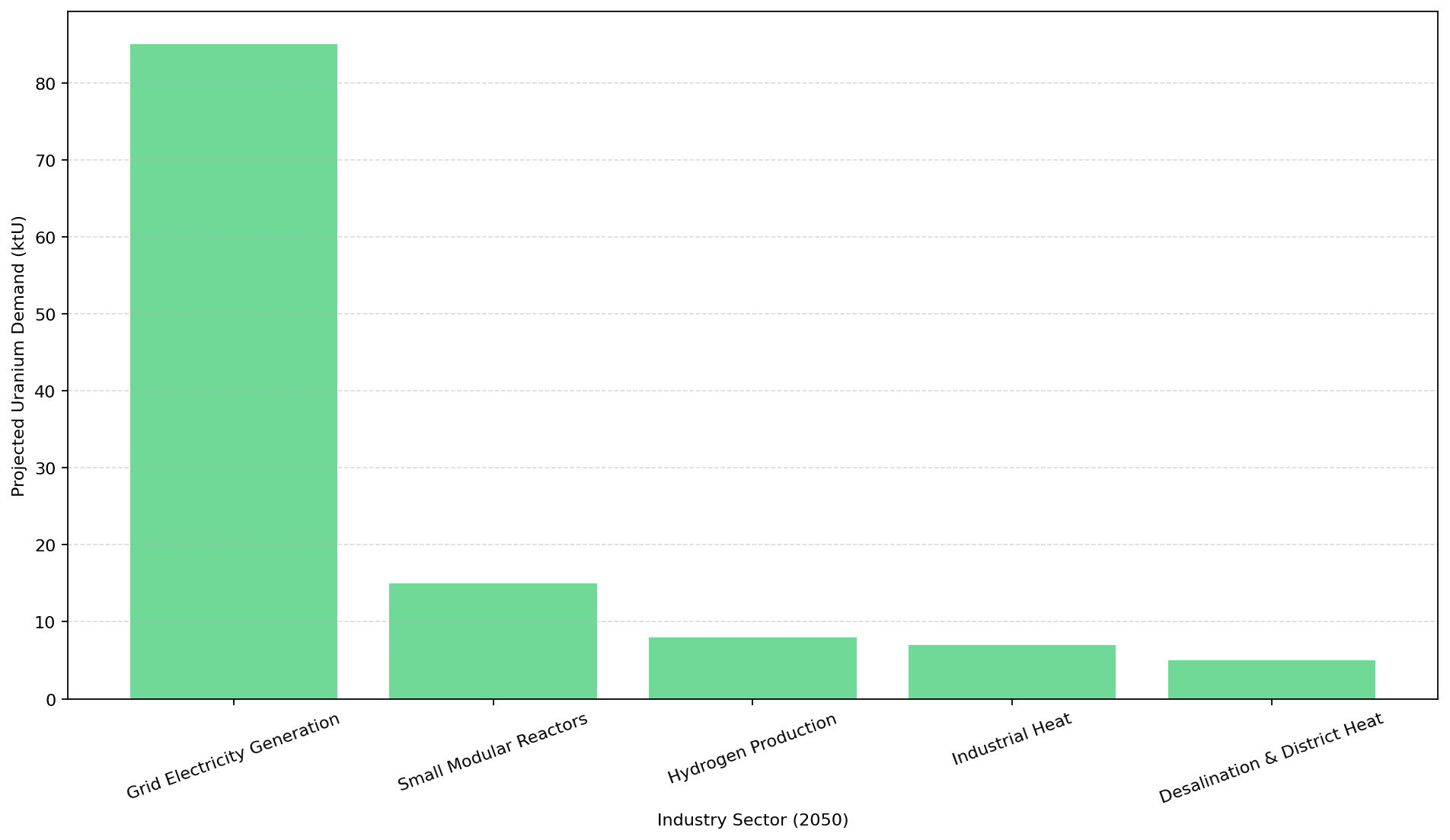

Small Modular Reactors are receiving particular attention as a scalable solution for energy-intensive industries. Small Modular Reactors are compact nuclear reactors designed with standardized components to allow factory manufacturing and shorter construction timelines than conventional large-scale plants. Demand for uranium may eventually be tied not only to national climate policy but also to private sector infrastructure expansion, broadening the demand driver base beyond what utility procurement cycles alone could generate.

If technology companies and industrial users become direct or indirect contributors to nuclear fuel demand, the contracting structures governing the uranium market may evolve, creating additional pressure on producers to demonstrate long-term supply reliability and jurisdictional stability.

Uranium Price Dynamics & the Gap Between Policy & the Spot Market

Despite the strong policy signals emerging from the summit, uranium prices have moved in the opposite direction in recent months. The spot price reached $101.50/lb in January 2026 before declining to approximately $85.90/lb by mid-March. The primary driver was an unexpected increase in uranium production from Uzbekistan, which added supply to the market and temporarily eased tightness that had been building through 2025.

This illustrates a structural feature of uranium markets that institutional investors monitor carefully: short-term prices are driven primarily by supply changes and near-term contracting activity, while policy developments influence longer-term demand expectations. The near-term price environment reflects a market absorbing recent supply additions, while longer-term demand expectations remain supported by reactor commitment programs.

Western Supply Chain Restructuring & Jurisdictional Positioning

Another theme from the summit was the restructuring of the nuclear fuel supply chain across Western economies. Following sanctions on Russian nuclear fuel processing, governments in North America and Europe have committed significant capital to rebuilding domestic conversion and enrichment capacity. In January 2026, the US Department of Energy awarded $2.7 billion in contracts to three companies to rebuild domestic uranium enrichment capacity over the following decade, alongside expanded support for uranium conversion infrastructure.

These investments are creating strategic advantages for uranium companies operating in Western and allied jurisdictions. The United States, Canada, and Australia are increasingly positioned as priority supply sources for utilities seeking to reduce exposure to geopolitically sensitive fuel chains, though this positioning remains subject to sustained policy support and permitting conditions in each jurisdiction.

Energy Fuels operates the White Mesa Mill in Utah, the only operating conventional uranium mill in the United States. Beyond uranium, the facility is advancing a rare earth processing program: Phase 1A commercial capacity is in place to process up to 10,000 tonnes per annum of monazite and produce up to 1,000 tonnes per annum of light rare earth oxides. Phase 1B and Phase 2 expansions, targeting mid and heavy rare earth oxide commercialization, are planned for mid-2027. Mark Chalmers, Chief Executive Officer, describes the Energy Fuels’ broader strategy:

"We're building a critical mineral hub focused in Utah around our White Mesa Mill and built around our uranium business... We're looking at integration in the rare earth cycle, and that's what the world needs because the Chinese have integration from mining right on through to electric vehicles."

The company announced in January 2026 a proposed acquisition of Australian Strategic Materials, which holds metals and alloys production capabilities in South Korea and plans to expand into the United States. Mark Chalmers describes the rationale:

"We identified that we wanted to have the metals and alloys capability, which are very short in supply globally. We saw ASM with those capabilities in South Korea and a plan to expand into the United States, we're going to grab it, and that's what we've done."

In-Situ Recovery & Scale Dynamics in US Uranium Production

In-situ recovery (ISR) has become the dominant extraction method globally, accounting for approximately 60% of worldwide uranium output. ISR involves injecting a solution into a uranium-bearing aquifer, dissolving the uranium, and recovering it at surface facilities, a process that typically requires significantly lower capital expenditure and shorter reclamation timelines than conventional mining.

enCore Energy operates ISR uranium projects in Texas, with production currently underway at both the Alta Mesa and Rosita central processing plants. Alta Mesa commenced operations in the second quarter of 2024. William Sheriff, Executive Chairman of enCore Energy, frames the scale imperative for ISR producers:

"In terms of the ISR business, you're going to have some producers that produce more than a million pounds a year or you're going to be essentially running a mom and pop grocery store on the corner. You've got to get some size, your credit ratings go up, so your cost of capital goes down."

The company also holds a significant land and resource position in New Mexico. William Sheriff describes the district-scale opportunity:

"There's around 80 million pounds of resources there and four large deposits, and a whole host of mineral rights scattered across New Mexico, something on the order of 400 square miles... Having that large array of property, we have over 50% of the seventh largest uranium district in the world under control."

enCore's proprietary data position, built through the consolidation of exploration records from multiple predecessor companies that operated across its New Mexico acreage, reduces exploration risk and supports future resource development decisions in the district.

High-Grade Resource Scarcity & Development Pipelines

While production-stage companies respond to near-term supply opportunities, development-stage operators are positioning for the demand phase expected to emerge later this decade. High-grade uranium deposits are geologically rare, and scarcity of supply from established districts such as Canada's Athabasca Basin has historically been a key driver of project valuation.

IsoEnergy is developing Hurricane Deposit in the Athabasca Basin, which hosts an indicated resource of 48.6 million pounds of U3O8 grading 34.5%, as established in an NI 43-101 compliant technical report effective July 2022. Philip Williams, Chief Executive, characterizes Energy’s asset:

"Hurricane is the highest grade uranium resource in the world. We made a discovery in 2018, put a resource out in 2022, 34.5% grades, 48.6 million pounds."

ATHA Energy controls more than 7 million acres of exploration land in Canada, including the Angilak Project, which hosts the historical Lac 50 deposit. ATHA's land position represents the exploration end of the uranium development spectrum, where capital is deployed to define resources that may eventually underpin future production decisions. Projects at this stage carry higher geological risk but offer meaningful optionality if resource delineation advances during a period of strengthening long-term uranium demand.

Beyond traditional uranium districts, Atomic Eagle is advancing the Muntanga Project in Zambia's Karoo Basin, which hosts 47.4 million pounds of U3O8 resources. The project features shallow open-pit mining potential with conventional processing, and technical studies indicate recovery rates above 90%. Muntanga illustrates a broader trend toward geographic diversification in the uranium supply chain, as utilities and governments seek to reduce dependence on a concentrated group of producing jurisdictions.

The Investment Thesis for Uranium

- Long-term demand visibility is supported by formal government commitments to triple global nuclear capacity by 2050, establishing a policy-driven demand signal that extends well beyond current utility contracting cycles.

- Western supply chain realignment is creating jurisdictional advantages for uranium producers operating in the United States, Canada, and Australia, supported by direct government investment in domestic enrichment and conversion infrastructure.

- High-grade deposit scarcity, particularly in the Athabasca Basin, creates resource scarcity value for development-stage companies holding tier-one assets, with grade and contained pounds acting as primary valuation anchors.

- ISR production economics offer lower capital intensity and shorter development timelines relative to conventional mining, improving risk-adjusted returns for producers operating at scale in established US uranium districts.

- Electricity demand growth from artificial intelligence infrastructure and data center expansion is broadening the demand base for nuclear power beyond utility procurement cycles, potentially introducing new contracting structures and timelines.

- Vertical integration across the nuclear fuel cycle, from uranium mining through rare earth and metals processing, is emerging as a distinct strategic premium for companies operating in Western jurisdictions seeking to reduce import dependence.

The March 2026 Nuclear Energy Summit does not alter uranium supply or demand in the near term. What it does is clarify the direction of long-term policy, confirming that nuclear power has moved from the periphery of energy planning to a central position in how governments are approaching decarbonization and energy security simultaneously. The relevant question is not whether prices respond immediately to policy signals, but whether the commitments made in France eventually translate into reactor construction programs and the long-term fuel contracting cycles that follow. The supply chains being built today and the resource positions being established across allied jurisdictions represent the foundation on which that next demand cycle, if it materializes, will depend.

TL;DR

The March 2026 Nuclear Energy Summit in France produced a formal declaration to triple global nuclear capacity by 2050, marking the strongest coordinated policy signal for uranium demand in decades. Despite this, spot uranium prices fell from $101.50/lb in January to $85.90/lb by mid-March due to unexpected Uzbekistan supply increases, a reminder that short-term prices respond to supply changes while long-term demand is shaped by policy. Western governments are restructuring nuclear fuel supply chains away from Russian dependence, with the US committing $2.7 billion to domestic enrichment. High-grade deposit scarcity, ISR production economics, and AI-driven electricity demand are reinforcing the structural case for uranium exposure across the development pipeline.

FAQs (AI-Generated)

Governments formally endorsed a declaration to triple global nuclear energy capacity by 2050. Organized by the French Ministry of Europe and Foreign Affairs, the summit represented the most coordinated political endorsement of nuclear power in at least two decades, reaffirming nuclear's role in both decarbonization strategy and energy security policy.

The price decline from $101.50/lb in January 2026 to approximately $85.90/lb by mid-March was driven primarily by an unexpected increase in uranium production from Uzbekistan, which added near-term supply to the market. Policy developments influence long-term demand expectations, while short-term prices respond to supply changes and near-term contracting activity — the two operate on different timelines.

Following sanctions on Russian nuclear fuel processing, the US Department of Energy awarded $2.7 billion in contracts in January 2026 to rebuild domestic enrichment capacity. Producers operating in the United States, Canada, and Australia are increasingly positioned as priority supply sources for utilities seeking to reduce exposure to geopolitically sensitive fuel chains.

Small Modular Reactors are gaining attention as a scalable baseload solution for energy-intensive industries, particularly data centers and AI infrastructure. Unlike large conventional plants, SMRs are designed with standardized components for factory manufacturing and shorter construction timelines, potentially broadening uranium demand beyond traditional utility procurement into direct private-sector energy procurement.

High-grade deposits are geologically rare, and the Athabasca Basin in Canada is one of the few districts capable of hosting them at scale. Assets such as IsoEnergy's Hurricane Deposit — grading 34.5% U3O8 with 48.6 million indicated pounds — carry scarcity value that underpins project valuations independent of near-term spot price movements, with grade and contained pounds acting as primary valuation anchors.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed