Condor Gold (CNR, COG) - Production, Nothing Else Matters at This Point

Interview with Mark Child, CEO of Condor Gold

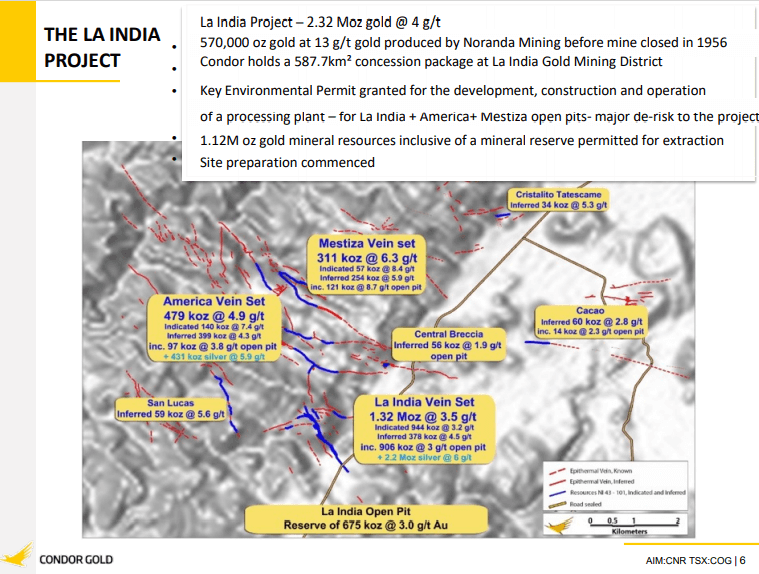

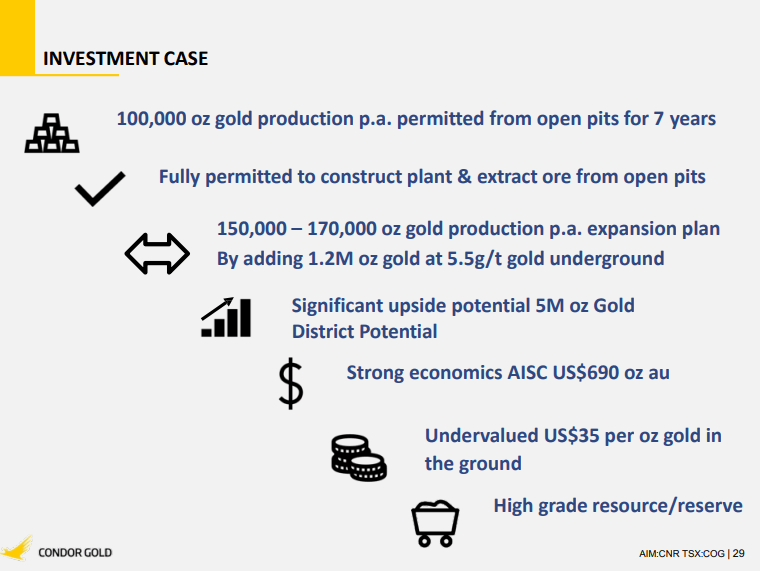

Mark Child is Chairman and CEO of Condor Gold Plc, a UK based AIM and Toronto listed exploration company. They have 2.4Moz of Gold in their 100% owned La India Project in Nicaragua. The project there is fully permitted to construct and operate a mine. Currently, Condor Gold is also looking to demonstrate a 5Moz Gold district.

Jurisdictions, Revenue Generators, & International Investors’ Perspectives

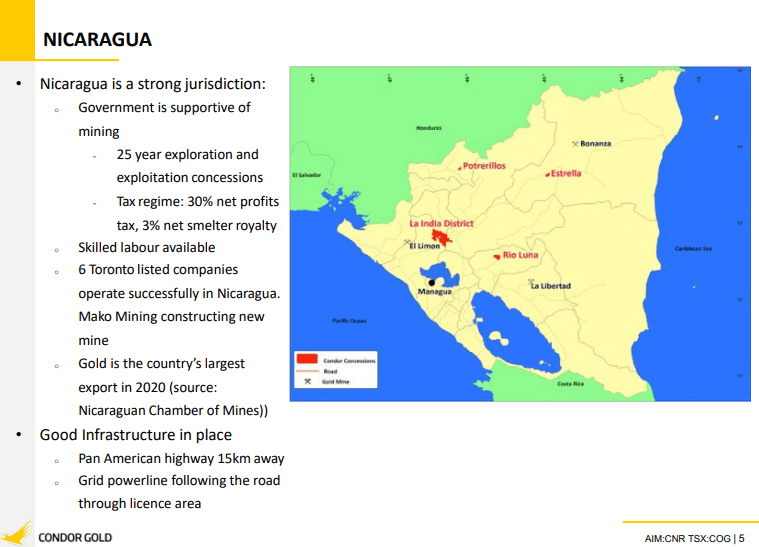

La India is a mining jurisdiction and Condor Gold has operated there for 15 years. Mark has been full time CEO of the company for 10-years and 25% of his time is spent in Nicaragua. Since Mark started, Gold has increased to become the number one export for the country, from last year. There are now 5 commercial mines in the country, with an artisanal mining community. The government has been permitting everything, which helps the project economics. There’s also a 25-year concession for exploration and exploitation. The government helps out on certain issues faced when mining, mainly around communing and land acquisition challenges. They also value the taxes, exports and jobs that are created from mining, so it is a good region to be in.

Condor Gold has projects across Central and South America, which are producing revenue. From a mining perspective, the company is getting on with it, however there are political issues in Nicaragua, which create political risk associated with the project. President Ortega is standing for a 4th term, which sends a negative signal as it confirms allegations of a lack of free and fair elections to be correct. The party controls most organs of the state including the military, police and judiciary. There have been US sanctions against individuals within Nicaragua. This has been reflected in the value of Condor Gold’s share price. However, as long as companies understand the local law of regimes like Nicaragua’s, they can successfully operate there. Half a dozen foreign companies operate successfully in the region and the currency is fully convertible; get paid dividends and repatriate capital.

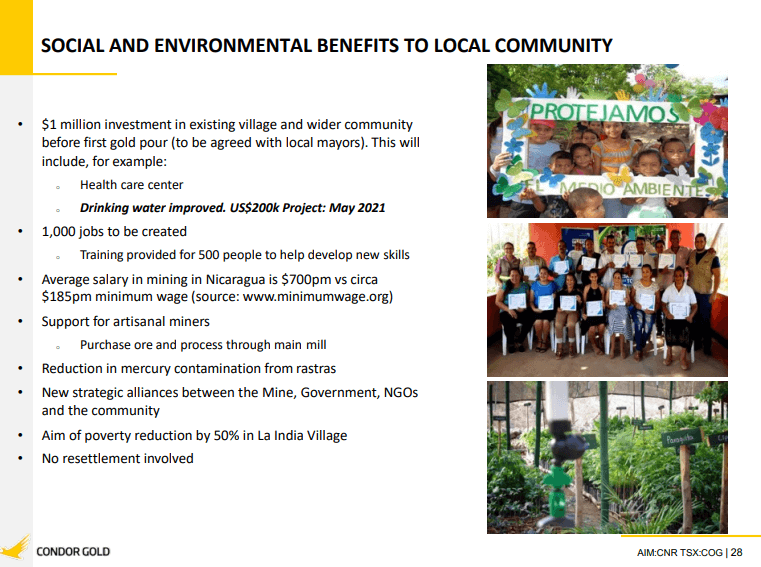

Multiple countries in South America have had elections which create a narrative not conducive to international investment. However, for Condor Gold’s operation in Nicaragua, they will do everything to the IFC performance standards and equator principles. They want to be an industry leader for the way mining should be conducted on their environmental emissions. They have already committed to tree nurseries and spending $20,000 a month on the community, and have spent over $200,000 to put up a water project. It is up to the leadership of the company to decide what to do on an ESG perspective, not the election narrative. In spite of elections, Nicaragua has a Ministry of the Environment. The country produces 75% of electricity using green methods like geothermal, wind and hydropower, due to the absence of oil. Condor Gold has environmental permits to construct and operate the mine and do 16 different technical studies.

Looking at the risk appetite for foreign investors and institutions, Condor Gold has $2.4Moz of Gold in the ground, which is close to $4bn in situ. Condor Gold is moving into the construction phase and plans to raise money for this endeavour and secure the debt against the asset. Issues encountered in the country doesn’t stop financiers lending to the US because Gold is an 8 trillion-dollar currency which can be secured against future revenue streams. It comes down to the IRRs, NPVS, cash flows and breakeven all-in sustaining cash costs. However, the riskier the country, the quicker the payback on the project should be. Condor Gold is looking for a 12-18 month payback, which they will demonstrate when they update their studies next month.

Working with Investors, Current Projects, & Years of Progress

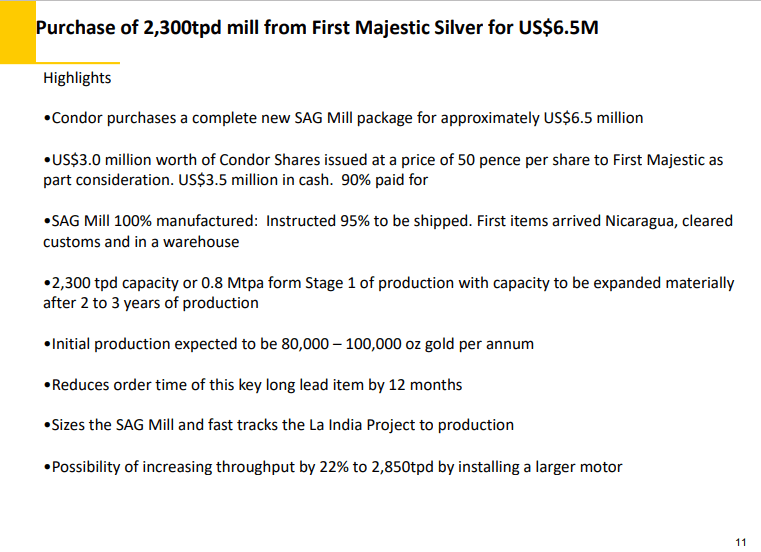

The strategy for Condor Gold is to construct and operate the mine and this year they bought a brand new SAG mill off First Majestic Silver at a cost of $6.5M. Condor Gold issued $3M of paper at 50p for that and the share price currently stands at around 45p. It is a slight premium for the company and the balance was paid in cash. The mill is made by Metso Outotec in Finland. It has a variable drive on the motor and can either use 24 for the environment, which can process 2300t a day. The items are being shopped into Nicaragua and 9 have been cleared into the country. This is a signal to the government that Condor Gold is serious about the construction phase.

They plan to release a PEA to show the different scenarios of what the project can do in 3 to 4 weeks. This will show a total open-pit scenario from 4 open pits plus underground. The main pit will produce over 600,000oz of Gold. Their PFS was 670, all in sustaining cash costs. That’s a lower quartile globally with over 3 grand pits. Therefore, it is very high-grade and economical. If Condor Gold adds 4 pits together, they will produce about 900,000oz of Gold. They also have 1.2Moz underground, which can be layered in those productions.

Going forward, they will do stage 1, which will be a minimum Capex and cash flow based high grading with quick payback based on the recently purchased mill. After 2 years, this will be expanded. They have appointed an engineering firm that is doing the FS level designs which will be with Mark at the end of August. It will be laid out so that they can double the capacity of the plot. A new Capex number will be given at this time too.

In December 2014, Condor Gold put 2 PEAs out and a PFS on the open pit. Gold at the time was 1400, peaked at around $1,900/oz and then it dropped by 42%. That ended the chronic bear market for their underlying metal in both Gold and Silver. In that period there was no point drilling to get it to 5Moz, as they already had 2.4Moz in reserves.

The company then went ahead with applications for permitting. In 2016 they applied for the main pit to be permitted and hit a setback with the community which had 40% poverty. The government agreed they could be resettled, however Condor Gold experienced resistance, with a demonstration at their public hearing. The villagers did not want to be resettled. Therefore, the management team redesigned their plans and shortened the pit by 20%, and lost 8% of the Gold there. They have put a big barrier of 5-10m high between the pits and the community and then reapplied for permits again and changed the senior manager to a mining engineer from the nearby El Limon mine, an hour drive away who’s a Nicaraguan.

The main pit was permitted in 2018. In August that year, Condor Gold had a setback linked with the permitting permits. The local community voted against the project the first time. Since then, they have been permitted to make it bigger with 1.12Moz permitted, with the last of the permits coming through last year. Typically, permits take 2 years, and this is part of the 16 technical studies on the environment. Once the final permits come in, they will conduct a western style bankable Feasibility Study, so lenders will provide financing.

Finances & Available Options

The 2.4Moz of Gold breaks down at 1.2M open-pitable and 1.2M underground. Condor Gold will not mine underground. This makes the 1.2M open-pitable, with 3 pits permitted containing 1.12Moz. They’ve got 90% of the open-pit material permitted to extract. 80% is indicated in the higher category. The mill was built to facilitate the construction of metal at 2300t a day and the apex will be around that. This will produce about 100,000oz of gold a year. This is financed off by the main open-pit with 80% of the permitted oz.

The underground won’t be drilled out as there’s a million oz beneath the bit, so it's much deeper and more expensive drilling. They will do drilling at a cash flow once they go into production. When it comes to getting enough finance, Condor Gold will provide banks full and quarterly mining schedules. Mark believes they will provide the indicated 80% from this. For the remaining 20% Condor Gold will highlight the probability of more info drilling into the M&I, however the project can be financed without this. Condor Gold just completed a 3700m of drilling in the La India open-pit, with results coming in shortly. They’re high grading, with the highest 10% being taken from the surface, which works at 60,000oz at the higher grade of about 4.2g. That is the last drilling the company needs to do ahead of extracting, which gives the first 6-months mill feed.

Underground Component, ASIC, & High Grading

There is 445,000t at 4.2g per 60,000oz of the main pit, which is less than 10%. Senior Management wants quick payback and therefore will put high-grade through earlier to pay back debt.

The ASIC is PFS level, which is good. Since 2014, they have done different tests, particularly on the MWI index and abrasion indices. They currently have 1000kg of rock sitting in a lab in Toronto, Canada, SGS and that brings them to an FS level metallurgy. The lab results are due back in a month. They are at 91% metallurgical recovery and are getting weekly reports from these stating no negative surprises. The mine history indicates they managed to get Gold out of the host rock for 15 years and produce 0.5Moz of Gold.

Financial Situation, Short-Term Business Plan, & Long-Term Business Plan

Currently, Condor Gold has £3M Sterling. They will need to have financing before the end of the year and will go to the market to do so. Mark Child and Jim Mellon, the directors of the company, own 22% of Condor Gold’s shares. As they have a stake in the £6M business, they are concerned with dilution and totally motivated by creating shareholder value. Between them, they have a lot of contacts who have supported the company over the last 10 years.

Value creation is down to getting permits. The market may not have recognised this with Condor Gold but a project without a permit cannot get the Gold out. In Nicaragua, they have political risk which is just a frontier market element that Mark accepted when he invested into the company. Risk is a common feature with a country with low GDP per capita, which is $1,912 in Nicaragua. Despite this, Condor Gold’s share price has doubled in 18 months. They bought 97% of the land from over 60 landowners and had a good team of 4 lawyers to see this through. The remaining 3% is owned by 5 separate landowners, but this is a non-risk issue for Condor Gold.

Quantum, Project Economics & Getting a Head Start

Financing will occur in 2 stages. One element will see Condor Gold through the FS and finalisation and beyond, with some headroom. The second stage is the main construction financing which will happen next year.

Condor Gold will raise some money for stage 1 over the next 3 to 4 months. The FS study will not be out until the end of the year or in 6 months’ time. In terms of bank debt, they have to wait for that to happen before they specify their Capex and FS.

The company will put out another PEA to update it to the 1550 gold price. The project has also changed materially due to redesigns. Mark believes when investors see the project’s NPV, it will be highly attractive to them.

With the PFS, PEA, mill purchase and $4M buyout of land, the project has changed materially. Under regulations, they need to update the project or the current state of knowledge due to what’s happened over the last 6.5 years.

Exploration, Drilling, Timeline & Creating Value

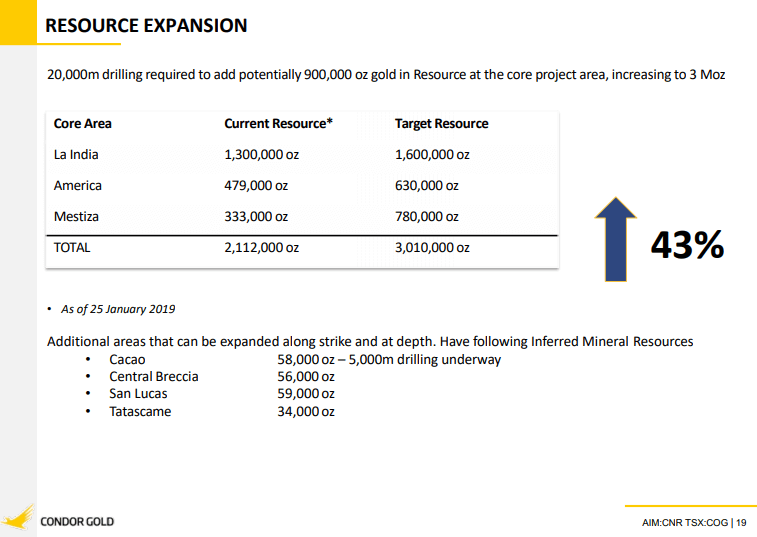

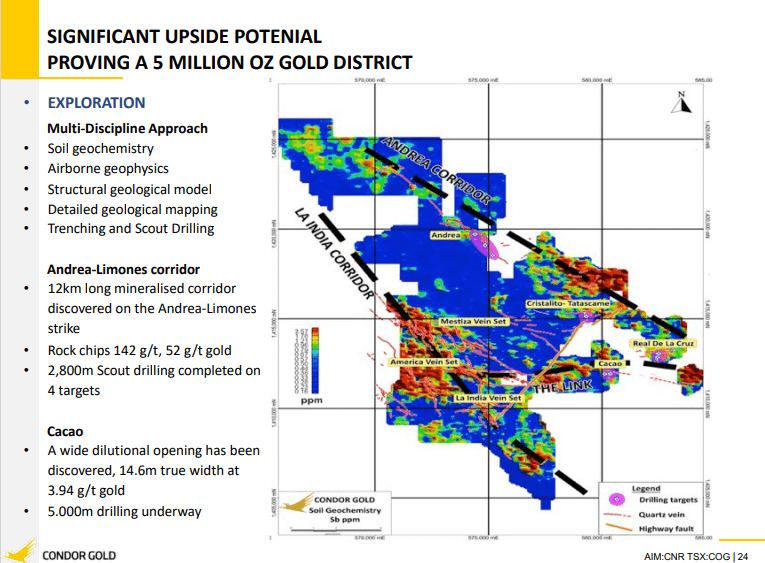

80% of Condor Gold’s money is going on the strategy construct and operate line due to their capital intensiveness. Part of the strategy is to demonstrate a 5Moz district and they have already completed 3600m. Under the 3 permitted pits, they can add 900,000oz. They haven’t so far as it’s 400m down which is expensive to drill. There are plans to develop this and have doubled the land package over the last 7-years on the project. This makes up to 580sq.km of adjacent and contiguous concessions.

They’ve got 2 major regional faults that they have flown with helicopter surveys, and have done soil sampling over 300sq.km of the Gold structural geological models. They’ve also walked it with over 110km of veining on the surface. It is a very large Gold District.

At Cacao, Condor Gold has a resource of 60,000oz which they’ve drilled and have come back with the opening. On the exploration side, they are looking for a structure with a wide opening of 15m at 4g. They are trying to show this and demonstrate the strike length of around 3000m. In La India, they have 1.3Moz, which changes the project entirely.

In terms of timing, the company is not planning to get a quick win to get to 2M of M&I over the next two years. They are focused on producing cash. They have a fully diluted mill feed. Out of those, 3 fully permitted pits of 8.5Mt, which is an eight-year mine life, followed by the 100,000oz of Gold at 1700 Gold’s $170M. With 700 all in sustaining, they have $100M of free cash flow. Mark believes it is a very good project. Once they have these cash flows coming in over the two year period, they will double their measured and indicated to get the banks more interested. In frontier markets like Nicaragua, the strategy is to prove they can build the mine, prove they can operate it and then double that production to 200,000 in year 3. Mark believes this is what creates the value without diluting the shareholders.

To find out more, go to the Condor Gold Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed