Energy Fuels Bets Big on Becoming the West's Critical Materials Powerhouse, But Execution Risk Looms Large

Energy Fuels is building the US's only mine-to-metal rare earth supply chain, backed by the country's sole uranium mill. Execution risk is real, but so is the opportunity.

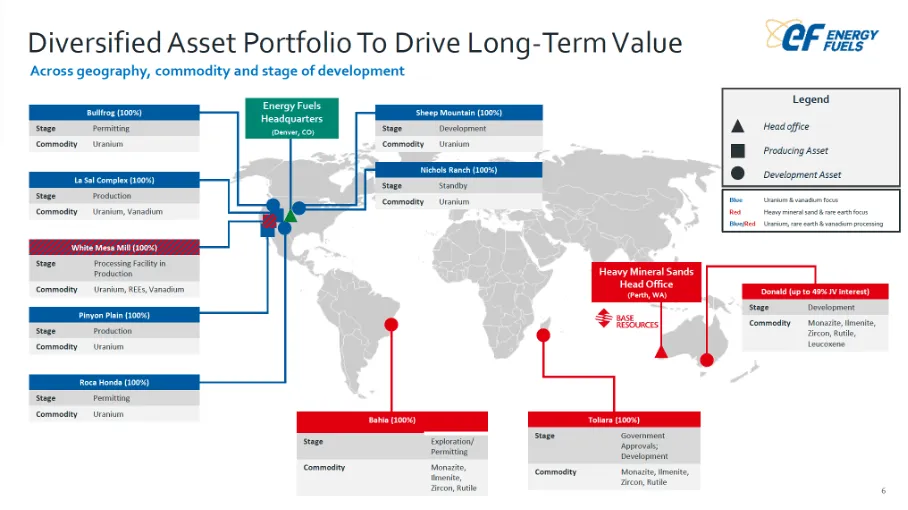

- Energy Fuels is transforming from a uranium-only producer into a diversified critical materials company, with the White Mesa Mill in Utah serving as the only US facility permitted to process monazite ore into separated rare earth oxides

- The Mill is already producing neodymium-praseodymium (NdPr) oxide for electric vehicle and defence magnet applications, with a Phase 1 expansion targeting commercial heavy rare earth oxide production by mid-2027 and a larger Phase 2 expansion planned thereafter

- A January 2026 acquisition of Australian Strategic Materials (ASM) adds a producing metals and alloys plant in South Korea, moving Energy Fuels up the rare earth value chain from oxide producer toward alloy supplier

- Uranium production exceeded one million pounds in 2025, underpinned by six long-term contracts with US nuclear utilities through 2032, with the uranium oxide spot price averaging US$73.54 per pound in 2025 while the long-term contract price hit a 14-year high of US$86.50 per pound in December 2025

- A $700 million convertible notes offering in October 2025, oversubscribed by more than seven times, provides capital for project development, though the gap between current cash generation and total project capital requirements remains a key variable to track

Energy Fuels has spent the past several years building something that does not yet exist anywhere else in the Western world: a single company that can take uranium-bearing ore out of the ground, process it into nuclear fuel, and at the same time extract rare earth materials from the same minerals, separate those materials into individual oxides, and turn them into the metal alloys that go into electric vehicle motors, military jets, and wind turbines.

That ambition is laid out in detail in the company's March 2026 corporate presentation. The asset base now stretches from Utah to South Korea, with mining development projects in Australia, Madagascar, and Brazil. The strategy is coherent and the market timing looks favourable. The question is whether a company of this size can execute across this many moving parts simultaneously.

The White Mesa Mill: A Regulatory Asset

The starting point for understanding Energy Fuels' thesis is the White Mesa Mill. Its significance lies not merely in what it does today, processing uranium ore, but in what cannot easily be replicated. The facility is the only US site licensed to process monazite for the production of separated rare earth oxides. That regulatory status, built over 45 years of operation, represents a barrier to entry that no amount of capital can quickly overcome.

This matters because monazite, a phosphate mineral that occurs as a byproduct of HMS mining, is a superior feedstock for rare earth production. It carries high concentrations of neodymium-praseodymium (NdPr), the oxides critical to permanent magnets used in electric vehicles, wind turbines, and defence systems. It also contains elevated levels of dysprosium (Dy) and terbium (Tb), the so-called heavy REEs that command prices dramatically above their lighter counterparts.

The company's existing Phase 1 capacity at the Mill can process up to 10,000 metric tonnes per annum (tpa) of monazite concentrate and produce up to 1,000 tpa of NdPr oxide. That capacity is already in place and operating. A planned Phase 1 expansion, targeting commercial production of heavy REE oxides by mid-2027, is installing the infrastructure for dysprosium, terbium, samarium (Sm), europium (Eu), and gadolinium (Gd) oxide production.

Phase 2, a more transformative expansion, would bring total monazite processing capacity to 60,000 tpa and NdPr output to 6,000 tpa, alongside approximately 300 tpa of dysprosium and terbium oxides combined. At current market prices, NdPr at roughly $135,000 per tonne, dysprosium at over $1.1 million per tonne, and terbium at approximately $4.5 million per tonne, the revenue potential is substantial. The company projects nearly $1.2 billion in annual revenue at Phase 2 volumes and current prices.

That figure warrants scrutiny. REE prices are notoriously volatile, and the premium to Chinese benchmark pricing for Western-sourced material, cited at 443% for dysprosium and 401% for terbium, reflects current supply anxiety rather than a guaranteed structural premium. Whether those spreads hold through a multi-year construction and commissioning cycle is an open question.

The Monazite Supply Chain: Ambition Across Three Continents

The REE processing story is only as good as the monazite supply that feeds it. Energy Fuels has been assembling a portfolio of projects at various stages of development to address this.

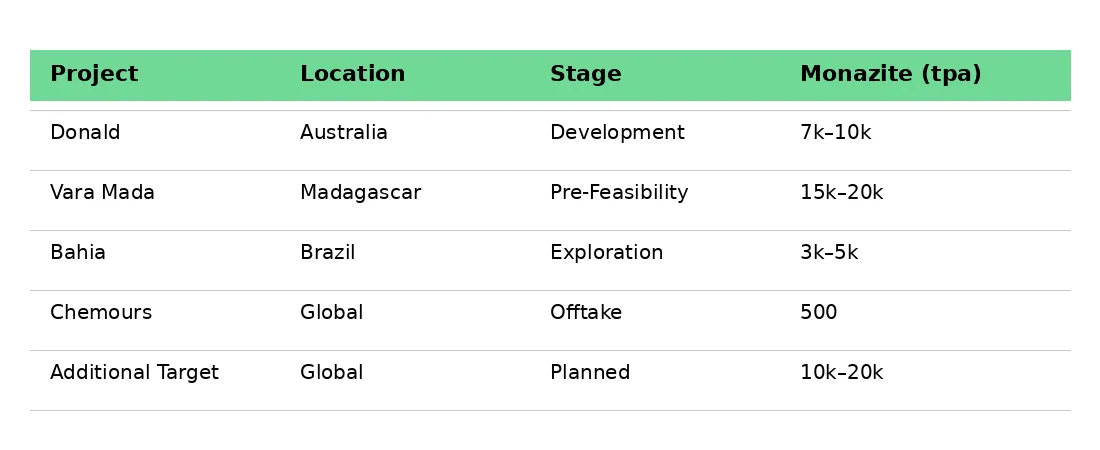

The Donald Project in Victoria, Australia, a joint venture (JV) with Astron Corporation in which Energy Fuels is earning a 49% JV interest, is the most advanced. Under the JV structure, Energy Fuels receives 100% of the monazite produced. The project has received conditional development financing support of A$80 million from Export Finance Australia, with total project funding estimated at approximately A$520 million (roughly US$340 million). A final investment decision (FID) was expected as early as the First Quarter of 2026, with monazite deliveries to the White Mesa Mill potentially beginning by late 2027.

The Vara Mada Project in Madagascar, formerly known as Toliara, is the larger and more economically significant prospect. The company's pre-feasibility work suggests a post-tax net present value (NPV) of $1.8 billion at a 10% discount rate, a 24.9% internal rate of return (IRR), and expected earnings before interest, tax, depreciation and amortisation (EBITDA) of $500 million following ramp-up, figures that, if achieved, would dwarf the current market capitalisation. Stage 1 capital expenditure (CAPEX) is estimated at $769 million. The critical caveat is that the project's timeline remains subject to Madagascan government approvals that have not yet been secured. That political and regulatory risk is non-trivial.

The Bahia Project in Brazil is at an earlier stage, with sonic drilling underway and a resource estimate expected to be completed in 2026. If exploration results hold, the project could eventually supply 3,000 to 5,000 tpa of monazite to the Mill.

In aggregate, Energy Fuels has identified a potential monazite supply of nearly 41,000 tpa from its portfolio across Donald, Vara Mada, Bahia, and an existing offtake agreement with Chemours for 500 tpa. The company acknowledges it is seeking an additional 10,000 to 20,000 tpa from other sources or purchased feedstock to fill Phase 2 capacity.

The ASM Acquisition: Closing the Loop from Ore to Alloy

The January 2026 announcement of the proposed acquisition of ASM adds the final link in the chain that Energy Fuels has been building. President and Chief Executive Officer of Energy Fuels, Mark Chalmers, speaking in a recent Crux Investor interview, explained the strategic rationale directly:

"We've been talking about integration in the rare earth cycle. The Chinese have integration from mining right on through to electric vehicles and they look at margins from the beginning to the end, not every single step. We identified some time ago that we wanted to have the metals and alloys capability, which are very, very in short supply globally."

ASM operates the Korean Metals Plant in Ochang, South Korea, currently producing neodymium iron boron (NdFeB) alloy at approximately 1,300 tpa, with expansion plans to 3,600 tpa in Phase II and 5,600 tpa in Phase III. Chalmers noted that the Korean plant's current plans would accommodate roughly 60% of Energy Fuels' Phase 2 processing capacity in terms of metals and alloys conversion, with the modular design allowing further expansion over time. The acquisition also brings the Dubbo Project in New South Wales, a construction-ready REE development with a 42-year mine life, and plans for an American Metals Plant at a US location to be determined.

Chalmers framed the acquisition's broader significance in terms of market access and customer relationships:

"A lot of people aren't looking for oxides. They want the alloys. It gets us a step closer to the magnet producers."

On the question of why build rather than buy, Chalmers was direct about the time factor:

"The world is wanting to wean dependence from China and five years from now, eight years from now is a long time. Speed is important. Proven capability is important. Know-how is important."

If completed, with the closing scheduled for mid-2026, the combined entity would span the full value chain from HMS mining through REE oxide separation, metal and alloy production, and ultimately supply to permanent magnet manufacturers and original equipment manufacturers. The company's presentation explicitly frames this as a "100% US controlled supply chain," though the Korean plant and Australian assets complicate that characterisation somewhat.

The strategic logic is sound. As Chalmers put it, fragmentation across the supply chain destroys economics:

"If you get two or three groups trying to make their 20% to 25% margin in the middle of all these steps, the time from the mining to the electric vehicle, it's too big of a margin, it's never going to be economic."

Energy Fuels believes vertical integration can improve its overall margins by up to 20%, which Chalmers described as material over the long term.

The execution risk, however, is correspondingly elevated. Managing assets across five continents, multiple regulatory jurisdictions, and several commodity streams simultaneously is a materially different challenge from running a uranium mill in Utah. Chalmers acknowledged this directly, noting that integrating two separately operating companies involves "a huge number of things" spanning people, systems, accounting, and reporting across multiple listed entities. He added that the company's prior experience integrating Base Resources, another Australian Securities Exchange-listed Perth-based company, had provided useful lessons for approaching the ASM transaction more efficiently.

Uranium Remains the Revenue Foundation

Amid the REE ambitions, it is worth noting that uranium continues to underpin the company's financial position. Energy Fuels produced over one million pounds of uranium oxide (U3O8) in 2025 and is targeting 1.5 to 2.5 million pounds in 2026. The Pinyon Plain Mine in Arizona, potentially the highest-grade uranium mine in US history having mined ore at 1.62% equivalent uranium oxide in 2025, is expected to contribute over two million pounds in 2026 alone, at costs of approximately $23 to $30 per pound.

The company holds six long-term contracts with US nuclear utilities, with deliveries contracted through 2032. In 2025, it sold 650,000 pounds at $74.20 per pound. The 2026 guidance calls for selling 1.5 to 2.0 million pounds through a mix of contract and spot sales.

The uranium business provides two things the REE ambitions currently cannot: revenue and cash flow. The uranium oxide spot price averaged US$73.54 per pound in 2025, compared with approximately US$84 to US$85 per pound in 2024, representing a decline of roughly 13% year-on-year, according to Cameco's composite of UxC and TradeTech month-end data. The long-term uranium price told a different story, however, strengthening throughout 2025 and peaking in December at a 14-year high of US$86.50 per pound, also per Cameco's data aggregating UxC and TradeTech. That divergence between a soft spot price and a firming long-term price is an important nuance for investors: Energy Fuels' contract portfolio, with fixed and market price components that escalate with inflation and include price floors and ceilings, is structured to capture more of the long-term price signal than the spot market alone would suggest.

With the company reporting a net loss of $86.1 million in 2025 and a balance sheet carrying $927.4 million in working capital, anchored by $797.1 million in marketable securities, Energy Fuels is capitalised to pursue its development programme. A $700 million convertible senior notes offering in October 2025, oversubscribed by more than seven times at a 0.75% annual coupon rate, provided additional runway.

That said, the gap between current cash generation and the capital demands of Phase 2 at White Mesa, the Donald Project, and the ASM integration is significant. The company will need uranium prices to hold, REE prices to remain elevated, and project execution to proceed broadly on schedule, a conjunction of favourable conditions that is historically uncommon in mining.

What to Watch Next

The next 12 to 24 months will determine whether Energy Fuels' integrated strategy holds together in practice. The following milestones are the ones most likely to move the investment case in either direction.

ASM acquisition closing (mid-2026): Completion and early integration of the Korean Metals Plant will be the first test of the mine-to-metal thesis in practice. Chalmers indicated he is "very confident" the deal will close towards the end of June 2026, subject to shareholder votes and court approvals.

Donald Project final investment decision: A formal FID, alongside confirmation of Export Finance Australia funding, would validate the monazite supply chain and provide a concrete commissioning timeline. A decision was expected as early as the First Quarter of 2026.

Vara Mada government approvals: Progress, or lack thereof, on Madagascan fiscal stability negotiations will be a material signal for the project's viability and timeline. This remains the single largest outstanding risk in the company's development pipeline.

White Mesa Phase 1 expansion commissioning: The installation of heavy REE separation capacity at the Mill, targeting mid-2027, represents the next meaningful operational step in the processing upgrade.

Uranium sales performance: Given that uranium revenues currently fund the company's operations, quarterly sales figures and contract pricing will remain closely watched indicators of financial health. With spot prices moving back above US$100 per pound in early 2026, according to Sprott Asset Management, the pricing environment entering the year is more supportive than the 2025 annual average implied.

Phase 2 engineering studies: Any formal scoping study or pre-feasibility study on the Phase 2 REE expansion will provide capital cost estimates that the market will scrutinise against the company's revenue projections.

Energy Fuels has built something genuinely rare: a company controlling the only processing infrastructure in the US capable of producing separated heavy rare earth oxides, backed by a uranium business with real contracts and real cash flow. The strategic logic is strong. The asset base is unusual. The execution challenge is equally real. The milestones above are the ones that will show whether the strategy is translating into progress.

Analyst's Notes

Subscribe to Our Channel

Stay Informed