Engineering, Permitting and Financing Progress Drive Troilus Mining Toward Construction

Troilus Mining nears full financing and permitting for its Quebec copper-gold mine, with basic engineering complete and construction mobilisation targeted for early 2027.

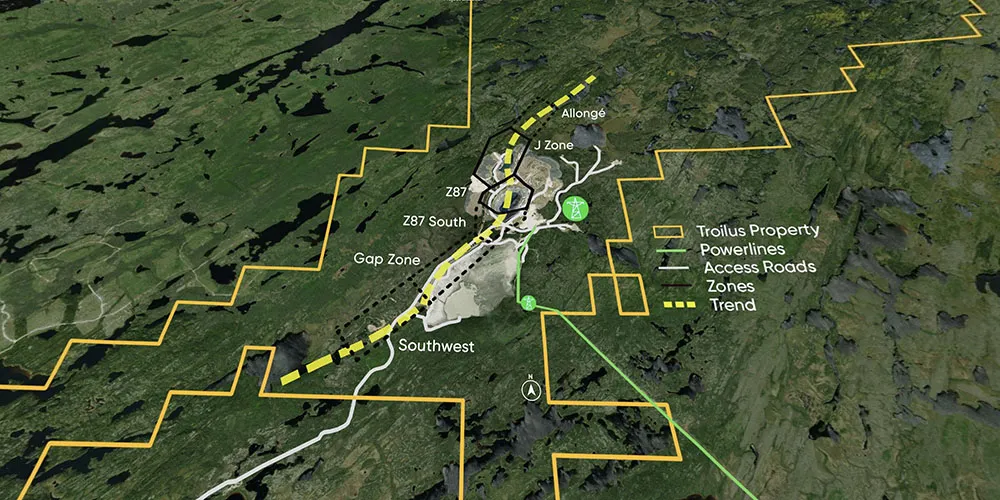

Troilus Mining is entering a decisive phase in the development of its flagship copper-gold project in the Chibougamau region of central Quebec. CEO Justin Reid outlined the status of the company's engineering programme, financing structure, permitting process, and early site mobilisation, painting a picture of a development-stage company that is systematically closing the gap between feasibility and full construction.

With gold above $4,500 per ounce, copper holding near $5 per pound, and institutional and sovereign-backed debt providers actively advancing due diligence, Troilus finds itself in a stronger position than at any point in its development history. What remains are the final procedural steps before ground is broken on what management expects will be one of the largest new mines in Canada.

Engineering: From Feasibility to Execution-Ready

One of the most significant milestones Troilus has reached is the completion of basic engineering, a phase that Reid describes as roughly three times more costly than a feasibility study, involving approximately 100,000 man-hours of work at a cost of around $15 million. This phase reduces the capital cost variance from plus-or-minus 35% at feasibility stage to plus-or-minus 10%, producing what engineers call a control budget.

The company has now moved into detailed engineering, which carries an $80 million budget allocation and will involve approximately 400,000 man-hours of work. This phase is being executed by Troilus's owner's team, EPCM lead BBA of Montreal and construction contractor EBC. Over 100 engineers are currently working full-time across these teams.

A parallel geotechnical programme is underway to fill data gaps in areas that carry the most execution risk including a diversion channel that must be relocated 800 metres, foundational zones beneath the mill building, and the upper slopes of the initial pit, where steeper walls would lower the stripping ratio and reduce operating costs.

Financing: Debt Structure in Place, Streaming Deal Imminent

Troilus has assembled a debt facility totalling $1 billion up from an earlier $700 million commitment. The facility is structured through eleven counterparties, with lead arrangers including Societe Generale, KfW IPEX-Bank, and Export Development Canada. Crucially, the facility is backstopped by European export credit agencies, which Reid says provides both lower-cost and more flexible financing than conventional project finance.

Due diligence is described as substantially complete, with documentation now underway across the eleven-party group. Credit committee approval is expected in the near term. The $172.5 million equity raise completed in November is deployed and covering all current expenditure. What remains is the streaming component, which Reid suggests will be smaller in scope than originally anticipated, owing to the improved economics at current gold, silver, and copper prices.

"The value of potential streams to us and to our shareholders is significantly better than it was even six months ago"

Permitting, Construction Permits Expected by Year-End

Troilus submitted its Environmental and Social Impact Assessment to federal regulators in June of the previous year. The first round of regulatory questions has been received, answered, and resubmitted. Reid characterises the process as orderly, noting that the company anticipated the nature of many questions, and had detailed engineering answers ready before they arrived. Where developers who begin permitting at the prefeasibility stage can take months to respond to technical regulatory questions, Troilus is able to respond in weeks because its engineering is sufficiently advanced to provide fully quantified, vendor-confirmed answers.

The company holds active mining leases from a prior fourteen-year operation on the same brownfield site, which simplifies the regulatory pathway. The Quebec government is also described as a significant shareholder, adding a degree of political alignment that Reid views as favourable to the ultimate outcome.

The construction permit is expected by the end of 2026, consistent with the company's target to mobilise full construction in Q1 2027.

Interview with Justin Reid, CEO of Troilus Mining Corp.

Compressing the Critical Path

Rather than waiting passively for the construction permit, Troilus is aggressively advancing pre-construction work under existing exploration and alternative permits. The camp is being expanded from 100 to 250 people, with a 350-person kitchen and a $5 million septic system being installed in anticipation of a 1,000-person peak construction workforce.

"We're going to be a fully operating pre-development advanced exploration site very shortly," Reid noted. "Those people are never going to leave. They're just going to stay for the next three years."

Three major road relocations are underway, including the main site entrance. Deforestation permits have been granted. Three mobile crushers are being brought on site to process waste rock and bulk sample material into aggregate, gravel, and sand for road bases, foundations, and concrete requirements during construction.

Early earthworks are being contracted to local suppliers from the Chibougamau, Chapais, and Mistissini communities, both to deliver immediate economic benefits to regional and First Nations partners and to identify skilled local workers who will continue into the full construction phase.

Drilling for Grade Optimisation

Troilus has announced a 40,000-metre drill programme for 2026. Reid was explicit that the objective is not to expand the existing 13-million-ounce gold-equivalent resource base but to optimise grade and reduce the stripping ratio in the early years of mine life which will determine the pace of capital payback.

Higher-grade zones immediately outside current reserve shells are being targeted. Reid confirmed that none of this drilling will affect the submitted mine plan or the permitting timeline, as the exploration targets lie outside the scope of the regulatory submission.

The Investment Thesis for Troilus Mining

- Near-term production de-risked by brownfield status. The Troilus project is being built on a site that operated for fourteen years, with active mining leases, existing infrastructure with a replacement value estimated at $650 million, and a well-understood geological and geotechnical environment.

- Financing is effectively complete. A $1 billion debt facility is in documentation, backstopped by European export credit agencies. A $172.5 million no-warrant equity raise is deployed. A streaming deal at favourable terms is expected imminently.

- Engineering is ahead of schedule. Basic engineering is complete and detailed engineering is underway. The company expects to be near 100% detailed engineering complete by the time ground is broken, an unusual level of execution certainty for a project of this scale.

- Commodity prices provide exceptional project economics. The feasibility study was completed at $1,975 gold. At $4,500 gold, the project economics are described as exceptional, with lenders modelling at $3,000 and still generating robust returns. Any investor gaining exposure at current valuations is acquiring optionality on prices that substantially exceed conservative lending assumptions.

- Grade optimisation drilling could materially improve early cash flows. A 20–30% grade improvement in Year 1 or a 20% reduction in the stripping ratio would have a significant compounding effect on capital payback pace, which is already expected to be within two and a half years at current prices.

- Scarcity value among quality near-term developers. Troilus represents one of a small number of development-stage copper-gold projects globally with fully engineered plans, institutional backing, brownfield permitting advantages, and sovereign debt support. Capital is abundant and chasing a very small pool of credible near-term projects.

- Actionable consideration. Investors with a two-to-three-year horizon should note that the financing announcement and construction decision are expected within months, not years. Historically, such catalysts have driven meaningful re-ratings in developer valuations. The current pullback in the broader gold equity market may represent an entry point ahead of these milestones.

Macro Thematic Analysis: Gold, Copper, and the Case for Advanced Developers

The macro backdrop for large-scale copper-gold development projects has rarely been more constructive or more complex. Gold has sustained prices above $4,000 per ounce for an extended period, driven by persistent central bank buying from sovereign institutions seeking to reduce US dollar exposure, sticky inflation that has kept real rates below levels historically associated with gold weakness, and geopolitical fragmentation that is elevating the metal's role as a reserve asset. Copper, meanwhile, is being shaped by two structural forces operating simultaneously: the clean energy transition's insatiable demand for electrification infrastructure and the multi-decade underinvestment in new mine development that has left the global supply pipeline structurally deficient.

Against this backdrop, the scarcity of advanced development projects with completed feasibility studies, permitted or near-permitted status, and credible financing structures has become a defining investment theme. The barriers to bringing a new large-scale mine into production have increased substantially over the past decade: permitting timelines have lengthened in most jurisdictions, capital costs have inflated sharply, labour availability has tightened, and community and environmental consultation requirements have grown more demanding. This means that projects which have navigated these hurdles successfully command a structural scarcity premium in the capital markets, one that is not yet fully reflected in many developer valuations relative to where producers trade.

The export credit agency financing model now underpinning projects like Troilus where European and Canadian sovereign institutions backstop project debt at low cost represents a relatively new dynamic in mining finance, driven by the strategic imperative to secure critical mineral supply chains outside geopolitically contested jurisdictions. Quebec, with its stable governance, existing resource infrastructure, and direct government economic participation in mining development, is precisely the type of jurisdiction these institutions are prioritising.

As Reid put it: "If somebody said, do you want $4,000 gold for 22 years, we'd take it all day long. Everybody would."

The combination of buoyant commodity prices, sovereign financial support, and a structural deficit of quality near-term supply creates the conditions in which advanced developers with credible execution teams stand to generate exceptional returns both for their shareholders and for the institutional capital increasingly competing to finance them.

TL;DR

Troilus Mining has completed basic engineering on a billion-dollar-plus copper-gold mine in Quebec, secured $1 billion in sovereign-backed debt, deployed $175 million in equity with no warrants, and is advancing permitting toward a construction decision by end of 2026. A streaming deal is expected imminently. The company is already mobilising pre-construction activity on site. At $4,500/oz gold and $5/lb copper, the project economics substantially exceed conservative lending assumptions. The primary remaining variable is permit timing, and the company is actively working to compress that risk. For investors, the re-rating from development-stage to construction-stage company is a near-term event, not a multi-year horizon.

Frequently Asked Questions (FAQs) AI-Generated

The company is targeting full construction mobilisation in Q1 2027, contingent on receipt of the construction permit, which is expected by end of 2026. Troilus is advancing pre-construction activity under existing permits in the interim to compress the timeline to first cash flow.

Troilus has assembled a $1 billion USD project debt facility structured through eleven counterparties and backstopped by European export credit agencies. A $175 million no-warrant equity raise completed in November is fully deployed. The remaining piece is a streaming arrangement, which CEO Justin Reid has indicated is nearing finalisation on terms more favourable than originally modelled due to current commodity prices. Management has stated that every dollar of the project cost is on track to be accounted for imminently.

The Troilus site operated as a producing mine for fourteen years, leaving behind active mining leases, substantial existing infrastructure with a current replacement value estimated at $650 million USD, and a well-characterised geological and geotechnical environment. This substantially reduces both the capital cost of development and the complexity of the permitting process relative to a greenfield project.

No. Reid confirmed explicitly that the drill programme targets zones outside the scope of the submitted mine plan and regulatory application. The objective is to identify opportunities to improve head grade and reduce the stripping ratio in the early years of production — outcomes that would accelerate capital payback — without modifying the existing permit submission or construction timeline.

The feasibility study was completed at a gold price of $1,975 per ounce. Gold is currently trading above $4,500. Debt providers are understood to be modelling at approximately $3,000 per ounce for lending purposes, a price at which the project still generates robust returns. The improvement in commodity prices has also reduced the size of the streaming deal required and improved the terms available, directly benefiting shareholders.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed