Bannerman Energy (BMN) - Large Scale, Robust Economics & Near Production

Matthew Gordon spoke to Brandon Munro, CEO and MD of Bannerman Energy.

Bannerman Energy Ltd. is an Australian-listed uranium development company. The company’s flagship asset is the Etango Project, one of the world’s largest undeveloped uranium assets. The project is located in the highly established uranium mining jurisdiction of Namibia, where the company has environmental permits in place for development. The Etango Project has been strongly de-risked through extensive drilling, technical evaluation, and operation of a process demonstration plant facility.

Matt Gordon caught up with Brandon Munro, CEO and Managing Director, Bannerman Energy. Brandon has over 20 years of experience as a corporate lawyer and resources executive, including as Bannerman’s General Manager between 2009-2011. He was appointed the company’s CEO in 2016. He lived in Namibia for over five years between 2009-2015, where he also served as Governance Advisor to the Namibian Uranium Association, Strategic Advisor- Mining Charger to the Namibian Chamber of Mines, and Trustee of Save the Rhino Trust Namibia, a high profile Namibian NGO.

Brandon is a prominent thought leader within the uranium sector. He has served as Co-Chair of the World Nuclear Association’s Nuclear Fuel Demand working group. He has also been an expert contributor on uranium to the UN Economic Commission for Europe. Brandon’s voluntary service includes board roles in the conservation, arts, and education sector.

Company Overview

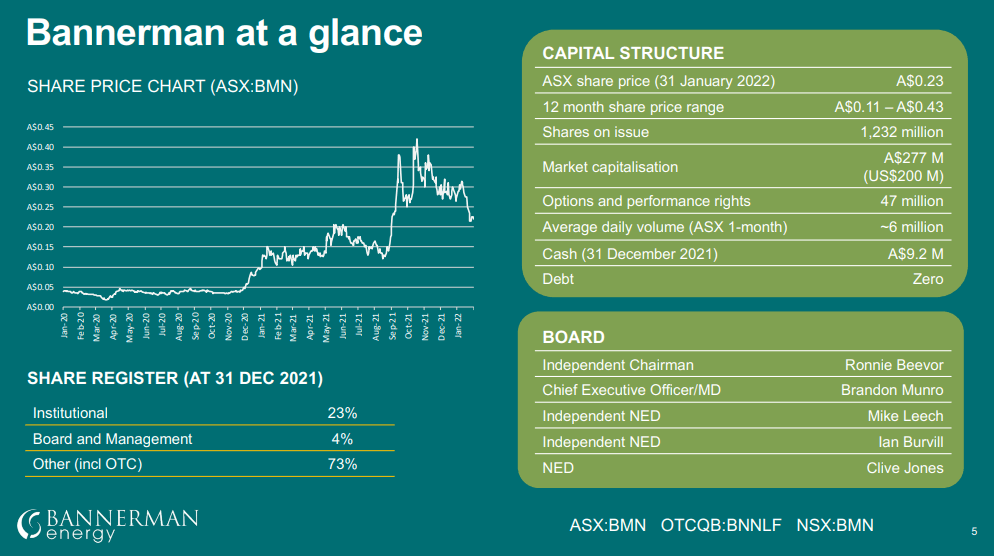

Bannerman Energy is a uranium development company that is established as an ESG (Environmental, Social, and Governance) leader within Namibia, and the global uranium sector. The company exercises best-practice governance in all aspects of its business. The company was founded in 2005 and is based in Subiaco, Australia. It is listed on the Australian Stock Exchange (ASX: BMN), the OTC Markets (OTCQB: BNNLF), and the National Stock Exchange (NSX: BMN).

Bannerman boasts a skilled management team led by CEO Brandon Munro, with extensive experience in uranium project development. The team will leverage Namibia's 45+ years of uranium production experience and well-trained local workforce during Etango's development and operations. This provides further confirmation of Namibia as an ideal jurisdiction for uranium mining.

Bannerman Energy's key asset is the Etango uranium project located in Namibia. With 220 million pounds of uranium resources, Etango has an initial 15-year mine life with low operating costs projected to be around $35/lb based on its definitive feasibility study. The project economics are attractive at current uranium prices and have additional leverage to further increases in the uranium price. Etango has also received its key environmental approvals from the Namibian government and has submitted its mining license application, significantly de-risking the development timeline.

On the financing side, Bannerman holds a strong cash position with $40 million available and no debt. This is sufficient to fully fund Etango through the construction phase to initial production. With existing cash reserves, Bannerman is able to self-fund the project without needing to raise additional capital in the near term. This provides flexibility in timing project development to match market conditions.

The Uranium Market

The uranium market has been highly volatile in recent times but at the recent COP28 climate summit, the U.S., Canada, France, Japan and the U.K. pledged $4.2 billion to develop a reliable global nuclear supply chain free from Russian dependence. This supports the goal set by 22 countries last week to triple nuclear capacity by 2050, which is key for achieving net-zero emissions. Meanwhile, uranium prices hit $81 per pound last week, their highest level since 2008, sparking investor interest. This price surge, predicting a sector rally, stems from a tightening spot market over the past few years as inventory drawdowns during the pandemic forced producers to the spot market. With nuclear newly recognized by Europe as sustainable and critical for climate goals, coordinated government investments to enhance enrichment capacity signal nuclear power’s growing prospects despite past opposition. If prices remain high amid rising demand, increased nuclear capacity could sustain the uranium market rally.

Operating in Namibia

According to Bannerman Energy, Namibia often has a misunderstood perception from the outside world. Namibia is a safe, secure, stable, and supportive country in Africa.

Namibia has had significant developments in the uranium space over the past 15 years. These include the Langer-Heinrich and the Husab Uranium Mine. In fact, Namibia has a decades-long history of exporting uranium. The country has a deep water port, a supportive jurisdiction. Additionally, the country also offers an indigenous workforce that has been brought up by the Rössing Uranium Mine that was initially run by Rio Tinto.

Notably, Majors in the mining space have previously operated in Namibia. It is a superior place for both investing and development. Compared to the first-world jurisdictions, the country offers development stability, government and community support along with political and environmental support in the uranium space.

Namibia offers a pragmatic environmental framework where the development agenda is supportive as long as companies are willing to comply with the world-class environmental standards. As long as the companies meet these standards, their work isn’t interrupted as it is often seen in other parts of the world.

According to Bannerman Energy, people often hold a similar perspective for Namibia as other countries in the African continent. In fact, Namibia is as good a place to invest as Canada, Australia, or the US.

Market Fundamentals

The global consumption for nuclear power reactors and new reactors approaching production is estimated at 175Mlbs of U3O8 (Triuranium Octoxide) in its equivalent nuclear fuel forms.

By comparison, the baseline global production for uranium is 135Mlbs, while the secondary supply is 25Mlbs. The secondary supply includes the recycled uranium retrieved from spent nuclear fuel by a process called underfeeding. The secondary material includes the limited government reduction supply. There’s a significant gap in the supply and demand for uranium.

The market has seen the impact of secondary demand from the physical investment funds. The major funds for physical uranium include the Sprott Physical Uranium Trust (SPUT), Yellow Cake, and the newly announced ANU Energy, a Kazakh-based physical investment fund. Additionally, hedge funds and other HNW (High-net-worth individual) family office investors have directly invested in uranium.

It is important to note that the commercial inventories carry a limited supply capacity. These are developed to address the deficit and the rising prices in the market. Additionally, these commercial inventories provide a competitive buying opportunity for financial investors in the form of SPUT and Yellow Cake. The utilities are looking to maintain the supply buffer going forward.

Covid has posed challenges when it comes to conducting business. It is expected that the physical uranium reserves will seek to replenish inventories.

Bannerman Energy anticipates that the demand for uranium will continue to grow. The demand is projected to grow at a rate of 2% per annum. This comes at a time when the uranium supply is projected to deplete significantly by the end of the decade.

The company forecasts that out of the top 10 uranium mines in the world, 3 of them will be closed or will run out of ore by the year 2030. These market conditions are a catalyst for a very late-stage advanced developer such as Bannerman Energy to deliver.

Company History

Bannerman Energy initiated resource drilling in 2006, followed by environmental baseline studies in 2008. These studies were planned for the original Etango project that had an annual production capacity of 7.2Mlb per annum. The company concluded a DFS (Definitive Feasibility Study) on the Etango Project in 2015.

Notably, a 7.2Mlb yearly supply can power 17-18 gigawatt-scale nuclear reactors. The company realised back then that the project is too big to carry out without a significant off-take partner. The company was looking to retain its independence in the marketplace for selling its product. At the same time, the company was being told by the equity market that its goals were too ambitious.

The Etango project had a huge CapEx (Capital Expenditure) that was relative to the project’s size. However, it was significantly bigger than the company’s market cap. Due to these factors, the company decided to reduce the scale of the project while maintaining scalability for the future. It planned to generate a 3.5Mlb yearly supply with an option to scale up operations once the market conditions were favourable.

Bannerman Energy’s Etango project is still among the largest prospective developers in the uranium space. In fact, it can sufficiently service 7-8 conventional nuclear reactors.

The Etango project features really good economics and improvements on a large scale. These are a result of a low-strip ratio along with an orebody that starts at the surface. The project has a large mine with a 15-year mine life. As per the company, the project has had a 50Mlb supply extracted so far. The mine has the potential to go deeper, which can lead to the extension of the mine life beyond 15 years. The company is planning to work towards a 200Mlb global resource along with satellite deposits that are located within trucking distance.

The company is currently in the process of completing its DFS. It has a strong technical steering committee that features one of the people who built the largest mine in Africa and was involved in numerous different Namibian projects.

The company also has Rössing Uranium Mine’s former Managing Director on the technical steering committee. The company has the right people in the right place to control the budget and timeframe to help achieve the desired outcomes.

As per the company, it is important to look at various aspects when analysing a project that features low grades. It is important to note the differences between an underground mine with low grades and a conventional open pit that has low grades. Although Namibia has some of the lowest grades of uranium in the world, companies have been able to develop profitable operations.

For instance, the Rossing Uranium Mine in Namibia has been able to operate for over 45 years despite the dips and the peaks within the uranium sector. The mine was still in operation when uranium was trading at $8/lb.

The Etango Project features low grades, but it’s an open pit with a very low stripping ratio of 2. The project has straightforward metallurgy along with outcrops at the surface. The material can be extracted through a conventional acid heap leaching operation. The extraction can be achieved without milling by simply crushing the material to a smaller size. The extraction is a low acid-consuming process, and the orebody is highly homogenous and massive in size.

These advantages along with a well-built infrastructure make for a strong project. In addition, the Namibian jurisdiction serves as a highly-favourable royalty regime with a good fiscal that has a positive impact on the project’s economics. The robust economics along with the other key project features provide the company with a strong position to generate shareholder value into the next cycle.

Project Economics

According to the PFS (Preliminary Feasibility Study), Bannerman Energy has indicated a $65 price point to move into production. This pricing generates a widely accepted incentive price with a 21% post-tax IRR (Internal Rate of Return), generating a post-tax $222M NPV (Net Present Value). The Etango project is a large-scale mine with a long mine life that has expansion capabilities for the future.

The company anticipates that the market pricing for uranium will go beyond the $65 mark. This would provide the company with leverage during contract negotiations. The company expects to deliver into the long-term bull market through its mine. The mine is designed in a way that allows the company to scale up operations from 3.5Mlb to 7.2Mlb per annum. Expansion plans will be based on market pricing trends. At a $75 uranium pricing, the company’s NPV jumps from $222M to around $350M post-tax. This would provide the company with significant leverage in the market.

Bannerman Energy anticipates that the incentive price for uranium will need to be at least $80/lb over the medium-to-long term to encourage the development of sufficient uranium projects in order to cater to market demands. Furthermore, the company forecasts that a number of demand factors or supply catalysts could end up causing further market volatility.

The company is looking to enter production in 2024. In the meantime, it is closely observing the market. The company believes that there’s a highly-interesting dynamic inflection point in the nuclear industry and as a result, the uranium market. It continues to closely observe the market for maximising shareholder value.

Permitting

Namibia offers a significant advantage when it comes to mining permits. However, it is important for companies to enter Namibia with the right mindset and not cut any corners. Bannerman Energy already has the environmental permits for the linear infrastructure and is currently in the process of acquiring environmental permits for the infrastructure supplied by third parties, such as water and power.

The country has a mining code that was introduced in the early 1990s, around the time it achieved independence. This mining code is a mix between the West Australian and the Canadian code. The mining code has been well-tested and has remained stable ever since. The country’s Ministry of Mines and Energy is responsible for processing renewals.

Over the years, the company hasn’t faced any permitting issues. It has a mineral deposit retention licence which it considers an optimal form of permitting. This permit ensures that the company does not have any particular expenditure obligations where it has to commence development by a certain date. Also, the company can transition into a mining licence when it deems the right time to start mining.

In order to attain a retention licence, the company needs to satisfy the Ministry of Mines that it's mine has everything needed for a mining licence. However, since the pricing was unfavourable, the company delayed the licence. Once the price point is desirable, the company is looking to demonstrate the project economics. Following this, It expects to obtain the mining licence fairly quickly.

Financing Considerations

Bannerman Energy is looking at the most conventional financing plan that would be supported by a panel or a club of bank financiers for the Etango project. The company is also considering off-take financing from China, India, South Korea, Russia, the Middle East, or Poland. Additionally, the company is also looking at an export credit finance facility from the UK.

Given the massive scale of supply, the company believes that its uranium can serve a nation-building nuclear fleet. This provides it with multiple financing avenues that are attractive from an equity holder's perspective.

China recently announced at COP26 that it plans to build 150 nuclear reactors over the next 15 years for an estimated cost of $440Bn. These nuclear reactors will require a large-scale supply of uranium.

As per the PFS, Bannerman Energy’s pre-production capital is $274M. The company expects to achieve realistic outcomes through favourable financing terms. It anticipates that an export credits arrangement or a potential offtake with a minority stake for China can generate a lot of interest among other parties as well. This is because China has been aggressively shopping for uranium for the past 5-10 years. There are expectations that other countries will also be interested in securing a uranium supply.

Cash Position

Bannerman Energy ended Q4 2021 with AUS$9.2M in cash flow. The company expected a total external cost of AUS$4M when it commenced its DFS back in August 2021. The company is highly frugal when it comes to spending capital and has been highly strategic with capital raises. The company expects that the current cash flow places it in a very comfortable financial position.

The Uranium Market

As per Bannerman Energy, the market fundamentals for uranium in the short term remain largely unchanged. Although the market has come off in the past 2 weeks, having an impact on other commodities, uranium remains unaffected.

The company anticipates that in the short term, there will be a pronounced impact on the uranium sector once Sprott completes its acquisition of the URNM (North Shore Global Uranium Mining ETF). There are expectations that following the acquisition, Sprott would turn its attention back to the Sprott Physical Uranium Trust which has had a strong determinative effect on the short-term investor sentiment in the past 6 months.

Additionally, the company expects that there will be added momentum in the market following SPUT’s NYSE listing. Notably, the SEC documentation for the listing has already been issued.

The company anticipates that these 2 factors will have a short-to-medium-term impact on the uranium supply and demand market, as it starts catching up to the fundamentals following the destruction caused by covid. This trend is expected to play out over the next 12 months.

Bannerman Energy anticipates that the market will be moving towards catching up on the contracts that couldn’t be signed due to covid. The pandemic caused a slowdown which made it harder to conduct business. Additionally, the utilities had faced difficulties in operating their nuclear plants with the added covid restrictions and regulations.

There aren’t any expectations to see a significant jump in contracts, especially for first-time producers. The company will treat any big push towards contracting over the next 6 months as a bonus.

A reasonable portion of the market’s uranium demand is being met primarily by 2 sources. The first source is the uranium producers who exclusively sell to the spot market. This can be a direct sale or through off-takers with traders that offload the product later either through the spot market or other mechanisms.

The demand for uranium has been struggling for the past few years to absorb the impact of direct selling, leading to the unsustainable and improbable spot market uranium prices.

Furthermore, the uranium demand is increasing further as both SPUT and Yellow Cake get closer to replenishing their physical uranium stock.

There are expectations that in the short term, the uranium inventory will be exhausted and the demand will overwhelm the primary uranium suppliers, producers, and traders into the spot market. This can potentially lead uranium to push past the $50 mark. As per the company, once the uranium starts pushing through $50, it is an indication that the mobile inventory for uranium has thinned out.

Bannerman Energy is looking to deliver its DFS by the end of Q3 2022. The company anticipates that by this time, the uranium market will be in an interesting and favourable position.

To find out more, go to the Bannerman Energy website

Analyst's Notes

Subscribe to Our Channel

Stay Informed