Geopolitical Risk & Monetary Expectations Drive Gold's Longest Rally Since 1973

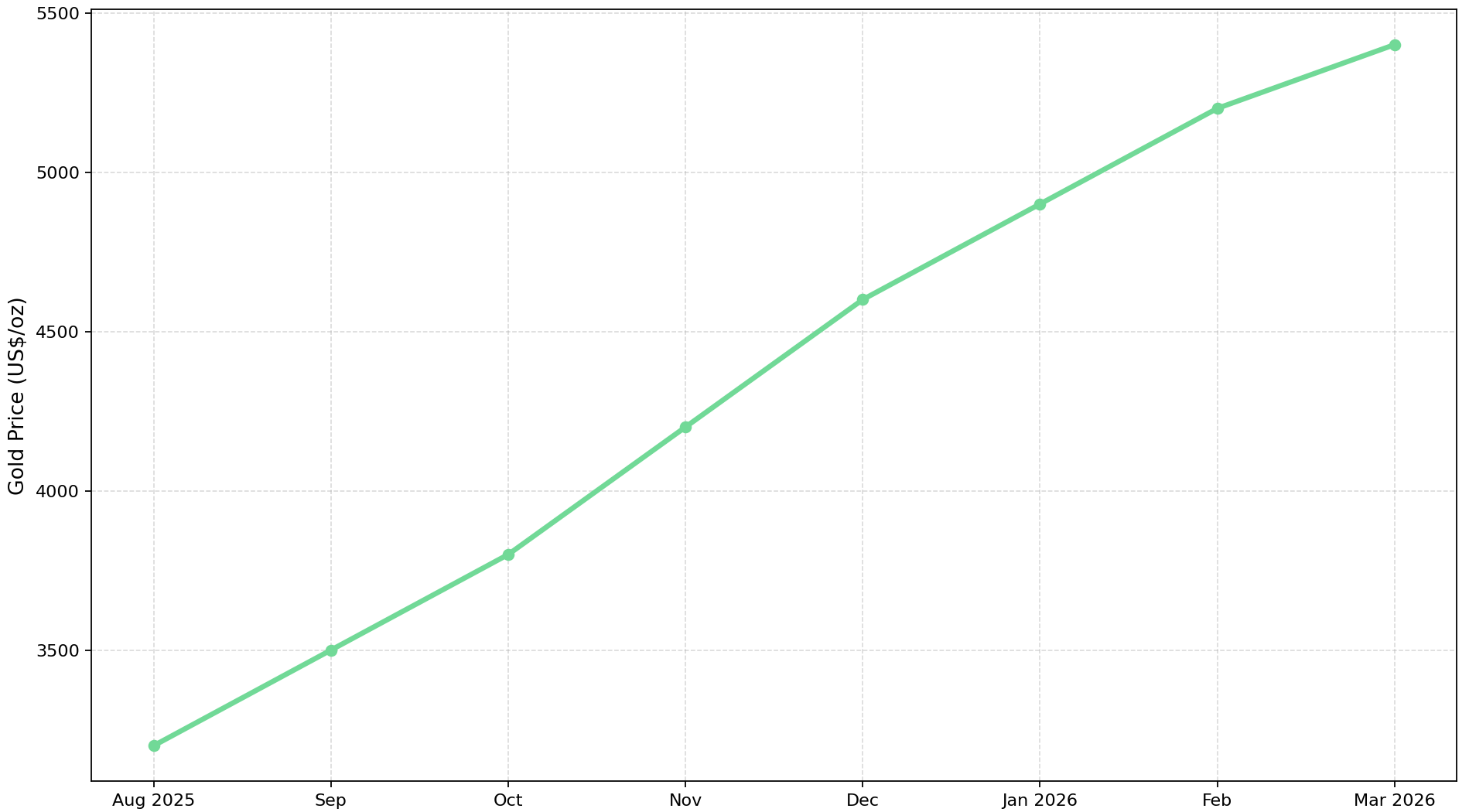

Gold's seven-month rally to $5,400/oz is driven by geopolitical risk, central bank diversification, and energy-inflation, equities offering leveraged upside.

- Gold has recorded seven consecutive monthly gains, its longest streak since 1973, due to continuous geopolitical tension, central bank reserve diversification, and shifting monetary policy expectations in the United States.

- Safe-haven capital flows have accelerated following disruptions to tanker traffic in the Strait of Hormuz, through which approximately 20% of global oil supply transits, raising global inflation expectations and broadening gold's demand base.

- Central bank accumulation remains structurally supportive, with new sovereign buyers including Malaysia and South Korea entering the market alongside established accumulators, indicating a broadening of reserve diversification beyond traditional buyers.

- Gold equities with AISC generating free cash flow at spot prices, IRRs expanding above base-case models, and near-term production timelines are attracting capital that lower price environments did not justify.

- The rally carries meaningful downside risk, and gold's momentum could reverse if geopolitical tensions ease, U.S. real interest rates rise materially, or energy markets stabilize in ways that reduce the war premium currently embedded in spot prices.

Why Gold's Seven-Month Rally Reflects a Shift in Global Capital Allocation

The rally began in 2025 as US monetary policy expectations shifted toward easing. When real interest rates - nominal yields minus inflation expectations - decline, the cost of holding a non-yielding asset falls, and institutional and sovereign capital allocates accordingly. What extended the rally into 2026 was US-Iran tension, including disruptions to oil tanker traffic through the Strait of Hormuz, which introduced energy supply uncertainty on top of existing monetary conditions.

20% of global oil supply transits that corridor, meaning any sustained interference carries immediate implications for energy prices, inflation expectations, and central bank policy frameworks. Gold began absorbing two reinforcing demand narratives simultaneously: its traditional safe-haven role during geopolitical crises, and its function as a hedge against energy-driven inflation. Spot gold reached approximately $5,400 per ounce as of March 2026 as both narratives took hold.

Central Bank Reserve Composition & the Demand Base for Gold

Monthly purchase volumes slowed in January 2026 relative to record levels in 2025, but the buyer base is expanding. China recorded its 15th consecutive month of gold purchases as of January 2026, bringing the metal to approximately 10% of total foreign reserves. Uzbekistan added nine tonnes in January. Malaysia increased reserves for the first time since 2018, while South Korea announced plans to resume gold investment after more than a decade, with a stated preference for executing purchases through overseas-listed physical gold exchange-traded funds. Unlike speculative or retail flows, central bank purchases tend to be strategic and long-duration, meaning gold benefits from a persistent demand base even during cyclical price corrections. Increasing geopolitical fragmentation and currency volatility are driving sovereign entities toward assets with no counterparty risk, a shift with structural implications for gold's price floor.

Energy Market Disruptions & Gold's Role as an Inflation Hedge

Disruptions in the Strait of Hormuz affect oil markets with immediacy. Even temporary supply interruptions drive sharp price volatility, feeding into inflation expectations across importing economies. Higher energy costs raise transportation, manufacturing inputs, and household expenses, creating pressure on central banks to choose between tightening to contain inflation or easing to support growth. Either path can be supportive for gold. Tighter policy maintains elevated inflation expectations; looser policy risks weakening fiat currency relative to hard assets.

The 1970s commodity inflation cycle is the relevant historical reference: oil supply shocks forced central banks into a policy bind between controlling inflation and supporting growth, and gold rose because neither path was clearly credible. The current setup shares that structure, when energy supply is uncertain, inflation expectations are harder to anchor, and gold benefits because it hedges against both tightening that fails and easing that overshoots.

Project Economics & Operational Leverage in a Rising Price Environment

Gold equities can offer significant leverage to bullion prices through the operational mechanics of mining economics. As spot gold rises above feasibility study assumptions, net present value increases and internal rates of return improve, often disproportionately relative to the percentage move in the underlying metal.

Integra Resources operates the Florida Canyon mine in Nevada and is advancing the DeLamar project in Idaho, where the feasibility study outlines an NPV of approximately $1.9 billion and an IRR of 97%. Florida Canyon is targeting 80,000 to 90,000 ounces per year in both 2027 and 2028 as capacity expansion progresses, providing near-term cash flow visibility while DeLamar advances through its development timeline. George Salamis, President and Chief Executive Officer, frames Integra Resources’ production strategy:

"2026 is about building capacity today at Florida Canyon to deliver more ounces, stronger cash flow, lower costs tomorrow."

Perseus Mining holds US$755 million in net cash alongside an undrawn US$400 million debt facility, providing US$1.2 billion in total liquidity for growth and acquisitions, operating three producing mines across West Africa. The company reaffirmed FY2026 production guidance of 400,000 to 440,000 ounces at AISC of US$1,600 to US$1,760 per ounce, with the Nyanzaga project in Tanzania targeting first gold pour in Q1 2027.

Serabi Gold operates the Palito Complex and Coringa mine in Brazil's Tapajos Province, processing Coringa ore through existing Palito infrastructure — a configuration that eliminates the capital requirement for a standalone plant and tailings dam at Coringa. A 2024 Prefeasibility Study outlines a 48% IRR at US$2,100 per ounce gold. The company holds US$54.3 million in cash, funds growth organically, and is targeting consolidated production of approximately 60,000 ounces by 2026.

Near-Term Cash Flow Visibility & Infrastructure-Led Cost Reduction

New Found Gold is advancing two assets in Newfoundland simultaneously: the Hammerdown mine, currently in production and ramping output, and the Queensway project, which hosts an initial indicated resource of 1.39 million ounces at 2.40 grams per tonne gold. The development strategy centers on routing Queensway material through the existing, permitted Pine Cove mill toward the end of 2027, removing significant early-stage capital expenditure from the schedule. Keith Boyle, Chief Executive Officer of New Found Gold, outlines the economics at prevailing gold prices:

"We're trucking 9 to 10 grams, all-in sustaining $1,300… Today's price, you're looking at over $250 million of free cash flow over that first four years while we build the mill on site."

Resource Scale & Long-Term Development Potential

Extended bull markets tend to redirect institutional capital toward large-scale development assets capable of delivering significant production over multi-decade mine lives. Hycroft Mining is advancing a large-scale gold and silver deposit in Nevada, where a recent resource update increased gold resources to over 16 million ounces and silver to just under 600 million ounces, representing approximately a 50% average increase from prior estimates. The company holds approximately $200 million in treasury, supported by institutional investors including Eric Sprott, who holds approximately 43% of the company, alongside Tribeca, BlackRock, Schroders, Franklin, and Pala. A preliminary economic assessment remains ongoing. Diane Garrett, President and Chief Executive Officer of Hycroft Mining, explains the development optionality:

"This gives us an option to start mining on the high-grade. We could go underground first, and by doing that you're getting better cash flows up front and then you can build in the scalability to mine the rest of the ore body."

Large-Scale Resource Bases & Multi-Decade Production Potential

Tudor Gold controls one of the largest undeveloped gold-copper systems in North America at its Treaty Creek project in British Columbia's Golden Triangle, with a 2026 mineral resource estimate of 24.9 million indicated ounces and 4.0 million inferred ounces. The company is targeting higher-grade underground zones above 3 grams per tonne gold, with road access within approximately 40 kilometers of power and infrastructure. Joseph Ovsenek, President and Chief Executive Officer of Tudor Gold, outlines the development approach:

"We're focused on this higher-grade underground line, targeting that 3 gram or better material to start with, and coming up with an 8,000 to 10,000 tonne per day underground mine. Capex a billion and a half, that's something we can handle."

Cabral Gold is advancing a Stage 1 heap leach operation at the Cuiú Cuiú project in Brazil's Tapajos Gold Province, where a July 2025 Prefeasibility Study outlines initial capex of US$37.7 million, an after-tax IRR of 78% at US$2,500 per ounce gold, and AISC of US$1,210 per ounce. At current spot prices near US$3,340 per ounce, the IRR rises to 139%. Construction is fully funded through a US$45 million gold loan closed November 2025, with first gold pour targeted for Q4 2026.

Jurisdictional Profile & Permitting as Determinants of Capital Access

Jurisdiction, permitting status, and regulatory predictability are significant determinants of financing access, particularly for companies seeking construction-stage capital in an environment where lender due diligence has become more rigorous. U.S. Gold Corp is advancing the CK Gold project in Wyoming, where a Mine Operating Permit was approved in April 2024. The company is finalizing a feasibility study expected to outline annual production of approximately 110,000 gold-equivalent ounces over a mine life of 10 to 11 years.

P2 Gold is advancing the Gabbs gold-copper project in Nevada, where a 2025 Preliminary Economic Assessment outlines a combined Indicated and Inferred resource of 3.45 million gold-equivalent ounces against a market capitalization of approximately US$110 million. The company is targeting a total resource exceeding 5 million gold-equivalent ounces and is awaiting a water permit expected in Q1 2026, the primary regulatory milestone before a formal production decision can be pursued.

i-80 Gold is pursuing an integrated hub-and-spoke development strategy in Nevada centered on refurbishing the Lone Tree autoclave facility, a former Newmont operation designed to process refractory gold ore in which gold is occluded within arsenopyrite and requires pressure oxidation to liberate. i-80 controls approximately 6.5 million ounces of measured and indicated resources across multiple Nevada deposits and is targeting Lone Tree production of 150,000 to 160,000 ounces per year at steady state, with a preliminary estimate of $150 million to $200 million in annual net cash flow.

The Investment Thesis for Gold

- US and Israeli military strikes on Iran beginning February 28, 2026, triggered Strait of Hormuz disruptions affecting approximately 20% of global oil supply, pushing gold to $5,423 per ounce before a subsequent sell-off to $5,085, a sequence that illustrates gold's sensitivity to energy supply shocks while also demonstrating that the safe-haven bid does not hold uniformly as conflict conditions evolve.

- Central banks outside traditional sovereign buyers are adding gold to reserves, creating demand that does not exit on short-term price corrections the way retail or leveraged flows do, which reduces the probability of sharp demand-driven reversals.

- Energy-driven inflation puts central banks in a position where both tightening and easing carry credibility risk, tightening into a supply shock risks recession, easing risks entrenching inflation, and gold functions as a hedge against policy error in either direction.

- Gold equities offer operational leverage to rising spot prices through expanding project margins and internal rates of return that rise disproportionately relative to the metal itself, particularly for companies with low all-in sustaining cost profiles.

- Projects in stable mining jurisdictions with advanced permitting and well-capitalized balance sheets are positioned to attract institutional financing where development risk and regulatory transparency remain primary screening criteria.

- Large-scale, long-duration resource assets provide disproportionate upside exposure when gold prices remain structurally elevated above original feasibility assumptions.

Gold's seven-month rally reflects a structural realignment of global capital driven by geopolitical fragmentation, energy market vulnerability, and sovereign reserve diversification. For investors evaluating sector exposure, the macro backdrop supports a focused analysis of project economics, jurisdictional stability, and development credibility. Companies that combine high-quality resource bases with disciplined capital allocation and clear production pathways are best positioned to capture durable value from an environment in which the fundamental conditions supporting gold demand remain firmly intact.

TL;DR

Gold's longest winning streak since 1973 reflects a convergence of structural forces rather than a single catalyst. Declining U.S. real interest rates reduced the opportunity cost of holding gold, while U.S.-Iran tensions and Strait of Hormuz disruptions, affecting roughly 20% of global oil supply, introduced an energy-driven inflation premium on top of existing monetary conditions. Central banks from China to South Korea are broadening reserve diversification into gold, creating durable, long-duration demand that does not exit on short-term corrections. Gold equities are capturing disproportionate upside as rising spot prices push project IRRs and NPVs well above original feasibility assumptions, with jurisdictional stability and permitting progress emerging as key determinants of institutional financing access.

FAQs (AI-Generated)

Gold's sustained rally reflects three reinforcing drivers: shifting U.S. monetary policy expectations toward easing (which lowers the cost of holding a non-yielding asset), escalating geopolitical tensions including U.S.-Iran conflict disrupting oil supply through the Strait of Hormuz, and accelerating central bank reserve diversification away from fiat currencies. These forces have operated simultaneously, sustaining demand across both safe-haven and inflation-hedge functions.

Central bank purchases are strategic and long-duration, meaning they do not exit positions during short-term price corrections the way retail or leveraged flows do. With new sovereign buyers — including Malaysia, South Korea, and Uzbekistan — entering the market alongside established accumulators like China, the demand base has broadened, reducing the probability of sharp demand-driven reversals and providing structural support for gold's price floor.

Disruptions to oil supply through key transit corridors like the Strait of Hormuz raise energy prices, which feed directly into inflation expectations across importing economies. This places central banks in a policy bind — tightening risks recession while easing risks entrenching inflation — and gold benefits from credibility risk in either direction. The parallel to 1970s commodity inflation cycles is instructive: when policy paths are uncertain, hard assets with no counterparty risk attract capital.

Gold mining companies benefit from operational leverage: as spot prices rise above the assumptions built into feasibility studies, profit margins expand disproportionately. A mine with fixed operating costs and rising revenue per ounce sees its NPV and IRR improve at a faster rate than the underlying metal price itself. Companies with low all-in sustaining cost profiles and near-term production timelines are particularly well-positioned to translate bullion price gains into free cash flow growth.

Gold's momentum carries meaningful downside exposure. A de-escalation of U.S.-Iran tensions or broader geopolitical stabilisation would reduce the war premium embedded in spot prices. A material rise in U.S. real interest rates — driven by stronger-than-expected economic data or hawkish Fed policy — would increase the opportunity cost of holding gold and trigger institutional reallocation. Stabilisation in energy markets that reduces inflation expectations could similarly erode two of the three primary demand narratives currently supporting the rally.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

Stay Informed