Almaden Minerals (AMM) - Gold-Silver Adrenaline Boost

Almaden Minerals (AMM) - Gold-Silver Adrenaline Boost

Poliquin is an honest, polite, intelligent, meticulous and amiable guy, without a promotional bone in his body. He and his team have patiently been exploring and developing their Ixtaca project for 10 years. This timescale is perhaps the root of Almaden Minerals' issues.

This is now a good project but one the market has forgotten about. It needs an injection of adrenaline. Maybe, it needs one of the things I hate most about this industry, that 'Vancouver-style promoter,' to get it noticed again. The alternative would be for Poliquin to focus on being a COO by bringing in a seasoned CEO with connections to the financial markets and the ability to shine a promotional light on the company. That might jar somewhat for Poliquin; he has been leading this project for 10 years, but it might just be the smartest thing he can do.

Almaden Minerals, which went public back in 1986, is a Mexican gold-silver exploration company. The company is based on the project that they found in 2010, and this decade has been far from an easy ride for the mining junior.

Matthew Gordon talks to Morgan Poliquin, 18th July 2020

A stagnant share price and lacklustre trading volumes are evidence that investors have become bored with this gold-silver story that is 10 years in the making. It is far from firing on all cylinders. However, if investors are to look a little bit deeper into this value proposition, there are some areas of genuine merit.

Almaden Minerals' flagship Ixtaca Gold-Silver Deposit is one of Mexico’s more promising precious metal discoveries. Discovered by Almaden in 2010, drilling programmes have outlined a multimillion ounce deposit. A Feasibility Study has been completed, and the company is now focussed on taking the project into production.

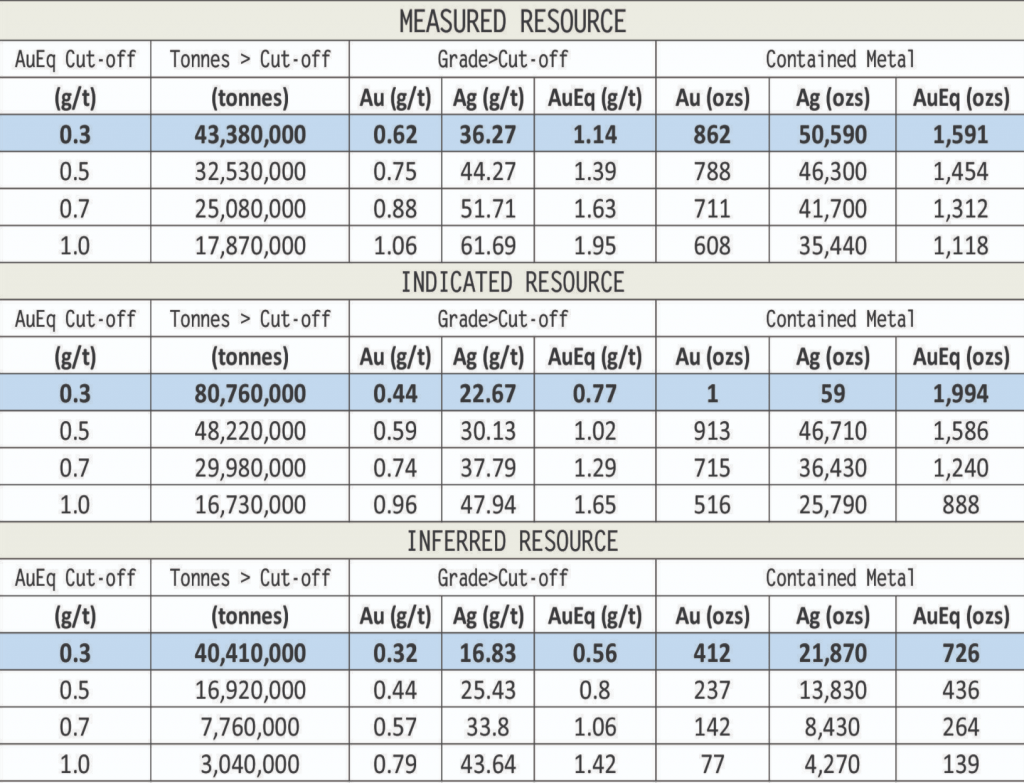

A 2018 Feasibility Study demonstrated some really encouraging numbers. Let's start with the 43-101 measured resource:

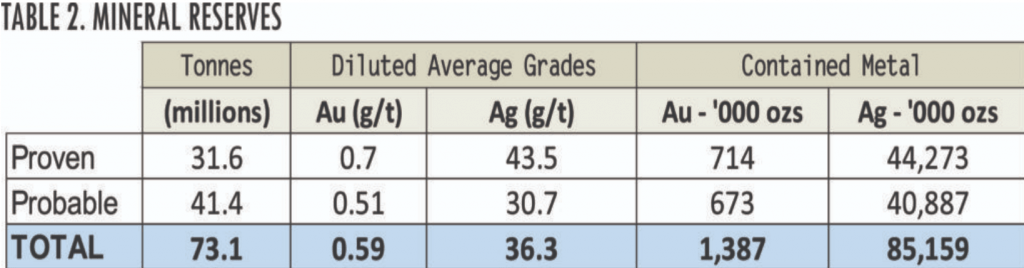

And then the mineral reserve estimate:

What are the headline figures using a US$1,275/oz gold price and US$17/oz silver price, with equivalency calculations assuming a 75:1 silver:gold ratio?

- Average annual production: 108,500oz gold and 7.06Moz silver (203,000oz AuEq) over the initial 6-years of production. This moves Almaden Minerals closer to becoming an established mid-tier gold producer.

- Average LOM annual production: 90,800oz Au and 6.14Moz silver (173,000oz AuEq).

- After-tax NPV(5%): US$310M and an internal rate of return of 41%.

- After-tax IRR: 42% with an after-tax payback period of 1.9-years.

- CAPEX: US$174M.

- Slightly reduced average annual production over the first 9-years of 88,780oz Au and 5.47Moz silver (168,100oz AuEq).

- Conventional open-pit mining methodology.

- Proven and Probable Mineral Reserve: 1.39Moz gold and 85.2Moz silver.

- Operating cost: US$716/oz AuEq.

- AISC: US$850/oz AuEq.

- Use of filtered tailings removes the tailings dam and reduces the environmental footprint.

I've seen companies with numbers like this that are valued 4x more by the market. A significant discount is being applied here, so investors may want to investigate further. The fact that Almaden Minerals has been cited in a lawsuit against the Mexican government by an NGO protesting a mining law, alongside the protracted development of the project, has not helped matters. Investors are also a little confused by the recovery rates for gold & silver projects in this type of open-pit structure with a variety of different ores to process: limestone, black shale and volcanic. What is the identity of this project? Is it high-grade or low-grade? It is now Poliquin's job to get out there and start telling the story in a resonant fashion or he will need to get a CEO in who can deliver results.

Since 2010, the company has spent c. US$40M to go from initial discovery to the Feasibility/permitting stage. That's a lot of exploration drilling! However, a lot of value has not been unlocked.

Having just raised C$2M in the "darkest week of coronavirus in March," i.e. expensive money, the company has around C$3M in the treasury to "wait out" this permitting stage. There is a lot of uncertainty surrounding Mexico in general terms, and investors will be concerned that this mining jurisdiction could be a potential permitting sticking point. In the meantime, the company will be pursuing new possible optimisations like using its limestone waste as cement feed.

The fundamentals look intriguing, but the many risk and sentiment factors in play mean that this is a project I'll need to hear more about before getting too excited.

Company Website: https://almadenminerals.com/

Analyst's Notes

Subscribe to Our Channel

Stay Informed