Undervalued? Is Cassiar Gold's Infrastructure, Resource Scale and Production Optionality Mispriced?

Cassiar Gold: 2.3M oz BC resource, existing permits/mill, $32/oz EV vs $50-900 peers. High-grade bootstrap potential 30-60K oz/yr, $30M capex. 5M oz exploration target.

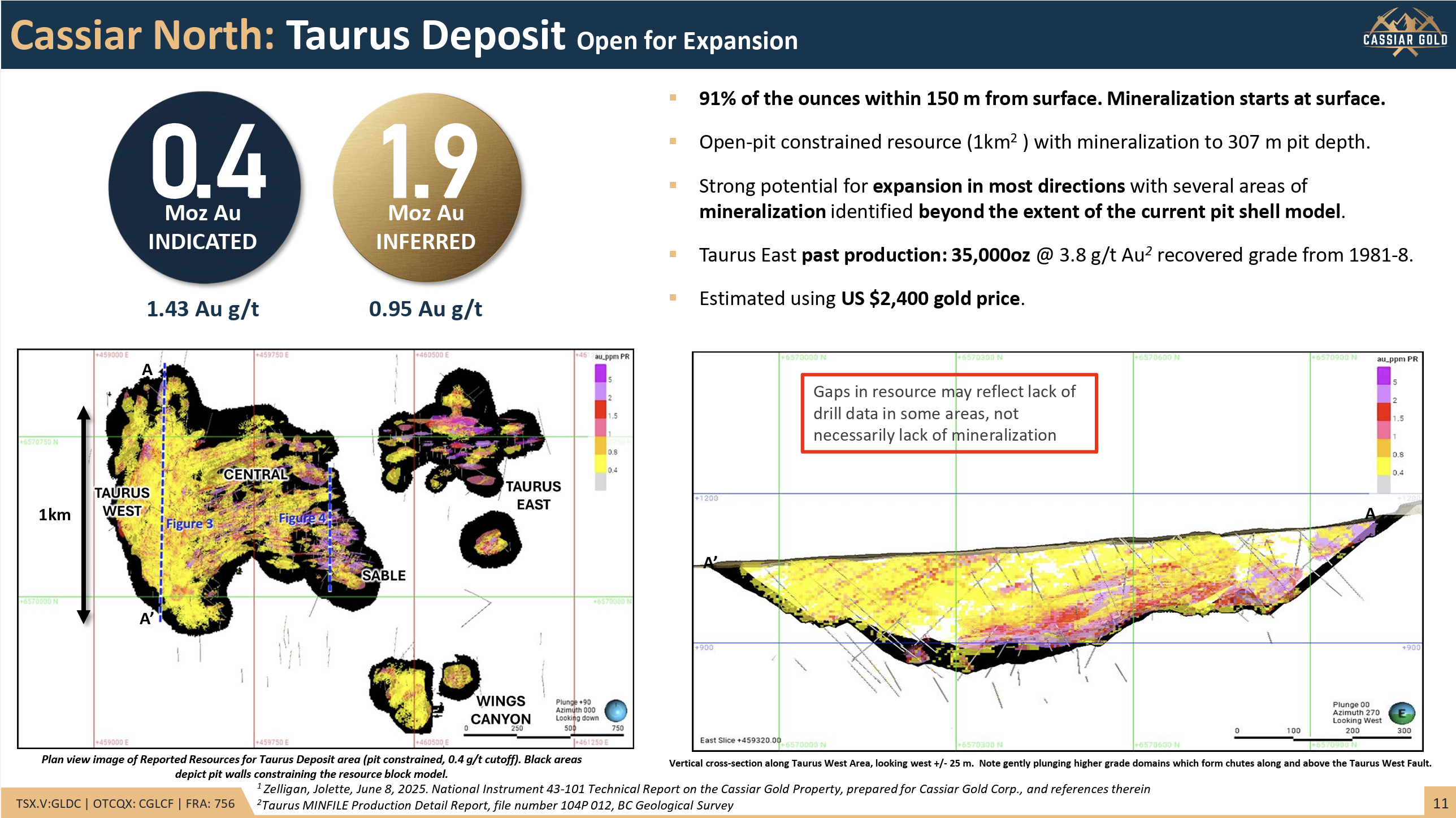

- Cassiar Gold controls 2.3 million ounces at the Taurus deposit in northern British Columbia (1.9M inferred at 0.95 g/t, 410K indicated at 1.43 g/t), with 91% of ounces within 150 meters of surface and significant expansion potential across a 600 square kilometer land package

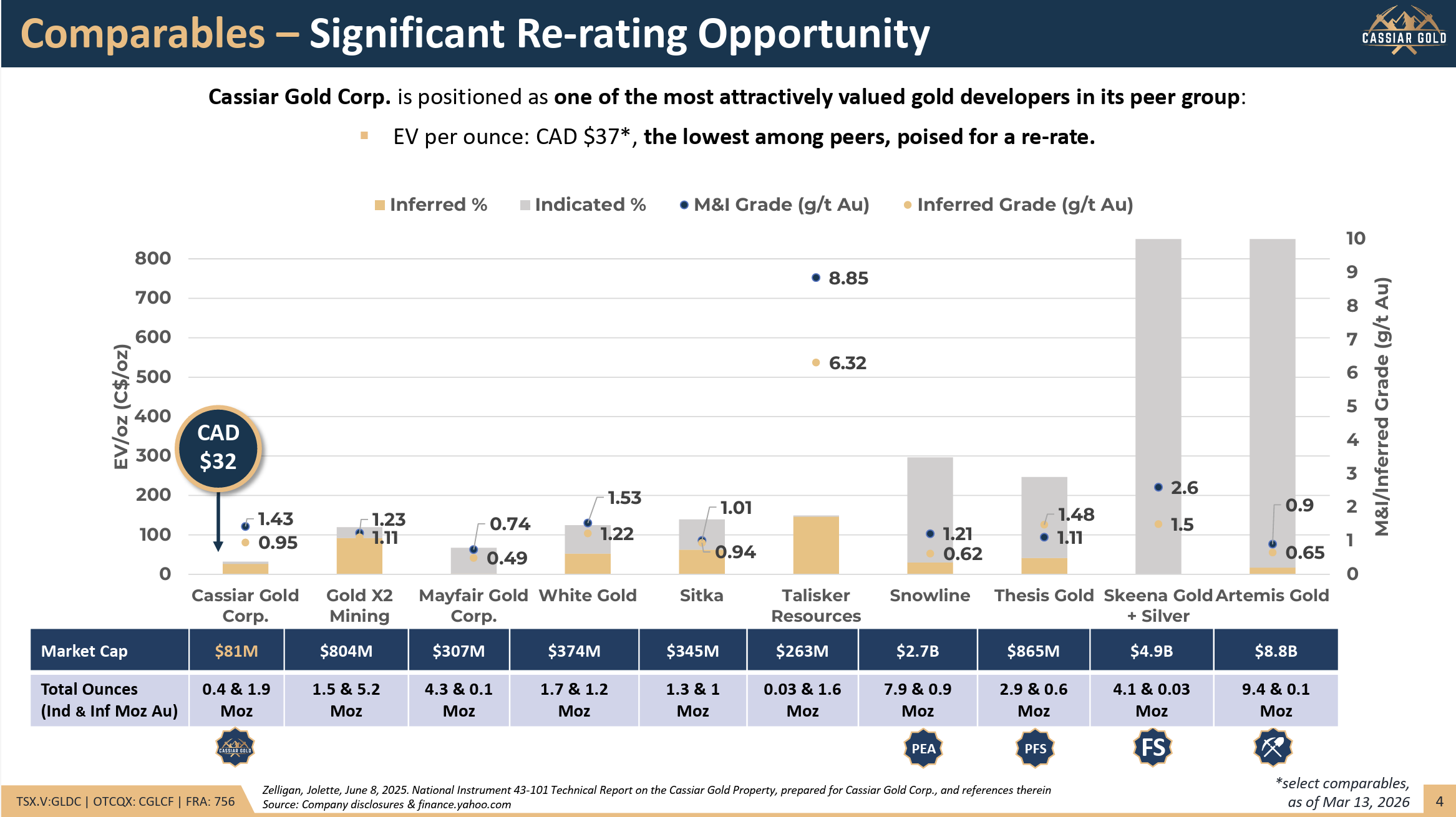

- Trading at approximately $32 CAD per ounce enterprise value versus peer range of $50-900 CAD per ounce, with an $80 million market cap that CEO Marco Roque characterises as significantly undervalued relative to infrastructure and resource quality

- Company possesses existing mine permits, a permitted 300 ton-per-day mill, paved road access, grid power, 25 kilometers of underground workings, and 160 kilometers of access roads - representing tens to hundreds of millions in pre-existing capital investments

- Near-term production optionality through high-grade underground veins (10-20 g/t) capable of generating 30,000-60,000 ounces annually with minimal capex (~$30M CAD), alongside longer-term open-pit development of the bulk tonnage deposit

- Targeting production within compressed timeframe using existing infrastructure, with critical path being tailings facility re-permitting (1.5-2 years), though direct shipping ore (DSO) option could accelerate timeline by 25-33%

Cassiar Gold Corp. (TSXV:GLDC) operates as an advanced exploration company focused on its flagship Cassiar property in northern British Columbia. With a current market capitalisation of approximately $80 million Canadian and a share price around $0.50-0.55, the company presents what management characterises as a significant valuation anomaly in the junior gold sector.

President and CEO Marco Roque leads a management team he describes as experienced mine builders who have navigated multiple industry cycles. The company's board includes Stephen Letwin as chairman, previously CEO of IAMGold. This operational experience forms the foundation of the company's strategy to advance from advanced exploration toward production.

The Taurus Deposit Resource Base

The Taurus deposit represents the entirety of Cassiar Gold's current resource inventory, containing 2.3 million ounces across two categories. The inferred resource totals 1.9 million ounces grading 0.95 grams per tonne, while the indicated resource comprises 410,000 ounces at 1.43 grams per tonne. The combined resource averages just over one gram per tonne.

What distinguishes this deposit from many modern discoveries is its proximity to surface. The mineralisation effectively outcrops at surface, with 91% of ounces located within 150 meters of surface and an estimated average depth of approximately 80 meters. The deepest point of the current pit design reaches 307 meters. The deposit covers just over one square kilometer of a nearly 600 square kilometer land package, remaining open laterally, at depth, and internally within the pit shell.

The district has historical significance, with the discovery of a 72-ounce solid gold nugget in the late 1800s sparking a regional gold rush. Five past-producing mines operated in the area, generating over 300,000 ounces historically at grades between 10 and 20 grams per tonne from underground vein systems.

Enterprise Value Disconnect

Roque emphasises what he views as a fundamental mispricing in the market. At current levels, Cassiar Gold trades at approximately $32 Canadian per ounce of enterprise value. According to management's analysis, exploration companies typically trade at minimum $50 Canadian per ounce, with valuations ranging up to $800-900 per ounce for companies in development stages.

The CEO acknowledges that a large portion of the resource sits in the inferred category, which may contribute to the discount. However, he argues that the near-surface nature of the deposit, combined with existing infrastructure and permits, should command a premium rather than a discount relative to peers with deeper deposits or less advanced permitting status.

Management attributes the valuation gap partly to visibility and market dynamics. Roque notes that the current cycle differs from previous ones, with junior gold companies experiencing sequential rather than parallel appreciation. Companies gain attention and valuation multiples in waves, creating what he characterises as a "haves and have-nots" market structure.

Existing Infrastructure Position

Cassiar Gold's infrastructure position represents a substantial competitive advantage. The company holds existing mine permits - described as "invaluable" in the Canadian and British Columbia regulatory environment. A fully owned and permitted 300 ton-per-day mill sits on the property, specifically designed for processing high-grade vein material.

The property features paved road access bisecting the land package, which Roque and Letwin both emphasise as exceptionally valuable for a mining project. Grid power is available on site. The company controls 160 kilometers of access roads beyond the paved infrastructure, along with 25 kilometers of existing underground workings. At current Canadian development costs of approximately $5,000 per meter minimum, these underground workings alone represent over $100 million in sunk capital. As Roque stated:

“The fact that we have mine permits is extremely unique and almost impossible to value… It's invaluable to have mine permits especially in Canada, especially in British Columbia.”

Interview with Marco Roque, President & CEO of Cassiar Gold

District-Scale Expansion Potential

While the current resource stands at 2.3 million ounces, management has established a corporate target of five million ounces, with Roque indicating he envisions significantly larger potential. The company has identified multiple Taurus-style targets across the property showing similar veining, alteration, mineralisation, and grades.

The New Coast target, located 2.5 kilometers south of Taurus along a 15-kilometer regional structural trend, has returned encouraging results from approximately 20 drill holes. A highlight intercept of 141 meters at 0.89 grams per tonne demonstrates similar width and grade to Taurus mineralisation. Management believes New Coast combined with Taurus expansion could achieve the five million ounce target independently of other prospects.

Additional targets include Hopeful and Lucky prospects, with the Main Mine area five kilometers south of Taurus showing intercepts exceeding 200 meters at bulk-tonnage grades. The company continues to identify new anomalies through geophysics, soil surveys, and outcrop sampling across the extensive land package.

Dual Development Strategy: High-Grade Bootstrap and Bulk Tonnage

The company's strategic positioning centers on two distinct but complementary development paths. The high-grade underground vein systems offer near-term production optionality with minimal capital requirements, while the bulk tonnage open-pit deposit provides longer-term scale and economic foundation.

The high-grade veins historically produced over 300,000 ounces at 10-20 grams per tonne. Using the existing 300 ton-per-day mill, processing at 10 grams per tonne would generate approximately 30,000 ounces annually, while 20 grams per tonne feed would produce roughly 60,000 ounces per year. This production scale exceeds typical bootstrap operations of 5,000-20,000 ounces annually. The current gold price environment transforms the economics of this strategy.

“Two or three years ago, you would be looking at a $200-$300 an ounce margin. These days with the current gold price... you're looking at thousands of dollars of potential margin there.”

Near-Term Production Pathway

Management has outlined specific steps required to achieve production from the high-grade vein systems. The mine permit must be amended from care-and-maintenance to production status, a relatively streamlined process. The mill requires refurbishment, which management expects to be straightforward given it last operated in 2007 and was partially refurbished in 2010, with recent technical reviews providing positive assessments.

Underground infrastructure requires dewatering of partially flooded portals, screening and bolting work, and complete replacement of underground services. The vein system offers the most accessible high-grade material, requiring approximately 50 additional meters of development after dewatering the final 200 meters of existing workings to access material grading over 20 grams per tonne. The vein systems average three meters in width.

The critical path item is re-permitting of tailings facilities to current British Columbia standards, estimated at 1.5 to 2 years. The company has four tailings facilities with capacity but requiring upgrades to modern standards. To potentially compress this timeline, management is evaluating direct shipping ore (DSO) arrangements, which would involve trucking material to offtakers rather than processing on-site until tailings permits are secured. This approach could reduce the timeline by one-quarter to one-third.

Management has scoped internal capital requirements at approximately $30 million Canadian for the restart, and is actively engaged in discussions for non-dilutive capital, offtake agreements, and DSO arrangements. The company is targeting production within five years for the bulk tonnage project, with the high-grade bootstrap occurring on a faster timeline.

Rising Strategic Interest

Roque noted increasing strategic interest in the company, particularly accelerating in recent months. He attributed this partly to the improved margin environment at current gold prices, which changes the risk-reward profile of development projects. The management team, characterised as experienced and conservative mine builders, previously hesitated to pursue aggressive development when gold prices offered lower margins and less cushion for operational variability.

The CEO emphasised that cash flow generation currently receives the most market recognition and valuation support, suggesting this drives the company's strategic focus on moving toward production rather than solely growing resources. When asked about capital allocation priorities, Roque indicated the company would not risk its balance sheet or overextend operationally, but acknowledged that the current margin environment makes development risk more acceptable than in previous years.

Key Takeaways and Investment Implications

Cassiar Gold presents an unusual combination of attributes in the junior gold sector: a multi-million ounce resource at surface with existing infrastructure, permits, and dual development optionality. The company's enterprise value per ounce sits at a significant discount to comparable peers, which management attributes to factors including the proportion of inferred resources, limited market visibility, and historical perceptions of the project at smaller resource scales.

The strategic value proposition centers on leverage to gold prices through high-margin production optionality requiring minimal capital, combined with significant exploration upside across a district-scale land package. The existing infrastructure and permits eliminate hundreds of millions in typical development capital and years of permitting timeline, though operational execution risk remains in refurbishing facilities and achieving production targets.

The compressed timeline to potential production, supported by existing permits and infrastructure, differentiates Cassiar from typical exploration stories while the bulk tonnage resource and exploration potential provide longer-term scale. Market recognition of this positioning appears to be the key variable in closing what management views as a substantial valuation gap relative to peers and intrinsic value.

TL;DR: Executive Summary

Cassiar Gold controls 2.3 million ounces in northern British Columbia with exceptional infrastructure including existing mine permits, a permitted mill, paved roads, and grid power - trading at $32/oz enterprise value versus peer range of $50-900/oz. The company offers dual development optionality: high-grade underground veins (10-20 g/t) capable of 30,000-60,000 oz/year production with ~$30M capex, and a bulk tonnage deposit with 91% of ounces within 150m of surface. Current gold prices create exceptional margins on high-grade material, transforming the risk-reward profile of near-term production while 5+ million ounce exploration target provides longer-term scale potential.

FAQs (AI Generated)

The company possesses existing mine permits, a permitted 300 ton/day mill, paved road access, grid power, 25km of underground workings, and 160km of access roads - representing pre-invested capital typically requiring hundreds of millions and years of permitting.

At ~$32 CAD per ounce enterprise value, Cassiar trades below the $50-900 range for peers, despite near-surface mineralisation (91% within 150m), existing infrastructure, and permits that management argues should command premium rather than discount valuations.

Management estimates ~$30M CAD capex for restart, with critical path being tailings re-permitting (1.5-2 years). Direct shipping ore option could compress timeline by 25-33% by deferring on-site processing until permits secured.

High-grade material (10-20 g/t) at current gold prices margins are many multiples of the $200-300/oz margins two years ago, fundamentally altering the risk-reward profile and making development more economically compelling with greater operational cushion.

Current 2.3M oz resource is constrained only by drilling and open in all directions. New Coast target 2.5km away shows similar mineralisation. Multiple Taurus-style targets identified across 600 sq km land package with similar geological signatures.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

%20(1).png)

Stay Informed