DRDGOLD (DRD) - Hybrid Model Appeals to Investors

DRDGOLD is a gold producer & gold tailings player. DRDGOLD appears to offer investors a unique value package: exposure to gold mining with less risk.

DRDGOLD (JSE/NYSE: DRD) is a conglomeration of two investment classes that seem to have a lot of momentum right now: gold mining and gold recovery from the re-treatment of surface tailings. These two facets of the company work together towards the aim of leveraging a gold price that has been more accretive than at any other time in history, briefly surpassing the US$2,000/oz mark.

Investors are attracted to the upside exposure that the best mining stories can offer up, but the risk profile can often be unsatisfactory. Moreover, when it comes to tailings, there is a reduced level of geological risk; enhanced safety by cutting out the need for mining; and many would also argue that it is greener. With this in mind, let's dig into the investment case of DRDGold.

We recently interviewed the CEO of DRDGOLD, Niël Pretorius. DRD GOLD is a South African NYSE/JSE-listed gold producer and a large player in the recovery of gold from surface tailings. The company has a network of assets spread across South Africa. In his previous interview with us, Pretorius labelled them as "unrivalled"; a bold claim, but is it one with substance?

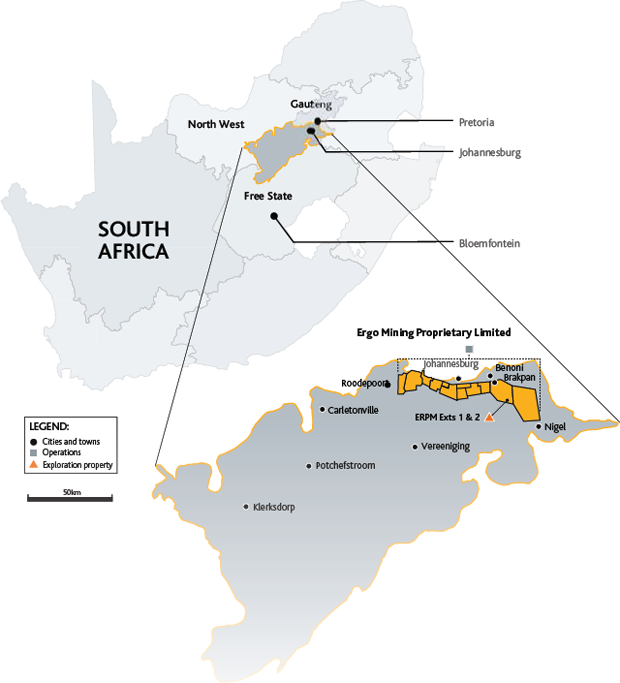

The history of DRDGOLD is lengthy. The company can trace its origin back to 1985. It is regarded by some as an important pioneer and innovator of mining methods in South Africa. Having now come full-circle, DRDGOLD is directing its focus towards the recycling and re-mining of at-surface tailings. The company's gold projects are distributed around Johannesburg and Carletonville.

DRDGOLD's share price has been accretive this year, riding up to a peak of around $17.71 before retreating back to $12 today. This performance has cemented the company as a mid-tier, unhedged gold producer that claims to be a 'world leader in surface gold tailings re-treatment.'

10 years ago, having recognised that its gold assets were towards the lower-end of the quality scale, DRDGOLD segued away from pure gold production towards tailings in an effort to maintain economic manoeuvrability. On the face of things, it seems the company has formed into a vehicle that offers unique exposure to high volumes of material and a nano-extraction methodology. The wider tailings strategy is traditional and could offer continued stable growth.

DRDGOLD'S operations are consolidated into one operating entity, Ergo Mining Proprietary Limited. We will start by looking at the company's Ergo Project. Ergo was re-established in 2007 as Ergo Mining Proprietary Limited, a JV between DRDGOLD and Mintails Limited. This JV had a clear aim: to recover and retreat c. 186Mt of surface tailings contained in the Elsburg tailings complex and the 5L/29 dump over a period of 12 years. These tailings were estimated to contain as much as 1.7Moz of gold. The company acquired part of Mintails' stake in 2008, taking over the project in its entirety in 2010.

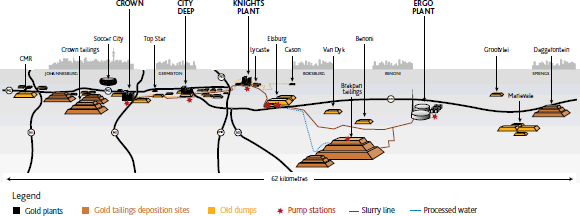

Ergo has now formed into a large, consolidated project. This is now a single re-treatment business and this synergistic approach appears to have driven down costs. The company's flagship Ergo metallurgical plant is located around 50km East of Johannesburg and has a 25.2Mt annual capacity, and the Knights Plant is situated in Germiston. Within this 62km space, DRDGOLD argues that this could be 'arguably the world's largest gold surface tailings re-treatment facility.' When the milling and pump station at former-plants Crown and City Deep are added into the mix, this becomes an operation that processes between 2.0Mt to 2.1Mt of gold-bearing tailings every month.

On August 5th, DRDGOLD announced a 9% increase in gold production for FY2020, bringing the company's total gold production to 174,385oz for the financial year ended June 30th. Having previously guided between 175,000oz and 190,000oz of gold, COVID-19 has had a noticeable impact. The company had approximately $103M in the bank having paid out cash dividends totalling $13M in June. Perhaps most importantly, the company is now free of bank debt. The company has experienced a '4-fold increase in Group operating profit,' resulting in close to $94M operating profit. Production has been steadily increasing YoY, having produced 150,423oz for the financial year in 2018.

DRDGOLD has access to between 750Mt and 900Mt of tailings that are deposited across the eastern, central and western Witwatersrand. The company treats material from a variety of sources.

There was always an active institutional element to this story. Sibanye-Stillwater, the largest individual producer of gold from South Africa and one of 10 largest gold producers globally, joined the action on 31st July 2018. The major obtained 38.05% of DRDGOLD in exchange for 250Mt of reserves from 'some of the highest grade mine dumps in Africa.' This doubled the company's gold resources and gave the company access to a 2nd project: Far West Gold Recoveries (FWGR). At the time of our last interview with DRDGOLD back in December, Sibanye-Stilwater had the option of acquiring a majority stake (51%) in DRDGOLD before February, and as expected, the company took this option up in January for roughly $60M.

Sibanye-Stilwater has stated that it is buying into the the phase 2 expansion of DRDGOLD's other project, FWGR. Project. It has a 20-year life-of-mine and is a hydraulic mining operation to recover gold from tailings. Options such as the installation of a new re-treatment plant and tailings storage facility to exploit a larger, regional mineral resource have been mooted. Roughly $2M has been spent on the project already. It was declared commercial on April 1st and produced just over 20,000oz of gold in phase 1 of development.

We look forward to seeing exactly what DRDGOLD can accomplish at FWGR and if it can continue to produce results from its Ergo project. What do you think about all of this?

Analyst's Notes

Subscribe to Our Channel

Stay Informed