Energy Fuels: $35.7M Uranium Revenue as ASM Acquisition Nears Close

Energy Fuels reported a $10.8M Q1 2026 net loss, $35.7M in uranium revenues, and a $1.9B NPV rare earth feasibility study ahead of the ASM acquisition closing.

- Energy Fuels reported a first-quarter 2026 net loss of $10.8 million, or $0.04 per share, narrowing from a $26.3 million net loss in the first quarter of 2025, supported by $35.7 million in uranium revenue from 510,000 pounds of uranium oxide sold at $70.04 per pound.

- Liquidity at quarter-end stood at $956.6 million, comprising $108.4 million in cash and cash equivalents and $802.2 million in marketable securities.

- The White Mesa Mill in Utah produced 790,000 pounds of finished uranium oxide in the first quarter of 2026, reaching the 1 million pound milestone in April, with full-year production guidance unchanged at 1.5 million to 2.5 million pounds.

- The Bankable Feasibility Study (FS) for the Phase 2 rare earth element expansion at the White Mesa Mill outlined $410 million in capital expenditure (capex), a net present value at an 8% discount rate (NPV8%) of $1.9 billion, an internal rate of return (IRR) of 33%, and average annual earnings before interest, taxes, depreciation, and amortisation (EBITDA) of $311 million for the first 15 years of operation.

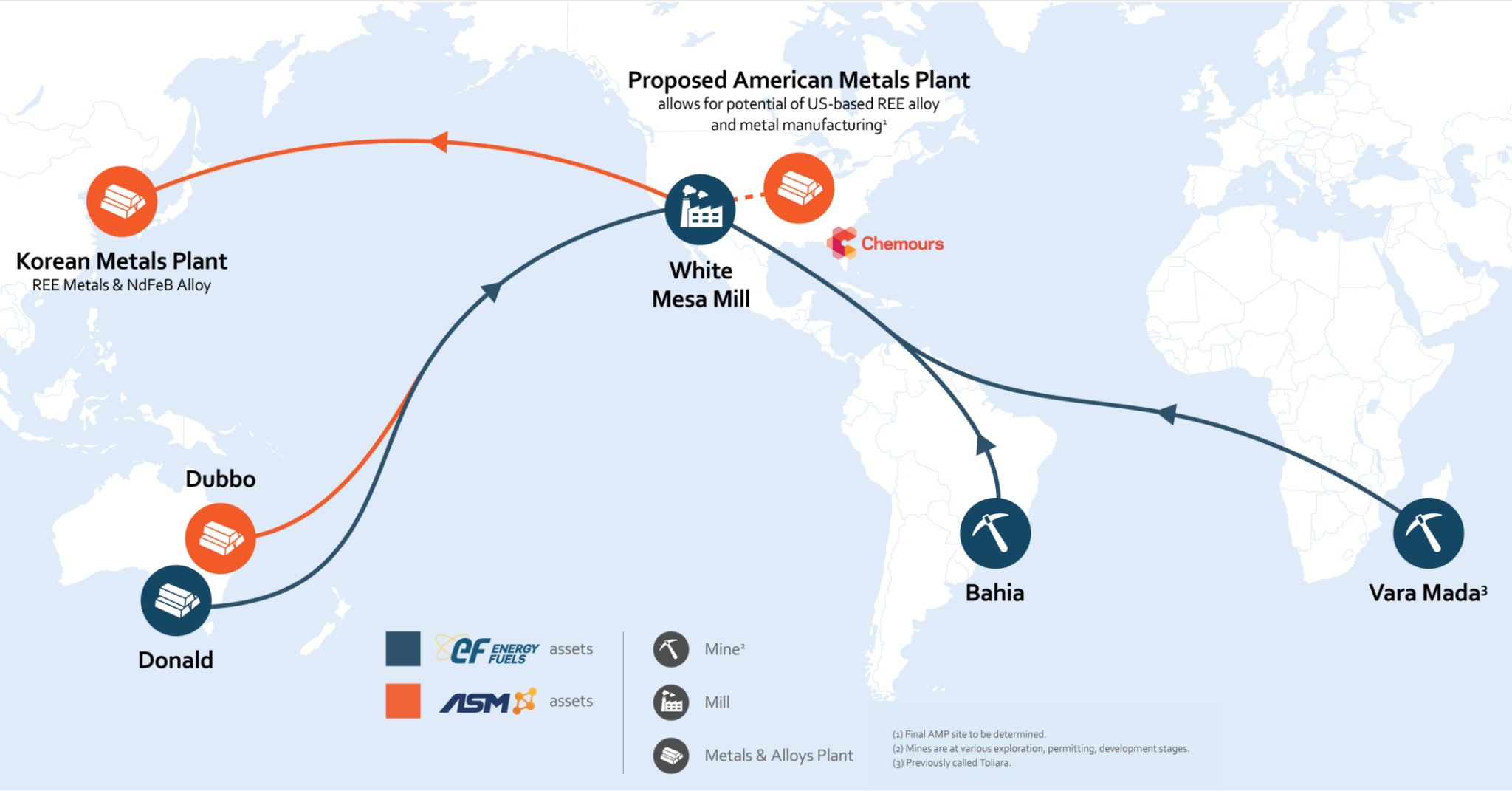

- The pending acquisition of Australian Strategic Materials Limited, anticipated to close as early as July 2026, would add an operating metals-and-alloys plant in South Korea and a construction-ready rare-earth development project in New South Wales, extending Energy Fuels' supply chain from monazite mining through to neodymium-iron-boron alloy production.

What Happened

Energy Fuels Inc. (NYSE: UUUU | TSX: EFR) reported a net loss of $10.8 million, or $0.04 per share, for the first quarter ended March 31, 2026 - down from a $26.3 million net loss, or $0.13 per share, in the same period of 2025. Sales of 510,000 pounds of uranium oxide at a weighted average realised price of $70.04 per pound generated $35.7 million in revenue. The company produced $8.3 million in operating cash flows, compared with $18.8 million used in operating activities in the first quarter of 2025.

Liquidity at quarter-end stood at $956.6 million, comprising $108.4 million in cash and cash equivalents and $802.2 million in marketable securities consisting primarily of short-term interest-bearing instruments and uranium equities.

Uranium: Cash Flow Engine

Mining operations at the Pinyon Plain, La Sal, and Pandora mines produced 425,000 pounds of contained uranium oxide during the quarter, with the White Mesa Mill in Blanding, Utah, processing 790,000 finished pounds. The company reached the 1-million-pound production milestone in April 2026. The weighted average cost of finished uranium oxide inventory declined approximately 16% from end-2025 to roughly $36.00 per pound, with costs to mine, transport, and process Pinyon Plain ore positioned at $23.00 to $30.00 per pound.

Full-year 2026 production guidance remains at 1.5 million to 2.5 million pounds of processed uranium oxide, with sales targeting 1.5 million to 2 million pounds. The company holds 6 long-term contracts with US nuclear utilities covering deliveries from 2026 through 2032. The Pinyon Plain mine in Arizona mined ore averaging 1.12% euranium oxide during the quarter, with grades expected to rise as mining advances into higher-grade zones.

Rare Earth Platform: Processing, Metals & Feedstock

The White Mesa Mill is the only US facility with commercial capacity to process monazite concentrate into separated rare earth element (REE) oxides, making it the sole domestic processing node for a feedstock pipeline contracted by the company at 40,900 tonnes per annum across 4 projects. The existing Phase 1 circuit can process up to 10,000 metric tonnes of monazite per annum and produce up to 1,000 metric tonnes of neodymium-praseodymium (NdPr) oxide per annum. During the first quarter, the company announced pilot-scale production of terbium oxide at 99.9% purity, meeting the specifications of permanent magnet manufacturers.

A completed Bankable Feasibility Study (FS) for the Phase 2 expansion at the Mill outlined capital expenditure (capex) of $410 million to increase combined NdPr production capacity to 6,229 tonnes per annum, with commissioning targeted for 2028 and 2029. The study returned a net present value at an 8% discount rate (NPV8%) of $1.9 billion, an internal rate of return (IRR) of 33%, and average annual earnings before interest, taxes, depreciation, and amortisation (EBITDA) of $311 million for the first 15 years of operation.

The pending acquisition of Australian Strategic Materials Limited (ASM), announced in January 2026, adds the operating Korean Metals Plant in Ochang, South Korea - currently producing approximately 1.3 thousand tonnes per annum of neodymium-iron-boron (NdFeB) alloy with expansion plans to approximately 3.6 thousand tonnes per annum - and a planned American Metals Plant targeting an initial capacity of approximately 2 thousand tonnes per annum of alloy. The transaction also includes the Dubbo Project in New South Wales, a construction-ready rare earth development asset with a 42-year modelled mine life. The ASM acquisition remains subject to court, regulatory, and shareholder approvals and is anticipated to close as early as July 2026.

Feedstock Pipeline

Energy Fuels has contracted approximately 40,900 tonnes per annum of monazite across 4 projects to supply the White Mesa Mill's REE circuits. The Donald Project in Australia, a joint venture with Astron Corporation in which Energy Fuels is earning a 49% interest and is entitled to 100% of monazite produced, is targeting deliveries to the Mill by late 2027. The Vara Mada Project in Madagascar has an FS NPV of $1.8 billion at a 10% discount rate over a 38-year mine life, with development pending a final investment decision (FID) and a fiscal agreement with the government of Madagascar.

The Bahia Project in Brazil is currently under active drilling, with a resource estimate targeting completion by late 2026 and a potential monazite supply of 3,000 to 5,000 tonnes per annum. An existing offtake agreement with Chemours contributes a further 800 tonnes per annum. Combined, the 4 projects contain an estimated 5,381 tonnes per annum of NdPr, 260 tonnes per annum of dysprosium, and 64 tonnes per annum of terbium. The ASM acquisition supports Energy Fuels' strategy of building an integrated rare earth supply chain spanning feedstock, processing, and alloy production.

Former Energy Fuels Chief Executive Officer Mark Chalmers discussed the challenge of competing with Chinese producers on cost and scale:

“To really compete with China, you have to have all those steps. You can't be missing a step in the middle of it, so we've been very focused on the integration at least through alloys, and we've got the hydromet step skills. We've got the heavy mineral sand skills, and then the mining skills and then the metal alloy skills. We've done a lot, and I think what people are seeing is that we've got this critical mass with those steps, and they don't just happen overnight, so you really have to acquire those skills, you can't just grow them organically, because it'll take years”

Medical Isotopes

The White Mesa Mill is targeting commercial-scale production of radium-226 and radium-228 for use in targeted alpha therapy cancer treatments as early as 2028, subject to successful production of research-scale quantities and required regulatory approvals. Pilot-scale separation of both isotopes is currently under research and development at the Mill.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed