Canada Nickel (TSX-V: CNC) - Game Changing Incentive Worth Hundreds of Millions

Interview with Mark Selby, Chairman & CEO of Canada Nickel (TSX-V: CNC)

Canada Nickel Corp. is advancing the next generation of high-quality, high-potential nickel-cobalt projects to deliver the metals needed to power the electric vehicle revolution and feed the high-growth stainless steel market. The company possesses industry-leading nickel expertise and is focused on low-risk, well-established mining jurisdictions.

Matt Gordon caught up with Mark Selby, Chairman, CEO, and Director, Canada Nickel. Mark previously served as the President and CEO at RNC (Royal Nickel Corporation) Minerals where he successfully raised over $100M to advance the Dumont nickel-cobalt project from an initial resource to a fully-permitted, construction-ready project. He has held a number of senior management roles with Quadra Mining, Inco, and Purolator Courier. He was also a partner at Mercer Management Consulting. Since 2001, Mr. Selby has been recognized as one of the leading authorities on the nickel market. He graduated from Queen’s University with a Bachelor of Commerce (Honors) and has also served on the boards of multiple junior mining companies.

Company Overview

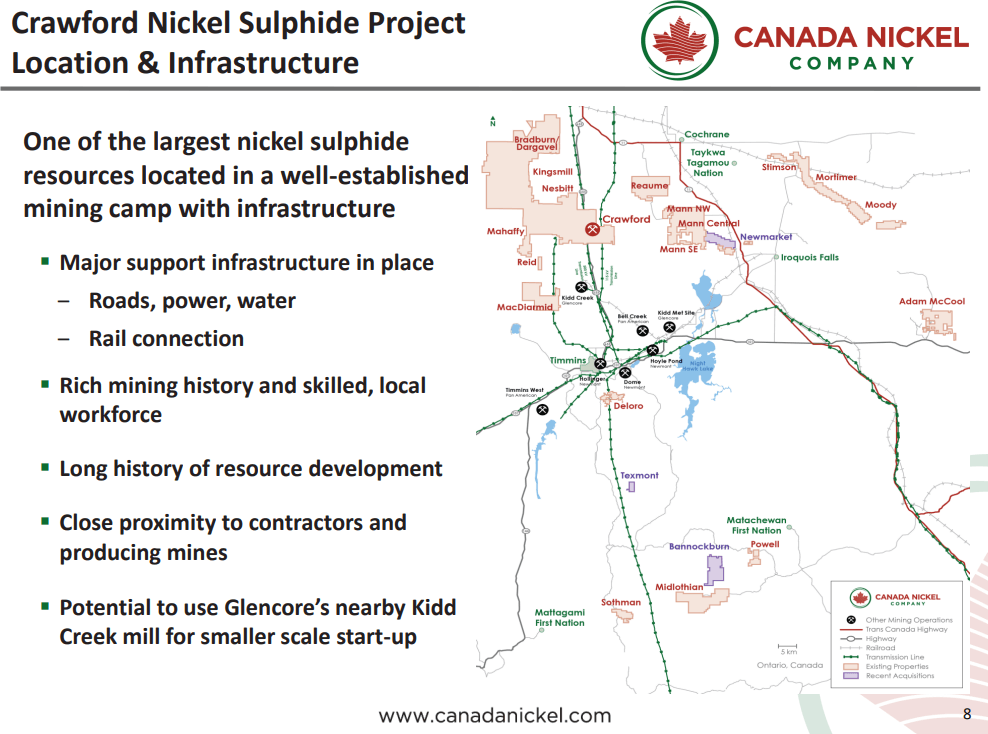

Canada Nickel is advancing the new 100% owned Crawford nickel-cobalt sulphide discovery with large-scale potential located in the established Timmins mining camp adjacent to major infrastructure. The company was founded in 2019 and is headquartered in Toronto, Canada. It is listed on the Toronto Stock Exchange (TSX-V: CNC). In 2020, the company was one of the best performers on the TSX.

Carbon Credits

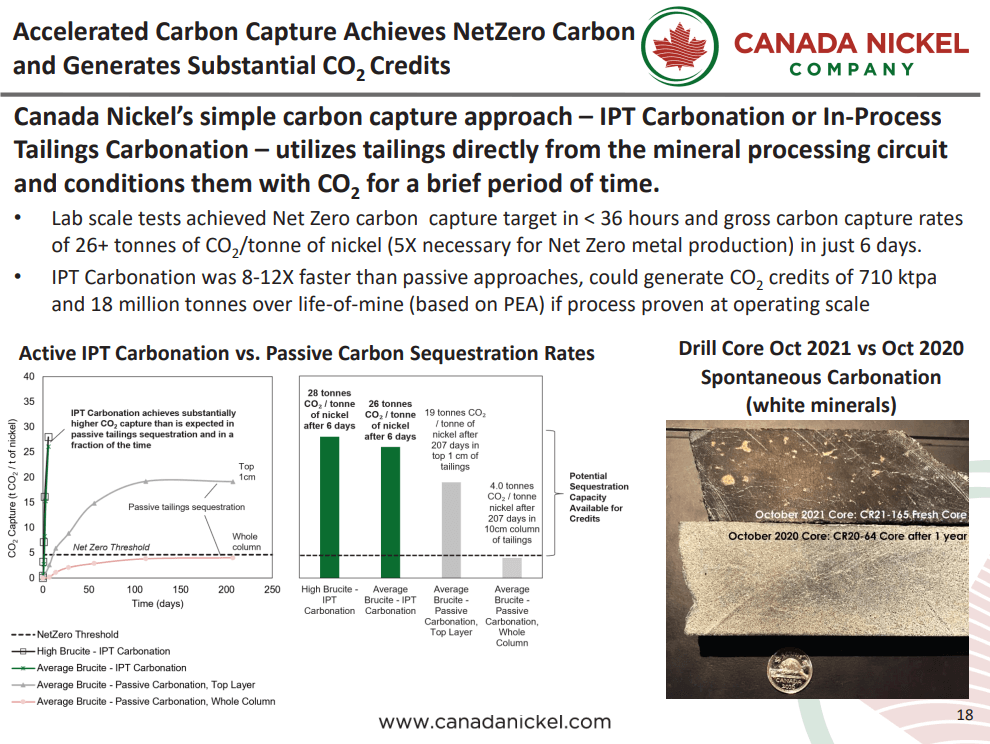

Canada Nickel is advancing the Crawford Nickel Project in the Timmins Nickel District. In 2022, the company announced IPT (In-Process Tailings) carbonization, a breakthrough in carbon capture. In this process, carbon dioxide is injected as the material is going through the mill. The process enables the capture of anywhere between 750,000Mt to 1Mt of carbon dioxide per annum. This carbon capture process is expected to generate close to 20Mt carbon credits over the project’s lifetime.

There was another notable development in 2022 where as part of the federal budget, the Canadian government announced refundable tax credits for anywhere between 37.5% to 60% of the project CapEx (Capital Expenditure) for projects that operate in the carbon capture, carbon transportation, and carbon storage facility. Recently, the company treated two existing streams in the mill to be able to capture carbon. The new integrated feasibility study is expected to take around 4-5 additional months to integrate carbon capture as part of the process. This process enables the company to be eligible for availing between 37.5% to 60% of a large portion of the process planned expenditure, which translates to hundreds of millions of dollars in upfront cash and hundreds of millions of dollars of NPV (Net Present Value) for the project. The company believes that it’s a move in the right direction.

Canada Nickel is confident that it can take the existing mineral processing equipment, adapt it to utilize the carbon dioxide, and add that into the process plant. This process is expected to cost tens of millions of dollars of additional CapEx along with some small amount of incremental OpEx (Operational Expenditure).

The company is looking to build the process plant in multiple phases. The process plant has an estimated build cost of over $1Bn. It will enable the company to get between $300M-$700M in carbon credits. It is important to note that the company would need to apply and qualify for the carbon credits. Acquiring the incremental cash in terms of the NPV and the project IRR (Internal Rate of Return) serves as an exceptional opportunity. The company is looking to reach a point where it the project not only has the potential to have carbon credits but will also be generating 20t of carbon dioxide credit per ton of nickel.

The company is positioning itself to acquire premiums that will be available for zero-cost nickel projects. Verifiable and measurable carbon credits are a key part of the process. A combination of carbon and pipe at point x, the carbonation process, and the carbon coming out of the pipe will enable the company to generate a third revenue stream based on the carbon credits. The company has an opportunity to bake this into the main part of the Feasibility Study.

Canada Nickel believes that by crushing and grinding the rock, taking off the finer fractions will enable a lot of carbon capture. There isn’t any reason for the company to not qualify for the carbon credits from the government. However, it is important to note that until the government provides a sign-off, there is a risk.

The largest carbon storage facility in Canada is 1.2Mt. Shell spent $1.3Bn building the plant. For this process, Shell received $900M in direct government subsidies. Based on a recent press release, Canada Nickel is expecting to capture around 700,000t carbon, which is close to 1Mt of carbon credits per year. This would make the company the only currently contemplated carbon storage in Ontario, which happens to be the largest economy in Canada. The company’s plant would be the largest in the country.

From a government policy perspective, the company is helping advance the climate change objectives. In terms of critical minerals strategy, the company is going to be a major nickel and cobalt producer in North America and the continent’s only chromium producer. It will also be producing platinum and palladium in limited quantities.

In terms of EV strategies for the provincial and the federal government, the project hits three separate government objectives, positioning the company close to the front of the line in terms of being able to tap into the pools of available government subsidies, which is good money for the project and the shareholders.

Revenue Generation

Canada Nickel has the cash flow to advance the project and the expected rebate comes upfront. In terms of carbon credits, Canada has a stated carbon price of $170/t by 2030. Interestingly, the price was $50/t in the previous year. While the company won’t be able to capture all the price, given the quality of carbon credits being generated, it can lead to a substantial revenue stream.

There are other companies that are also carrying out mineral sequestration. One such example is Carbfix in Iceland and Carbon Engineering. The latter is building a pilot plant in British Columbia and has partnered with Oxy Petroleum to build a large plant in Texas. 750,000t or 1Mt of credits per year at a $30/t-$100/t or higher price will generate a significant amount in incremental revenue.

It is important to note that Canada Nickel had optionality for the carbon sequestering and took a conscious decision to delay the Feasibility Study. The project already has good geology, mining, and processing metrics. The company believes that taking a few extra months won’t take it off the critical path. Instead, acquiring the permit, which is already under process is the critical path. The company is still on track for a mid-2025 permit, which would be followed by construction. It is focused on making the most robust project possible coming out of the gate from day one.

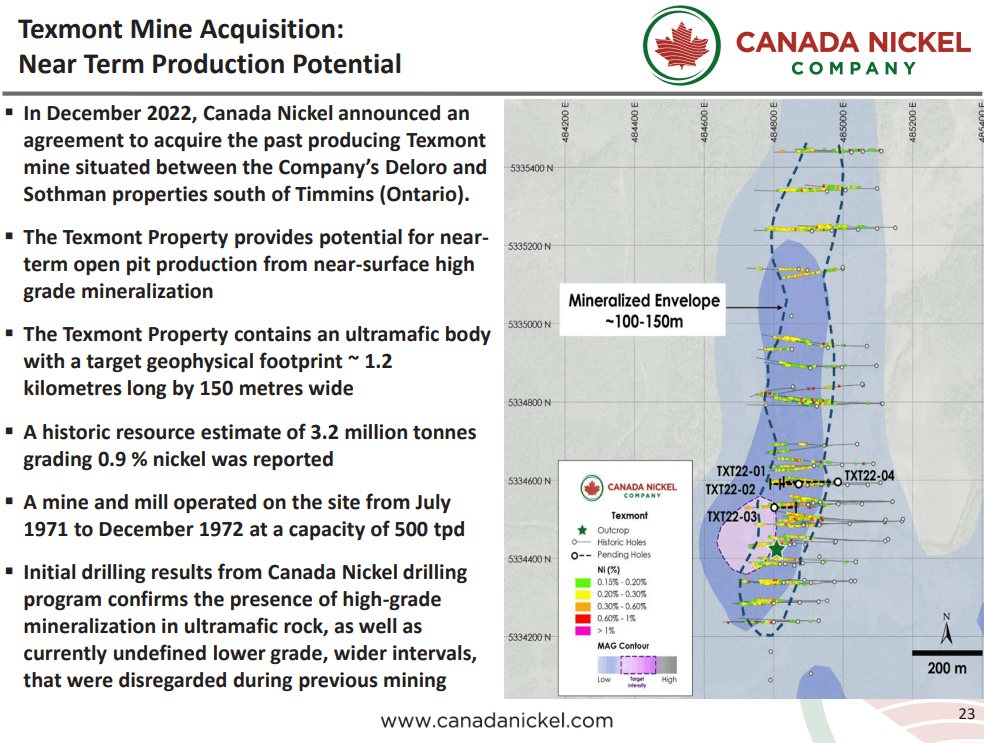

The company understands that the project is about scale and scalability based on the market demands. Battery manufacturers and car companies are looking for large quantities of nickel that can come online in the second half of the decade, or preferably sooner. Canada Nickel’s Texmont acquisition is one such project that has the potential to be scaled up multiple times.

Canada Nickel has been in discussions with several Korean companies for over a year. It has also been talking to a few of the more future-focused car companies. In mid-November 2022, the entire car industry realized that in order to source the raw materials, they’d need to provide capital. Pre-Christmas, the company had discussions with most of the European and North American companies and found that the car makers are cognizant that capital would need to be provided. This goes beyond signing an off-take deal. It’s about getting the money in place in order to advance the projects. Car companies require a steady supply of nickel.

One such example is a Korean company that consumed 30,000t of nickel in 2022. The company’s midterm goal is to consume 200,000t of nickel in 5 years. Interestingly, the company isn't looking to source the nickel from high-carbon, Chinese-controlled sources in Indonesia. The Inflation Reduction Act has made it clear that there’s an increased focus on having supply chains of non-Chinese origin. Companies are looking for large-scale projects like Canada Nickel’s to meet the growing nickel demands.

Vale recently spent close to $1Bn opening the new Copper Cliff Mine. The mine is expected to produce around 10,000t-15,000t nickel per year, which is going to be less than a month’s worth of nickel consumption by car makers. Large-scale projects with zero-carbon nickel sources are highly desirable for this generation of nickel consumers.

Canada Nickel is advancing the Crawford project at light speed. While there is a few months' delay in the Feasibility Study, the company continues to be on track, going from the fifth drill hole to a full Feasibility Study in less than 4 years, which is a rare achievement. It is important to note that the company will enter construction by mid-2025 and will start operating by 2027-end.

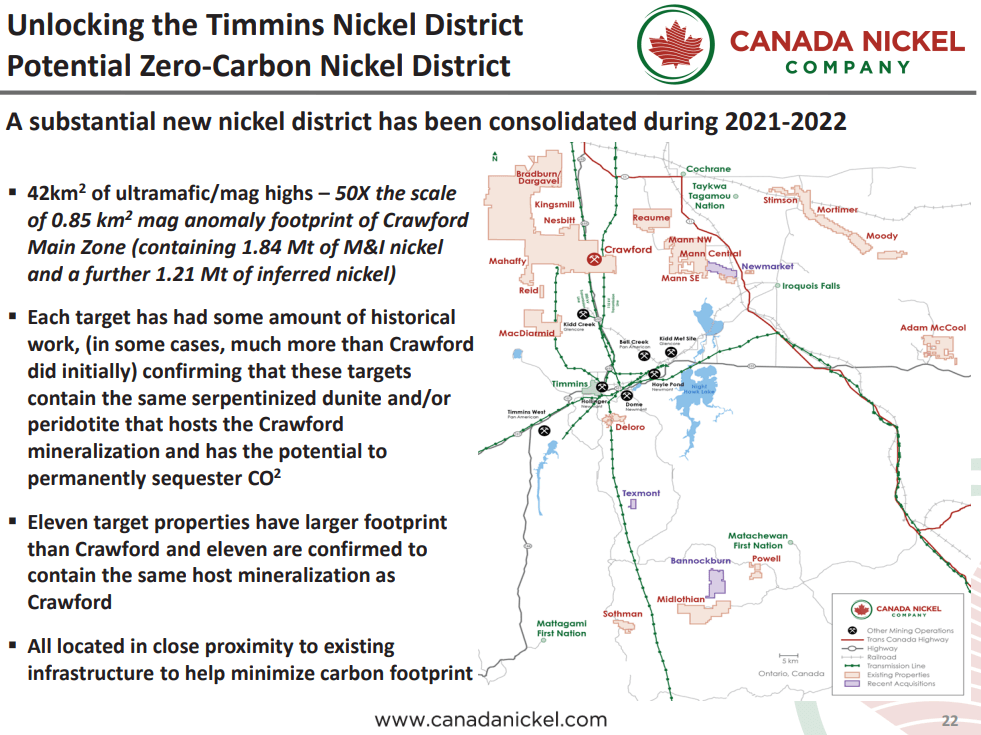

Based on the conversations with the Korean companies, it is clear that there’s a strong inclination to source as much nickel as possible from North American sources. 18 months ago, Canada Nickel set out to collate the entire Timmins Nickel District, which had the potential for half a dozen Crawford assets in the region. The results published in the second half of the year support this assumption. At the same time, the company is looking at smaller, lower CapEx, shorter time-frame operations that will enable it to get into production, generating 3,000t-5,000t of nickel and creating tens of millions of dollars in free cash flow annually within the next 2 years. This would generate a good cash flow without having to spend a lot of shareholder equity. There are a lot of investors that are interested in financing the small CapEx producers. In terms of the investor pool, there are a limited number of parties that are willing to bet on bigger projects that will come online in a few years’ time. On the other hand, there are a lot more investors that are interested in near-term exposure, and near-term production for a particular metal.

The company started working on the Texmont mine 18 months ago, but it got tied up in the State. It took the company more than a year to engage, and it was able to acquire the asset for $4M cash, which is due in a couple of months. Notably, there are a lot of financing sources lined up for the Texmont mine, which makes the capital acquisition process fairly straightforward.

The previous owner had the Texmont mine in the 2000s. At the time, a 28,000m drill program was carried out that was never included in the resource. The drill program alone provides 80% of the data for the mine’s underlying geology. This asset has the potential to attract a whole new base of investors and it can be turned into a cashflow story potentially by 2025. Canada Nickel is looking to work on the mine as quickly as it did on the Crawford asset. Since the mine was a past producer with mining leases, the permitting process is expected to be easier and significantly faster.

Targets 2023 and Beyond

According to the company, the Texmont mine will have zero impact on Crawford’s timeline. The resource and drilling for the Feasibility Study for the Crawford asset are completed for the most part. The team will carry out geology studies on the asset which will be followed by the mine design. Next, a PEA (Preliminary Economic Assessment) would be carried out as the project moves closer to the Feasibility Study. By Q2 2023, the company intends on putting a person in charge of the project to ensure undeterred focus. The company will hire staff accordingly, leading to two teams working in parallel once the resources are in place.

Shortly before Christmas, the company announced the appointment of Scotiabank and Deutsche Bank. This announcement was well-received by the market, as reflected in the share price. The fact that Scotiabank and Deutsche Bank are working with Canada Nickel speaks volumes about the quality of the company’s team and the project. The banks have been specifically mandated with putting together the overall equity cheque, which will be 40% of the project’s capital cost. This announcement has also exposed the company to the banks’ marketing and distribution channels, leading to a massive global footprint exposure. The company anticipates that this development will pay significant dividends as it moves through the year, and it will open the company to even broader financing sources going forward.

In terms of the CapEx, the current Feasibility Study metrics continue to be on track. The company is looking at a 50% larger operation, choosing a single expansion as opposed to two expansions, bringing the overall production to 120,000t/day. The CapEx in the PEA was 50% larger, which is expected to be within range. The inflationary pressure is offset by the fact that the company is operating on a much larger scale. Large-scale deposits offer a lot of flexibility with areas of operation, whereas most smaller deposits do not offer such flexibility.

For underground mines, the geometry of the ore body can be used to determine the maximum throughput at which the mine can operate. A large and broad ore body with a low-strip ratio provides significant flexibility in terms of daily processing capacity. The company can potentially expand it multiple times to take the advantage of the scale of the operation. Larger ore bodies offer a degree of freedom that isn’t possible with a smaller operation.

From day one, the company has focused on advancing operations with minimum equity dilution. The company’s CEO, Mark Selby has been buying the stock in the market over the last 2 years. Most of his net worth is invested in Canada Nickel.

The company is not in a favor of a bought deal for financing. The first piece of the financing stack is a PGM (Platinum Group Metals) stream. In the Feasibility Study, the company will include the palladium and platinum ounces. These metals are expected to generate between $50M-$100M in project capital.

The next financial stack would come from car companies and green battery companies. Both parties are desperate for an off-take agreement for the next 10-15 years. The company has put proposals where in order to acquire a portion of the off-take, the car company or green battery company would need to provide a chunk of capital that will function as equity to the project finance facility.

In a case where the project CapEx requirements aren’t fulfilled, the company has an alternative. It has been approached by several Japanese trading houses and other companies that have shown project-level interest. Here, the company could let the part buy 10%-20% of the project. This will provide the needed equity to advance the project with little-to-no equity dilution to the average shareholder.

In a recent press release, the company talked about appointing a debt advisory past life warranty by January 2023. It is in discussions with the Rothschilds, a handful of groups that are known to carry out billion-dollar project financings. For the majority of the past year, Canada Nickel has been in discussions with the parties. The parties have been keen to work on the project due to its scale, potential, and jurisdiction. Majors and major consumers have also shown interest in project involvement.

The company is looking to appoint one of the groups in January 2023. The group will work alongside the equity portion of the project. The company is looking to work with the group in lockstep so that by the time the permits are acquired in mid-2025, everything is set up and ready to go. By this time, the company is looking to have a fully-financed project ready for construction. While it isn’t confirmed that the company will be working with the Rothschilds, the discussions are ongoing and it could be a group with a similar financing capacity.

In Ontario, Canada, every EV (Electric Vehicle) investment that’s been made by a car company or into the supply chain has received around 10% of the capital from the provincial government and an additional 10% capital from the federal government in various types of financing support. It is important to note that this is in addition to the tax credits for carbon capture and storage. Canada Nickel ticks three separate boxes for the government in terms of climate change, EV strategy, and critical minerals. This makes it highly likely that the company will get carbon credits and financing support from the Canadian government.

In terms of near-term financing, Canada Nickel has a loan due with Auramet in mid-January. The company has the option to extend it by 3 months if needed. There are a number of ongoing conversations and the company is expecting a closure in the near future. There’s a lot of flexibility and Auramet has been highly supportive in this regard. The short-term financing will be in place within the next 2 months.

For the overall project financing timeline, the company is looking at off-take discussions as a key driver. It anticipates that either by the first half of 2023 or by the third quarter, it will have off-take partners in place. Some Korean companies and car makers are currently spending billions of dollars on other Canadian investments. From the company’s purview, it would be ideal to approach the government to accelerate the permitting timeframe, which is currently the critical path.

The off-take portion of the financing will serve as an anchor for the equity. Following this, the company can determine any additional requirements, and based on this, it intends to start discussions with various Japanese trading houses and other partners that are interested in taking 10%,15%, or 20% of the project.

The debt part of the equation usually takes a long time. The company is looking to enter discussions with interested parties at the earliest so that it can assign a debt advisor by January 2023. Following this, the company will meet with various groups in the first and second quarter. According to the company, the parties would need around a year or so to go through various processes. In the meantime, the ongoing Feasibility Study will approach completion.

Canada Nickel looking to have equity and debt in place by the second half of 2024. In the meantime, it will have discussions with the government about streamlining the permitting process, which could potentially bring the process up by 6 months or more.

One of the reasons for postponing the Feasibility Study is that it allows for add-ons where the testing, piloting, and engineering can be carried out. The company is looking to potentially commission a small pilot plant that leads to a data sheet. Once the plant is reviewed by a good engineering firm, the company will be confident in relation to the emerging carbon credits.

According to the company, these credits are highly-verifiable and measurable that can be presented to the bank. Given the growing demand for real carbon credits, the future potential looks highly promising. Canada Nickel is looking to publish the project Feasibility Study by end of Q2, 2023.

To find out more, go to the Canada Nickel website

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed