COMEX–LME Premium Decline Ends Policy Distortions & Re-anchors Copper Pricing to Supply and Demand

COMEX-LME premium collapse ends copper policy distortion, triggering 20% price drop. Strategic positioning favors ESG-compliant projects in Tier-1 zones.

- The collapse of the COMEX–LME premium marks the end of a policy-driven distortion, forcing copper markets back toward fundamentals.

- A U.S. tariff exemption triggered a 20% copper price correction, a surge in U.S. inventories, and the unwinding of speculative arbitrage flows.

- Investors face near-term volatility from oversupply while longer-term demand anchors, electrification, AI infrastructure, and decarbonization, remain intact.

- Structural supply constraints continue to favor projects with scale, low-carbon intensity, and secure jurisdictional positioning.

- Companies such as Marimaca Copper (Chile), Gladiator Metals (Canada), and Fitzroy Minerals (Chile/Argentina) are strategically aligned with investor priorities in the new equilibrium.

Policy Distortions Unwind, Market Returns to Fundamentals

The dramatic collapse of the COMEX–London Metal Exchange premium in late July 2025 represents a watershed moment for global copper markets, marking the end of an artificial pricing distortion that had reached unprecedented levels. The premium, which had widened to over 28% between COMEX and LME copper futures, evaporated virtually overnight following the U.S. Treasury's announcement of a tariff exemption on refined copper imports.

The July 30, 2025 tariff exemption on refined copper removed the primary arbitrage driver that had sustained the extraordinary premium for months. This policy shift immediately triggered a realignment of global trade flows, as market participants rapidly unwound positions that had been profitable under the distorted regime. The announcement caught many investors off-guard, highlighting the inherent risks of policy-dependent trading strategies in commodity markets.

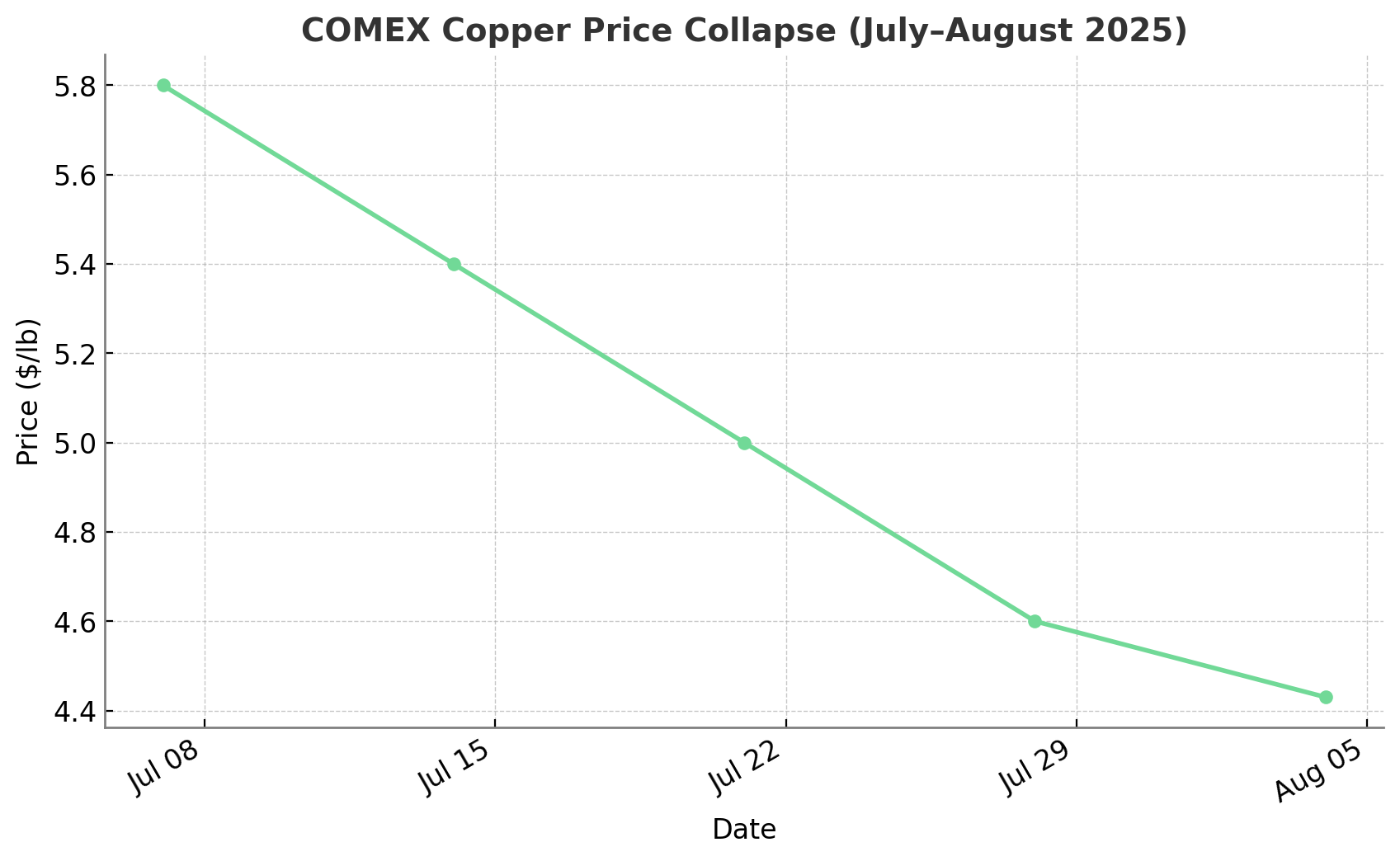

The immediate market shock was severe. COMEX copper prices dropped 20% in less than four weeks, falling from $5.80 per pound to $4.43 per pound as speculative positions unwound and inventory dynamics shifted. This correction eliminated approximately $1.4 billion in paper profits from hedge funds and other speculative participants who had been positioned to capture the premium spread.

The unwinding process revealed the extent to which policy uncertainty had distorted natural market mechanisms. U.S. copper inventories surged by over 600,000 tonnes as previously redirected shipments found their way to American warehouses, creating several months of excess supply relative to normal consumption patterns.

Unpacking the Drivers Behind the Spread

Tariff Fears and Distorted Flows

The COMEX–LME premium originated from anticipation of a potential 50% tariff on copper imports, prompting traders to redirect copper shipments from traditional Asian destinations to U.S. ports. This artificial demand surge transformed the United States into what market analysts described as an "artificial demand sink," absorbing copper that would have otherwise flowed to established industrial consumption centers.

The policy uncertainty created a feedback loop that amplified the premium. As traders positioned for potential supply constraints in the U.S. market, their buying activity pushed COMEX prices further above LME levels, justifying additional speculative flows. This self-reinforcing mechanism divorced copper pricing from underlying supply-demand fundamentals for the better part of six months.

Speculative Positioning on COMEX

Hedge funds and other speculative participants recognized the arbitrage opportunity early, building substantial long positions in COMEX futures while shorting equivalent LME contracts. This positioning amplified the price split between the two exchanges, as speculative flows began to dwarf commercial hedging activity in the COMEX copper market.

The concentration of speculative interest created dangerous liquidity imbalances. During peak premium periods, speculative net-long positions on COMEX exceeded 200,000 contracts, representing approximately 3 billion pounds of copper, roughly equivalent to three months of U.S. refined copper consumption.

Arbitrage Incentives and Cargo Movements

Physical traders exploited the premium through complex cargo arbitrage strategies, purchasing copper in traditional markets and shipping it to U.S. ports for premium capture. These trades pushed the spread beyond levels that could be justified by transportation costs, storage expenses, or financing requirements.

The arbitrage mechanics became increasingly sophisticated, with participants using warehouse financing, cross-currency hedging, and complex shipping arrangements to maximize returns from the distorted pricing environment. Once the tariff exemption was announced, these trades unwound rapidly, contributing to the sharp price correction and inventory buildup.

Immediate Consequences for Copper Markets

The 20% price drop in COMEX copper futures created immediate challenges for market participants across the supply chain. Mining companies faced margin compression as their hedging strategies, often calibrated to pre-correction price levels, became misaligned with new market realities. Equipment suppliers and service providers experienced sudden project deferrals as miners reassessed capital expenditure priorities.

Increased volatility has become a persistent feature of the post-correction environment. Daily price swings exceeding 3% have become commonplace, requiring adaptive hedging strategies from both producers and consumers. This volatility premium has increased options pricing and complicated long-term planning for industrial consumers.

Inventory Surge in U.S. Warehouses

The rapid accumulation of over 600,000 tonnes of refined copper in U.S. warehouses represents several months of normal consumption, creating substantial downward pressure on near-term pricing. This inventory overhang must be absorbed through natural demand growth or export to deficit regions before normal market dynamics can resume.

Warehouse operators have reported utilization rates approaching capacity limits in key storage locations. The geographic concentration of excess inventory has created regional pricing distortions within the U.S. market, with delivered copper prices varying significantly based on proximity to major storage facilities.

Arbitrage Reversal and Trade Route Realignment

The collapse of the premium triggered immediate reversals in established trade routes. Copper cargoes that had been destined for U.S. ports were either diverted to alternative markets or placed in temporary storage pending favorable pricing windows. Some traders executed costly cargo diversions mid-transit, accepting significant losses to minimize exposure to further premium erosion.

Export flows have resumed from the United States to traditional deficit regions, though at reduced premiums reflecting the elimination of artificial scarcity. Investors are recalibrating their trade flow models to account for normalized shipping patterns and the removal of policy-driven demand distortions.

Re-anchoring to Real Supply and Demand

China's copper consumption, representing over 50% of global demand, has shown concerning weakness throughout 2025. Housing completions declined 8% year-over-year in the first seven months, while manufacturing output growth slowed to 4.2% compared to the previous year's 6.8% pace. Solar installation activity, a significant copper consumer, decreased 15% as policy support waned and grid interconnection bottlenecks persisted.

The Chinese government's infrastructure stimulus programs have yet to materially impact copper-intensive sectors. Railway electrification and grid modernization projects, while announced, have faced delays in funding allocation and regulatory approval. This demand uncertainty has complicated inventory management for both Chinese and international copper suppliers.

Currency and Federal Reserve Policy

The U.S. dollar's strength throughout 2025 has maintained downward pressure on dollar-denominated commodities, including copper. Dollar Index levels above 104 have made copper more expensive for non-U.S. buyers, dampening international demand and contributing to inventory accumulation in dollar-zone markets.

Expectations of Federal Reserve rate cuts in autumn 2025 could provide relief for industrial metals, though the timing and magnitude of policy easing remains uncertain. Forward markets are pricing in 75-100 basis points of cuts by year-end, which would typically support copper prices through reduced financing costs and dollar weakness.

Structural Supply Challenges

Despite short-term oversupply pressures, longer-term supply fundamentals remain constrained. Global copper ore grades have declined from 0.62% in 2000 to 0.47% in 2024, requiring increased mining volumes to maintain production levels. Permitting timelines for new projects have extended to an average of 8.2 years in major jurisdictions, creating significant barriers to supply growth.

Environmental, Social, and Governance requirements have elevated development costs and extended feasibility study timelines. Projects must now demonstrate carbon intensity reductions, water usage optimization, and community engagement protocols that were not required in previous development cycles.

Chief Executive Officer Hayden Locke of Marimaca Copper emphasizes this strategic advantage:

"The company's focus is on high acid soluble mineralization that delivers better recoveries through our integrated processing approach"

Implications for Investors

Copper prices face continued pressure as U.S. inventories normalize through the remainder of 2025. The 600,000-tonne overhang requires either accelerated consumption or export flows to clear, creating tactical challenges for investors seeking optimal entry points.

Risk management strategies must account for potential further corrections if Chinese demand continues underperforming expectations or if additional inventory releases pressure spot markets. Conservative positioning suggests waiting for clearer demand signals before establishing full strategic allocations.

Medium-Term Arbitrage Opportunities

Regional price spreads are likely to remain elevated as markets adjust to post-distortion dynamics. Sophisticated investors can capitalize on cross-market positioning strategies, though these require detailed understanding of shipping logistics, warehousing costs, and regulatory frameworks across multiple jurisdictions.

Currency hedging has become increasingly important as exchange rate volatility affects relative pricing between regional markets. The correlation between copper prices and major currency pairs has intensified, creating additional complexity for cross-border arbitrage strategies.

Long-Term Structural Bullishness

Fundamental demand drivers remain robust despite near-term oversupply concerns. Electrification initiatives across major economies continue expanding, with grid infrastructure investments exceeding $300 billion annually. Electric vehicle adoption is accelerating in key markets, while artificial intelligence data center buildouts are creating unprecedented copper demand from power infrastructure and cooling systems.

Copper intensity per capita is projected to increase significantly in developed markets due to energy transition policies. The International Energy Agency estimates that achieving net-zero emissions targets will require 30% more copper production by 2030 compared to current output levels, highlighting the structural supply-demand imbalance emerging over the medium term.

Marimaca Copper: Financeable Green Copper in Chile

Marimaca Copper represents a compelling development opportunity in Chile's established mining jurisdiction. The company is nearing completion of its Definitive Feasibility Study for the MOD copper project, which demonstrates attractive economic metrics with capital expenditure of $587 million, All-in Sustaining Costs of $2.09–$2.29 per pound, and Internal Rate of Return of 31%.

The project's environmental profile positions it favorably for ESG-focused institutional investors. Marimaca has secured recycled seawater supply agreements and certified renewable electricity access, achieving 38% lower carbon intensity compared to traditional copper processing methods. This positioning addresses growing institutional requirements for sustainable commodity exposure.

Recent exploration success at the Pampa Medina satellite deposit has expanded the company's resource base significantly. Chief Executive Officer Hayden Locke notes the strategic importance of this discovery:

"We are nearing the completion of our DFS and we've just put out stellar drill results at our Pamper Medina project area"

The company's measured and indicated resources now represent 86% of total resource tonnes, providing confidence for debt financing discussions. Institutional backing from Mitsubishi Corporation and Assur International demonstrates sophisticated investor validation of the project's technical and financial merits.

Gladiator Metals: High-Grade Yukon Copper Belt

Gladiator Metals has positioned itself within Canada's established mining framework through its Whitehorse Copper Project in Yukon Territory. The 35-kilometer copper belt benefits from historical production data from Hudbay Mining's operations, which extracted 10-12 million tonnes at 1.5% copper with significant gold by-product credits.

The company's focus on the Cowley Park prospect reflects disciplined capital allocation toward the highest-grade portions of the copper belt. Technical analysis indicates potential for 15-20 million tonnes at 1.5% copper from surface, supporting low-strip-ratio development scenarios that enhance project economics.

Infrastructure advantages differentiate the Whitehorse project from remote development opportunities. Highway access, established power infrastructure, and proximity to Whitehorse City provide operational cost advantages and reduce execution risk. Year-round drilling capability accelerates exploration timelines compared to seasonal access restrictions common in northern jurisdictions.

Chief Executive Officer Jason Bontempo emphasizes the project's scalability:

"We have over 100 million tons at above 1% copper not including any credits"

The company maintains a strong financial position with C$15 million in treasury, supporting an aggressive exploration program targeting a maiden resource estimate in Q1 2026. This timeline positions Gladiator for potential development decisions during the anticipated copper supply shortage in the late 2020s.

Fitzroy Minerals: Scalable Oxide and By-product Leverage

Fitzroy Minerals has assembled a portfolio of copper projects across Chile and Argentina that emphasize near-term development optionality and critical mineral by-product exposure. The Buen Retiro Iron Oxide Copper Gold system features near-surface oxide mineralization well-suited for heap leach processing, offering lower capital intensity compared to conventional sulfide developments.

The company's strategic approach emphasizes toll processing agreements to minimize development capital. A potential partnership with Pucobre, which operates an underutilized solvent extraction-electrowinning plant 90 kilometers from Buen Retiro, could eliminate approximately $40 million in capital expenditure while accelerating time to first production.

Chief Executive Officer Merlin Marr-Johnson highlights the operational flexibility this provides:

“The Buen Retiro IOCG system offers low-capital expenditure optionality as US manufacturers prioritize feedstock diversity"

The Caballos project adds significant value through by-product diversification. Recent drilling has identified a copper-molybdenum-gold-rhenium system with molybdenum grades substantially exceeding typical Chilean porphyry deposits. Molybdenum's strategic importance for steel production and aerospace applications provides additional revenue stability during copper price volatility.

Rhenium occurrence at Caballos addresses critical mineral supply concerns, with Chile representing the world's second-largest rhenium producer. Aerospace and defense applications for rhenium create stable demand from strategic buyers willing to pay premium prices for secure supply relationships.

With over 12,000 meters of drilling planned for 2025 and C$5 million in treasury, Fitzroy maintains aggressive exploration momentum across multiple targets. This diversified approach reduces single-asset risk while maximizing exposure to potential discoveries across two established mining jurisdictions.

The Investment Thesis for Copper

The copper market's return to fundamental pricing creates both challenges and opportunities for strategic investors. Policy distortion has ended, forcing markets to price based on underlying supply-demand dynamics rather than artificial arbitrage opportunities. This transition, while temporarily painful, establishes a more stable foundation for long-term investment strategies.

- Short-term oversupply pressures require careful timing of entry positions. Inventory builds in U.S. warehouses will weigh on prices until natural consumption or export flows restore normal stock levels. Conservative investors may prefer waiting for clearer inventory normalization signals before establishing full allocations.

- Structural demand fundamentals remain compelling despite near-term headwinds. Electrification mandates across major economies, artificial intelligence infrastructure buildouts, and grid modernization requirements anchor long-term copper intensity growth. The International Energy Agency projects 30% higher copper production requirements by 2030 to meet decarbonization targets, creating substantial supply-demand imbalances over the investment horizon.

- Scarcity value increasingly favors projects in established mining jurisdictions with transparent regulatory frameworks. Declining ore grades globally and extended permitting timelines elevate the strategic importance of Tier-1 jurisdictions like Chile, Canada, and Spain. These locations offer regulatory predictability, established infrastructure, and political stability that justify valuation premiums during uncertain market periods.

- Strategic company positioning within this framework favors developers with specific competitive advantages. Marimaca Copper offers low-cost, ESG-compliant development with near-term production potential and strong institutional backing. The company's definitive feasibility study completion and advanced permitting position it for debt financing and construction decisions during the anticipated supply shortage.

- Gladiator Metals provides exposure to high-grade copper resources in Canada's stable regulatory environment. The Whitehorse project's infrastructure advantages and historical production data reduce execution risk while the company's strong treasury position supports aggressive exploration toward a maiden resource estimate. The Yukon location offers year-round operational capability and established mining services infrastructure.

- Fitzroy Minerals delivers scalable oxide development optionality with critical mineral by-product diversification. The company's toll processing strategy minimizes development capital while rhenium and molybdenum exposure provides revenue stability during copper price volatility. Multi-jurisdictional positioning across Chile and Argentina reduces single-country risk while maintaining access to established mining frameworks.

- Risk-adjusted positioning favors companies with demonstrated management execution, appropriate financing, and technical advantages that remain valuable regardless of short-term price movements. The policy-driven distortion's collapse serves as a reminder that sustainable investment strategies must be anchored in fundamental project economics rather than temporary market inefficiencies.

A New Risk Adjusted

The collapse of the COMEX–LME premium demonstrates the inherent instability of policy-driven market distortions and underscores the importance of fundamentals-based investment strategies. While the correction has created near-term challenges for copper markets, it has also eliminated artificial pricing mechanisms that obscured true supply-demand dynamics.

Copper markets are recalibrating by structural demand growth, supply constraints, and evolving regulatory frameworks across key jurisdictions. The elimination of policy distortions allows investors to focus on companies with genuine competitive advantages rather than those positioned primarily to capture temporary arbitrage opportunities.

The copper market's return to fundamental pricing creates a more stable foundation for long-term investment strategies, even as short-term volatility persists. Investors who maintain discipline during the current oversupply period while building positions in strategically aligned development opportunities should benefit from the structural supply-demand imbalance that continues building beneath current market noise.

Analyst's Notes

Subscribe to Our Channel

Stay Informed