Denison Mines (DML) - Uranium: It's All in the Planning

Interview with David Cates, President and CEO of Denison Mines (TSX: DML, NYSE: DNN)

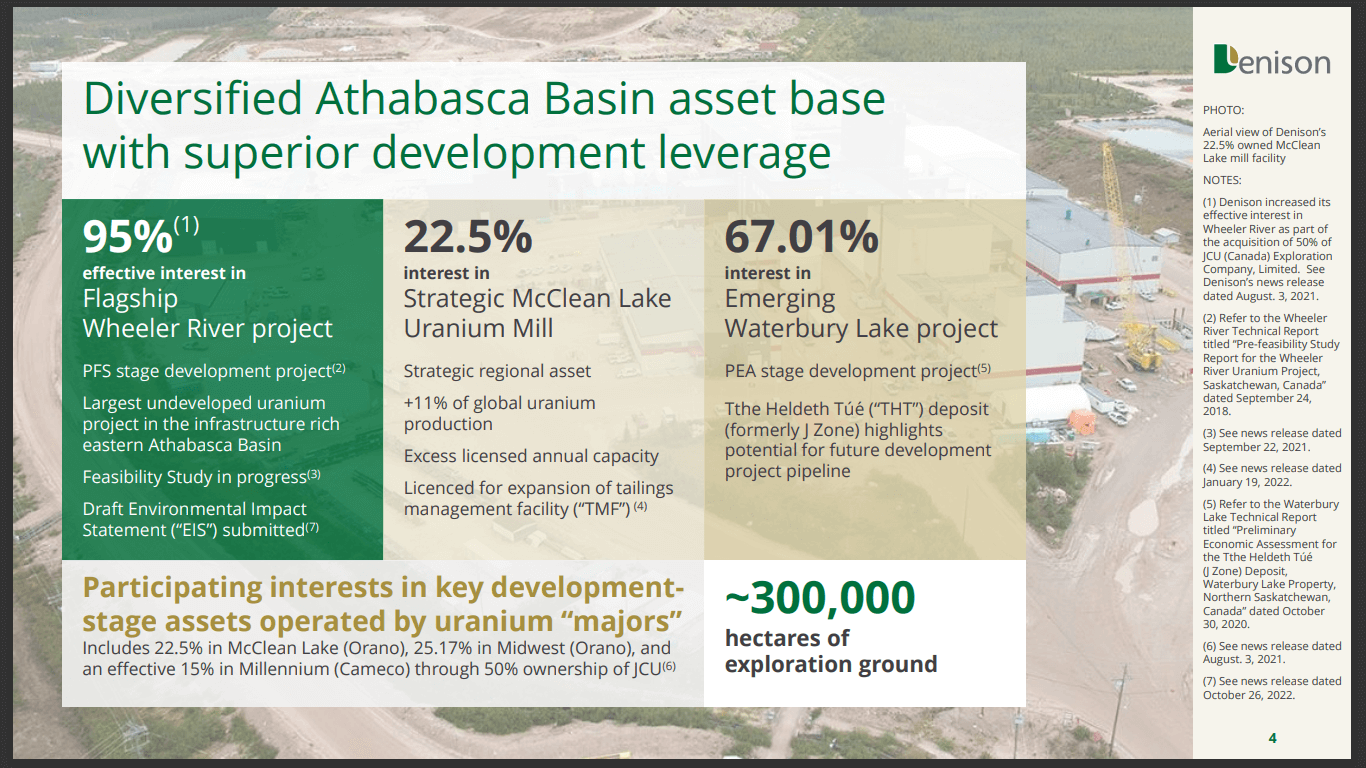

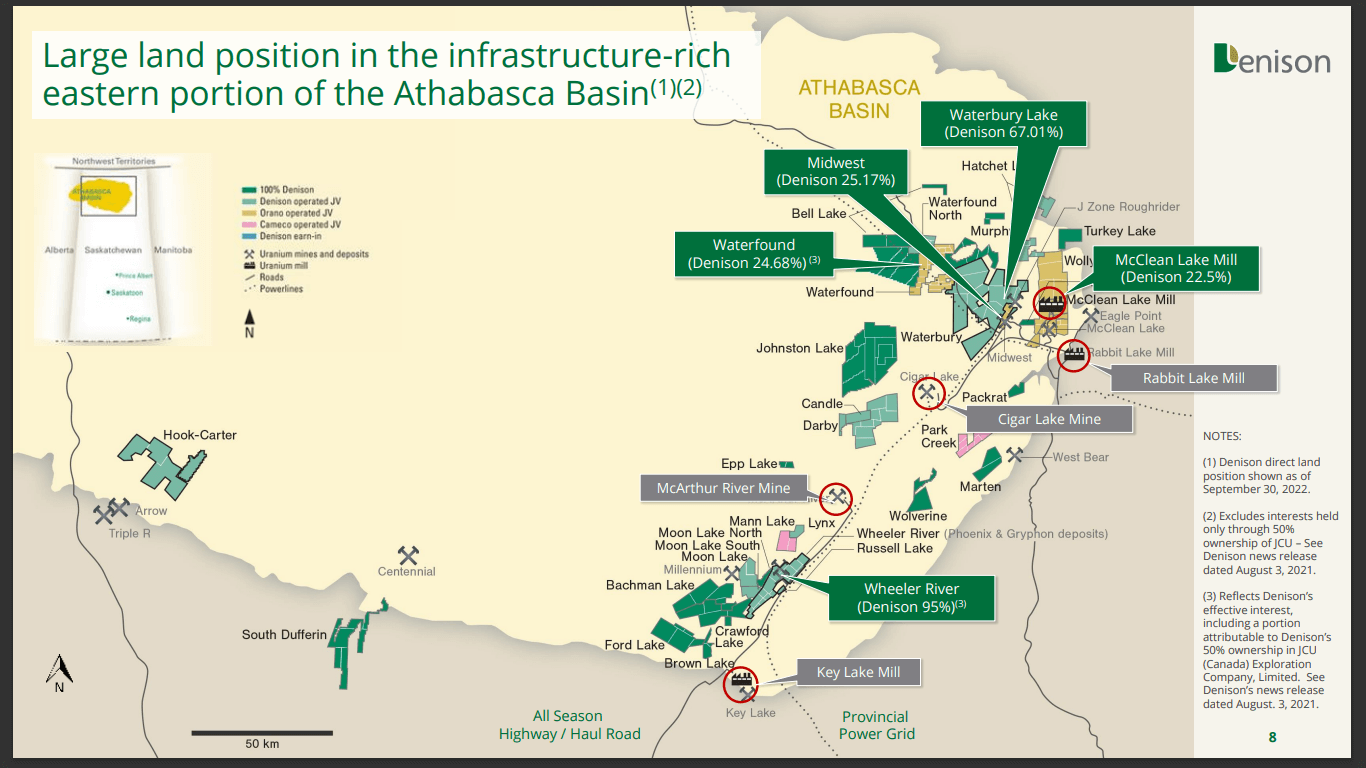

Denison Mines Corp. is a TSX and NYSE- listed uranium exploration and development company focused on the advancement of its projects located in the Athabasca Basin region of Northern Saskatchewan, Canada. The company’s flagship project is the Wheeler River project. The company holds a 95% effective interest in the project and it is the largest undeveloped uranium project in the Eastern part of the Athabasca Basin. The company also has a 22.5% interest in the McClean Lake joint venture with Orano Canada, which comprises several uranium deposits and the McClean Lake uranium mill. The McClean Lake uranium mill is an operating and licensed processing facility which has been contracted to process the ore from the Cigar Lake mine, majority-owned by Cameco Corporation, under a toll milling agreement.

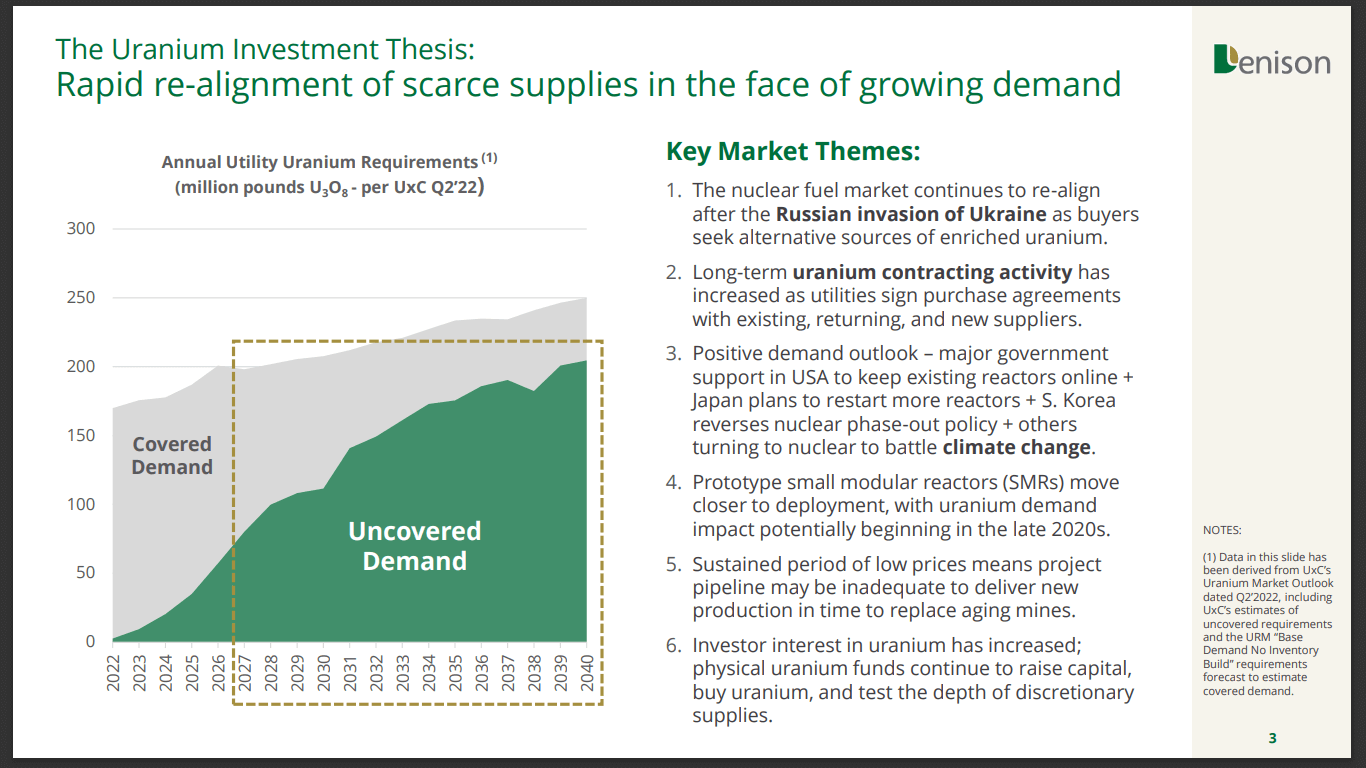

The company has been very aware of the changing uranium space, with Cates explaining that the reduced production from Kazakhstan, amongst others, has led to the rise in the uranium spot price and influenced the company’s strategy. The company believes that as the drive for a greener form of energy generation becomes more prominent, the resistance in the spot price will also be broken to above USD$ 50.

Denison Mines Corp. has been designed to play a strategic part in the uranium supply chain with the company planning as such. The signing of off-take agreements by larger uranium suppliers will lead to their supply capacity being met. The moment when this point is reached Denison Mines Corp. will be perfectly positioned to not only supply at a competitive price but also for longer periods due to the size and lifetime of its projects.

Denison Mines Corp. will continue to advance its projects as per the company strategy. The company holds approximately CAD$ 55 million in working capital and a cash and cash equivalent position of approximately CAD$ 225 million, placing it in a position to advance its projects.

Market cap and projects

Denison Mines Corp. holds a market cap between CAD$ 1.2 billion and CAD$ 1.5 billion, with the company’s share price trading on the TSX between CAD$ 1.75 and CAD$ 1.60, for November 2022. Dave Cates, the CEO of Denison Mines Corp. explains that the market cap of the company may not have been justifiable two years ago, but due to the company’s high-quality assets as well as the de-risking activities it has completed to date, the market cap is supported.

“Our market cap is in the range of CAD$ 1.2 billion to CAD$ 1.5 billion. We’re really getting quite close to a development decision, so if you were asking that question 2 to 3-years ago, it might have been a bit of a different answer. But today, we’ve really come much closer to making a development decision on Wheeler and Phoenix. And ultimately, what we’re doing is de-risking our company’s net asset value.”

Cates explains that the market cap of the company has been supported by various market analysts, with the majority further believing that Denison Mines Corp. is trading at a discounted price.

“We have many analysts covering us from a number of reputable investment banks in Canada and the United States, so we’re not really the ones saying that we’ve got a market cap or value in that range. But what I can say is that the consensus of that group says we’re trading at a significant discount to that NAV, and our job is really to keep on de-risking the project and getting closer to actually being in production, and we’ve been doing that over the last several years and we’ve had great success, to the point where we’re now within a year of completing a Feasibility Study for our Phoenix ISR project, which is part of Wheeler River.”

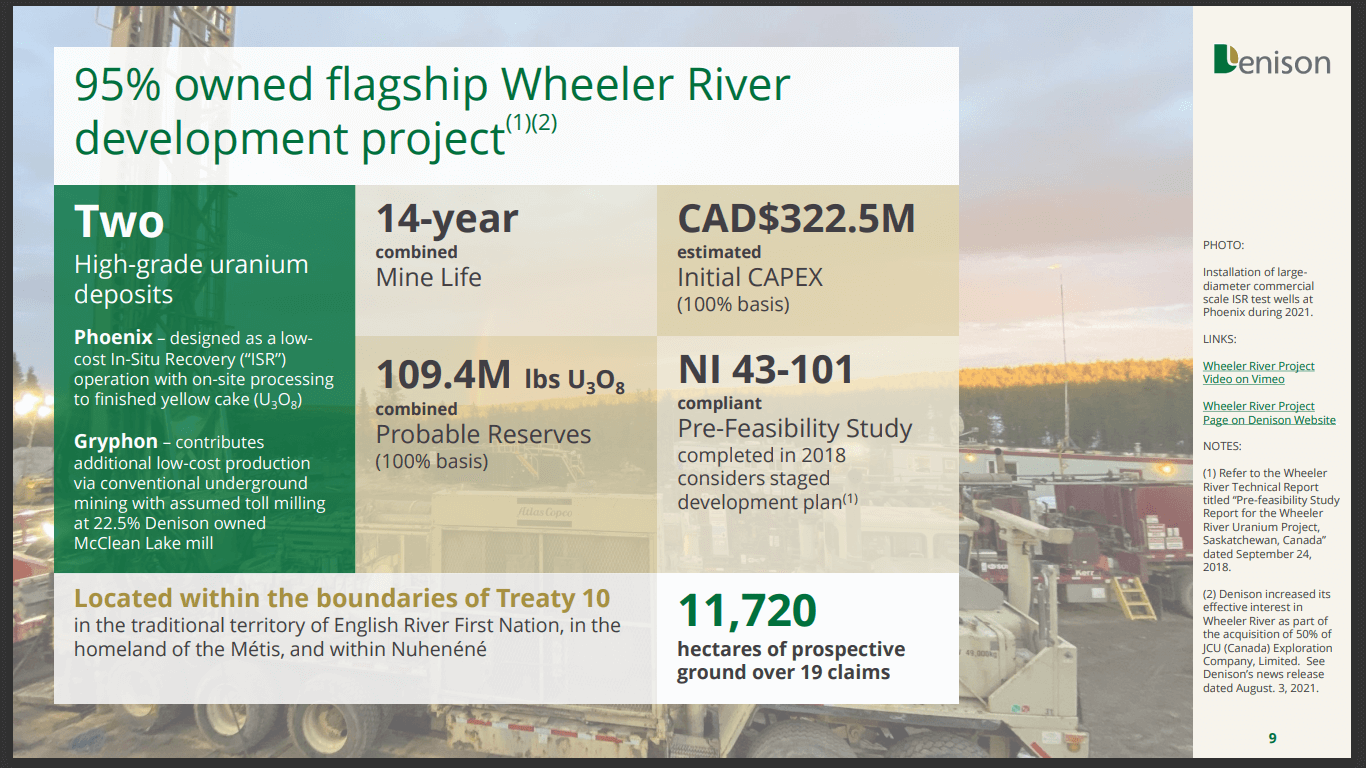

Cates believes one of the largest factors that support the company’s valuation, is the Wheeler River project, which is the largest undeveloped uranium project in the eastern Athabasca basin.

“If I look at their details and I look at our own internal models of this, it’s for sure that the biggest driver is the Wheeler River project. This is our flagship; it is the largest undeveloped uranium project in the eastern portion of the Athabasca Basin.”

The advanced stage of the Wheeler River project including the 2018 pre-feasibility study conducted on the Wheeler River project, the mineral resource estimate, and various field tests including in-situ test work on the Phoenix deposit of the project, all contribute to the potential and promise of Denison Mines Corp. The studies fit into the company’s larger plan to position itself as a future producer in the uranium space.

“We have a 2018 Pre-Feasibility Study that sets out our basis for declaring reserves. So, this project has reserves that have been declared on it, and NPVs associated with the return on that. Now, we’ve been de-risking that over the last 3-years to add even further confidence to those estimates, reserves and economics through a bunch of field tests that we’ve run primarily focused on the use of in situ recovery as a mining method at Phoenix, but also just on refining and updating our cost estimate so that we can produce a new Feasibility Study in the first half of next year, which will really refresh all of those numbers that go into those NAVs and allow for the analysts to price the company.”

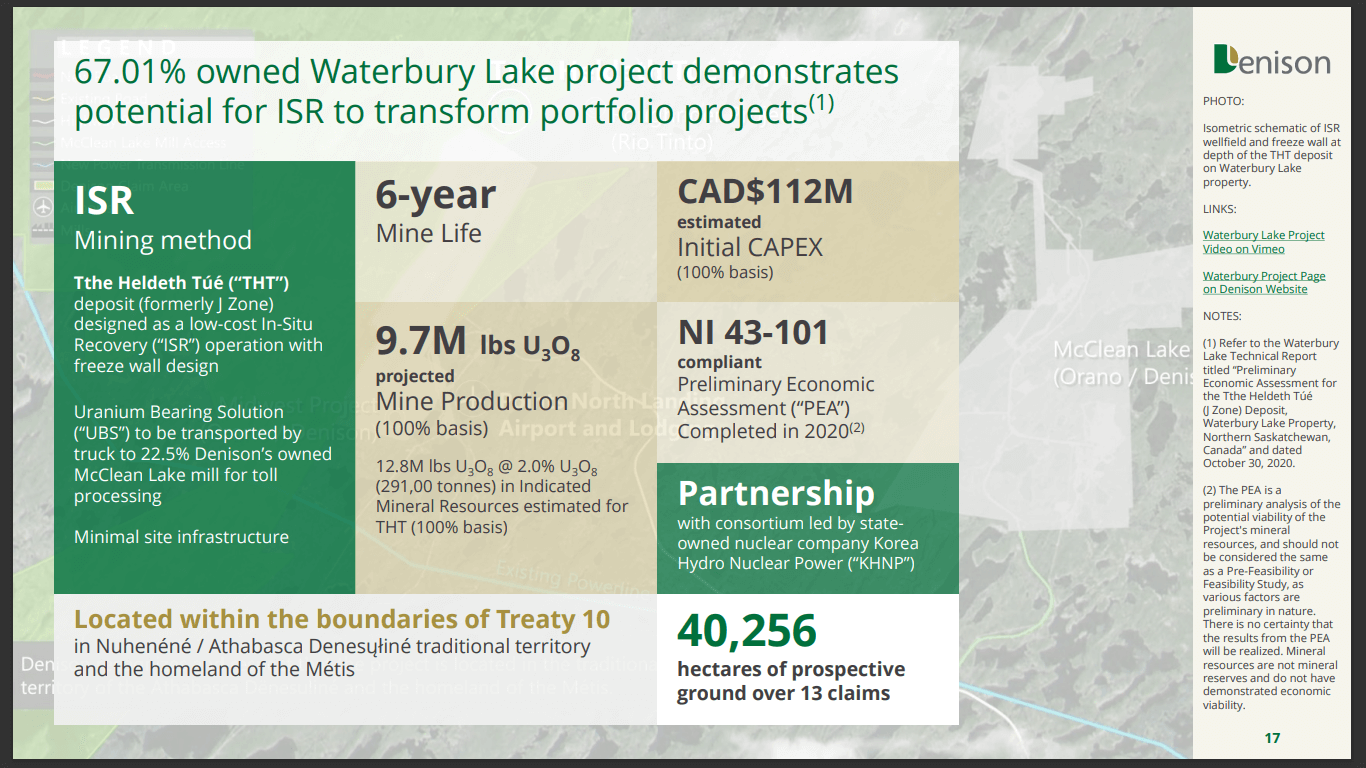

Aside from the Wheeler River project, Denison Mines Corp. also has various non-core assets such as its 22.5% interest in the McClean Lake Mill, which holds a toll mining agreement with the Cigar Lake mine, which is majority-owned by Cameco Corp.

“We have a strategic 22.5% interest in the McClean Lake mill. This is an operating licenced processing facility that right now is toll milling all of the production from the Cigar Lake mine. It has excess licence capacity today, and we’ve recently had an expansion of the tailings facility approved by our provincial and federal regulators. So, this mill is a hugely strategic asset for the region that we have a strategic interest in, and it has quite a long runway. Add on to that - and of course, it’s not easy for these analysts to cover us because we do have many pieces in our development portfolio beyond Wheeler River.”

Adjusting to the changing uranium market

The current global uranium market is according to Cates still primed for growth, however, the various geo-political factors that the uranium space faced in 2022 have had an impact on the market including supply shortages.

“We are obviously bullish on the uranium price. We do think there’s quite a tailwind for the uranium sector given the climate change narrative and global acceptance of nuclear power being necessary for climate change objectives. All that said, we are probably one of the most cautious groups in the industry. We really have focused on how we think the market might actually evolve.”

The company has been very aware of the changing uranium space, with Cates explaining that the reduced production from Kazakhstan, amongst others, has led to the rise in the uranium spot price and influenced the company’s strategy. The company believes that as the drive for a greener form of energy generation becomes more prominent, the resistance in the spot price will also be broken to above USD$ 50.

“We’ve been cognisant that the Kazaks have reduced their rate of production over the last several years, that those sources of supply would come back to the market, and that those sources of supply would likely offer a higher price, which they have - being curtailed, they did offer a higher price. But they would also create resistance, and we’ve also seen that happen where the price has moved up from USD$ 30 to USD$ 50, and now we’re seeing resistance at USD$ 50.”

Cates explains that Denison Mines Corp. has been designed to play a strategic part in the uranium supply chain with the company planning as such. He states that as large producers such as Cameco Corp. or Kazatomprom sign off-take agreements, their supply will be met. The moment when this point is reached Denison Mines Corp. will be perfectly positioned to not only supply at a competitive price but also for longer periods due to the size and lifetime of its projects.

“We’ve designed our business strategy around that happening. We’re looking to be a supplier once Cameco and Kazatomprom have met the incumbent preference of customers. At some point, their businesses will be exposed for not having the next upper asset, for not having production at a reasonable price, or anywhere in a reasonable timeline to meet even more demand. And that’s where we’re designed to slide in.”

Joining the North American Uranium ecosystem and future plans

Denison Mines Corp. has recently also started to play a role in the North American uranium market, with various utilities approaching the company. Cates explains that the company is being pursued by various utilities.

“A lot of that stuff’s coming to us rather than us chasing it. We’ve done an excellent job of having a very calm, steady story around Wheeler River amongst the future customers, so the nuclear utilities. It almost perplexes them a little bit because a number of the players out there that have very high-cost production are shopping to get that contract that gives them that margin that turns their mining project into a bit of a bond. But they need to do that because if they don’t get that certainty then they really can’t justify advancement.”

The company is following a more passive approach according to Cates, with the project economics of the company projects enabling it to justify advancement, without having to sign future off-take agreements.

“we’ve been taking much more of a passive approach because we don’t need that contract to advance the project, and what’s curious is that with that approach of us not going and banging down doors with utilities, we’re actually getting a great deal of interest from the utilities, many of which are US-based utilities or European-based utilities that are turning and looking at their book for future production and their purchase commitments, and they’re saying, ‘Where can I get more Canadian uranium?’

Denison Mines Corp. will continue to advance its projects as per the company strategy. The company holds approximately CAD$ 55 million in working capital and a cash and cash equivalent position of approximately CAD$ 225 million, placing it in a position to advance its projects.

“At the end of the third quarter, we’re on CAD$ 55 million of cash, but around CAD$ 225 million in cash and investments including that physical uranium. What we’ve done is we have actually been committing to our future spending around Wheeler River, and we’re committing to the de-risking process, completing the Feasibility Study, and now we’re actually looking forward to which other projects deserve capital based on the great success we’ve had proving up the ISR mining method.”

The strong balance sheet, high-market cap, discounted share price and strategy of the company has enabled the company to advance its projects without being dependent on the uranium market, as it grows and stabilises. Denison Mines Corp. will continue with its strategy in the future and focus on its long-term objective of being a sustainable uranium producer.

“So, with that strong balance sheet, investors can expect that we’ll continue to be dynamic, and we’ll continue to add value to the assets because we are not beholden to being in the market to be able to keep moving. We have a very stable balance sheet that allows us to focus on the long term.”

To find out more, go to the Denison Mines website

Analyst's Notes

Subscribe to Our Channel

Stay Informed