Consolidated Uranium (CUR) - Focus on Buying Up Near Term Producers

Interview with Phillip Williams, President & CEO of Consolidated Uranium

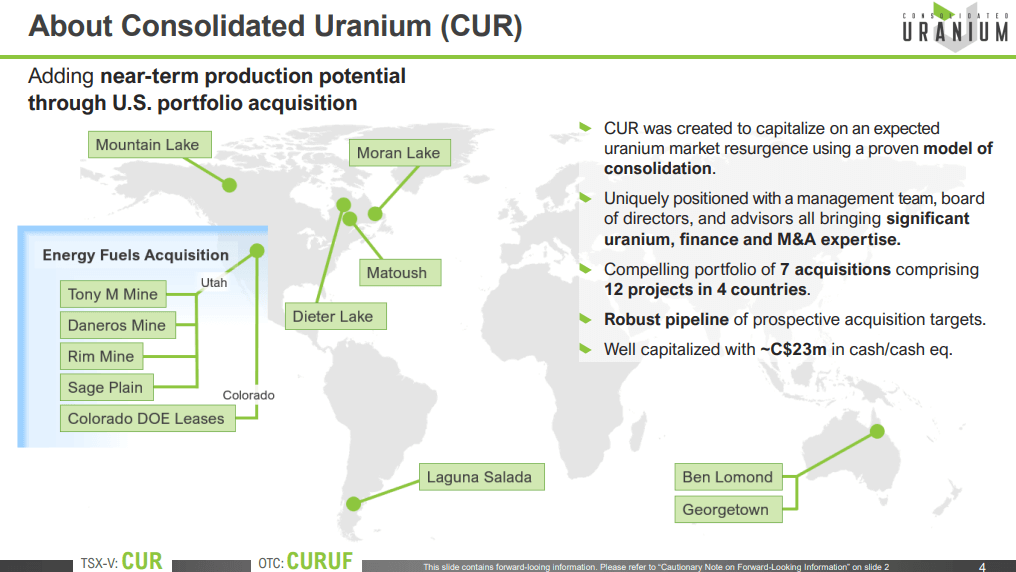

Consolidated Uranium is a new entrant to the space, created in early 2020. The company's focus is to capitalize on an anticipated uranium market resurgence using the proven model of diversified project consolidation.

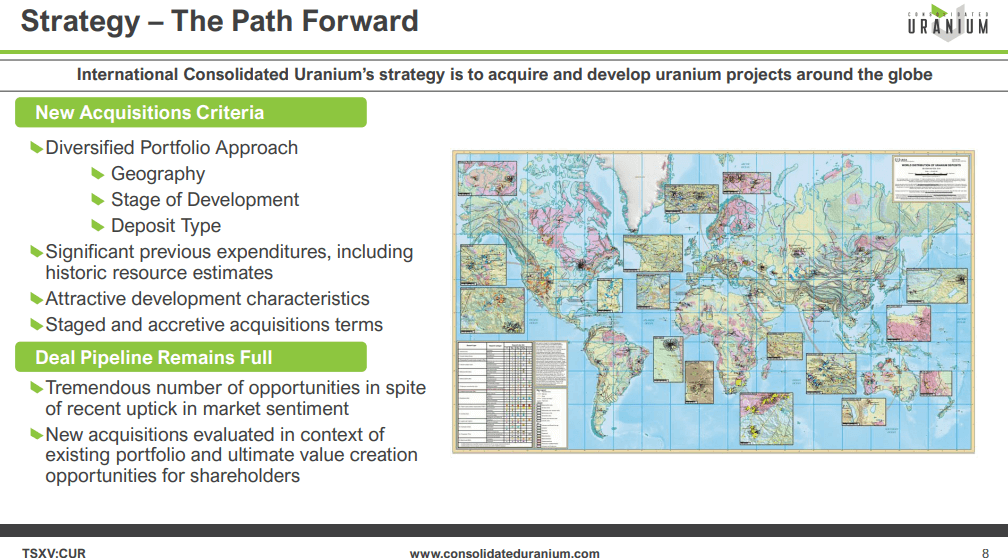

The company has acquired or has the right to acquire uranium projects in Australia, Canada, Argentina and the United States each with significant past expenditures and attractive characteristics for development.

Matthew Gordon spoke to Phil Williams, the CEO and President of Consolidated Uranium. The company has acquired 12-projects in 4 different jurisdictions around the world.

Company Overview

Consolidated Uranium has an experienced team and is focused on a diversified portfolio of jurisdictions and countries, to create diversification in the uranium sector. Their track record to date shows the company can make deals happen.

The Management Team

Philip Williams has been in the mining business since 1999. In 2006, he started as a research analyst covering the uranium space. For a few years, he was on the sell side writing reports on uranium companies around the world. Then he moved to a buy side investment fund, which was a junior natural resource fund, with about $1Bn under management, of which about 20% was in uranium.

Williams looked at uranium projects around the world and then went into investment banking where he spent 4.5-years as a managing director of an institutional investment dealer in Toronto, focused on all metals, but uranium was a big part of his portfolio. Over this period of time, the company raised about $1Bn foruUranium companies and he was an M&A advisor on about half the transactions that occurred in that space. In 2017, he left the street and started a private uranium royalty company. He spent 2-years there and put together a portfolio and now that company is a public Uranium Royalty Corp.

Last year, Williams realised there was an opportunity to go out and consolidate some of the forgotten about, orphaned projects that had significant past expenditures and resources in place. Consolidated Uranium was formed.

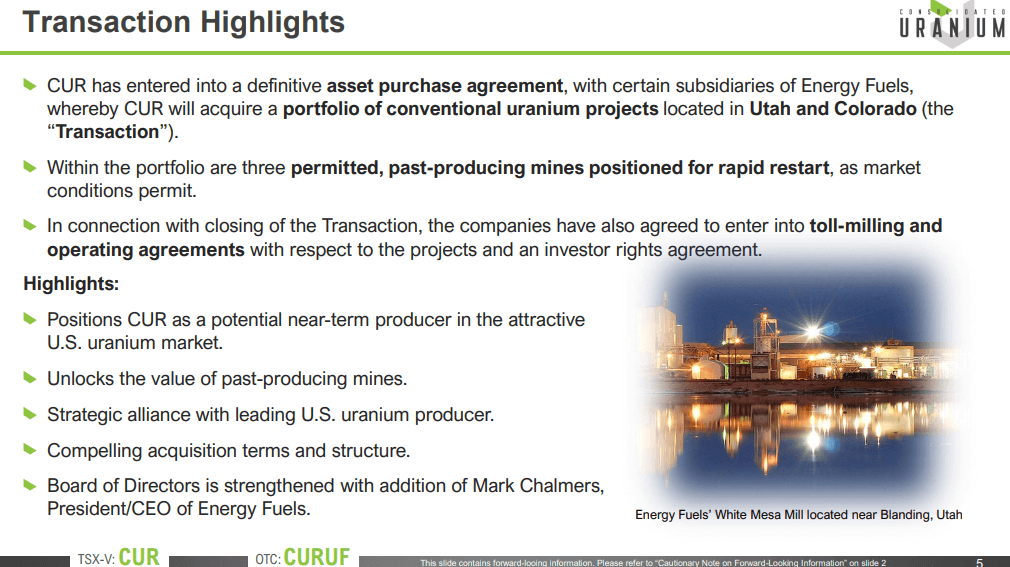

Peter Mullens joined early on as the VP of corporate development, based in Brisbane, Australia. Mullens is a geologist by training and has a lot of experience in the uranium space. Consolidated Uranium has also added Mark Chalmers of Energy Fuels as a member of the board and is now in partnership with Energy Fuels. On the advisory side, the company has Leigh Curyer, the CEO of NexGen. Curyer was one of the original founders of Consolidated Uranium and remains an advisor and strong supporter of the company.

Present Assets, Energy Conversion, & Business Plans

Consolidated Uranium is multi-jurisdictional, but has selected those jurisdictions very specifically. Canada, the US and Australia are good mining jurisdictions but also have uranium mines already in production. Argentina doesn't have a uranium mine but it is a nuclear country. They have reactors, so are interested in having domestic sources of supply.

Consolidated Uranium focuses on the jurisdiction, but also wants to diversify portfolio jurisdictions to spread the risk.

Nuclear power is being tied into the solution for climate change and there is likely to be a growing interest in uranium. The Queensland project has some interesting features that would make it a project because it's small and high-grade. The Labour government in Queensland needs to change from being anti-uranium to pro-uranium to support this project. This could be a possibility as in Queensland in particular, there are other mines in the state.

Consolidated Uranium has put the portfolio together with the strategy to buy projects without needing to spend money working on these projects and then hold on to them. Some of the portfolio is parked up but will have future value, and some projects will be producing assets when the price is right and could create value for the company.

Consolidated Uranium has taken a phased approach

- Phase 1: to build up some critical mass in the portfolio, get the company's capitalization right with their market cap, and access to cash.

- Phase 2: was to go after larger and more development ready projects.

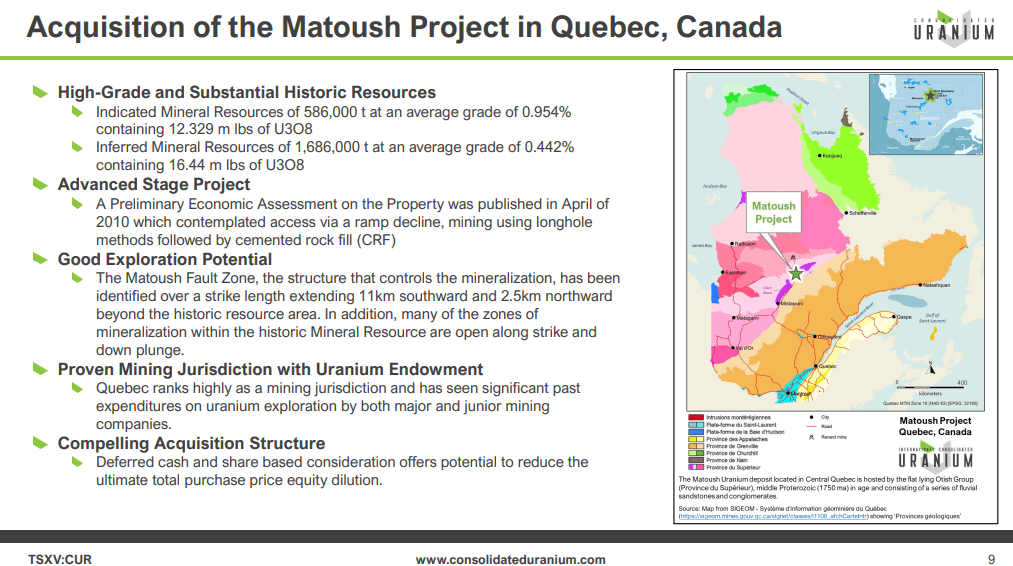

The last 2 acquisitions, Matoush in Quebec and the Energy Fuels portfolio are projects that can be developed and into production relatively quickly.

Finding Opportunities, Public Stories & Cash Position

On the M&A front, the company is looking at consolidation of complementary assets in some jurisdictions but they don’t plan to go into other jurisdictions at the moment. If something spectacular comes up which is available for attractive terms then the company might be interested. But otherwise, the plan is to look at projects that fit within what they already have.

The uranium market changes weekly at the moment with prices moving fast one way or the other, including the Consolidated Uranium share price. The company plans to get the Energy Fuels transaction closed, and then evaluate other opportunities in the space. The company is not planning to stretch themselves as it is comfortable with the current portfolio with a near term production asset in the US, a key development asset in Quebec and a portfolio of other projects.

The Energy Fuels deal is $2M up front, plus another $3M in 18 months time, and a further $3M after 36 months. Consolidated Uranium has over $20M in working capital so they are fully funded to complete the Energy Fuels transaction.

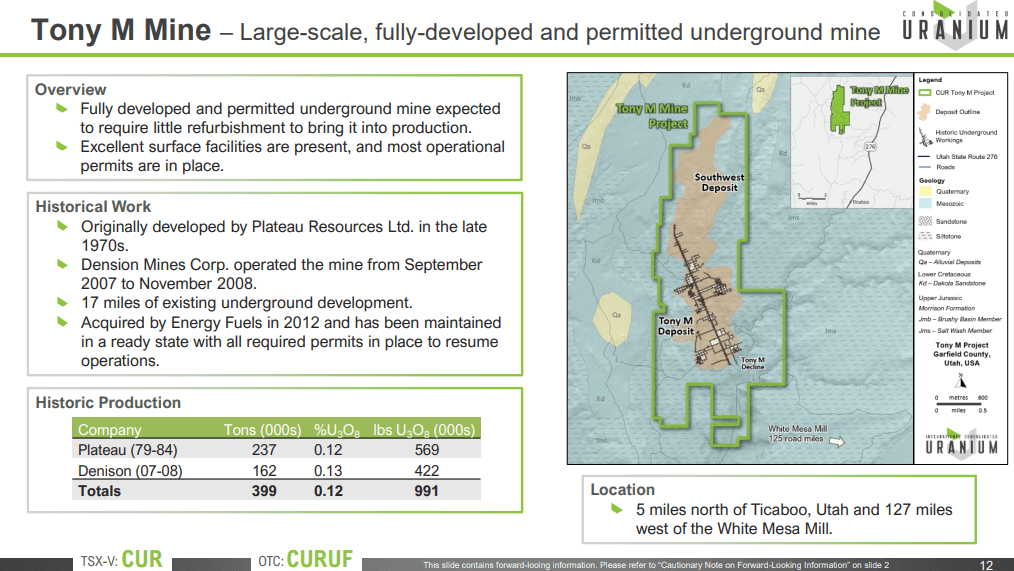

The company is planning a drill programme on the ‘Tony M’ Energy Fuels project to update the resource and put a PEA together on that project which will cost about US$1-$1.5M which the company is fully funded for.

Rethinking dialogues, near-term vitality, & well-organized finances

The uranium market currently has a lot of volatility, with the spot price moving very quickly. There is a lot of attention on the market and on the equity side companies need to fund their businesses and have plans to move forward to generate value. There are many new institutional investors coming into the market as new generalist funds interested to understand the market going forward.

Consolidated Uranium has been active for 18 months so it is not a brand new story, but is a new concept and a new group of people that investors should be looking at.

Consolidated Uranium has a good portfolio, with near-term production potential, advanced projects, and key projects around the world. The company is well funded with over $20M in the bank to execute on their strategy and has a team with deep knowledge of the space and exciting plans for the future.

To find out more, go to the Consolidated Uranium Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed