Niger’s Contested Uranium Sales Intensifies Procurement Risk for 12,000-Tonne European Nuclear Demand

Niger's contested uranium sales disrupt 6-7% of global supply, intensifying European procurement risk and driving utilities toward stable jurisdictions.

- Niger's move to nationalise uranium assets and proceed with contested uranium sales disrupts approximately 6-7% of global U₃O₈ supply, intensifying concerns over geopolitical concentration in the nuclear fuel cycle.

- European utilities, already dependent on 12,000-13,000 tonnes per annum, face heightened procurement risk as strategic inventories tighten and long-term contract prices begin incorporating new political risk premiums.

- The disruption accelerates capital rotation toward Tier-1 jurisdictions, strengthening the strategic position of uranium operators and developers in Canada, the United States, and Australia.

- Companies such as Energy Fuels (producer), enCore Energy (producer), IsoEnergy (development-stage), and ATHA Energy (exploration) benefit from jurisdictional stability, high-grade resources, and increasing utility interest in long-term contracting.

- Investors should expect tighter spot markets, more aggressive long-term contracting, and accelerated timelines for projects capable of adding secure supply during the next procurement cycle.

How Niger's Uranium Nationalisation Resets Global Supply Dynamics

Niger's decision to nationalise uranium assets and proceed with contested material sales despite International Centre for Settlement of Investment Disputes orders represents a material shift in global nuclear fuel supply chain stability. The West African nation has historically produced significant volumes of U₃O₈, accounting for approximately 6-7% of global supply, a non-trivial volume in a market where demand is locked in by existing reactor fleets and substitution is impossible. The 2023 coup and subsequent structural pivot away from Western partners increases uncertainty over future production reliability, forcing utilities and procurement strategists to reassess long-held assumptions about supply security.

Nationalisation measures implemented between June and December 2025, followed by contested uranium shipments in 2025, undermine the enforceability of international investment protections. The geopolitical realignment toward Russian involvement, formalised through a memorandum of understanding with Rosatom, signals a long-term shift in trade flows that extends beyond immediate supply disruptions. This pivot introduces competing standards for operational governance and contractual stability, effectively fragmenting what had been a relatively cohesive global uranium market governed by Western legal and commercial frameworks.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, contextualises the supply-side environment:

"The vast majority of the risk is on the supply side, and there's supply side uncertainty here… The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career."

Why This Disruption Matters for Nuclear Economies

France's dependence on nuclear electricity, which accounts for approximately 70% of total generation, and Europe's annual demand for uranium heighten systemic vulnerability to supply chain fragmentation. A 6-7% global supply disruption is meaningful because the uranium market is inelastic: demand is locked in by reactor fleets operating under multi-decade licenses, and substitutions are technologically and economically impossible. Unlike fossil fuel markets where alternatives can be mobilised during supply shocks, nuclear utilities must secure uranium supply or face operational curtailment.

European utilities are simultaneously managing the phase-out of Russian enrichment services, navigating energy security imperatives, and planning for reactor life extensions that will require sustained fuel supply through the 2040s. Niger's nationalisation removes a key supply node precisely when diversification strategies are already strained.

Supply Concentration & the Cascading Effects of Political Risk

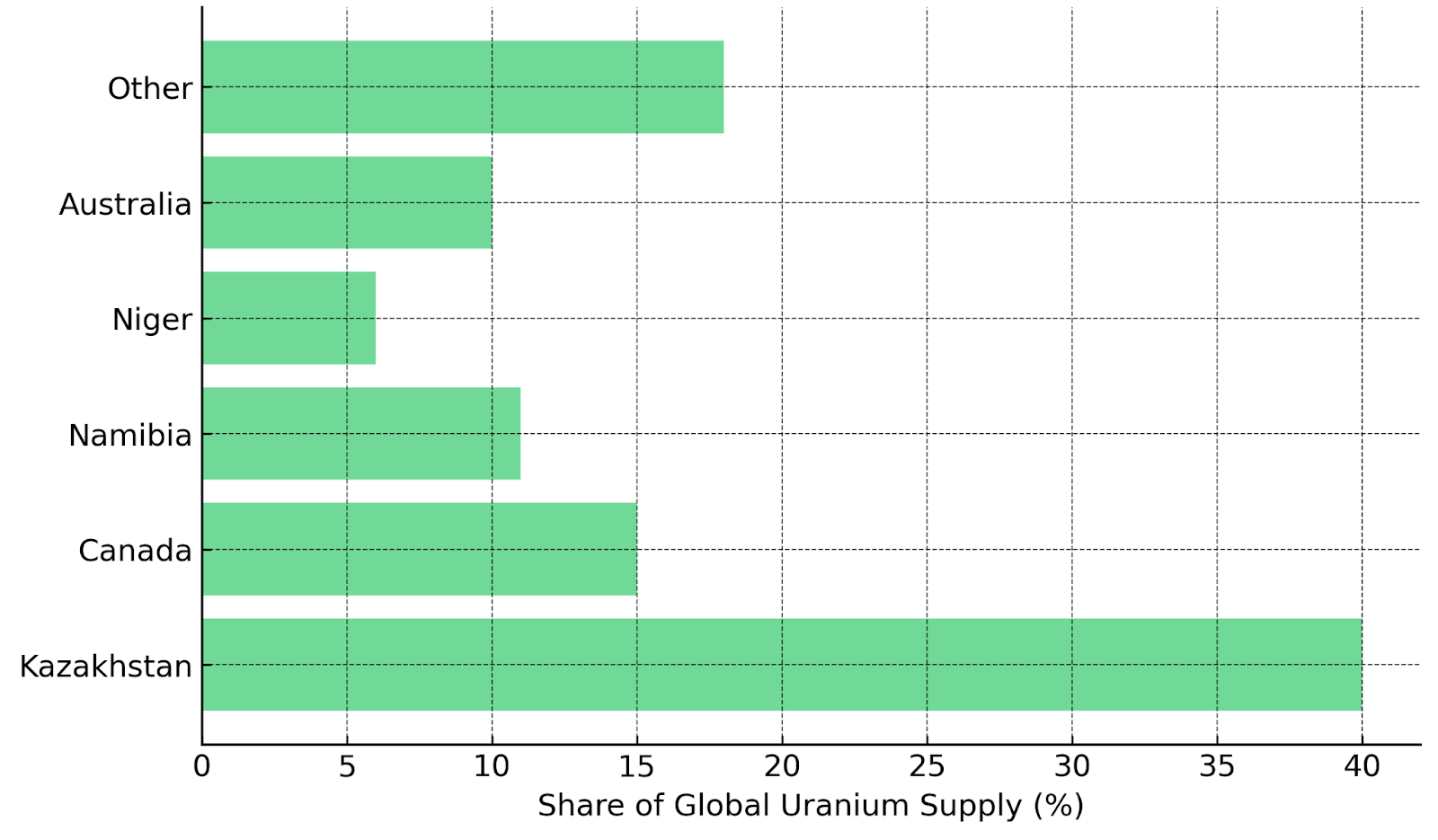

The top five producing nations, Kazakhstan, Canada, Namibia, Niger, and Australia, have historically controlled 80-85% of global uranium supply. This concentration creates cascading risk exposure: if disruptions extend beyond Niger to other top-tier producers, supply loss could reach 15-20%, materially affecting long-term pricing dynamics and forcing utilities into emergency procurement protocols. Kazakhstan's production, representing approximately 40% of global output, operates under Russian technical and logistical support, introducing additional geopolitical interdependencies that utilities must now factor into risk models.

Canada and Australia, by contrast, have historically provided jurisdictional stability backed by transparent regulatory frameworks, established mining codes, and predictable permitting processes. This divergence in political risk profiles is driving a structural repricing of uranium assets, where location now commands valuation premiums alongside traditional metrics like grade, metallurgy, and development timelines.

Geopolitical Tensions & the Weakening of Traditional Uranium Governance Structures

Niger's actions challenge global uranium governance norms that had prevailed since the sector's commercialisation in the 1970s. The breakdown of contractual stability previously provided by joint venture frameworks, where Western operators partnered with state entities under internationally recognised legal protections, signals a shift toward resource nationalism that prioritises sovereign control over commercial certainty. Selective enforcement of permits and licenses has become a tool of geopolitical alignment, highlighting how political considerations now shape project continuity.

Russia's deepened relationships in the Sahel, formalised through technical cooperation agreements and financing arrangements, reshape fuel supply routes and introduce competing standards for operational governance. Rosatom's involvement in Niger extends beyond uranium extraction to encompass enrichment services and fuel fabrication, creating vertically integrated supply chains that bypass Western commercial networks.

ICSID Limitations & the Rise of Resource Sovereignty

The International Centre for Settlement of Investment Disputes issued an interim order instructing Niger not to sell uranium from Somaïr, yet the government effectively bypassed this directive by proceeding with contested shipments. The incident signals to investors that legal protection frameworks may not prevent supply redirection in military-led or resource-nationalist governments. This erosion of investor protections raises the cost of capital for uranium projects in jurisdictions with weak governance institutions or histories of resource nationalism.

Implications for Western Utilities & Procurement Cycles

European and United States utilities typically hold inventory buffers, but as reserves decline, procurement cycles tighten, pushing utilities into earlier and more aggressive contracting strategies. This shift increases spot market exposure and amplifies price volatility during periods of geopolitical uncertainty. Utilities are responding by accelerating engagement with development-stage projects, a departure from traditional procurement strategies that prioritised established producers.

Uranium Market Mechanics: Why Disruptions Amplify Pricing Volatility

The spot market accounts for only 15-25% of global uranium trade, meaning even small supply disruptions magnify volatility disproportionately. Long-term contracts, which represent 70-80% of trade, shield utilities temporarily by locking in prices negotiated years in advance, but these contracts serve as the baseline for pricing revisions during renegotiations, transmitting spot market volatility into the broader pricing structure over time.

William Sheriff, Founder and Executive Chairman of enCore Energy, describes the supply-side challenges facing the industry:

"There's a real shortage of producers. There are a lot of wannabes, and some of those certainly will be in the near future, but I think the last year or two we've seen a lot of hurdles to that production. It's a lot easier to talk about than to actually do."

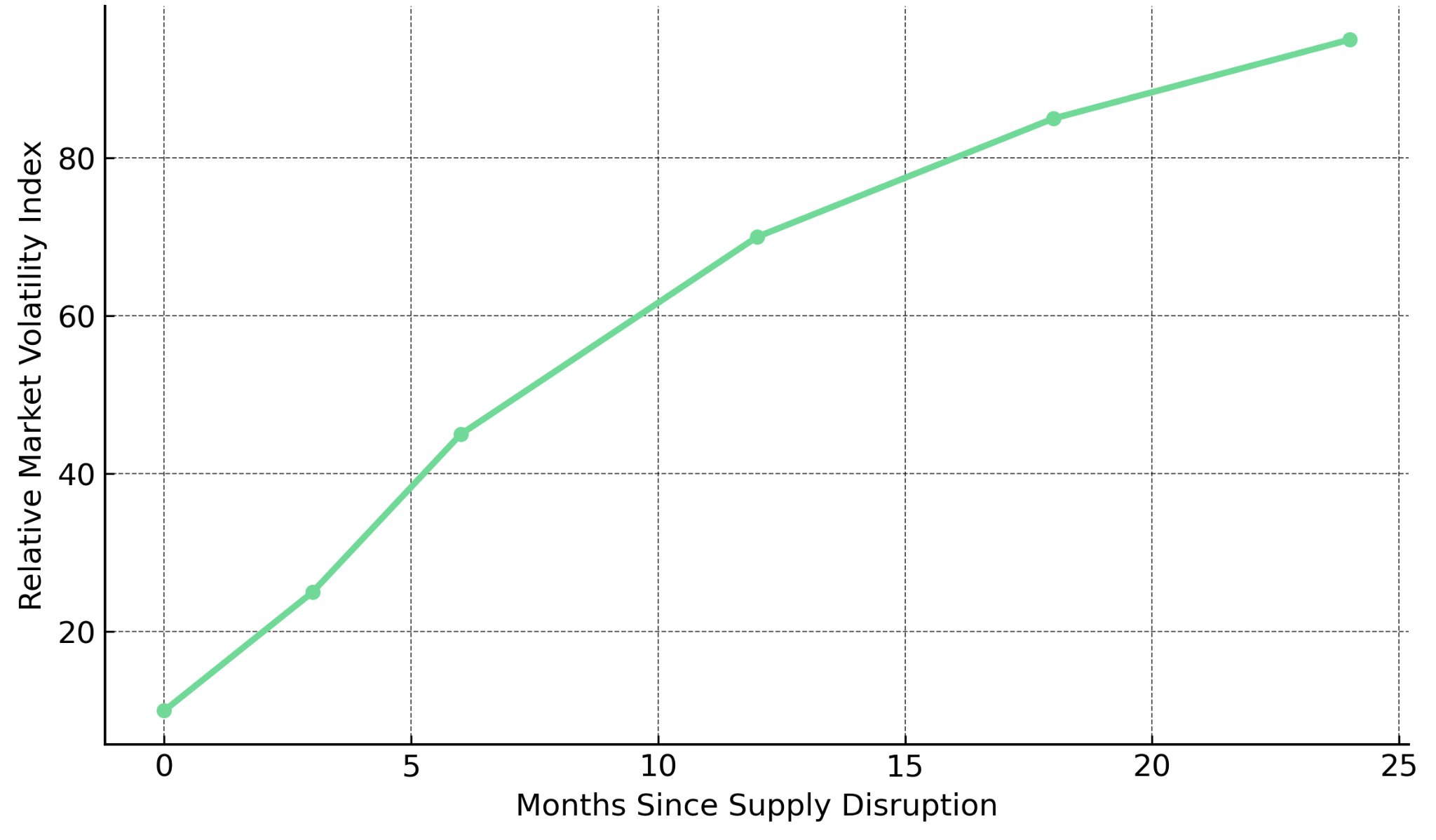

The 0-24 Month Impact Timeline for Supply Disruptions

The price transmission mechanism from geopolitical disruptions follows a predictable timeline. In the 0-6 month window following a supply disruption, utilities draw down strategic inventories while maintaining normal procurement protocols. Between 6 and 12 months, inventory buffers decline to levels that trigger increased spot purchasing, driving volatility as buyers with urgent needs accept higher prices. By the 12-24 month mark, long-term contract prices adjust upward as utilities execute new agreements or renegotiate existing terms.

Risk Premiums & the Resurgence of the Security-of-Supply Thesis

Geopolitical risk premiums are integrating into all-in sustaining cost planning, financing models, and cost-of-capital assumptions for uranium developers. Projects in jurisdictions with transparent permitting, established mining codes, and predictable regulatory frameworks command lower discount rates and attract capital more readily than equivalent-grade deposits in higher-risk regions. Utilities are now willing to accept modestly higher contract prices in exchange for jurisdictional certainty, effectively paying a premium for supply reliability.

Why Stable Jurisdiction Uranium Assets Are Being Repriced by Investors

With geopolitical risk rising, jurisdictional stability has become a key valuation driver alongside traditional metrics like grade, metallurgy, and development timelines. Assets in Canada, the United States, and Australia attract premium multiples because they reduce procurement risk for utilities constrained by long-term fuel supply commitments.

Energy Fuels: Vertical Integration & Critical Mineral Diversification

Energy Fuels operates the only conventional uranium mill currently operating in the United States at White Mesa in Utah, providing strategic infrastructure that reduces development timelines and all-in sustaining cost variability for domestic producers. As of November 2025, the facility is running at a production rate of approximately 2 million pounds of U₃O₈ per year. Mark Chalmers, President and Chief Executive Officer of Energy Fuels, describes the company's strategic positioning:

"Energy Fuels is a company that is unique from all others because we are focused on building a critical mineral hub that is built around our uranium business but also includes the rare earth suite of elements including the neodymium and the praseodymium and the dysprosium and the terbium and potentially samarium and also the heavy mineral sands which is the ilmenite, rutile, and zircon."

As well as uranium, the White Mesa Mill is the only facility in the United States with commercial capacity to process monazite for the production of high-purity rare earth oxides. This includes neodymium-praseodymium oxide (which is currently in production) and dysprosium-terbium oxides, targeted for commercial production by late 2026.

enCore Energy: ISR Scalability & Low-Cost Production

enCore Energy operates in-situ recovery projects in South Texas, with operations currently underway at the Alta Mesa Central Processing Plant, which commenced operations in the second quarter of 2024, and the Rosita Central Processing Plant. The Alta Mesa facility is configured to operate at 1 million pounds per year and is currently running at 60% of that capacity. The Rosita facility has an 800,000-pound annual capacity. William Sheriff contextualises the operational advantages:

"We're America's leading ISR firm, in-situ recovery of uranium. That's our business. We only use in-situ methods and have been in production now going on our second year and have expanded operations considerably and looking forward to a significant growth period in the near future."

Technical assessments for enCore's development pipeline indicate cash operating costs between $15.51 per pound for the Gas Hills Project in Wyoming and $19.61 per pound for the Dewey Burdock Project in South Dakota, based on preliminary economic assessments completed in 2024. In October 2025, the company announced exploration discoveries at Alta Mesa East, identifying uranium-mineralised roll fronts in at least three areas near existing wellfields.

IsoEnergy: High-Grade Assets & Development Optionality

IsoEnergy controls the Hurricane deposit in Saskatchewan's Athabasca Basin, featuring a 34.5% indicated grade and 48.6 million pounds of indicated resources, based on a technical report dated July 2022. This grade profile places Hurricane among the highest-grade undeveloped uranium deposits globally. Philip Williams, Director and Chief Executive Officer of IsoEnergy, describes the strategic rationale:

"We're focusing on the highest grade uranium resource in the world in Canada at the Hurricane deposit… We have a group of assets in the United States that could be a part of the solution to the problem. We have near-term production assets."

IsoEnergy's United States portfolio includes the Tony M Mine, Daneros Mine, and Rim Mine in Utah, all past-producing, permitted assets with near-term production potential. The company has stated these projects have toll milling arrangements in place, given their proximity to processing infrastructure.

ATHA Energy: District-Scale Exploration Leverage

ATHA Energy holds a land position exceeding 7 million acres across Canada's uranium districts, including 3.8 million acres in the Athabasca Basin, 3.1 million acres in Nunavut, and 268,000 acres in the Central Mineral Belt. The company also holds 10% carried interests in key portions of land controlled by NexGen Energy and IsoEnergy. In 2025, ATHA discovered the Mineralised Rib Corridor along a 31-kilometre trend, with drill hole RIBN-DD-001 intersecting 26.3 metres of continuous mineralisation. Troy Boisjoli describes the exploration strategy:

"The objective here is not exploration for the sake of exploration. It's exploration for discovery's sake, to move projects forward, to be extremely relevant in this cycle."

The Investment Thesis for Uranium

- Geopolitical supply concentration is raising long-term contract price floors as utilities incorporate political risk premiums into procurement strategies and financing models.

- Stable-jurisdiction producers such as Energy Fuels and enCore Energy are positioned to secure premium pricing and long-term contracts reflecting jurisdictional reliability and operational certainty.

- Development-stage high-grade assets, exemplified by IsoEnergy's Hurricane deposit, are increasingly valuable as utilities move earlier in the procurement cycle to secure future supply from low-risk jurisdictions.

- Exploration-stage optionality offered by companies such as ATHA Energy provides asymmetric upside in a structurally undersupplied market where discovery success commands disproportionate valuation premiums.

- Vertical integration and critical mineral diversification reduce operational risk and broaden revenue streams, insulating companies from uranium price volatility.

- Inventory drawdowns and accelerating contracting cycles point toward structurally tighter markets over the next 24 months, creating favourable conditions for producers and developers with near-term production capacity or clear pathways to commercial operations.

Niger's nationalisation actions are not an isolated geopolitical event but rather a structural signal of changing global alliances, weakened governance frameworks, and the return of resource nationalism to commodity markets. As a result, uranium markets are entering a phase where security of supply outweighs pure cost considerations, and where jurisdictional stability commands valuation premiums across producers, developers, and explorers. Investors should expect more aggressive long-term contracting as utilities compress procurement timelines and prioritise supply certainty over price optimisation. Capital flows into Tier-1 jurisdictions will intensify as geopolitical fragmentation persists and utilities reassess procurement strategies built on assumptions of reliable international trade flows and enforceable contracts.

TL;DR

Niger's nationalisation of uranium assets and contested sales despite International Centre for Settlement of Investment Disputes orders disrupt approximately 6-7% of global supply, creating material procurement risk for European utilities dependent on 12,000-13,000 tonnes annually. The 2023 coup and subsequent geopolitical realignment toward Russian involvement through Rosatom fragment global uranium markets and undermine international investment protections. As strategic inventories tighten and supply concentration intensifies across the top five producing nations controlling 80-85% of global output, utilities face compressed procurement cycles and political risk premiums. The disruption strengthens the strategic position of uranium operators in Tier-1 jurisdictions (Canada, United States, and Australia) where jurisdictional stability now commands valuation premiums. Companies like Energy Fuels, enCore Energy, IsoEnergy, and ATHA Energy benefit as utilities prioritise supply security over cost optimisation.

FAQs (AI-Generated)

Niger's actions disrupt approximately 6-7% of global uranium supply (4,700 tonnes annually), creating procurement risk for European utilities that require 12,000-13,000 tonnes per year. The disruption is significant because uranium demand is inelastic—locked in by existing reactor fleets with no substitution possible—and comes when European utilities are simultaneously managing the phase-out of Russian enrichment services and planning reactor life extensions through the 2040s.

In September 2024, ICSID issued an interim order instructing Niger not to sell uranium from the Somaïr mine. Niger proceeded with contested shipments in November 2025 despite this order, effectively bypassing international legal protections. The military government characterises these sales as exercising legitimate sovereignty over natural resources, while previous operator Orano maintains that contractual agreements and international arbitration protections remain binding, creating an active legal dispute over resource sovereignty versus investment protections.

Companies in Tier-1 jurisdictions (Canada, United States, Australia) benefit from jurisdictional stability backed by transparent regulatory frameworks, established mining codes, and predictable permitting processes. As geopolitical risk premiums integrate into procurement strategies, utilities are willing to accept modestly higher contract prices in exchange for supply reliability. Assets in these jurisdictions now command valuation premiums because they reduce procurement risk for utilities constrained by long-term fuel supply commitments.

The top five producing nations—Kazakhstan (40%), Canada (20%), Namibia (6-8%), Niger (6-7%), and Australia—control 80-85% of global uranium supply. If disruptions extend beyond Niger to other top-tier producers, supply loss could reach 15-20%, materially affecting long-term pricing and forcing utilities into emergency procurement protocols. Kazakhstan's production operates under Russian technical support, introducing additional geopolitical interdependencies that amplify systemic vulnerability.

Price transmission follows a predictable pattern: In the 0-6 month window, utilities draw down strategic inventories with minimal price impact. Between 6-12 months, inventory buffers decline, triggering increased spot purchasing and driving volatility as buyers with urgent needs accept higher prices. By 12-24 months, long-term contract prices adjust upward as utilities execute new agreements or renegotiate existing terms, transmitting spot market volatility into the broader pricing structure.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed