Banyan Gold - Infrastructure Discount, Perception Lag and a Franco-Nevada Tell

8M Ounces of Gold at $43/Oz. One Royalty Company That Noticed

A large-scale Yukon gold deposit trading at exploration-stage multiples. The question is not whether it is cheap, it probably is. The question is what finally closes the gap, and how long an investor must carry the risk to find out.

Defining the asset

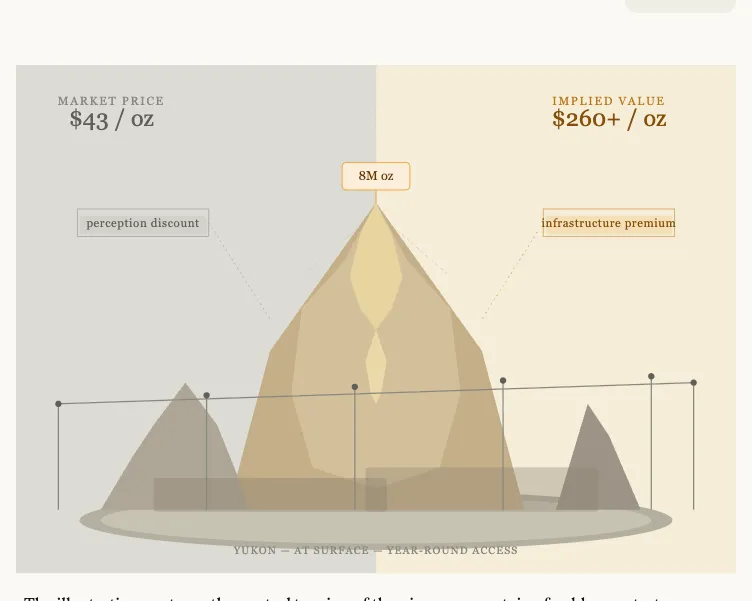

Banyan Gold is not, in any honest framing, a development-stage company. It is a large-scale, surface-amenable gold accumulation in a jurisdiction that was recently re-priced for idiosyncratic reasons and has not fully re-priced back. At roughly $43 per ounce of resource, it is being valued as though the 8-million-ounces in the ground are marginal, isolated, and expensive to access. They are none of those things. What is being offered here is a optionality vehicle on a generational-scale deposit at what is effectively an exploration-stage multiple, a structural dislocation created by a combination of overhang events and grade perception that have persisted long past their informational relevance.

The category matters. This is not a story about drilling results or a speculative exploration play. The resource exists. The infrastructure exists. The variability being priced in is now largely reputational and analytical grade perception, jurisdictional hesitancy, and the delayed institutional recognition that typically follows a re-rating of peer group benchmarks.

What Actually Matters

The single most consequential factor here is the infrastructure discount and it is being significantly underestimated by the market. Banyan's AurMac deposit sits at surface, accessible via year-round roads, with hydropower directly adjacent. In a capital environment where construction-stage mining projects routinely see permitting delays measured in years and access infrastructure costed in the hundreds of millions, these attributes translate directly into a lower capital intensity, a faster permitting pathway, and a materially higher probability of project execution. The comparable set, particularly the Snowline valuation at $260 per ounce reflects, at least in part, the market's recognition of what a genuinely accessible, at-surface deposit in a stable Canadian jurisdiction is worth. Banyan has that. It is not being priced for it.

The second driver is the PEA, due in the second half of 2026. This is not merely a valuation milestone, it is the mechanism by which the infrastructure advantage gets quantified and made legible to institutional capital. The argument that a surface deposit with existing roads and grid power produces dramatically different economics than a comparable remote deposit cannot be fully priced until the number is in front of people. The 43,000 metres drilled in 2025, specifically focused on starter-pit economics and high-grade domain extension, means the PEA is arriving with a substantially improved underlying dataset. This is not a routine box-ticking disclosure. It is the first time the project's economics will be formally benchmarked, and it will land in a gold price environment where the inputs are generationally favourable.

Third: the Franco-Nevada royalty purchase. At $52.2 million for what is, in the most likely development scenario, essentially a 1% NSR after the $10 million buydown, the implied valuation significantly exceeds current market pricing. Franco-Nevada does not buy royalties on projects it does not believe will be built. They are not paying for optionality on a marginal asset. This is arguably the most credible third-party signal in the investment case, and it appears to have registered surprisingly little with the broader market.

The Franco-Nevada signal deserves more weight than it has received. Stripping out the $10M buydown and discounting for timing, they appear to have paid approximately $42M for 1% of net smelter returns. At any reasonable production assumption on 300,000+ ounces per annum, that royalty takes many years to pay back at face value, meaning they are pricing in significant production longevity, scale, and commodity price. That is a more substantive endorsement than any drill result.

What is Priced in & What is Not

The market is pricing Banyan as though the Victoria Gold overhang is still partially live, the Yukon jurisdiction remains structurally compromised, and the grade profile is irredeemably low-tenor. None of these are currently accurate, and the first two have been formally resolved. The overhang cleared via court order in late 2025. The share position was fully liquidated. A conservative business government replaced the prior administration. These are not narrative improvements, they are structural changes to the risk profile of the asset, and they have not been reflected in the valuation relative to peers.

What is not priced in: the infrastructure premium that the PEA will make explicit, the high-grade silver optionality at the Airstrip zone which represents a potentially self-funding near-term cash flow story, and the M&A strategic value of an 8-million-ounce deposit at a time when the majors are cash-generative at $4,000 gold and demonstrably short of large, buildable assets. The Victoria Gold mine, adjacent, potentially for sale, and providing a direct benchmark comparison, could catalyse a re-rating purely by making the valuation gap visible through a third-party transaction.

The current $43 per ounce multiple is not a fair reflection of risk-adjusted value. It reflects an information lag and an investor base that has been conditioned to apply a perception discount that events have already invalidated.

Where the Real Risk Sits

The key risk is not grade, it is time. The grade overhang can be addressed analytically and will be addressed operationally by the PEA. The key risk is not jurisdiction — the regulatory environment has materially improved and the infrastructure is already in place. The key risk is the duration of the re-rating. Banyan's investment case requires several sequential catalysts to land, be absorbed, and be re-priced by a market that has demonstrated it can discount positive news for longer than seems rational. The resource update, the PEA, the Victoria Gold transaction, the silver drill results, each of these individually is a positive data point. The question is whether any single one of them is sufficient to force a step-change re-rating, or whether the stock simply continues to track gold price with a persistent structural discount until an M&A event collapses the gap instantaneously. An investor buying today is being asked to carry not valuation risk but timing risk, and in junior mining, those two are not the same thing. The funding runway looks adequate for the current programme, but a prolonged capital markets disruption would change the calculus materially.

Positioning Within the Peer Group

Within the Yukon explorer cohort, Banyan is straightforwardly the most infrastructure-advantaged project and one of the largest by resource base. The Snowline comparison at $260 per ounce illustrates the premium the market will assign to high-grade, high-conviction assets in the same jurisdiction, but Snowline case rests heavily on exceptional intercept grades and an emerging discovery narrative. Banyan's case rests on scale, accessibility, and economics, which are objectively more bankable attributes at the development stage, if less exciting at the exploration stage. The discount to peers appears to reflect lingering exploration-era thinking applied to an asset that has moved beyond it.

Where the differentiation is overstated: the silver discovery, while genuinely interesting and potentially material to near-term cash flow optionality, is early-stage and should not anchor a primary valuation argument until further drilling substantiates the size and continuity of the zone. Management is right to pursue it; investors should discount it heavily until the 2026 drill programme provides clarity.

The "So what" Investor Relevance

The PEA, expected in the second half of 2026, is the event that matters most. Not because it will reveal something unknown, but because it will translate qualitative infrastructure advantage into a capital cost estimate and a project NPV that institutional generalists can anchor to. That is the moment when the perception gap between "low-grade Yukon explorer" and "large-scale, infrastructure-advantaged development asset" becomes explicitly navigable. The resource update in Q2 2026, with material conversion from inferred to indicated expected, provides the intermediate step. If the Franco-Nevada transaction and the incoming resource update do not together begin to close the valuation gap before the PEA, then the PEA itself becomes the forced re-rating event — provided the economics are as compelling as the infrastructure setup suggests they should be.

The bear case is not a geological one. It is a market structure one: that the junior mining re-rating cycle peaks before Banyan's catalysts land, that M&A does not materialise, and that a prolonged gold price correction resets the entire sector before the PEA can be absorbed. In that scenario, the discount is not wrong — it is merely early. For investors with the right time horizon and risk tolerance, that distinction makes all the difference.

Five Key Takeaways

- The Franco-Nevada royalty purchase implies a project valuation that is meaningfully above current market pricing, this is a third-party signal that has been anomalously discounted by the market.

- Banyan's infrastructure advantage is not a talking point, it is a capital cost differential that has never been formally quantified, meaning the PEA is the first time the market will be forced to price it explicitly.

- The Victoria Gold overhang that suppressed the stock through 2024 is legally and operationally resolved; the valuation has not fully recovered to where it would have been absent that event.

- At ~$43 per ounce versus a peer range of $80–$260, the discount is not a function of asset quality, it is a function of perception lag compounded by sequential bad luck in 2024.

- The timing risk here is more consequential than the geological risk; this is a re-rating story that depends on catalysts landing in a specific sequence within a gold market that is historically volatile and non-linear in how it assigns junior premiums.

Investment Thesis

- Core opportunity: A large-scale (~8M oz), surface-accessible, infrastructure-advantaged gold asset in a stable Canadian jurisdiction, trading at a multiple consistent with exploration-stage risk despite having moved firmly into the development stage.

- Variant perception: The market continues to apply a low-grade discount and a jurisdiction discount that were arguably valid in 2023–2024 but have since been structurally resolved. The infrastructure premium, the single most capital-relevant attribute of the project has never been formally priced because no economic study has existed until now.

- Key execution risk: The re-rating is catalyst-dependent and sequentially fragile; if the PEA economics disappoint (particularly on capital cost and strip ratio assumptions), the entire reframing of the asset collapses.

- Key structural risk: Timing. The junior re-rating cycle is non-linear, and early positioning carries duration risk that is independent of asset quality.

- Trigger to monitor; bullish: Q2 2026 resource update with material indicated conversion and expanded ounce count. H2 2026 PEA with compelling capital cost estimates and clear strip ratio advantage.

- Trigger to monitor; inflection: Sale or transaction involving the Victoria Gold mine next door, any deal that assigns a per-ounce value to a comparable adjacent asset forces a direct Banyan comparison.

- Signal to watch; bearish: PEA capital cost assumptions that fail to reflect the infrastructure advantage, or drill results from the 2026 silver programme that are inconclusive, removing the near-term cash flow optionality argument.

TL;DR

Banyan Gold is a credibly large, infrastructure-advantaged gold deposit trading at a multiple that reflects neither its development stage nor its strategic relevance at $4,000+ gold. The Victoria Gold overhang is cleared, the jurisdiction narrative has improved, and Franco-Nevada's $52M royalty purchase provides a hard third-party valuation signal the stock has not absorbed. The PEA, due H2 2026, is the catalyst that forces the gap to close or confirms that it won't. For a fund with tolerance for catalyst-dependent junior exposure, this is worth a meeting, not because the narrative is compelling, but because the structural disconnect between asset quality and current pricing is measurable and specific. The risk is not geological. It is whether the re-rating cycle in junior gold sustains long enough for the catalysts to land.

Risk Profile Addendum

For the Low-Risk Fund Manager

This stock does not belong in a capital-preservation mandate today. The resource is inferred-heavy, the economics are unstudied, and the re-rating path is catalyst-dependent in a sector with a demonstrated capacity to remain mispriced for extended periods. The conditions for conservative consideration are specific: a PEA that demonstrates compelling capital cost efficiency and a strip ratio consistent with the infrastructure narrative; material conversion of inferred to indicated in the Q2 resource update; and evidence that institutional coverage is beginning to re-engage with the name. None of these have occurred yet. The cost of waiting for them is real entry price after a PEA-driven re-rating could be 50–100% higher than today, but that premium buys the removal of the most material uncertainty in the investment case. For a benchmark-sensitive mandate, that trade-off is probably correct. Watch the PEA. If it delivers, it will still be early.

For the High-Leverage Fund Manager

The framework for early entry rests on three things that must hold simultaneously: first, that the infrastructure advantage is real and will be reflected in PEA capital cost assumptions, meaning the project is not just large but economically viable at current gold prices; second, that the Franco-Nevada transaction is genuinely informative rather than a structured deal with idiosyncratic terms that do not reflect fair market value per ounce; and third, that the current gold price environment ($4,000+) is sustained long enough for the PEA to land in a constructive market. If any of those assumptions fails, the position reverts to a discounted exploration asset with a long wait for the next catalyst. The specific signal that would tell you the thesis is wrong: a PEA with capital cost estimates that imply per-ounce construction costs inconsistent with the infrastructure narrative, or a gold price correction of 20%+ before the H2 2026 catalyst window. The bull case entry today is essentially a bet that Franco-Nevada has already done the diligence you would otherwise need to do yourself and that the market has not yet noticed.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed