Copper's Price Ceiling Comes Into Focus as Speculative Capital May Unwind

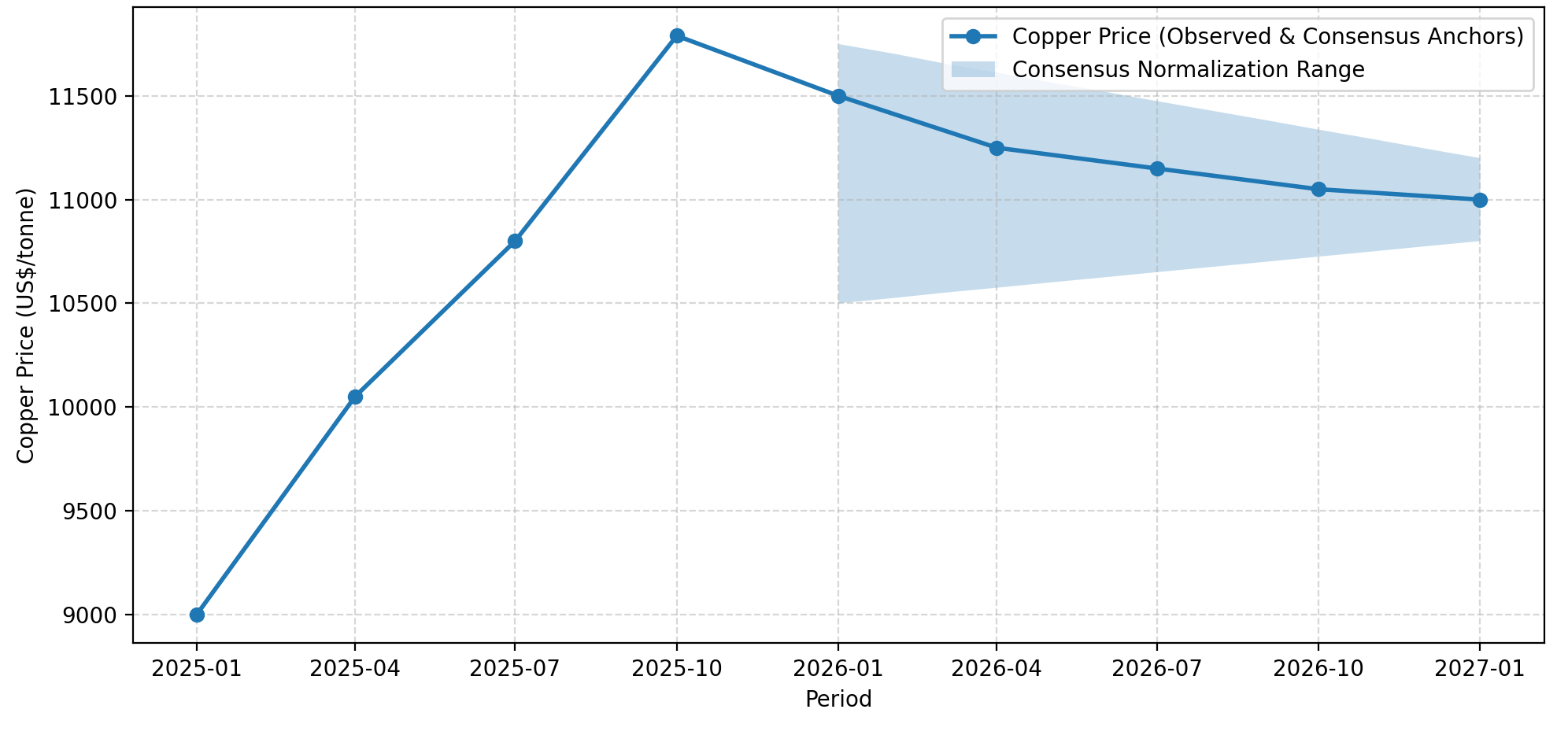

Goldman Sachs forecasts 18% copper price correction to $11,000/t by Dec 2026 as $30B in speculative flows unwind and surplus risks build. Low-cost producers positioned to outperform.

- Copper's rally above US$13,000 per tonne has been driven more by speculative positioning and policy fear than by end-use demand or structural deficits.

- Goldman Sachs forecasts an 18% correction to US$11,000 per tonne by December 2026 as surplus risks build and substitution accelerates.

- Scrap supply, inventory accumulation, and declining copper intensity in electric vehicles are reshaping medium-term demand assumptions.

- As prices normalize, investor focus is likely to shift from beta exposure to margin resilience, capital discipline, and execution visibility.

- Developers and explorers with low all-in sustaining cost profiles, oxide metallurgy, and clear permitting pathways may outperform in a re-priced copper environment.

From Momentum to Mean Reversion: Why Copper's Rally Is Being Re-Examined

Copper's price surge through 2025 and into early 2026 has been one of the defining trades in industrial metals. Prices punched through US$13,000 per tonne on the London Metal Exchange without a corresponding inflection in Chinese construction activity or grid infrastructure spending. The disconnect between price action and physical fundamentals has become a source of concern rather than conviction. This raises questions about the sustainability of current valuations and the durability of the investment thesis that supported the rally.

The rally unfolded as part of a broader risk-on trade across base metals, supported by macroeconomic narratives around electrification, deglobalization, and supply security. Yet the underlying demand picture has been more measured. Chinese refined copper consumption growth has remained subdued, and there has been limited evidence of sustained supply disruption capable of justifying a structural repricing. The absence of these fundamental catalysts suggests that price appreciation has been driven primarily by financial flows rather than industrial demand.

In January 2026, Goldman Sachs published a revised outlook suggesting that copper could retrace toward US$11,000 per tonne by December 2026, representing an 18% correction from recent highs. This is not framed as a bearish call on copper's long-term relevance, but rather as a normalization thesis following an extended period of sentiment-driven price appreciation. Margin sensitivity and balance-sheet strength are likely to reassert their importance as the macro tide recedes.

Speculative Inflows Drove the Upside: They May Also Drive the Downside

Goldman Sachs' base metals team, led by Eoin Dinsmore, reported that more than US$30 billion flowed into base metal markets in 2025, the largest annual speculative inflow on record. Copper absorbed more than half of this capital. The metal became a preferred vehicle for macro funds seeking exposure to multiple investment themes simultaneously: a China reopening proxy, a geopolitical hedge against supply chain disruption, and an inflation or currency debasement trade.

Flat demand growth out of China's refined copper sector and the absence of meaningful supply curtailments suggest that a significant portion of the price move has been attributable to financial flows rather than industrial consumption. The distinction matters because financial positioning can reverse quickly when narratives shift, whereas industrial demand tends to be more stable over medium-term horizons.

Positioning-led rallies tend to unwind faster than they build. Once the catalysts that attracted speculative capital begin to fade, the reversal can be swift and pronounced. For copper equities, this creates asymmetric volatility risk, particularly for companies operating at higher cost points or carrying elevated leverage on their balance sheets.

A Softer Fundamental Backdrop Is Emerging Beneath the Price

Beneath the elevated spot price, supply-side and demand-side adjustments are beginning to reshape medium-term market expectations. On the supply side, elevated prices have incentivized scrap recovery and secondary supply, while inventory builds across global exchanges have begun to accelerate. Goldman Sachs has increased its 2026 surplus projection from 160,000 tonnes to 300,000 tonnes, a notable shift from the deficit narratives that characterized earlier forecasts.

Goldman Sachs notes that high prices may encourage the use of aluminum in wiring rather than copper where technical specifications permit. More significantly, demand from electric vehicle manufacturers is decreasing as the copper intensity of newer models falls. Early electric vehicle designs used significantly more copper per unit than current platforms, and this optimization trend is expected to continue.

The implication is that cost curve positioning matters more than headline copper price forecasts. Companies with all-in sustaining costs in the lower quartiles of the industry will retain margin protection even if prices revert toward the US$10,000 per tonne range that UK brokerage Peel Hunt views as a long-run equilibrium.

Policy Premiums Fade as Stockpiling & Tariff Fears Ease

Throughout 2025, tariff concerns led to defensive stockpiling by United States buyers, creating a premium on COMEX-deliverable copper relative to LME pricing. This geographic arbitrage reflected expectations that tariffs would become the primary tool for addressing supply security concerns. Buyers accelerated purchases and built inventory positions as a hedge against potential disruption, contributing to price strength that exceeded underlying demand growth.

However, Goldman Sachs notes that policy developments suggest a shift away from tariff-based approaches, reducing the urgency for defensive inventory accumulation. As these policy premiums unwind, pricing dislocations across exchanges are expected to normalize. For higher-cost producers who benefited from elevated regional premiums, this represents margin compression risk.

What This Macro Reset Means for Copper Equities

Copper equities are entering a selectivity phase rather than facing a blanket sell-off. The differentiation that emerges from this period will likely be defined by fundamental characteristics rather than beta exposure to the underlying commodity. Investor screening criteria are expected to emphasize all-in sustaining costs relative to long-run price assumptions of US$4.00 to US$4.50 per pound, capital intensity per tonne of copper produced, and permitting visibility with realistic execution timelines.

Companies that can demonstrate margin resilience under stress-tested price assumptions will attract capital that might otherwise remain on the sidelines during periods of elevated volatility. Balance sheet strength, cost discipline, and execution capability become the differentiating factors rather than simply exposure to copper price upside.

Late-Stage Developers With Margin Resilience

The current environment creates conditions where late-stage development projects with favorable cost structures and clear permitting pathways may offer defensive characteristics that production-stage assets at higher cost points cannot match. Marimaca Copper provides an illustrative example of how project-level economics can position a developer to navigate potential price corrections.

The company's oxide heap-leach flowsheet represents a lower-risk metallurgical approach compared to sulphide processing, with life-of-mine all-in sustaining costs of US$2.29 per pound according to its August 2025 definitive feasibility study. This cost positioning provides substantial margin cushion if copper prices revert toward consensus forecasts. At a base case copper price of US$4.30 per pound, the DFS demonstrates a post-tax net present value of US$709 million and an internal rate of return of 31%, with initial capital expenditure of US$587 million.

Marimaca Copper received its environmental approval, the Resolución de Calificación Ambiental, in November 2025. The company is now advancing sectorial permits, detailed engineering, and project financing workstreams. Remaining milestones include securing auxiliary permits for construction and operation, finalizing project financing, and procuring long-lead items.

Hayden Locke, the company's President and Chief Executive Officer, emphasizes the capital efficiency that underpins Marimaca Copper's development strategy:

"Industry-leading capital costs, very competitive operating cost, industry-leading return on invested capital metrics… The pre-production capital cost is just sub-$600 million US and I see opportunities where we can reduce that. "

The company's objective is to be ready to commence construction during 2026, subject to completion of financing and final permits.

Optionality & Capital Efficiency in the Exploration Segment

Exploration-stage companies face distinct challenges in a softer price environment, but those with capital-efficient business models and strategic partnerships can preserve optionality without balance-sheet stress. Fitzroy Minerals represents an approach to exploration that emphasizes joint venture-led development pathways and near-term cash flow potential.

The company's Caballos project in Chile hosts geological characteristics analogous to established deposits in the region, including similarities to Lundin Mining's Candelaria, Capstone Copper's Mantoverde, and the La Farola deposit. This geological context provides exploration upside that is asymmetric to the capital deployed, provided burn rates and funding risk remain controlled. Fitzroy holds C$11 million in cash, providing approximately twelve months of runway for its exploration budget and corporate costs.

The company has signed legally binding key terms with Pucobre S.A. for a heap leach joint venture at Buen Retiro, with a preliminary economic assessment now underway. This partnership structure creates potential for near-term non-operated cash flow.

Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, describes the positioning that differentiates the company from exploration peers:

"We are working on terms with Pucobre to do a heap leach joint venture. That operation gives us the potential for near-term non-operated cash flow which we think will distinguish us from many other explorers in the market."

The Investment Thesis for Copper

Despite near-term price correction risk, copper's long-term demand fundamentals remain supported by electrification trends and infrastructure investment cycles. Several factors distinguish companies positioned to outperform in a re-priced copper market:

- Copper prices may correct toward US$10,000 to US$11,000 per tonne, but long-term electrification demand remains intact, creating volatility rather than obsolescence for well-positioned equities.

- Companies with all-in sustaining costs in the lower quartiles of the industry cost curve retain margin protection under stress-tested price scenarios.

- Oxide projects with heap-leach flowsheets offer lower capital intensity, faster payback periods, and reduced technical risk compared to complex sulphide processing alternatives.

- Permitting certainty and existing infrastructure access reduce financing risk during macro drawdowns when capital availability becomes more selective.

- Exploration companies with joint venture-led development models can preserve upside exposure without balance-sheet stress or dilutive financing requirements.

- Jurisdictional stability and transparent regulatory frameworks provide risk-adjusted advantages during periods of heightened geopolitical uncertainty.

Goldman Sachs' revised outlook reflects a cooling of excess optimism rather than a collapse in copper's strategic relevance. The correction thesis is grounded in observable fundamentals: surplus projections, demand substitution trends, and the unwinding of speculative positioning that drove prices beyond levels justified by physical market conditions.

Macro-driven corrections historically reset valuation frameworks and improve long-term entry points for investors with the discipline to differentiate between price momentum and economic resilience. The selectivity phase ahead will reward companies that can demonstrate margin protection, execution capability, and capital discipline under a range of price scenarios.

The emphasis shifts from commodity exposure to company-specific fundamentals. Those who distinguish between speculative froth and structural value creation are likely to outperform as copper markets recalibrate toward a more sustainable equilibrium.

TL;DR

Copper's rally above $13,000/tonne has been driven primarily by speculative positioning rather than physical demand fundamentals. Goldman Sachs projects an 18% correction to $11,000/tonne by December 2026 as surplus risks increase to 300,000 tonnes and demand substitution accelerates. Key factors include reduced copper intensity in electric vehicles, increased scrap supply, and fading tariff-related policy premiums. The investment focus is shifting from broad commodity exposure to company-specific fundamentals—particularly all-in sustaining costs, balance sheet strength, and permitting visibility. Late-stage developers with oxide heap-leach projects and exploration companies with joint venture models may offer defensive positioning as prices normalize.

FAQs (AI-Generated)

Goldman Sachs attributes the rally to over $30 billion in speculative inflows rather than industrial demand growth. With flat Chinese consumption and no major supply disruptions, prices exceeded fundamental support levels and are vulnerable to positioning reversals.

Goldman Sachs projects copper will retrace to approximately $11,000 per tonne by December 2026, representing an 18% correction from recent highs above $13,000/tonne.

Copper intensity per EV is declining as manufacturers optimize designs. Newer platforms use significantly less copper than earlier models, reducing previously bullish demand projections from the EV transition.

Companies with lower-quartile all-in sustaining costs, strong balance sheets, clear permitting pathways, and capital discipline will outperform. Oxide heap-leach projects offer lower technical risk and faster payback periods.

Goldman Sachs has increased its 2026 surplus projection from 160,000 tonnes to 300,000 tonnes, a notable shift from the deficit narratives that characterized earlier market forecasts.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed